Golden Destinations Group Berhad IPO's Analysis

Golden Destinations Group Berhad

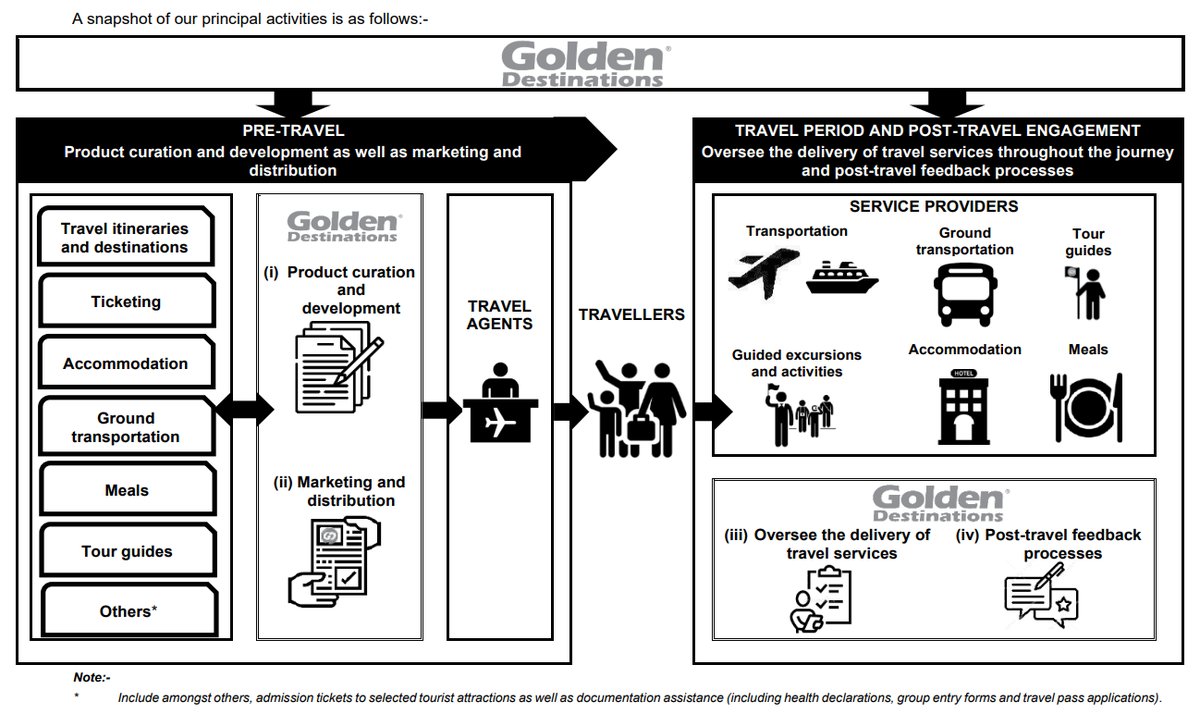

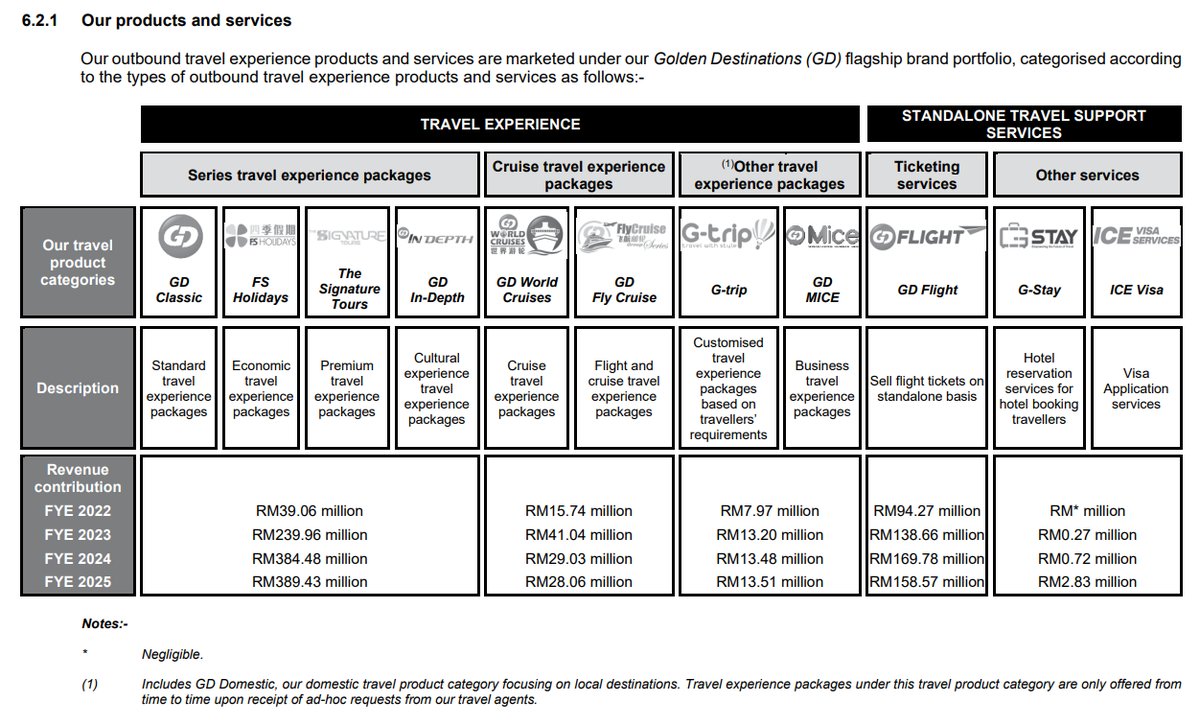

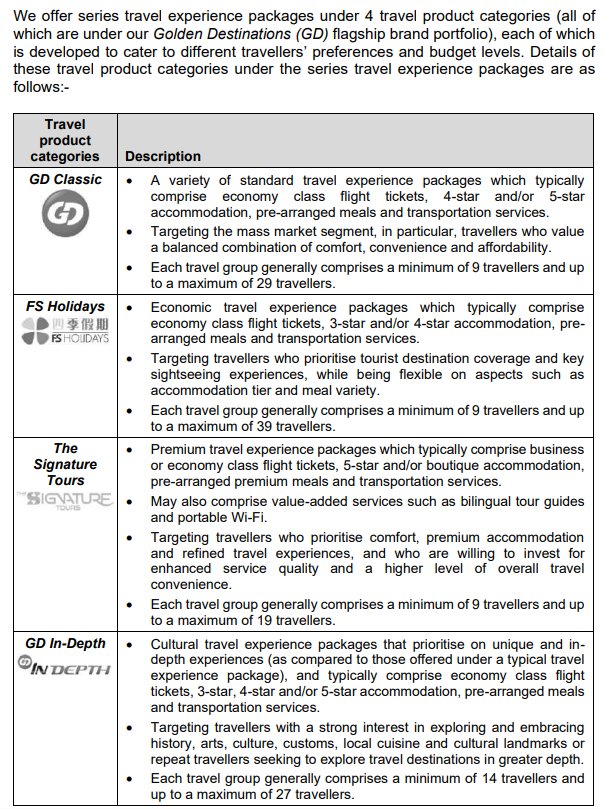

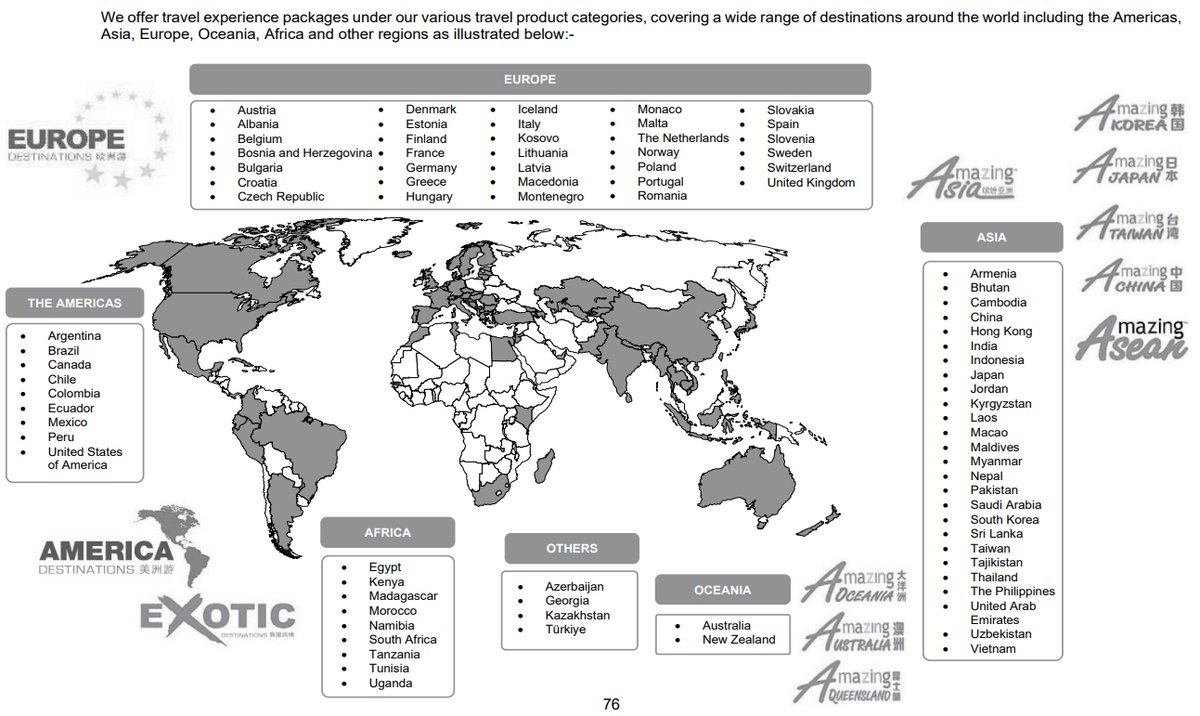

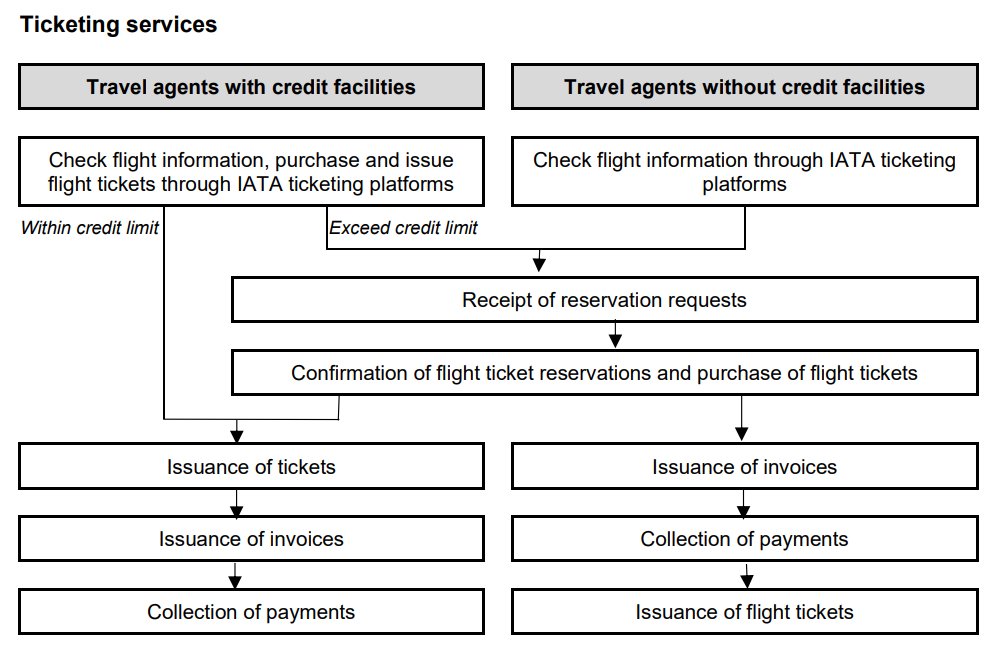

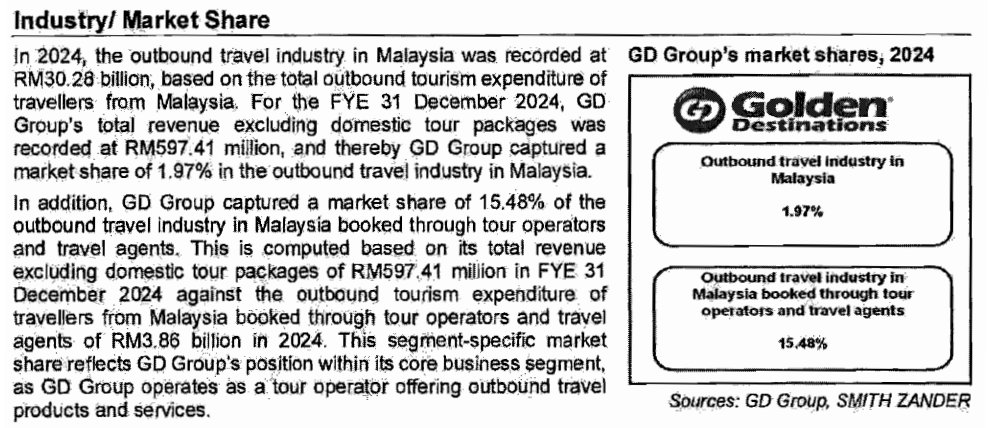

Golden Destinations Group Berhad, through its principal subsidiary ICE Holidays, operates as a full-service outbound travel experience curator in Malaysia. The company offers a comprehensive suite of outbound travel products and services under its flagship brand, Golden Destinations (GD). It functions primarily within the B2B segment, serving a wide network of licensed travel agents who act as its main distribution channel. The Group's offerings include a variety of curated travel experience packages such as series travel, cruise travel, and other specialized tours (FIT, MICE, Domestic), alongside standalone travel support services like flight ticketing, hotel reservations, and visa applications. Incorporated in Malaysia, the company has established a strong brand presence and extensive industry knowledge over approximately 30 years of operation.

IPO Details

- Consumer Products & Services (11.5)

- Travel, Leisure & Hospitality (14.9)

Strategic Overview & Data Visuals

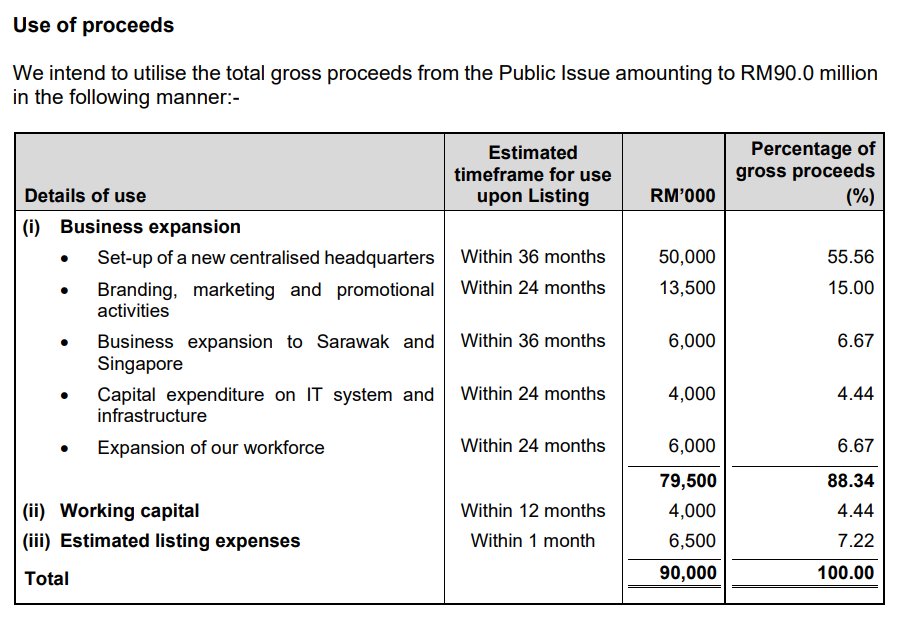

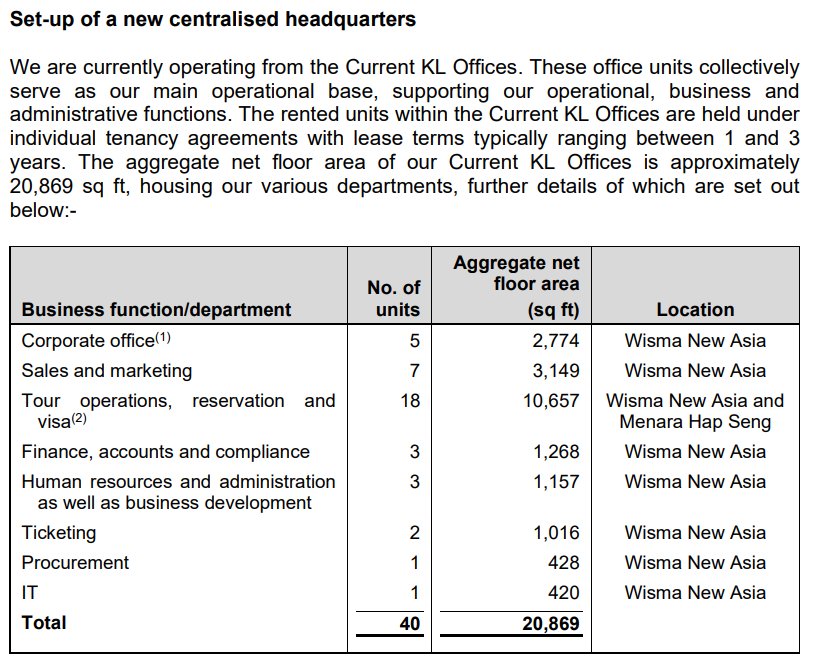

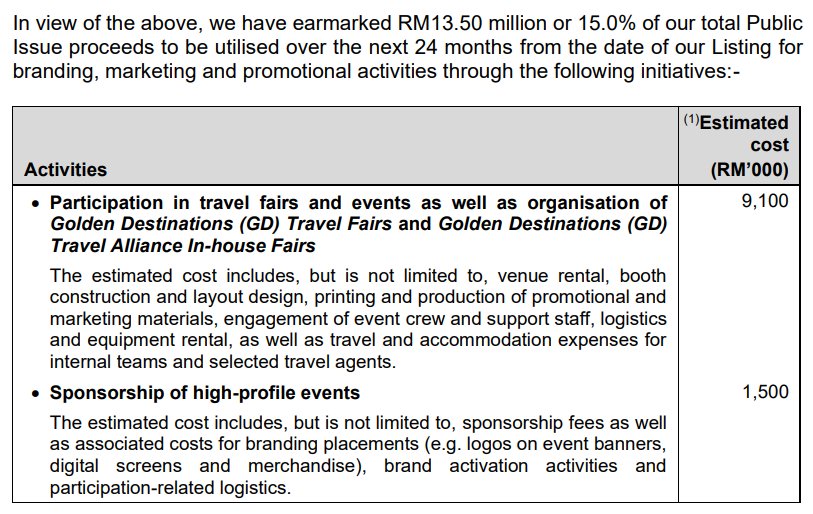

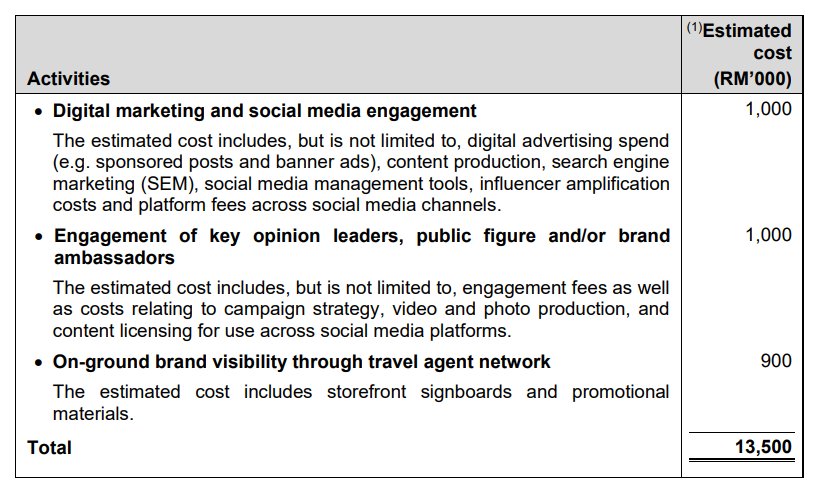

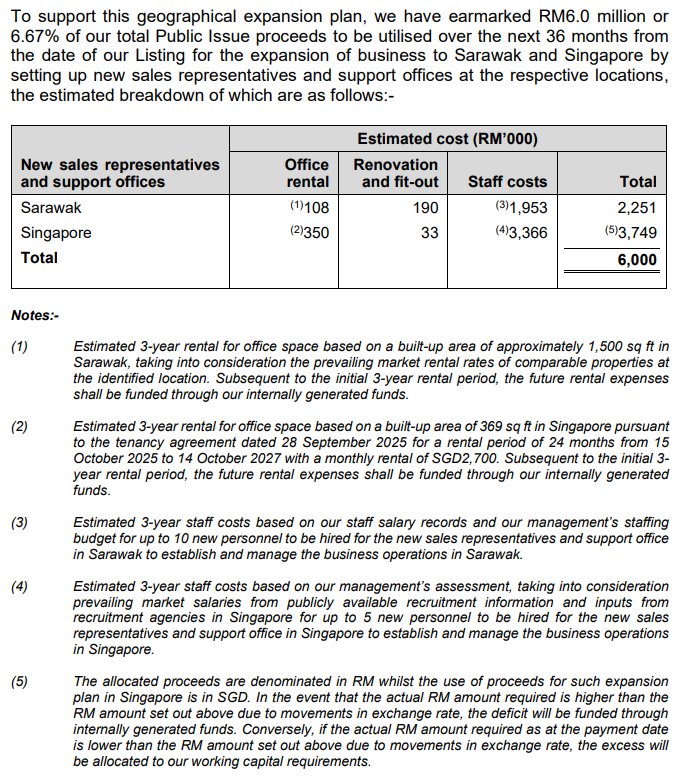

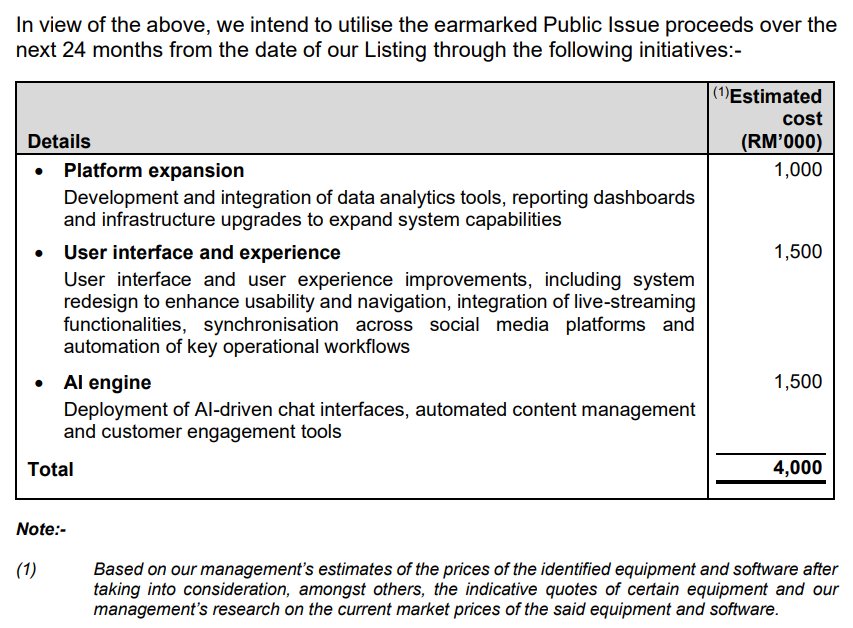

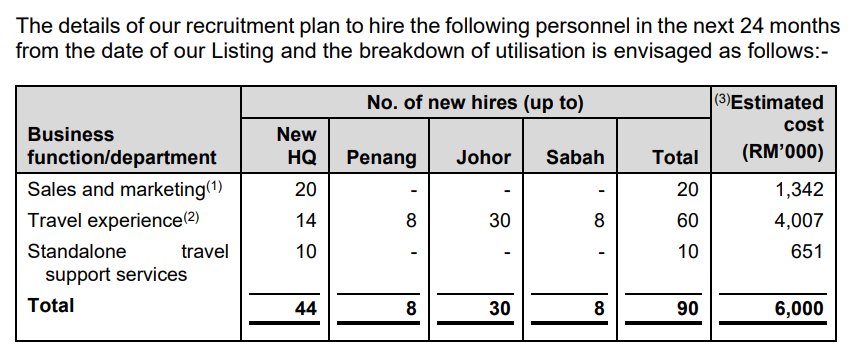

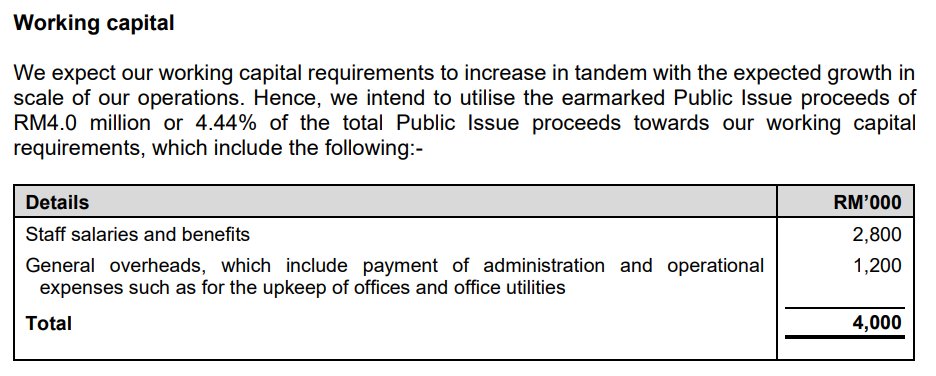

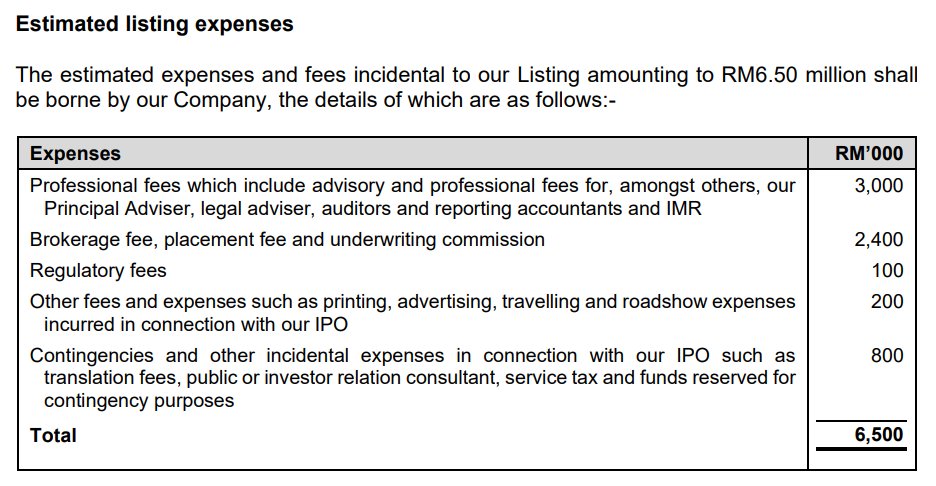

Utilisation of Proceeds

| Purpose | Amount (RM'000) | % | |

|---|---|---|---|

| Expansion | Set-up of a new centralised headquarters | 50,000 | 55.56 |

| Expansion | Branding, marketing and promotional activities | 13,500 | 15 |

| Expansion | Business expansion to Sarawak and Singapore | 6,000 | 6.67 |

| Expansion | Capital expenditure on IT system and infrastructure | 4,000 | 4.44 |

| Expansion | Expansion of our workforce | 6,000 | 6.67 |

| Working capital | Working capital | 4,000 | 4.44 |

| Listing expenses | Estimated listing expenses | 6,500 | 7.22 |

| Total | 90,000 | 100 | |

Comparable Companies (Peers Similarity)

| Company | % | Source | Note |

|---|---|---|---|

| PARLO | 95 | IMR | Primary direct peer specializing in outbound group tours and wholesale travel distribution |

| AVI | 40 | AI | Operates similar Inbound/Outbound services, but major revenue is from Hotels with Travel only ~20% |

Utilisation of Proceeds

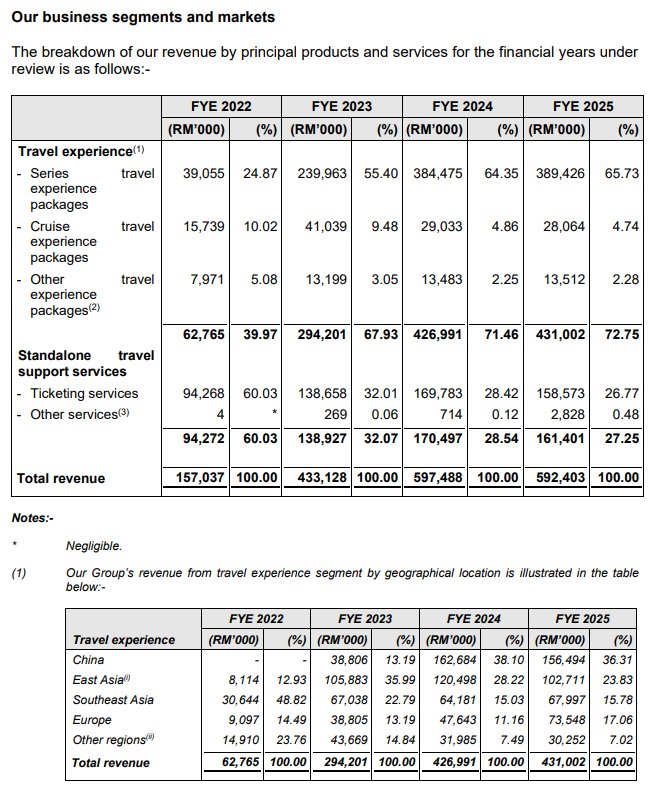

Business Segments

Geographical Segments

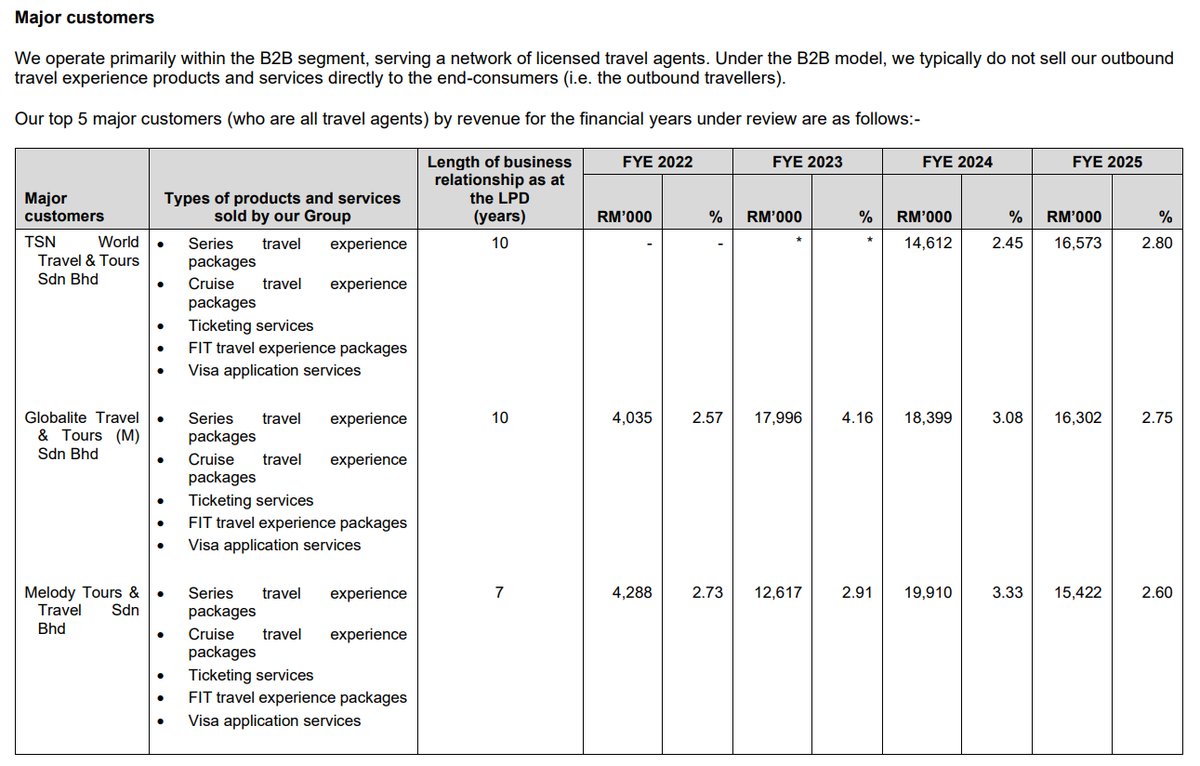

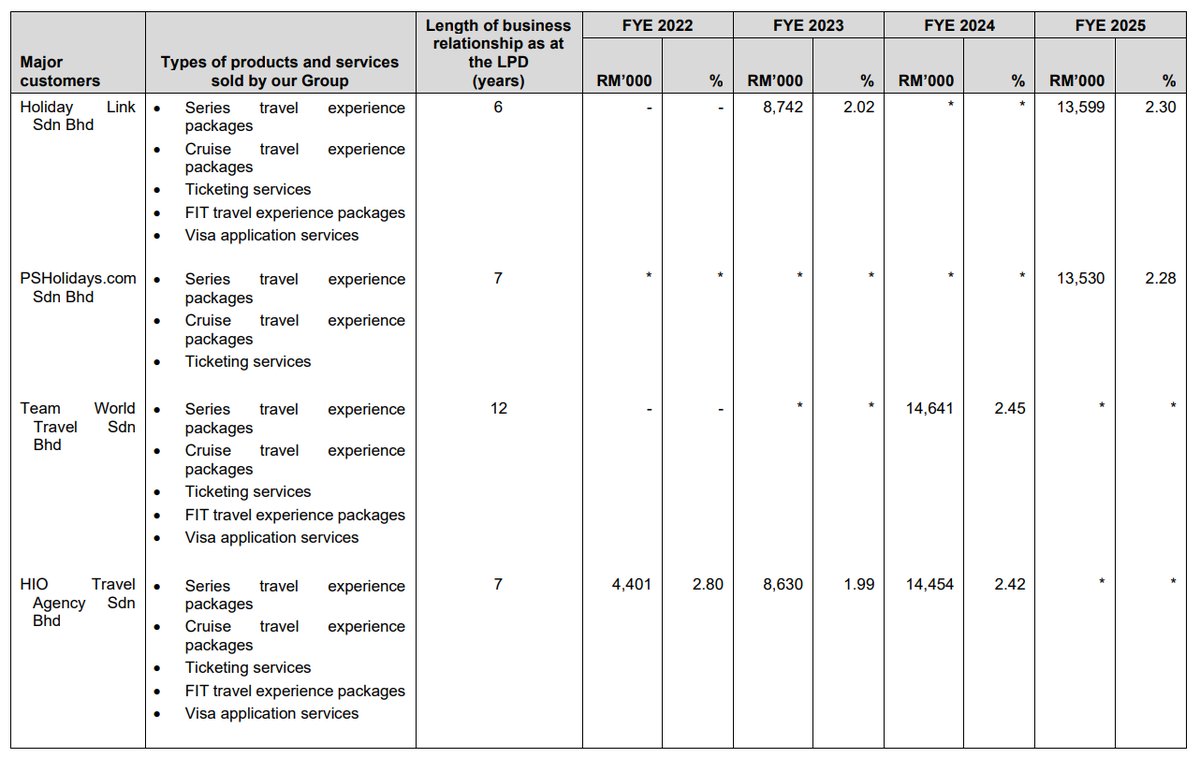

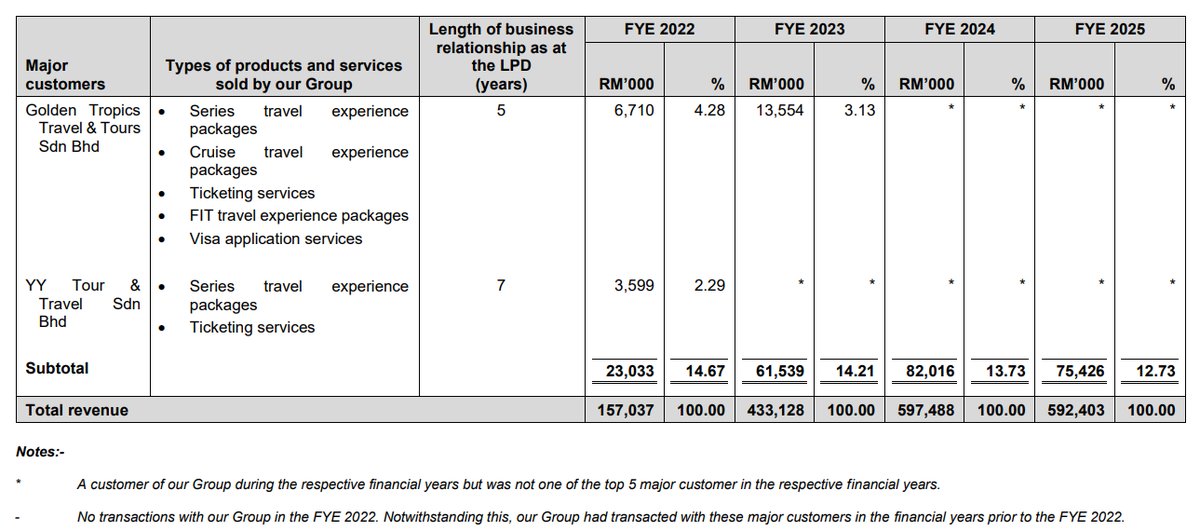

Major Customers

Profit After Tax (PAT) by Financial Year Ended

SWOT Analysis

Strengths

- Scalable B2B Model: GDGROUP utilizes a network of 848 licensed travel agents, allowing for national reach with minimal retail overhead and marketing costs compared to B2C models.

- Low Customer Concentration: The top 5 travel agent customers contribute only 12.73% of total revenue, insulating the company from the loss or price-pressure of any single partner.

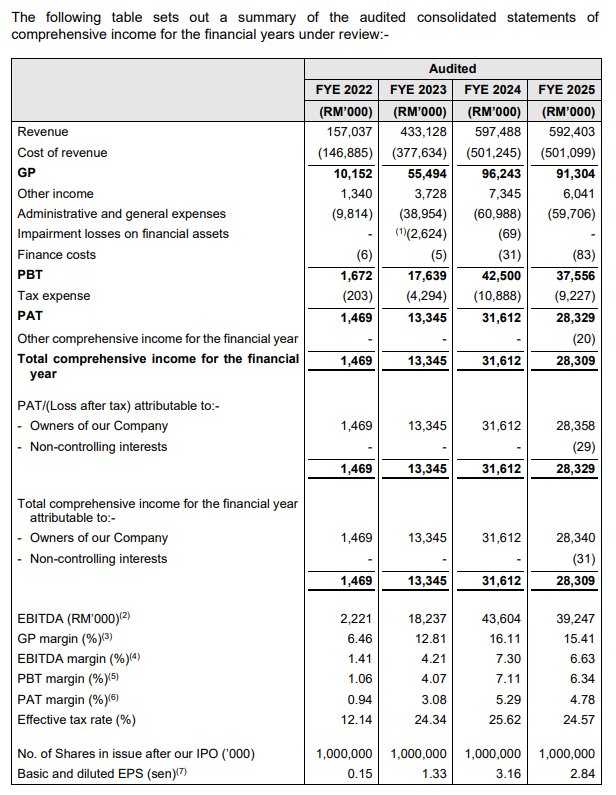

- Superior Peer Profitability: Unlike its primary listed peer Parlo Berhad (PARLO), which is loss-making, GDGROUP maintains a healthy PAT of RM28.3m, making it a stronger fundamental proxy for tourism.

Weaknesses

- Inefficient Capital Allocation: Allocation of 55.56% (RM50.0m) of IPO proceeds toward a new headquarters is a low-ROI use of capital for an asset-light service provider.

- Weak Cash Conversion: Operating cash flow plummeted 98% to RM1.01m in FYE2025 despite RM28.3m PAT, indicating heavy working capital absorption via supplier prepayments.

- Declining Profit Margins: GP margins fell from 16.11% to 15.41% in FYE2025 due to shifts in sales mix toward high-cost European tours and lower ticketing incentives.

Opportunities

- Singapore Market Entry: Expanding into Singapore allows the company to capitalize on a stronger currency and high outbound travel propensity among Singaporean consumers.

- AI Portal Integration: Planned IT infrastructure enhancements and AI integration into the B2B portal aim to capture higher wallet-share from agents via 'G-Stay' and 'GD Flight' services.

- Visa Policy Tailwinds: Bilateral visa exemptions, particularly for China, have already surged revenue contribution to 36.31%, showcasing an ability to benefit from favorable diplomatic policies.

Threats

- Geopolitical Macro Shocks: External tensions, such as Middle East conflicts, have historically triggered flight cancellations and immediate tour disruptions impacting millions in potential revenue.

- Digital Disintermediation Risk: The rise of Online Travel Agencies (OTAs) and generative AI itinerary planners threatens to bypass the B2B travel agents that GDGROUP relies on for distribution.

- FX/Fuel Volatility: Fluctuations in the Ringgit against the USD and RMB, alongside volatile airline fuel surcharges, pose constant risks to gross profit margins if costs cannot be passed on.

Key Highlights

Sorry, this feature only available for iSaham Pro

Conclusion

Sorry, this feature only available for iSaham Pro

Golden Destinations Group Berhad's Latest News