OGX Group Berhad IPO's Analysis

OGX Group Berhad

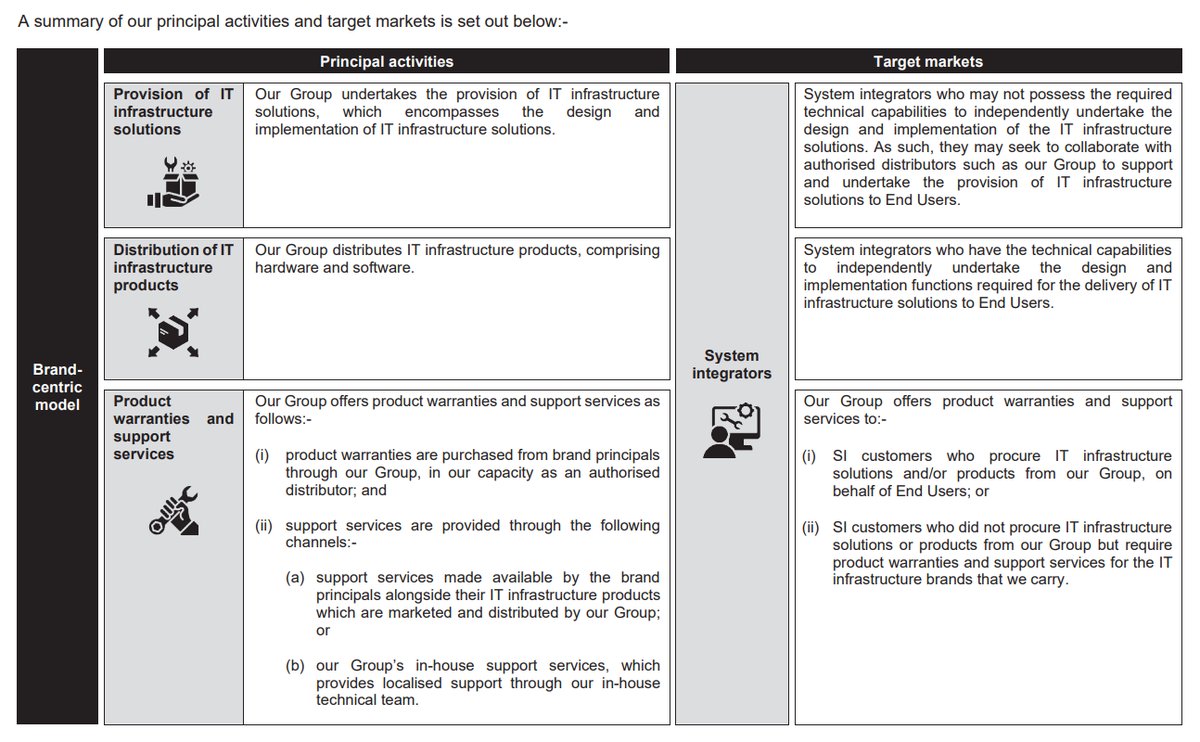

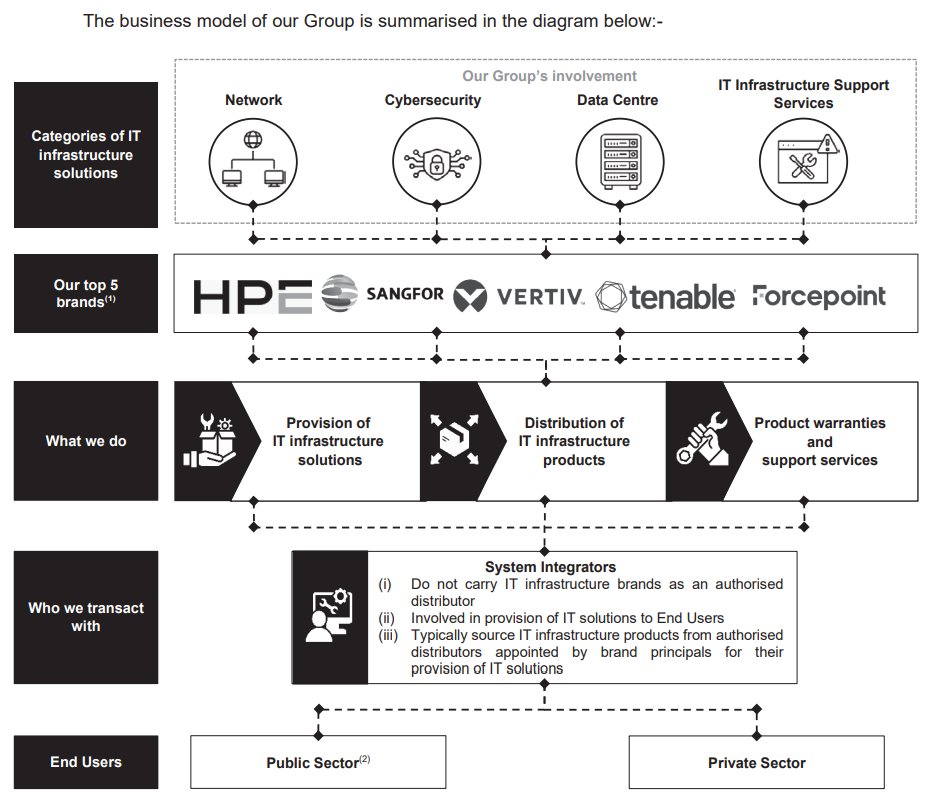

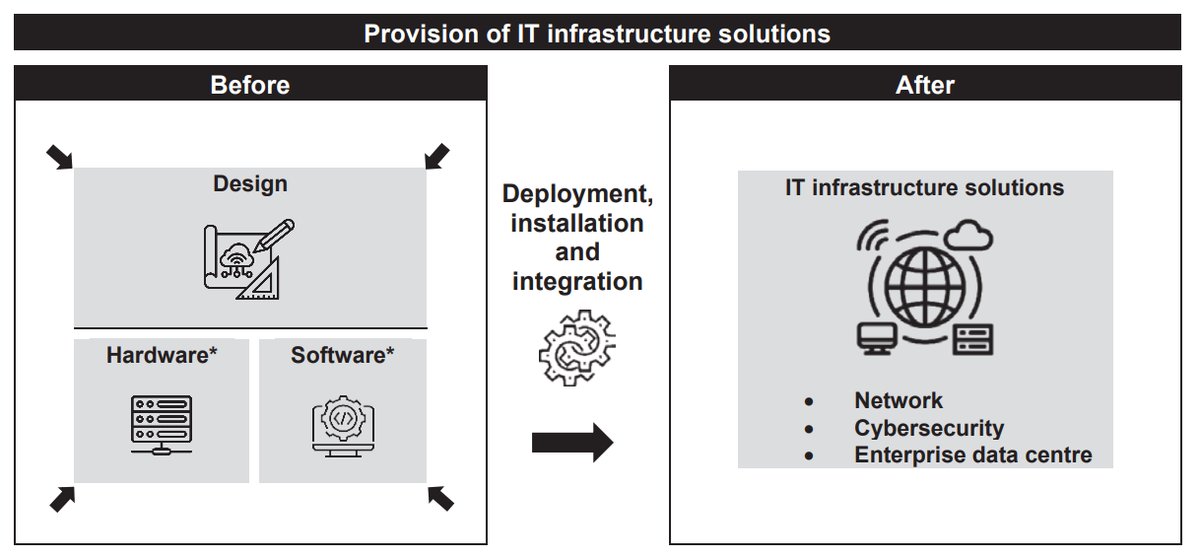

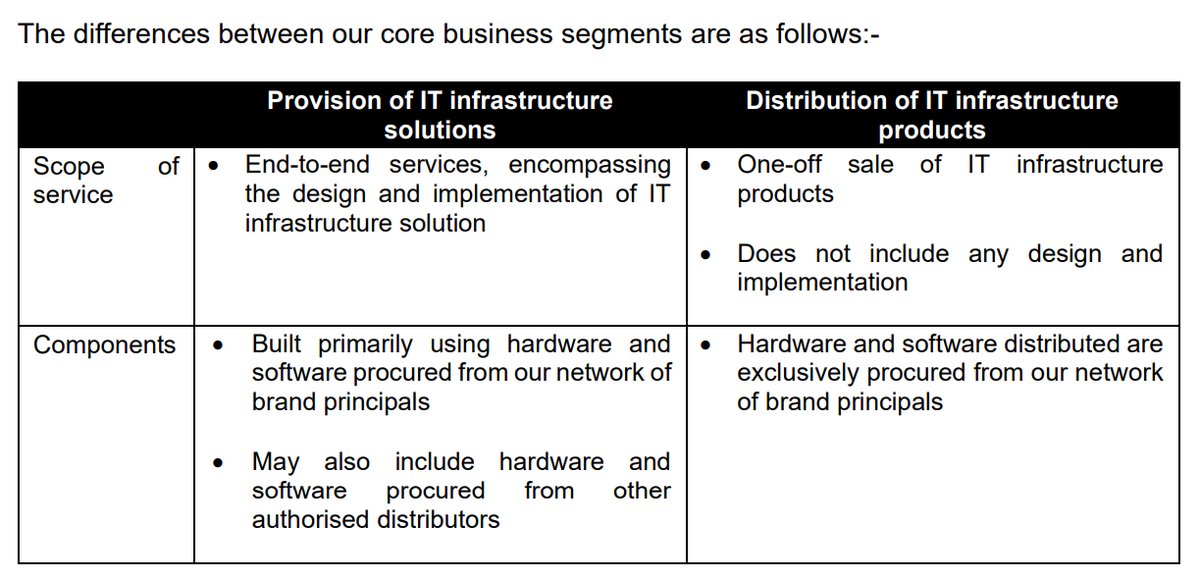

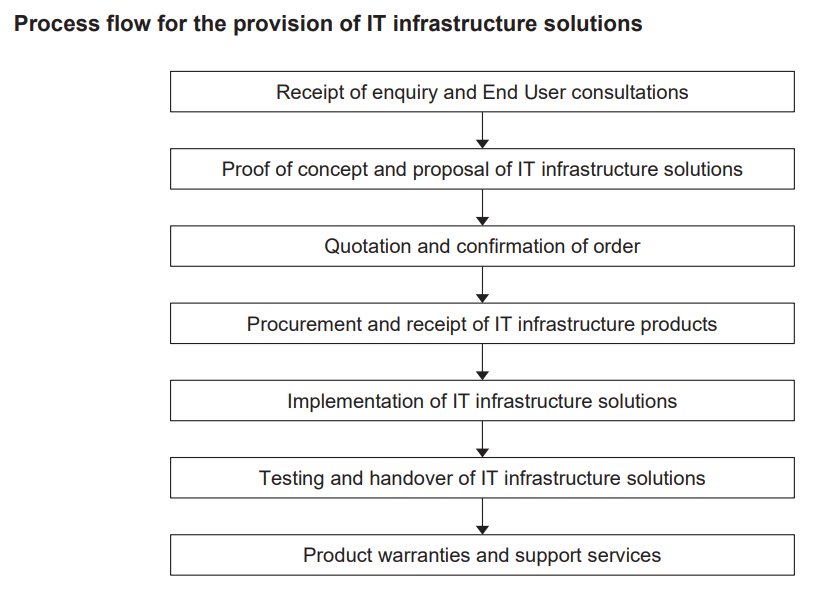

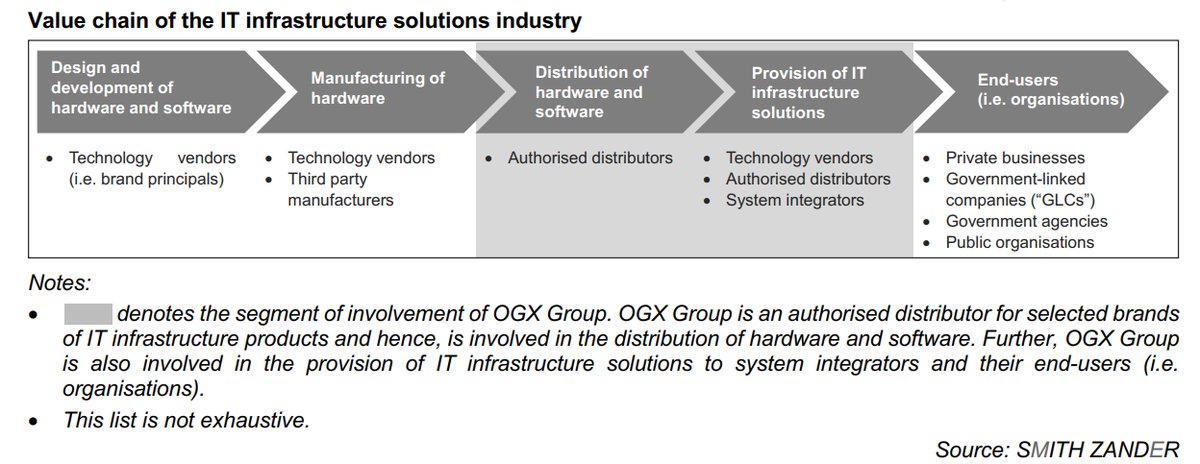

OGX Group Berhad is an IT infrastructure solutions specialist operating with a brand-centric, business-to-business (B2B) model. The Group is principally involved in providing comprehensive IT infrastructure solutions, which includes the design and implementation of network solutions, cybersecurity solutions, and enterprise data centre solutions. Additionally, the company engages in the distribution of IT infrastructure products, product warranties, and support services, primarily transacting with system integrators who serve end-users across various industries in Malaysia. The Group carries and supports a portfolio of 18 established brand-specific IT infrastructure products from principals for whom it is an authorised distributor.

IPO Details

- Technology (22.5)

- Technology Equipment (31.0)

Strategic Overview & Data Visuals

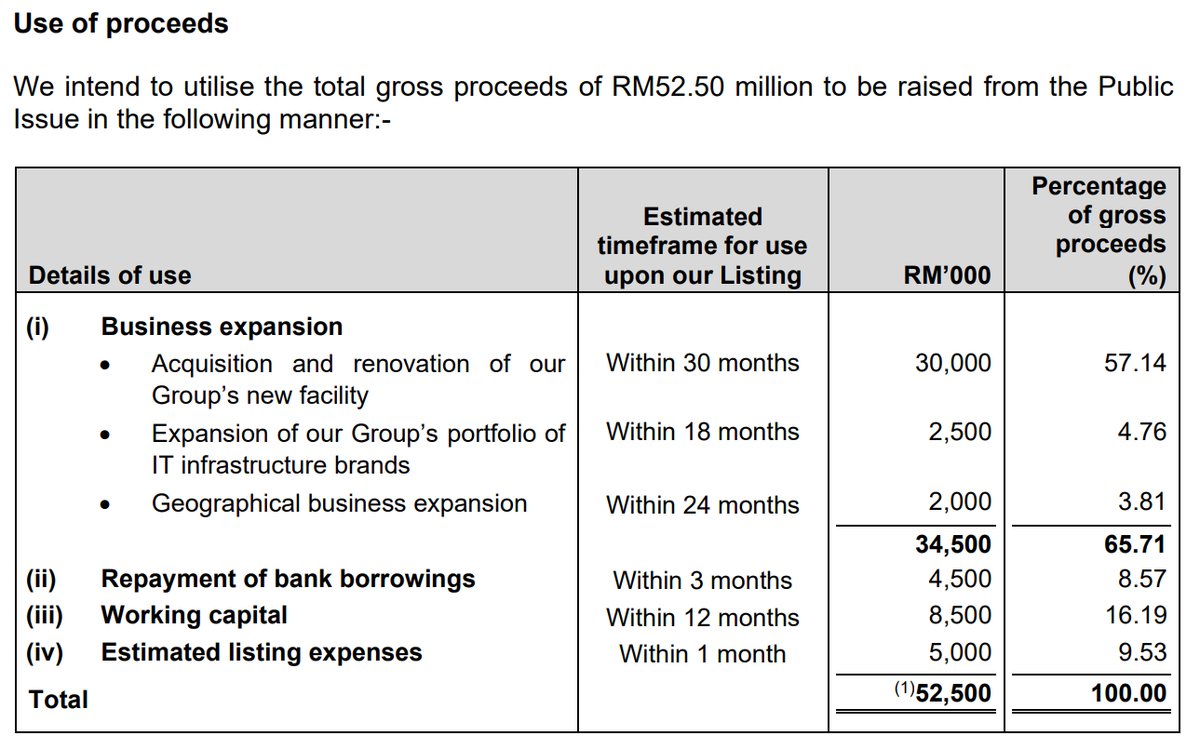

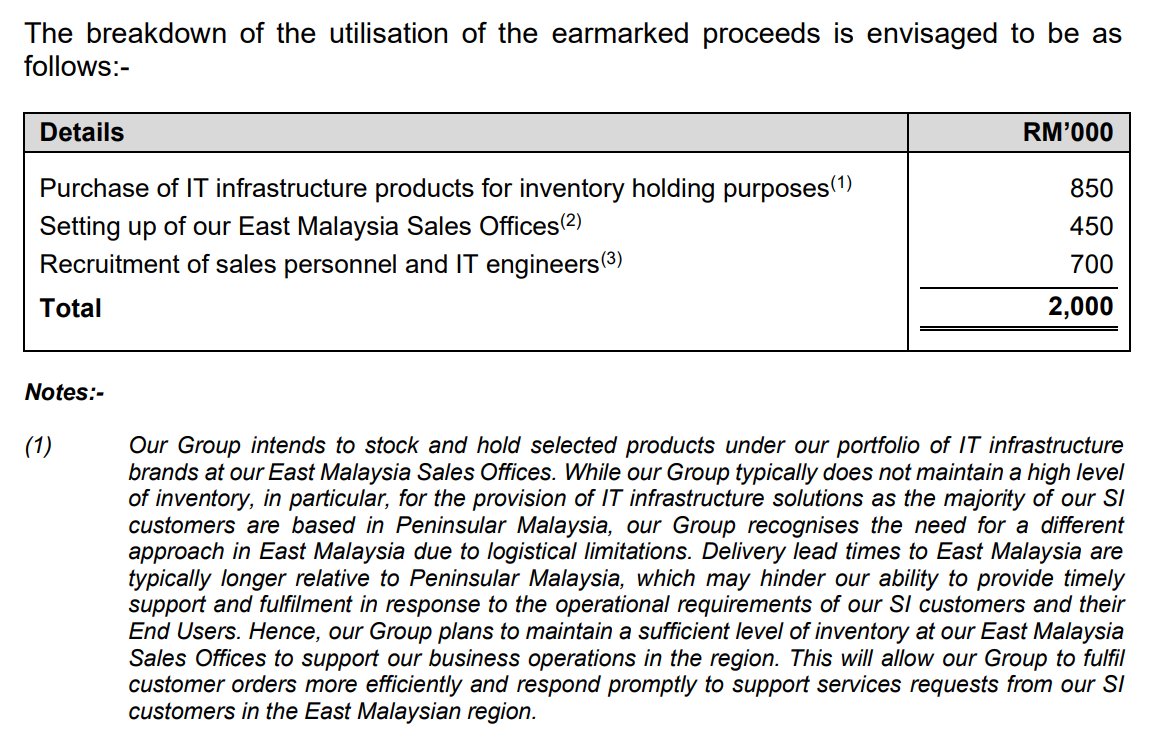

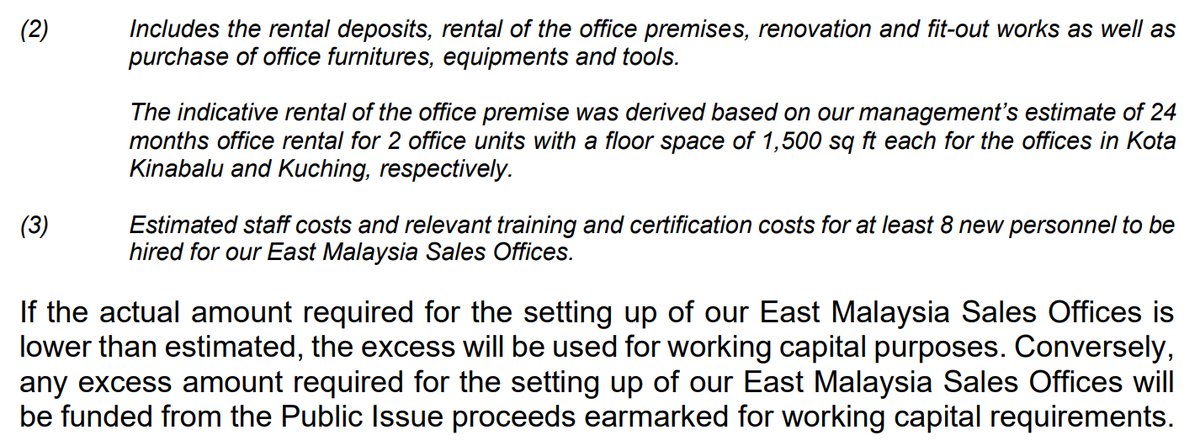

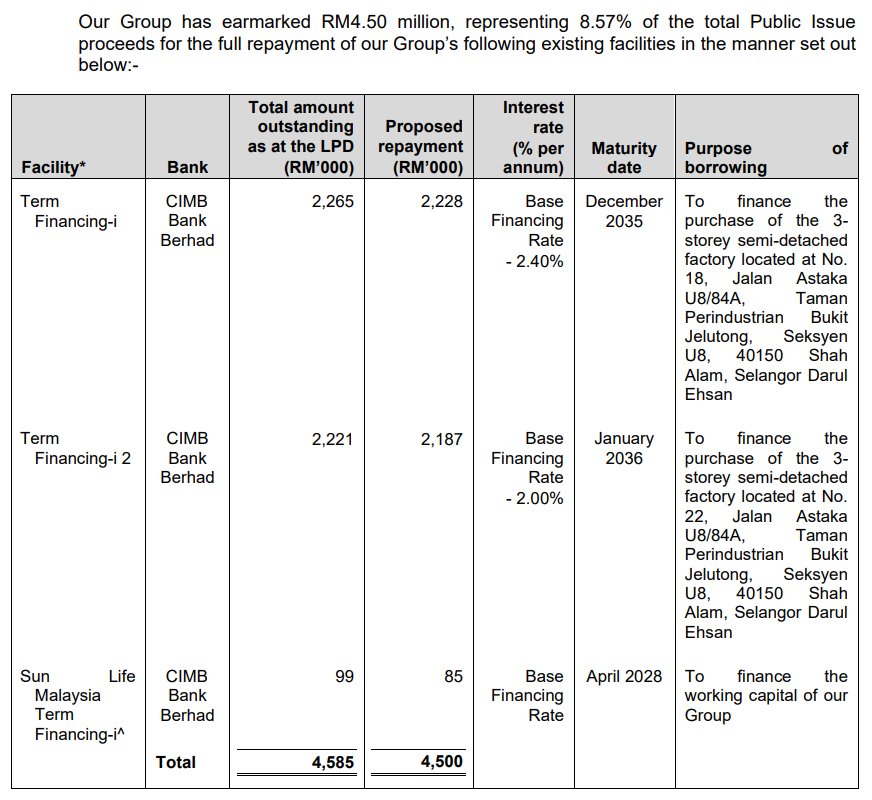

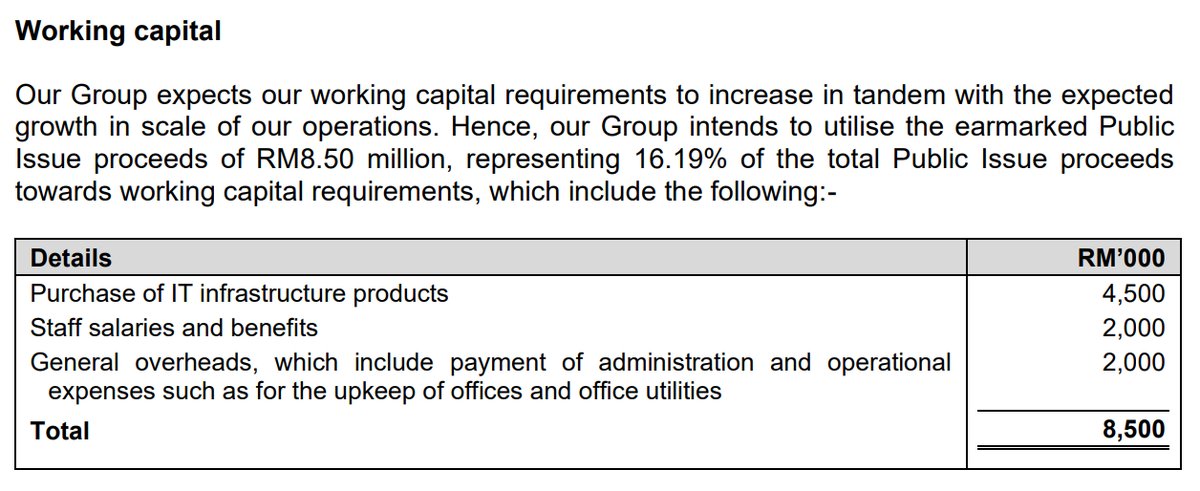

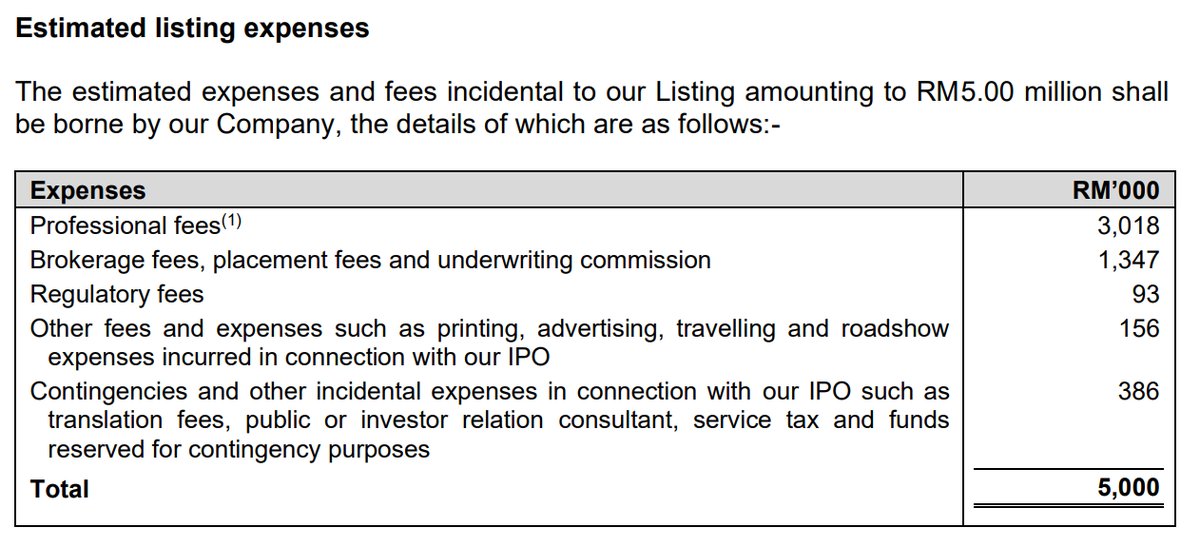

Utilisation of Proceeds

| Purpose | Amount (RM'000) | % | |

|---|---|---|---|

| Expansion | Acquisition and renovation of our Group’s new facility | 30,000 | 57.14 |

| Expansion | Expansion of our Group’s portfolio of IT infrastructure brands | 2,500 | 4.76 |

| Expansion | Geographical business expansion | 2,000 | 3.81 |

| Working capital | Working capital | 8,500 | 16.19 |

| Listing expenses | Estimated listing expenses | 5,000 | 9.53 |

| Debt | Repayment of bank borrowings | 4,500 | 8.57 |

| Total | 52,500 | 100 | |

Comparable Companies (Peers Similarity)

| Company | % | Source | Note |

|---|---|---|---|

| VSTECS | 65 | AI | Distributor (consumer electronics + enterprise infrastructure) |

| INFOTEC | 40 | AI | System Integrator (Networking, Cybersecurity, Data Centre physical infrastructure) |

| CLOUDPT | 20 | AI | System Integrator (Software, Cloud, and IT Service Management like ServiceNow, primarily for Tier-1 Banks) |

Analyst Highlights

| Date | Analyst Highlights |

|---|---|

|

03-Mar-2026

Mercury |

|

|

02-Mar-2026

Apex |

|

|

02-Mar-2026

Mplus |

|

|

02-Mar-2026

Public Invest |

|

|

02-Mar-2026

RHB |

|

|

27-Feb-2026

TA |

|

Utilisation of Proceeds

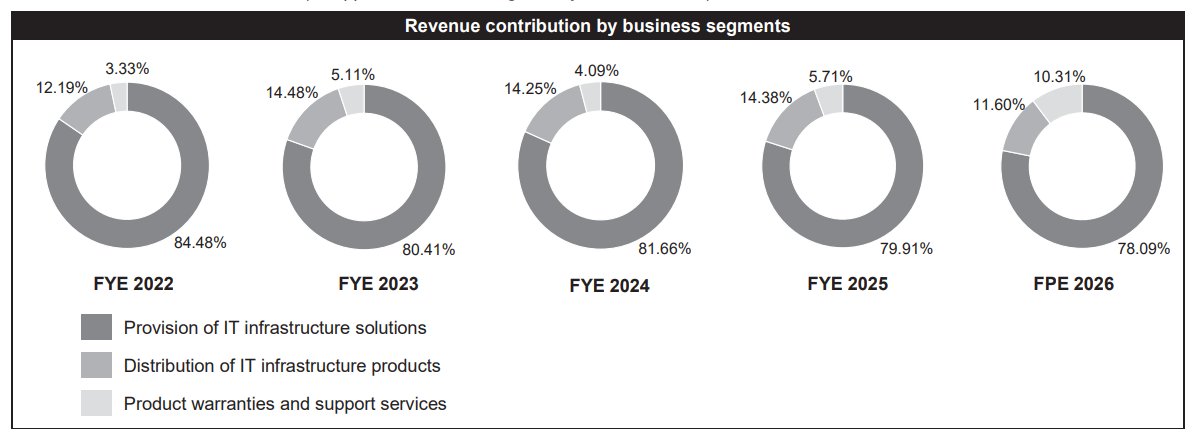

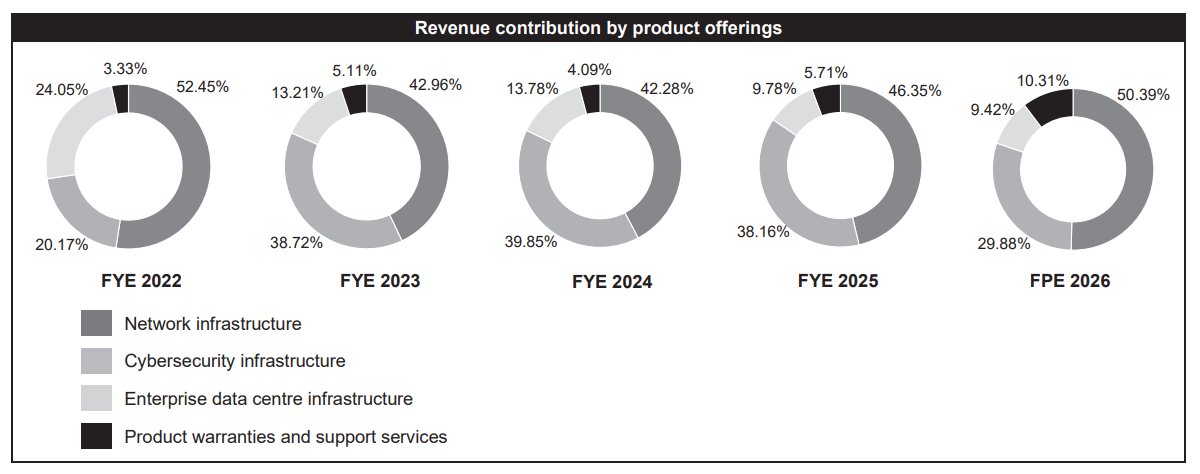

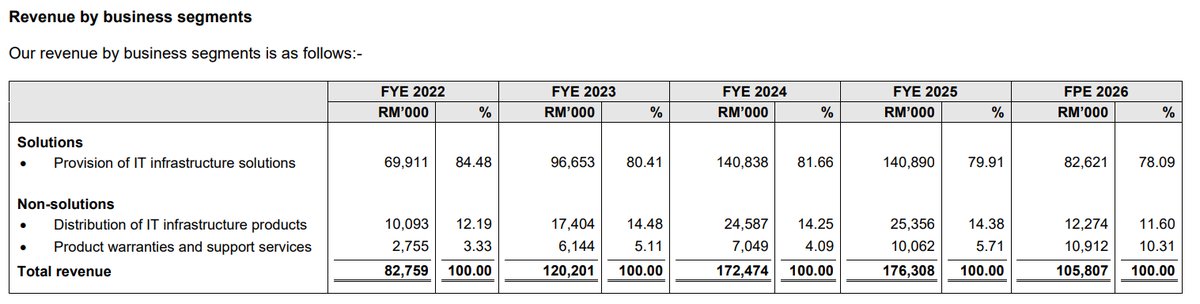

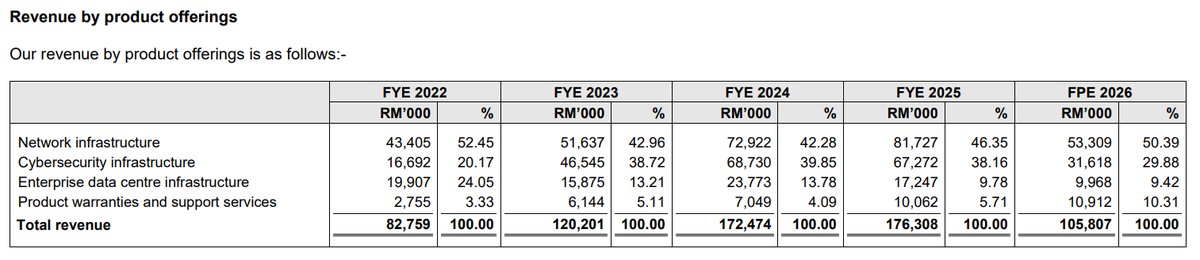

Business Segments

Geographical Segments

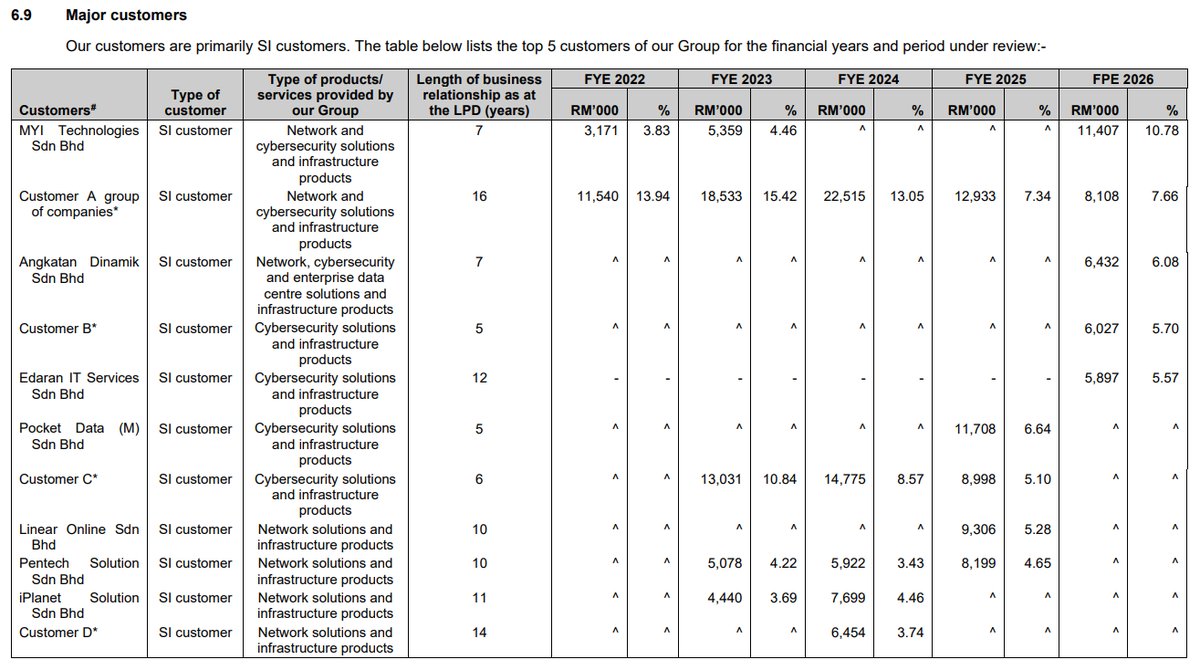

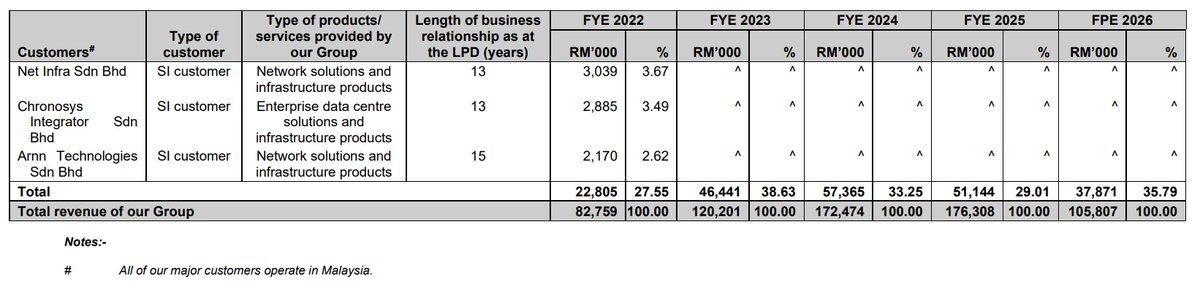

Major Customers

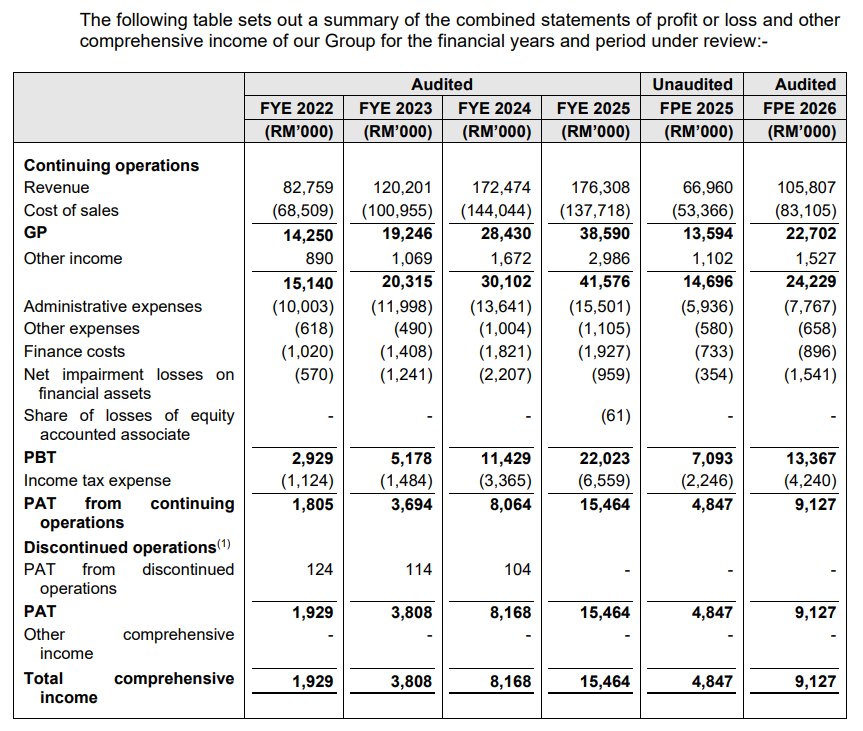

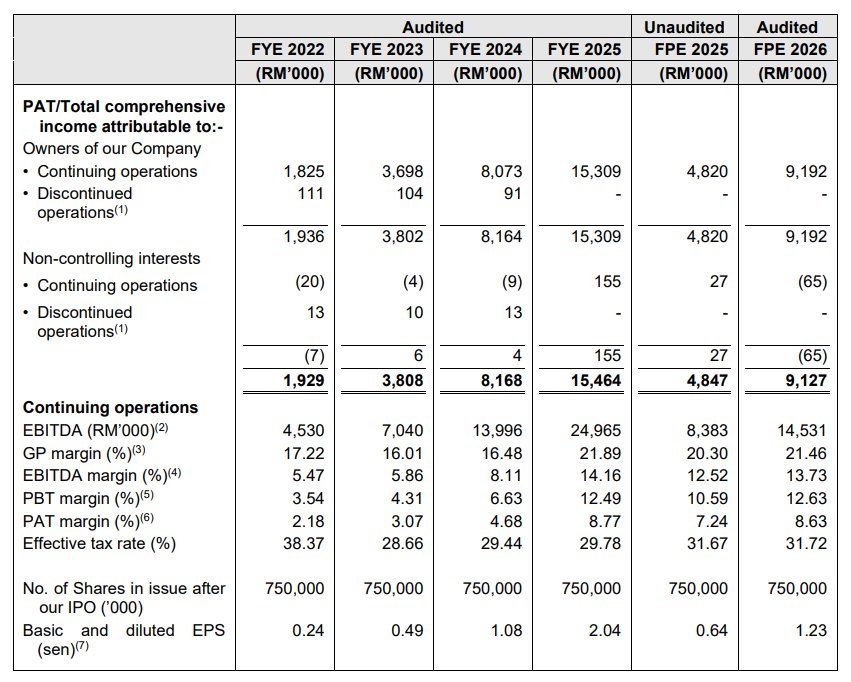

Revenue by Financial Year Ended

Profit After Tax (PAT) by Financial Year Ended

Revenue by Financial Period Ended

Profit After Tax (PAT) by Financial Period Ended

SWOT Analysis

Strengths

- High-Margin Hybrid Model: Achieves an 8.7% net margin, significantly higher than pure distributors like VSTECS (~2%), by bundling design and implementation services with hardware sales.

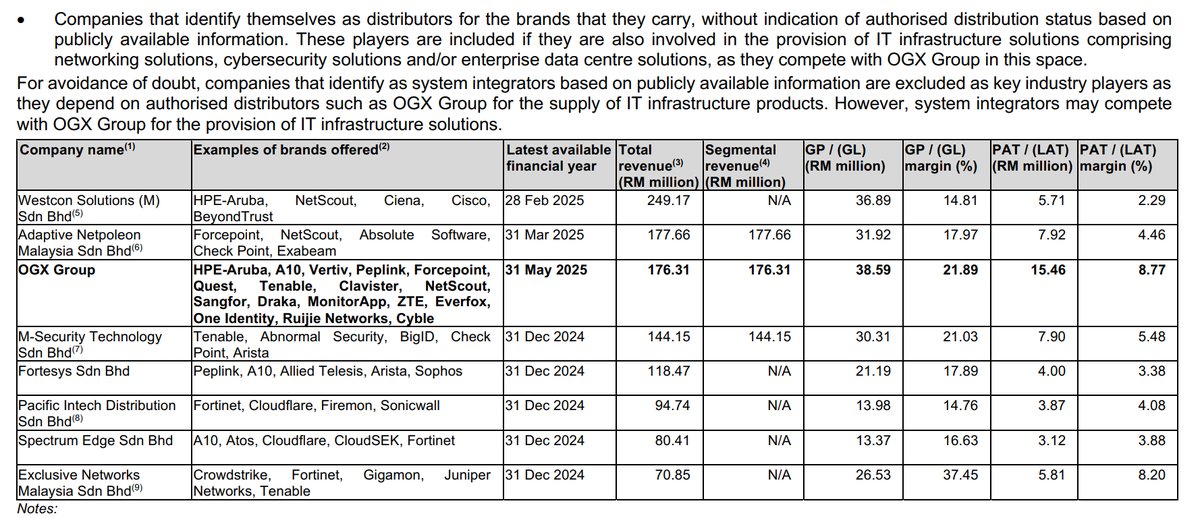

- Diverse Brand Portfolio: Acts as an authorized distributor for 18 global principals like HPE-Aruba and Sangfor, creating a competitive moat as customers cannot easily bypass them for direct purchases.

- Broad Customer Base: Serves 610 System Integrators with the top customer contributing less than 10% of revenue, indicating low customer concentration and counterparty risk.

- Strong Technical Team: Employs 56 engineers out of 127 staff, validating its position as a value-added solutions specialist rather than a simple hardware trader.

Weaknesses

- Slowing Revenue Growth: Top-line growth decelerated sharply to just 2.2% in FY2025 from over 40% in the preceding two years, raising concerns about market saturation or project delays.

- Low Recurring Income: The business model is reliant on one-off purchase orders, lacking long-term maintenance contracts which results in low future earnings visibility beyond the current order book.

Opportunities

- Data Centre Spillover: The boom in hyperscale data centers is creating downstream demand for enterprise-level data centre infrastructure, a key market segment that OGX services.

- Vietnam Expansion: A joint venture for DTCT modular data centres provides a strategic entry into the high-growth, relatively untapped data centre market in Vietnam.

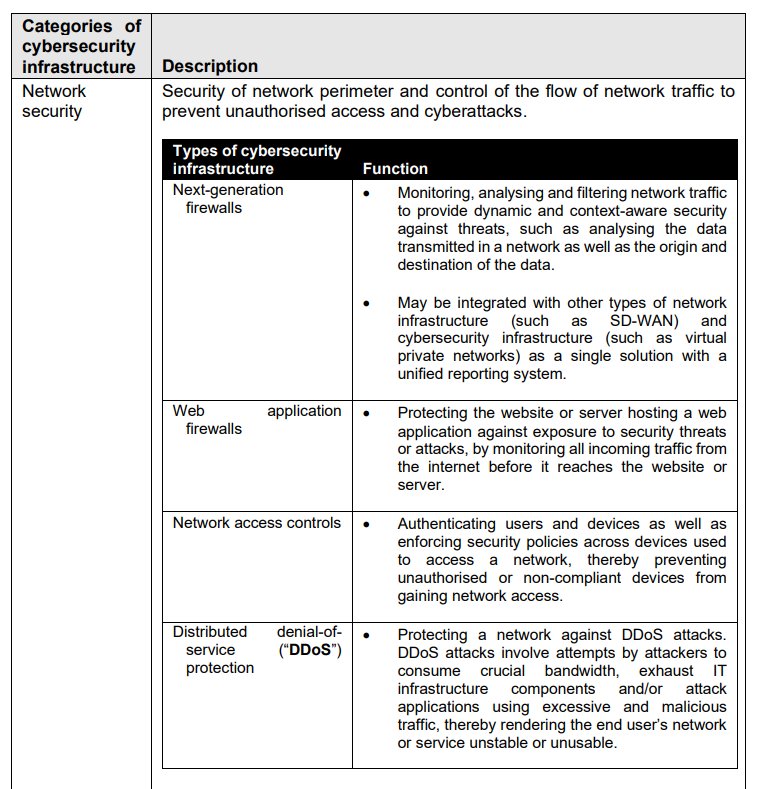

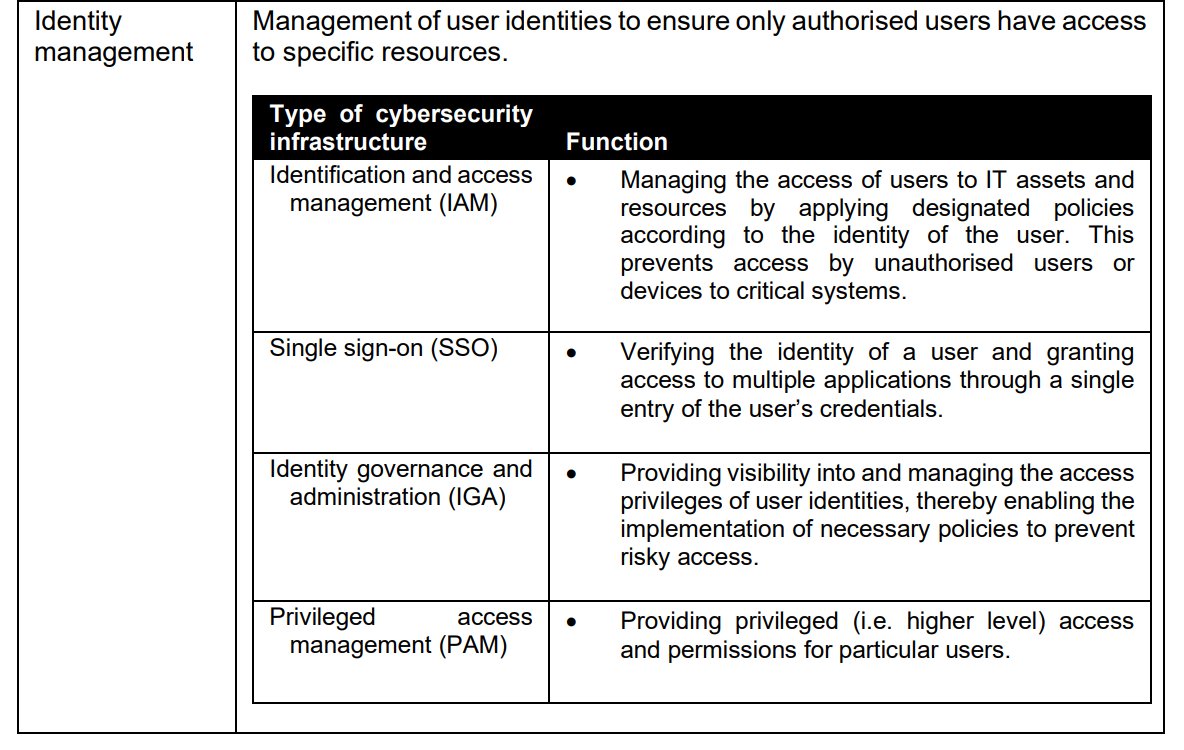

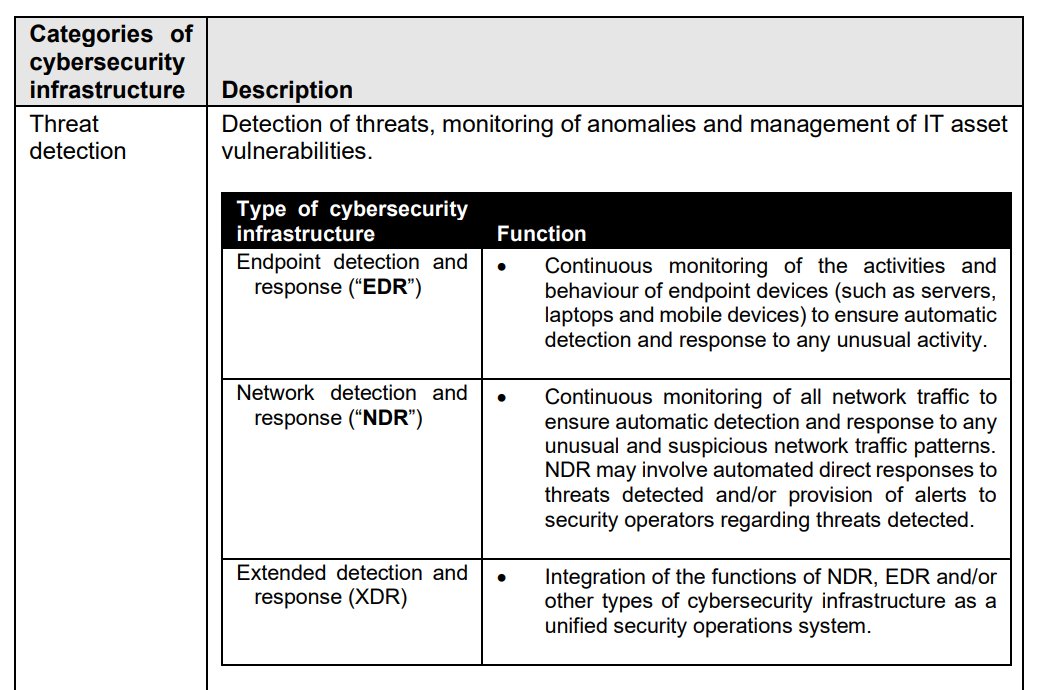

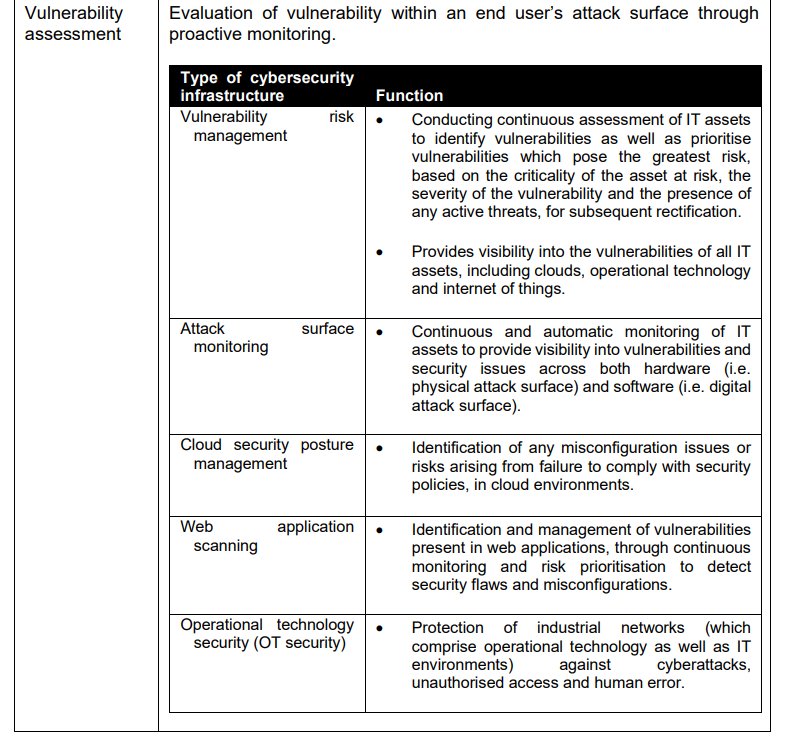

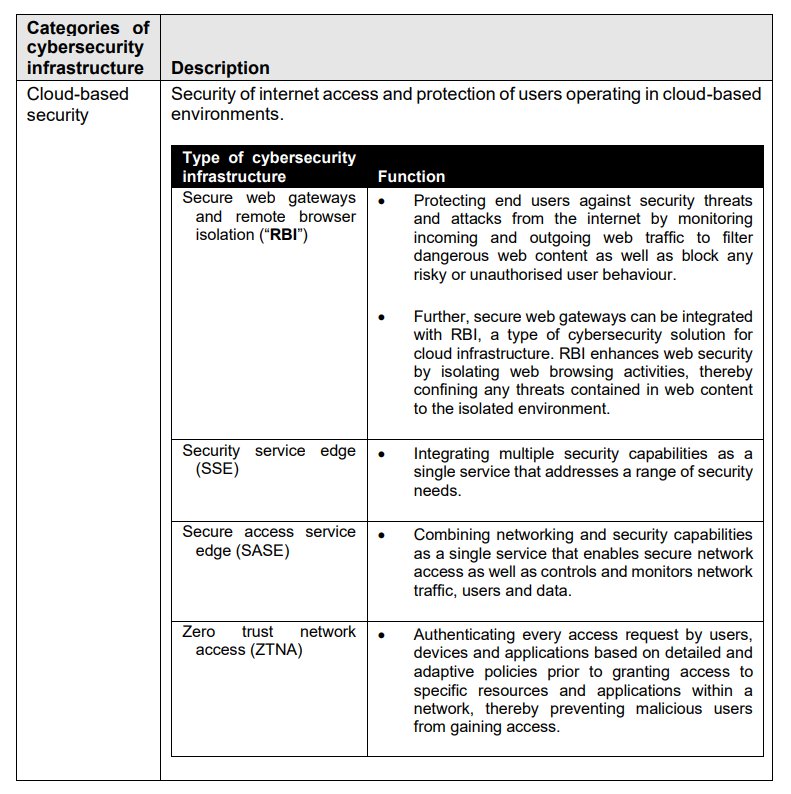

- Cybersecurity Mandates: New regulations like the Cyber Security Act 2024 are expected to compel corporations to increase spending on cybersecurity, directly benefiting OGX's second-largest business segment.

Threats

- Foreign Exchange Risk: Purchases are primarily in USD while sales are in RM. Rapid currency fluctuations can compress margins on fixed-price quotes if not managed effectively.

- Principal Dependency: Over 60% of purchases are from its top three principals (HPE, Sangfor, Vertiv). The potential loss of a key distributorship would severely impact the business.

- Inventory Obsolescence: Operating in the fast-paced technology sector, holding inventory for an average of 44-79 days carries a significant risk of products becoming outdated or superseded.

Key Highlights

Sorry, this feature only available for iSaham Pro

Conclusion

Sorry, this feature only available for iSaham Pro

OGX Group Berhad's Latest News