Empire Premium Food Berhad IPO's Analysis

Empire Premium Food Berhad

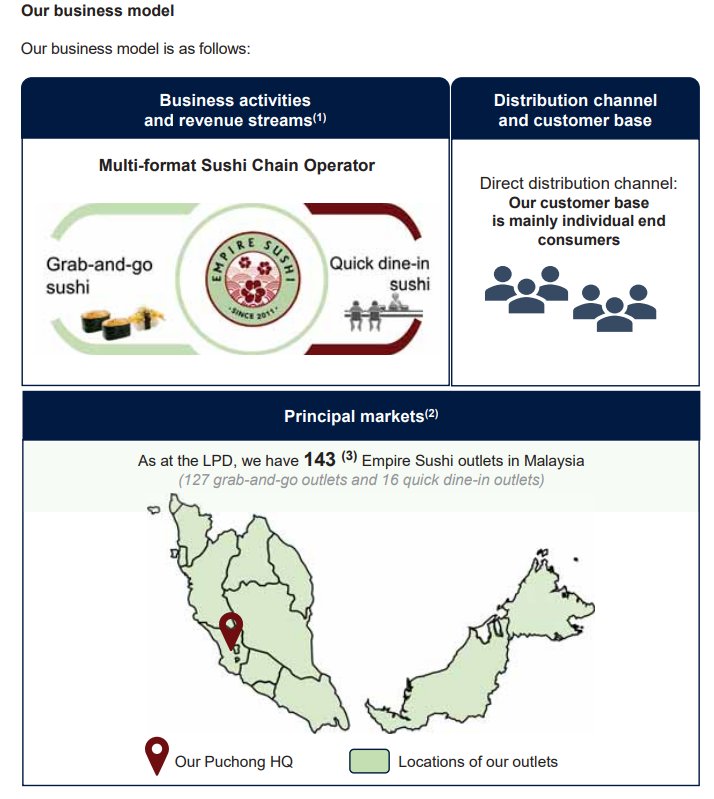

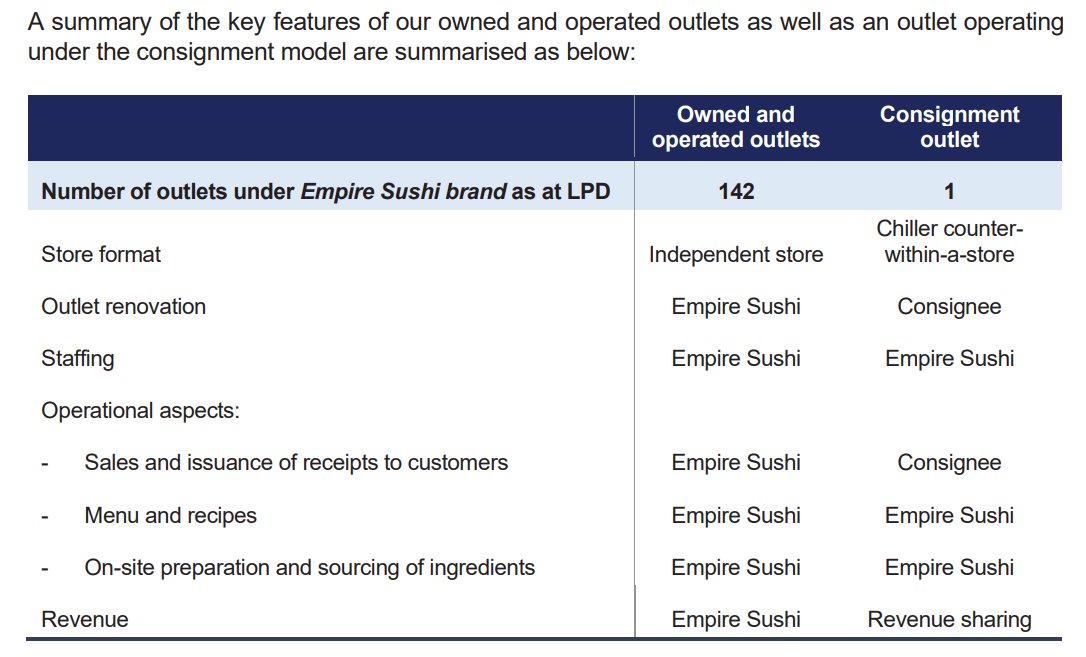

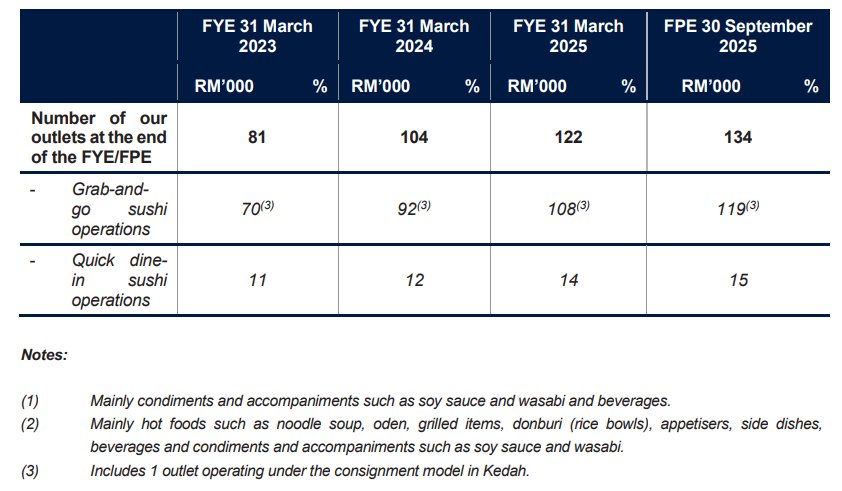

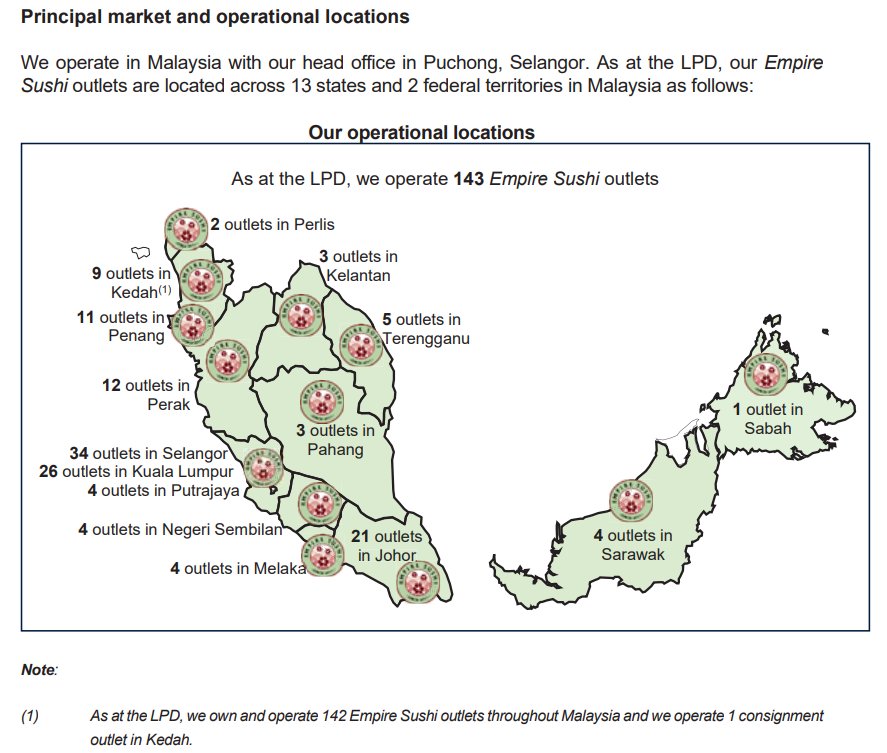

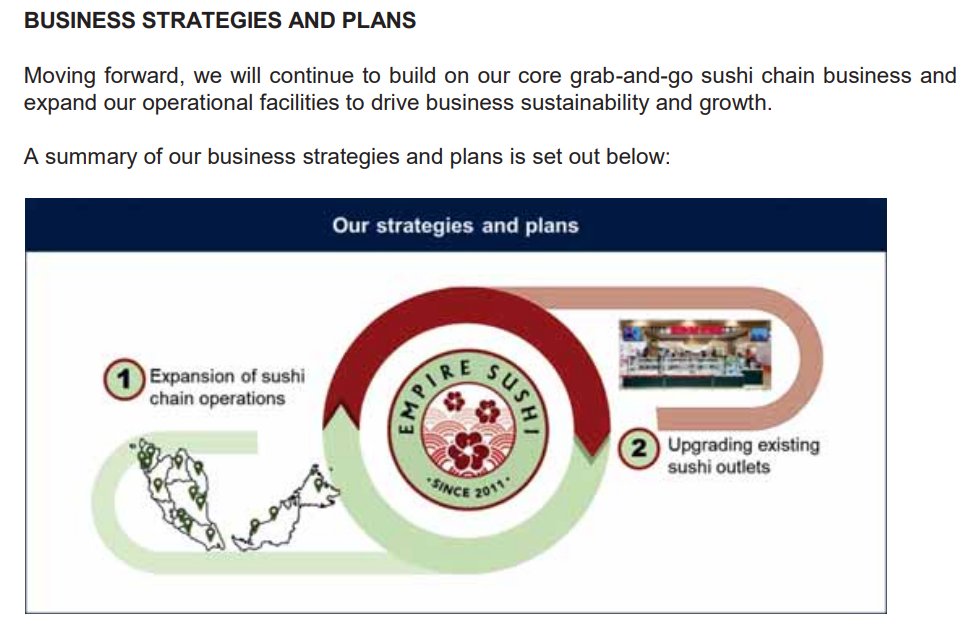

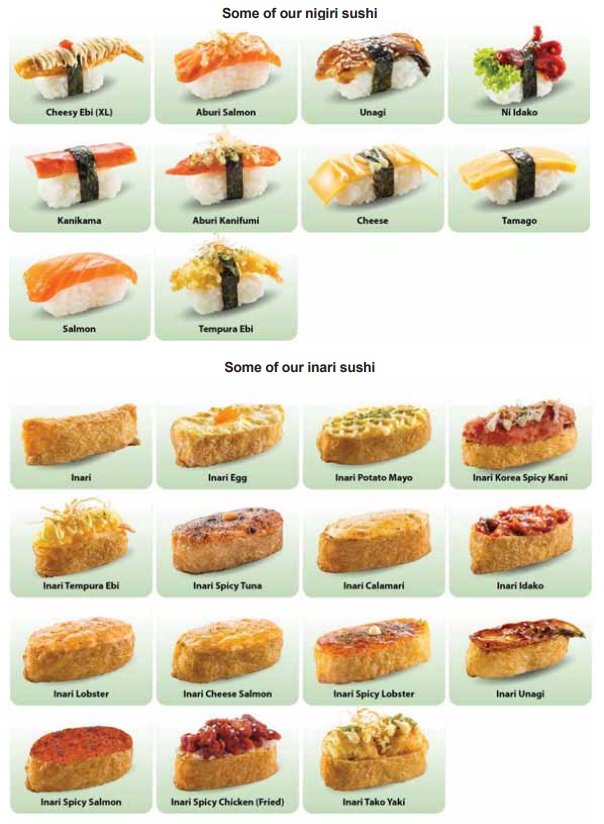

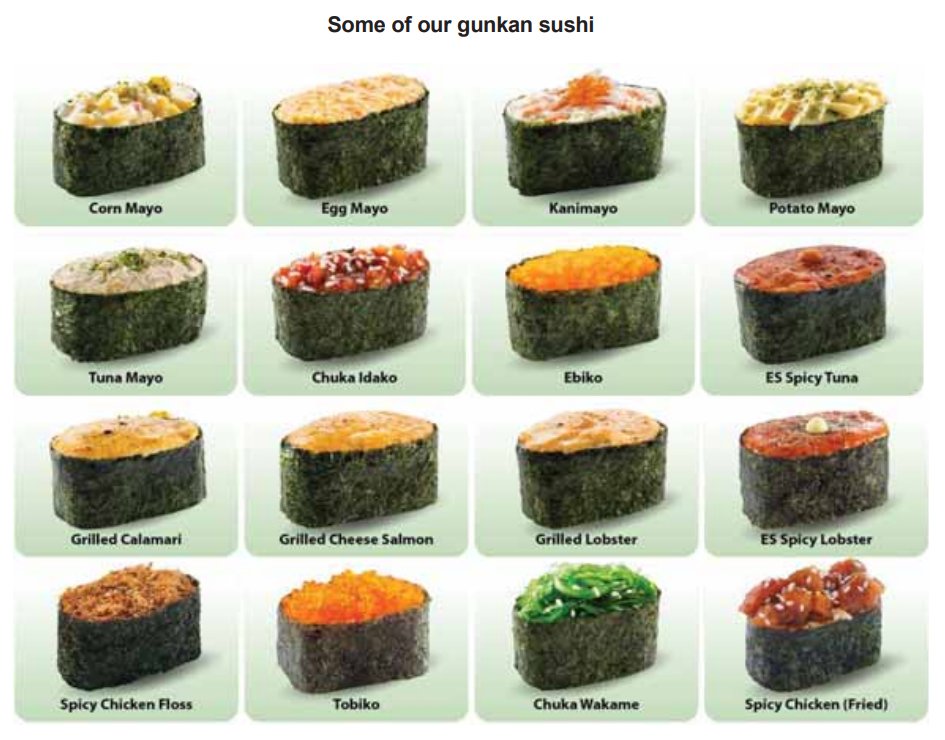

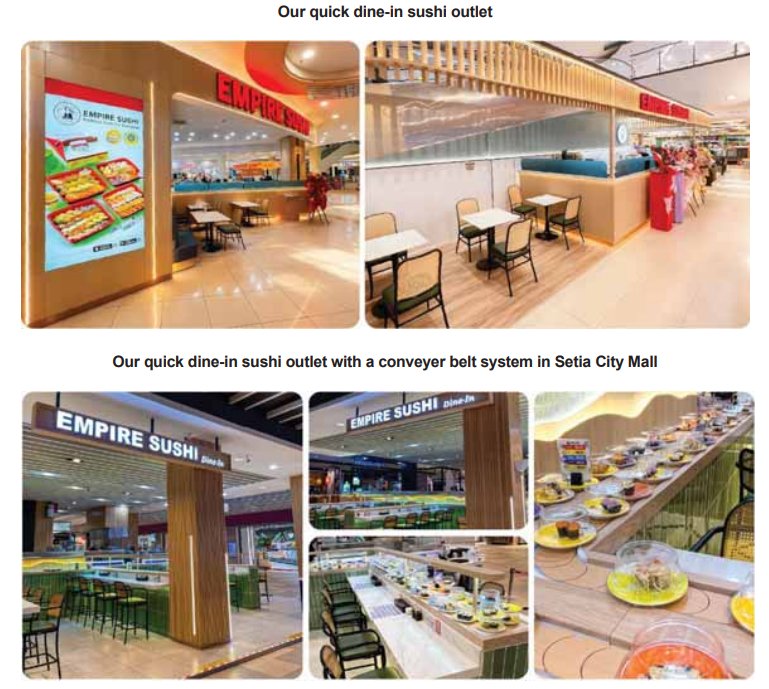

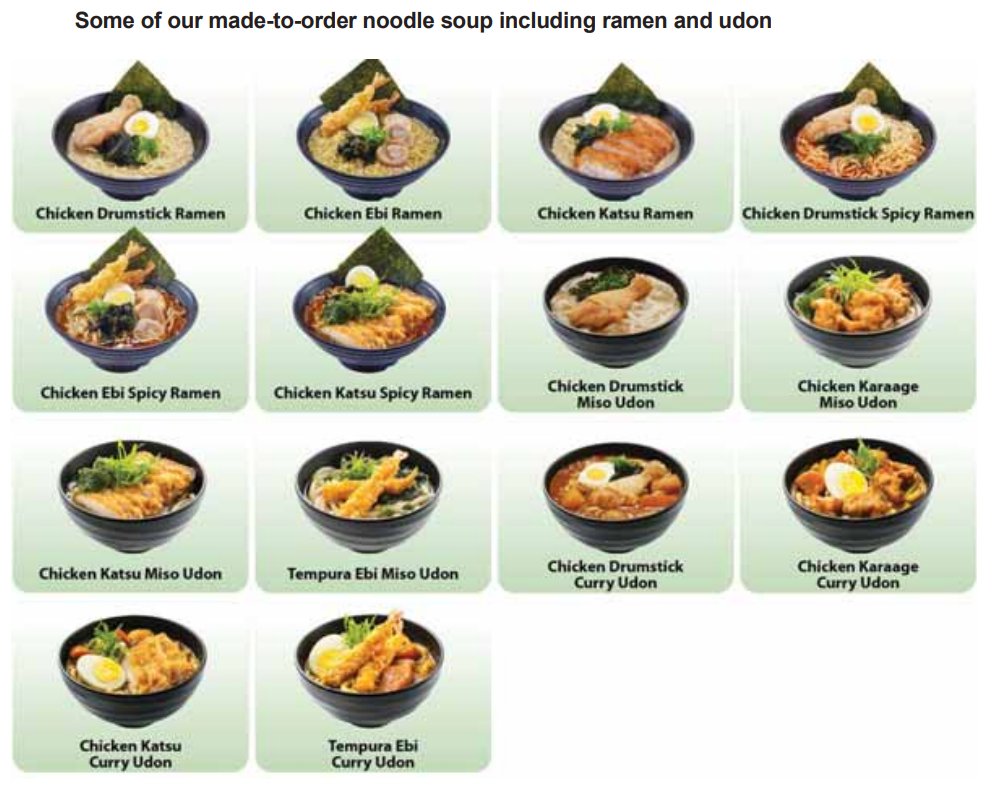

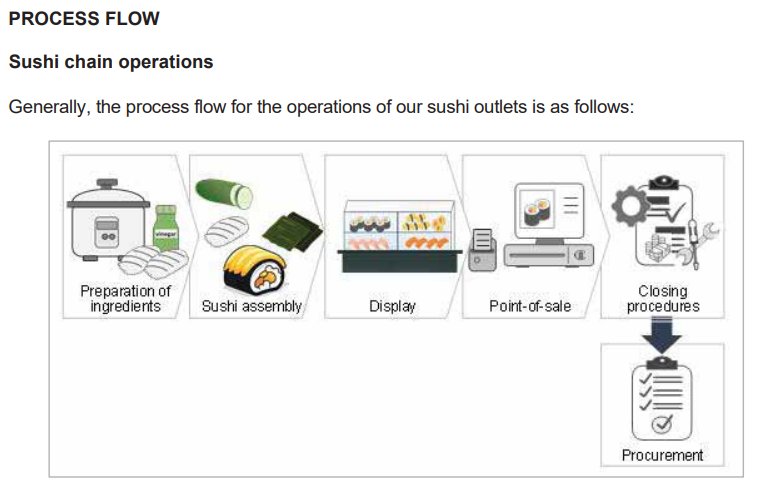

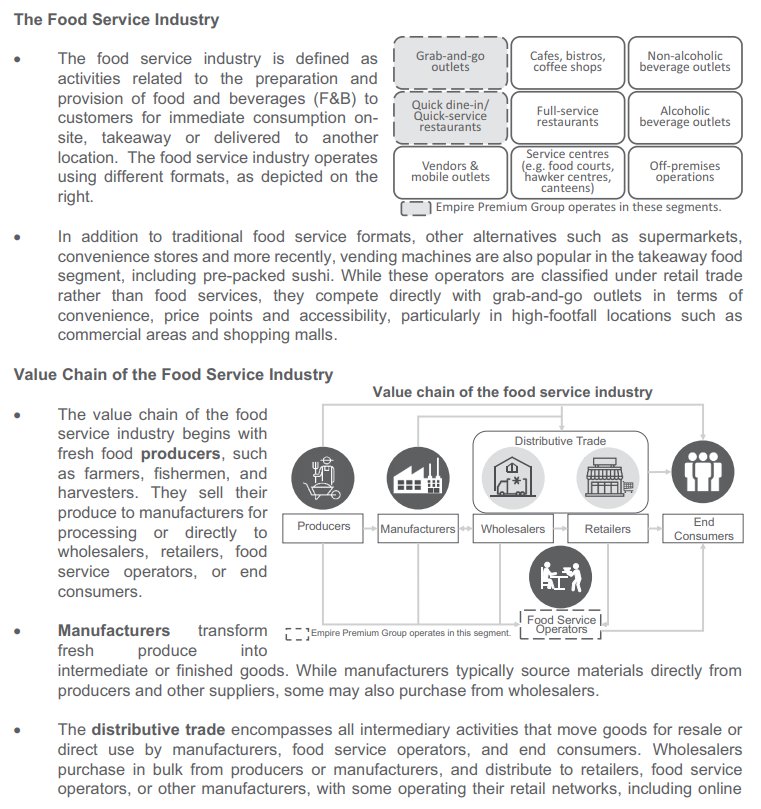

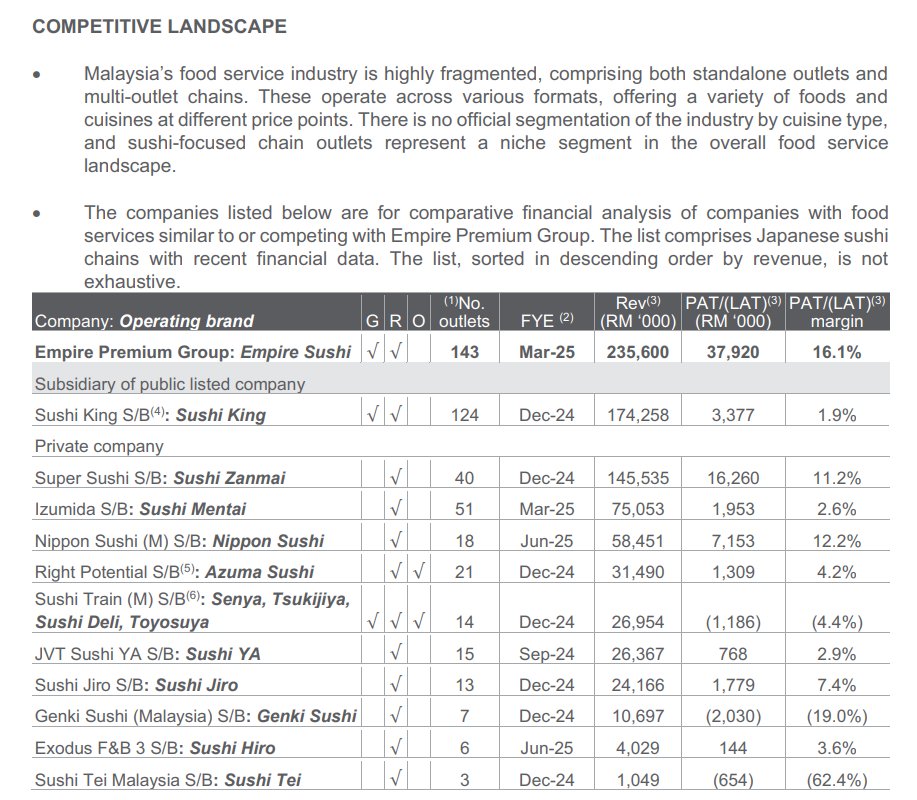

Empire Premium Food Berhad, through its subsidiary Empire Sushi, is an owner-operator of a chain of sushi food service outlets in Malaysia. The company targets the mass market with accessible and convenient localised Japanese food, primarily focusing on ready-to-eat sushi. As of the Latest Practicable Date (LPD), the Group operates 132 outlets across 12 states and 2 federal territories in Malaysia, comprising 117 grab-and-go outlets and 15 quick dine-in outlets. The business history traces back to 2010, starting with grab-and-go sushi operations on a consignment basis in hypermarkets and has since expanded its footprint and operational formats across Peninsular and East Malaysia.

IPO Details

Strategic Overview & Data Visuals

Utilisation of Proceeds

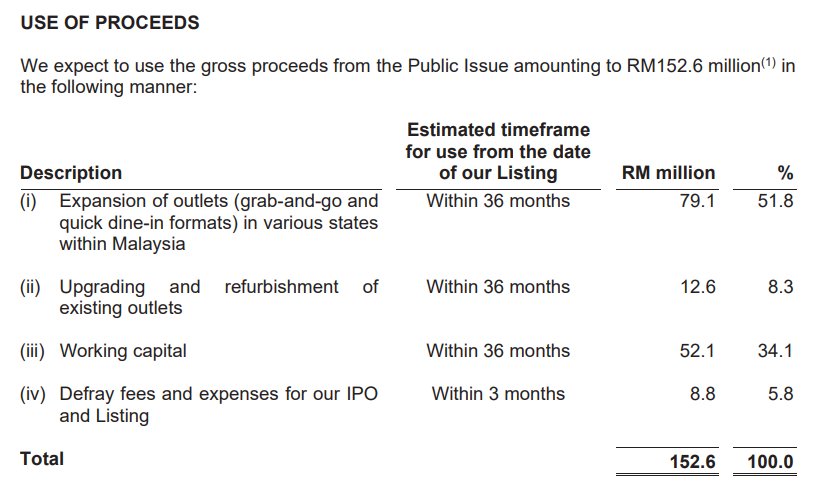

| Purpose | Amount (RM'000) | % | |

|---|---|---|---|

| Expansion | Expansion of outlets (grab-and-go and quick dine-in formats) in various states within Malaysia | 79,100 | 51.8 |

| Expansion | Upgrading and refurbishment of existing outlets | 12,600 | 8.3 |

| Working capital | Working capital | 52,100 | 34.1 |

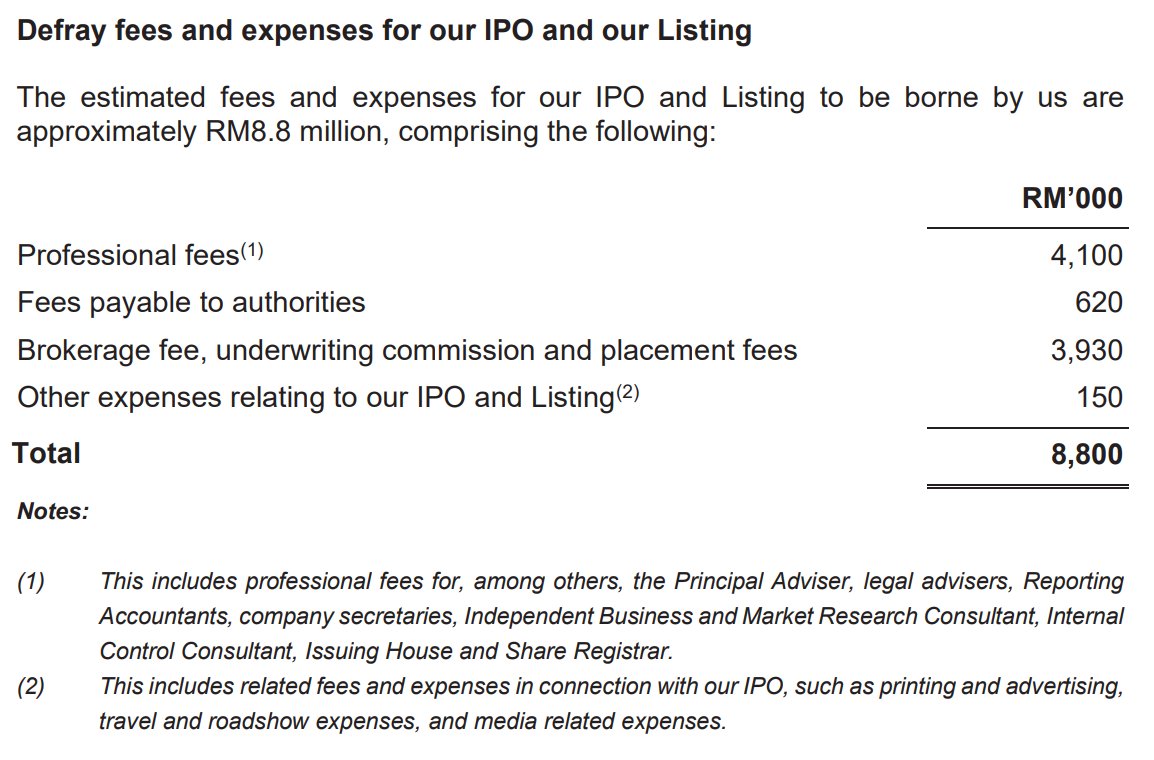

| Listing expenses | Defray fees and expenses for our IPO and Listing | 8,800 | 5.8 |

| Total | 152,600 | 100 | |

Comparable Companies (Peers Similarity)

| Company | % | Source | Note |

|---|---|---|---|

| KOPI | 90 | AI | Top pure-play peer with 100% retail F&B focus and high-growth mall dominance |

| BJFOOD | 88 | AI | Closest operational peer mirroring Empire's hybrid mix of grab-and-go kiosks and seated dining outlets |

| SDS | 45 | AI | Shares the retail store layout but differs as 61% of revenue is derived from wholesale manufacturing |

| TEXCHEM | 40 | IMR | Diversified conglomerate where F&B is a minority segment; product-only match (Sushi King) |

| FOCUSP | 20 | AI | Core business is Optical (85%); F&B (Komugi) is only a minor 14% revenue contributor |

Analyst Highlights

| Date | Analyst Highlights |

|---|---|

|

31-Mar-2026

RHB |

|

|

30-Mar-2026

Mplus |

|

|

30-Mar-2026

Public Invest |

|

|

27-Mar-2026

TA |

|

Utilisation of Proceeds

Business Segments

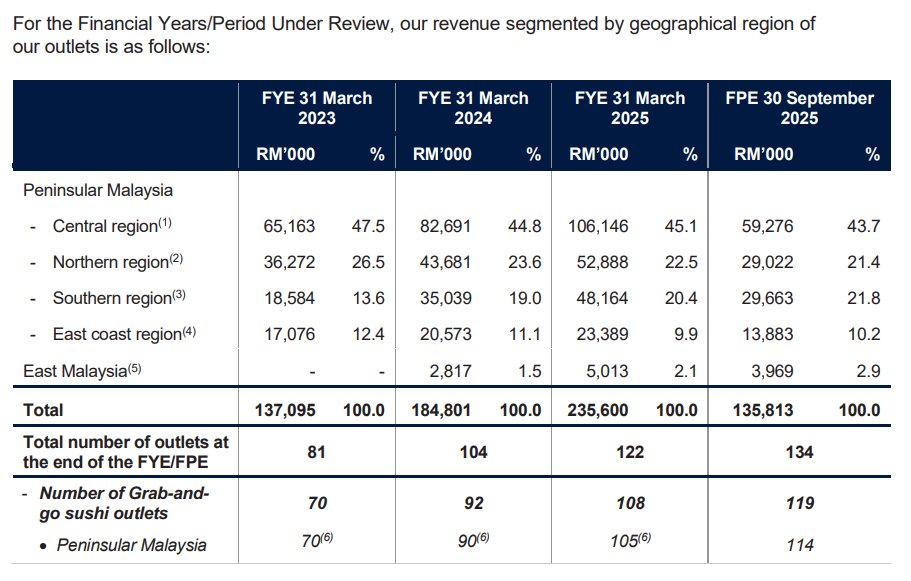

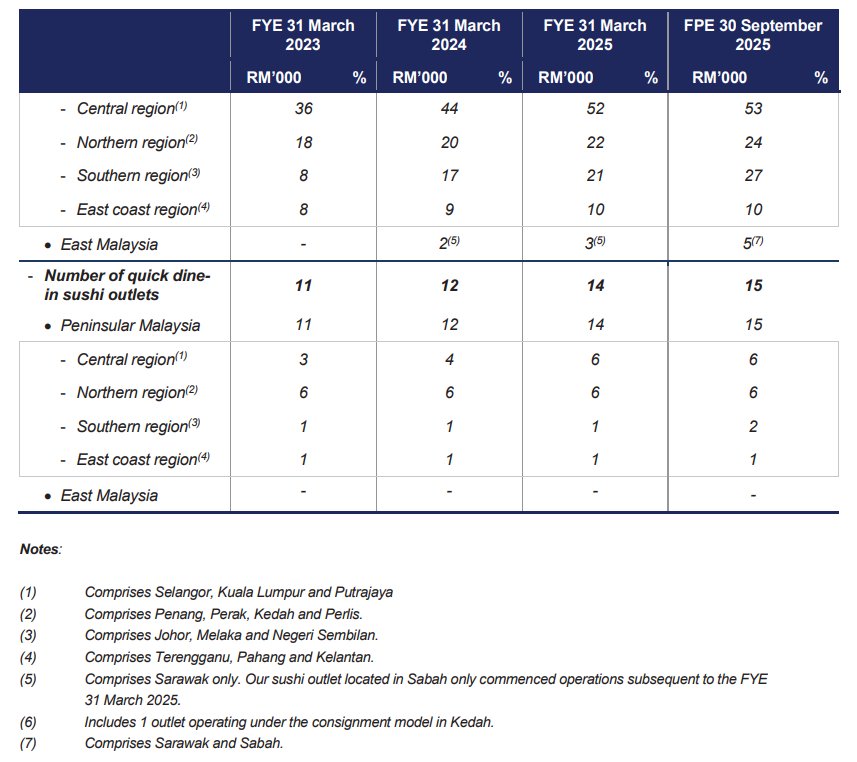

Geographical Segments

Revenue by Financial Year Ended

Profit After Tax (PAT) by Financial Year Ended

SWOT Analysis

Strengths

- Market Leadership: Empire Sushi is the largest sushi chain operator in Malaysia by both revenue and outlet count, managing 143 outlets which provides significant brand equity and procurement economies of scale.

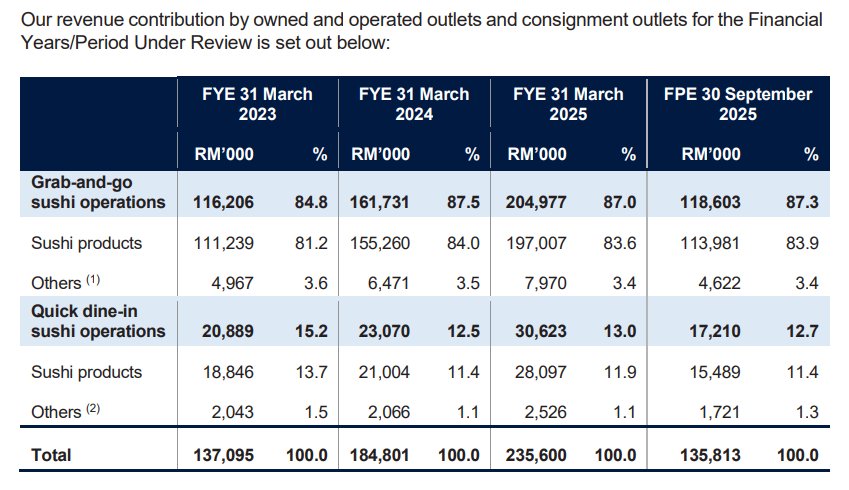

- Scalable Business Model: The grab-and-go format accounts for 87.3% of revenue, featuring small real estate footprints and low capital expenditure with rapid average payback periods of approximately 9 months.

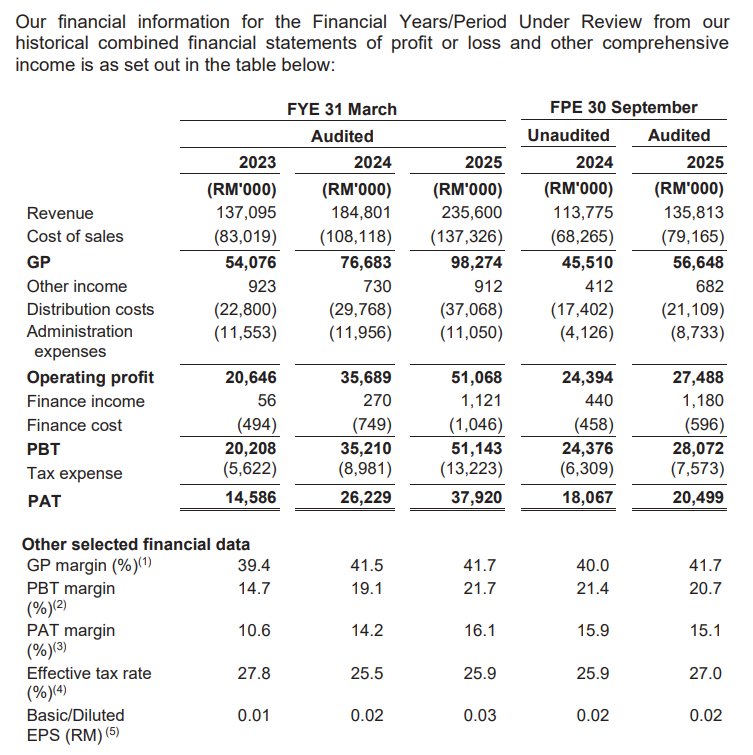

- Expanding Profit Margins: The company achieved significant operational efficiency, increasing PAT margins from 10.6% in FYE23 to 16.1% in FYE25 despite broad inflationary pressures.

- Wide Halal Accessibility: With 132 out of 143 outlets being JAKIM Halal-certified, the company effectively penetrates the majority Muslim demographic in the Malaysian market.

Weaknesses

- Tapering SSSG Growth: Overall Same-Store Sales Growth has slowed significantly from 12.2% in FYE23 to 1.6% in FPE25, indicating potential market saturation in existing locations.

- Internal Cannibalisation Risks: The Central region reported negative SSSG of -2.1% in FPE25, directly attributed to new outlet openings diverting traffic away from established stores.

- High Rental Dependency: The business operates entirely on tenanted commercial properties, making it susceptible to lease non-renewals and fluctuating rental costs across its 143 locations.

Opportunities

- Future Outlet Expansion: The IPO proceeds are earmarked to fund 64 new outlets over the next four years, targeting untapped suburban areas and transit hubs to drive volume growth.

- Increasing Convenience Demand: Growing urbanization and the rise of dual-income households support the structural shift toward affordable, ready-to-eat Japanese food options.

Threats

- Supplier Concentration Risk: Reliance on the top five suppliers for 78.8% of total purchases in FPE25 poses a significant risk to operational continuity if supply chain disruptions occur.

- Input Cost Fluctuations: Dependence on imported salmon and rice exposes the company to global commodity price swings and foreign exchange volatility.

- Competitive Market Rivalry: The company faces stiff competition from established peers like Texchem Resources Berhad (Sushi King), convenience stores, and other fragmented foodservice providers.

Key Highlights

Sorry, this feature only available for iSaham Pro

Conclusion

Sorry, this feature only available for iSaham Pro

Empire Premium Food Berhad's Latest News