Adnex Group Berhad IPO's Analysis

Adnex Group Berhad

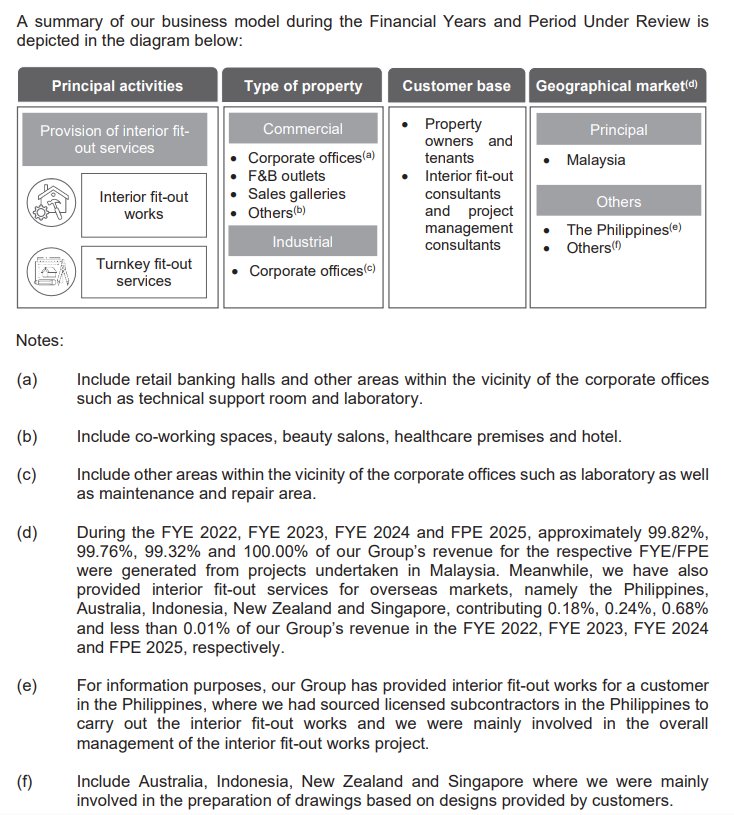

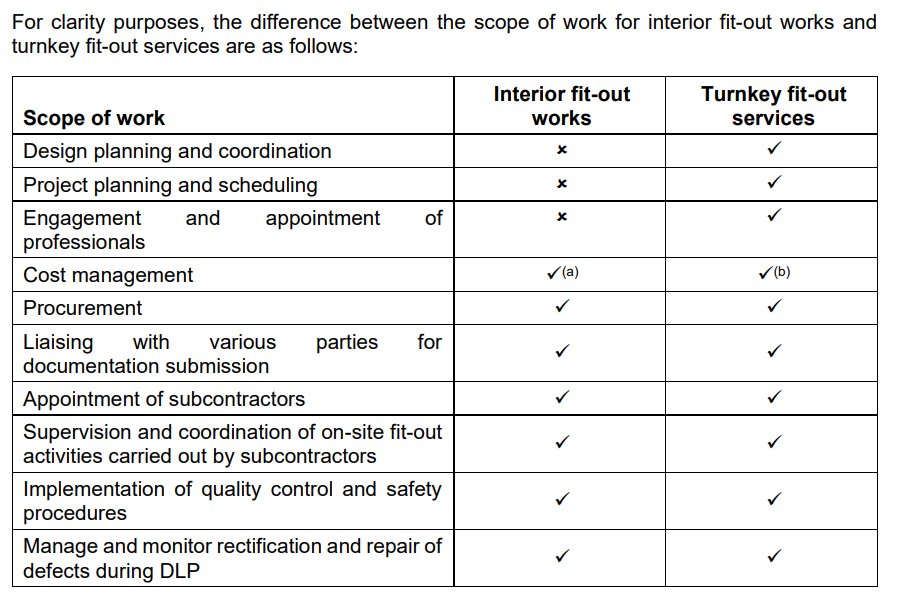

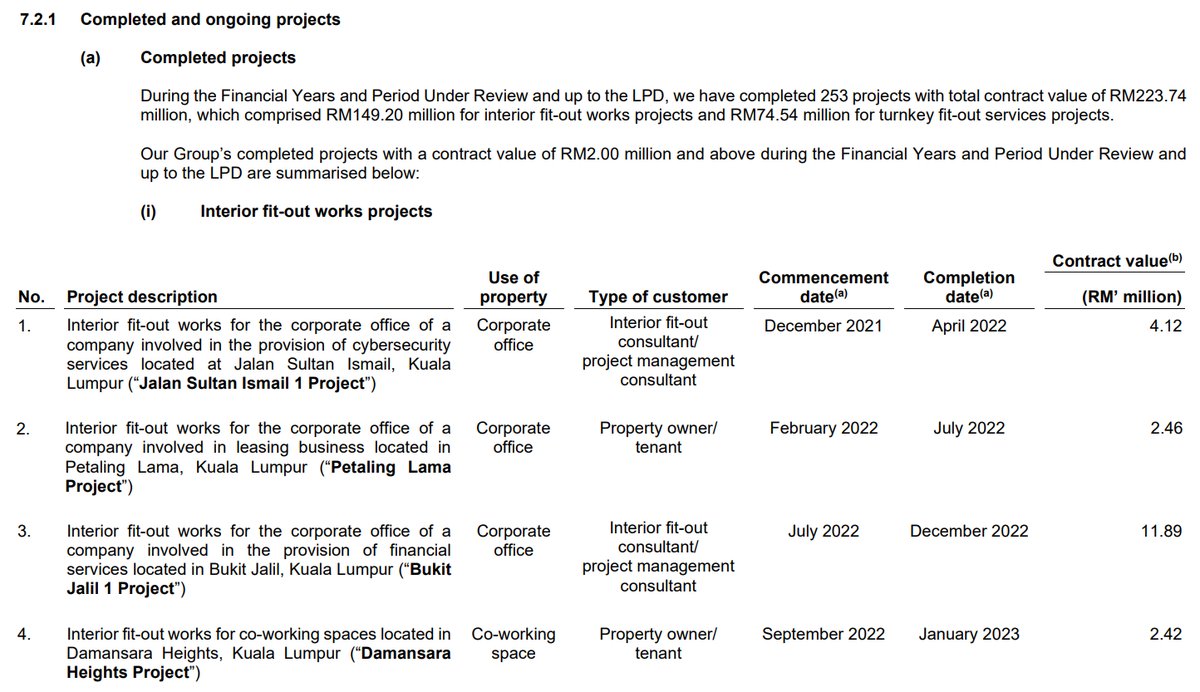

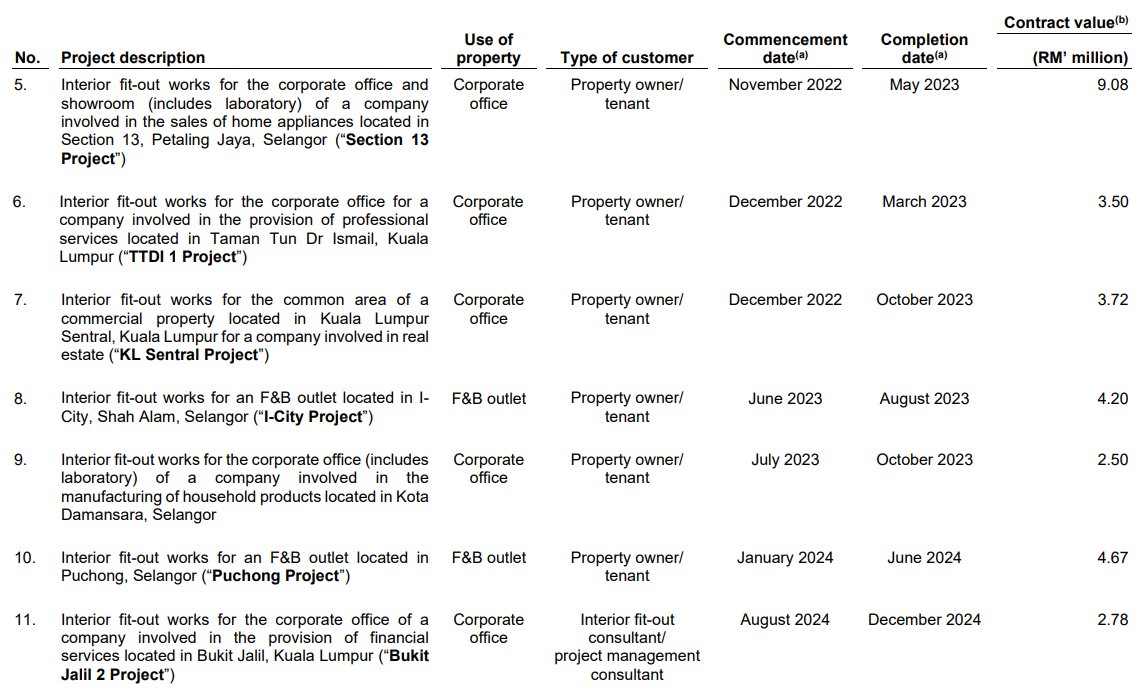

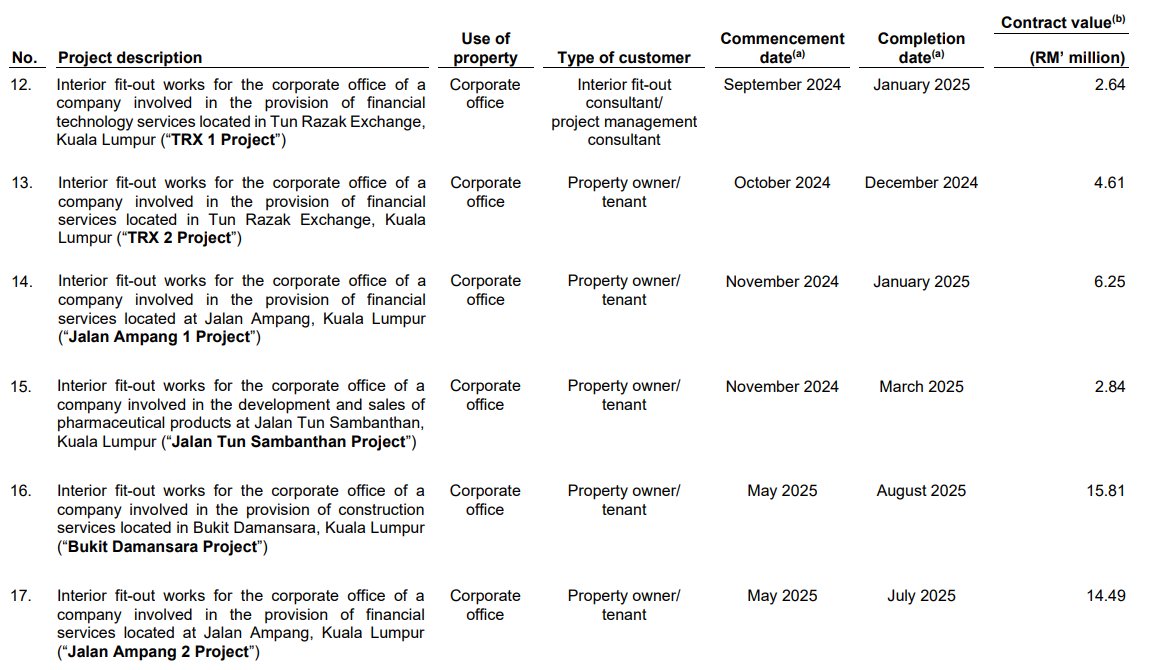

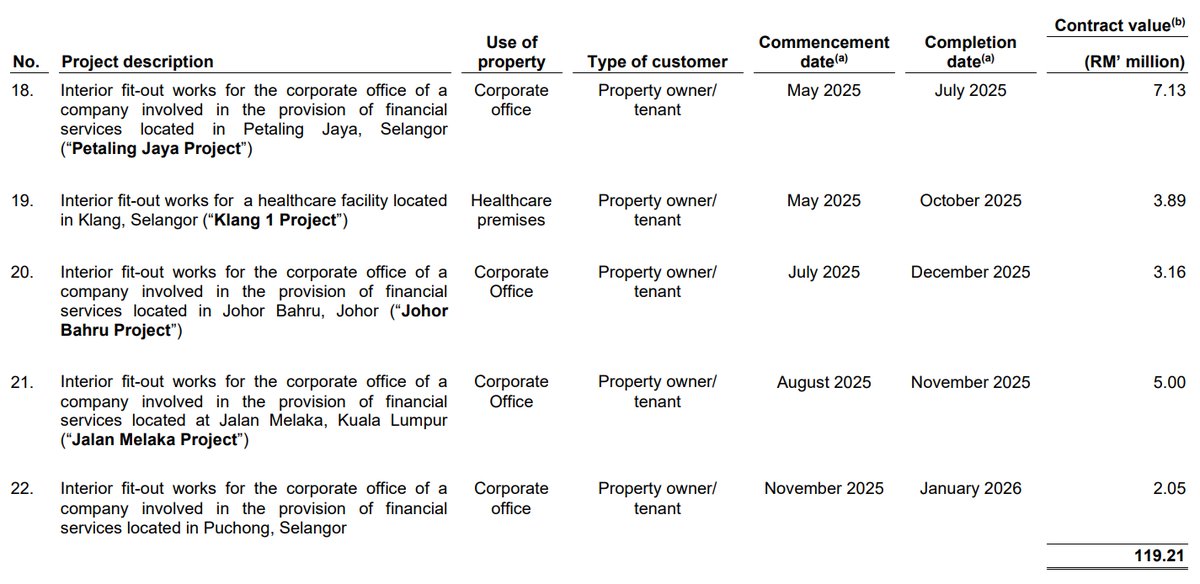

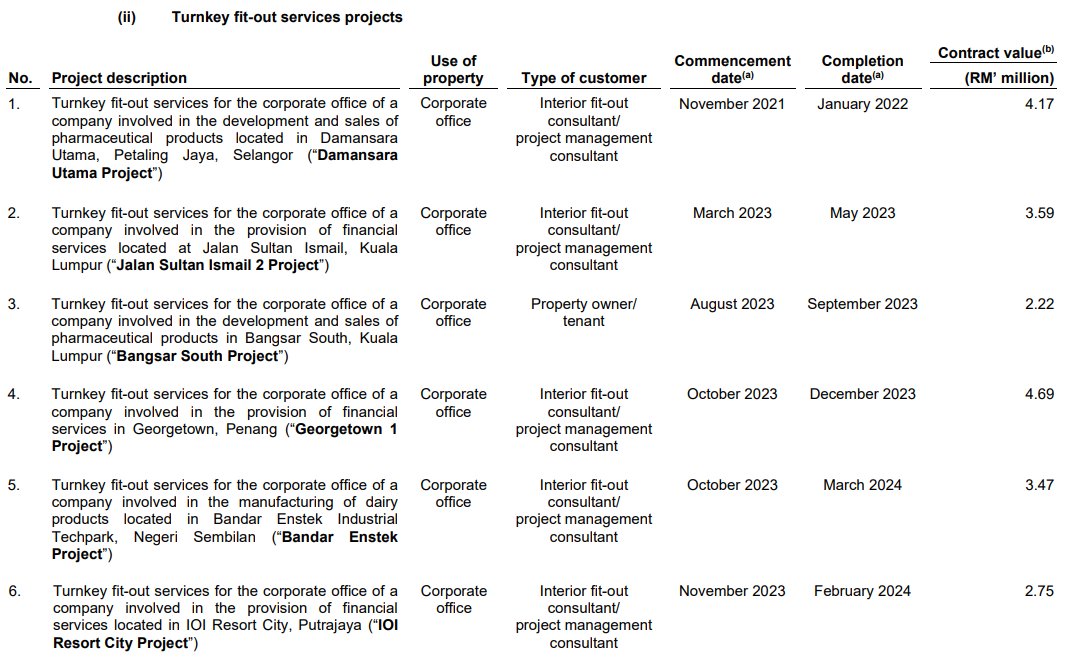

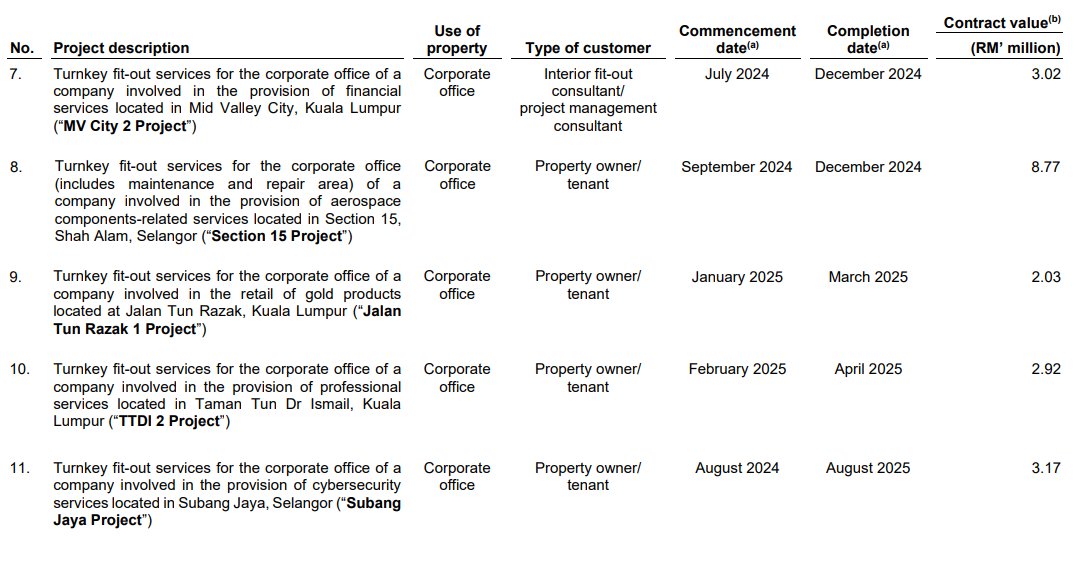

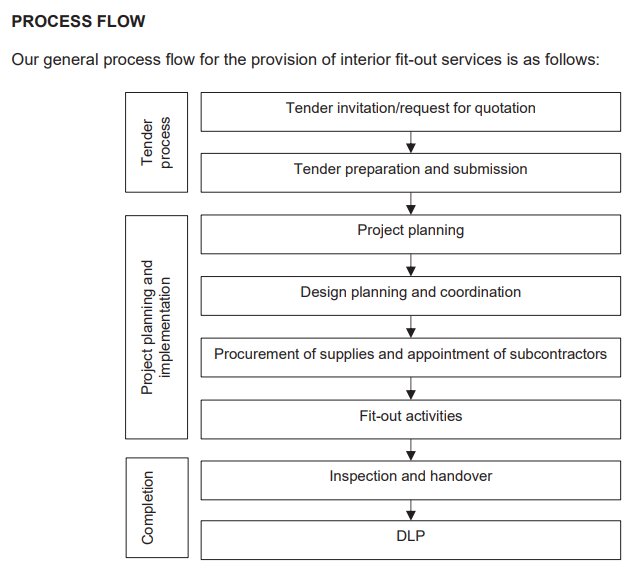

Adnex Group Berhad, through its subsidiaries, is principally involved in the provision of interior fit-out services in Malaysia. The Group specialises in providing these services for commercial and industrial properties, which are mainly used as corporate offices, food and beverage (F&B) outlets, and sales galleries. Its services encompass both interior fit-out works based on client-provided designs and comprehensive turnkey fit-out services, which cover the entire process from conceptual design to project completion. The company serves a diverse range of customers, including property owners, tenants, and project management consultants, across various industries such as financial services, manufacturing, and professional services. Adnex Group has also undertaken projects in overseas markets, including the Philippines, Australia, and Singapore.

IPO Details

- Construction (14.7)

Strategic Overview & Data Visuals

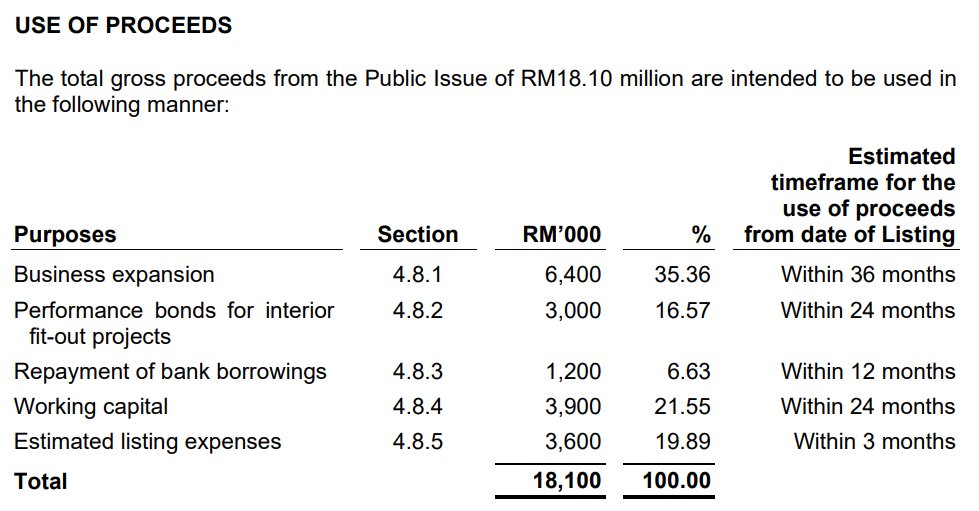

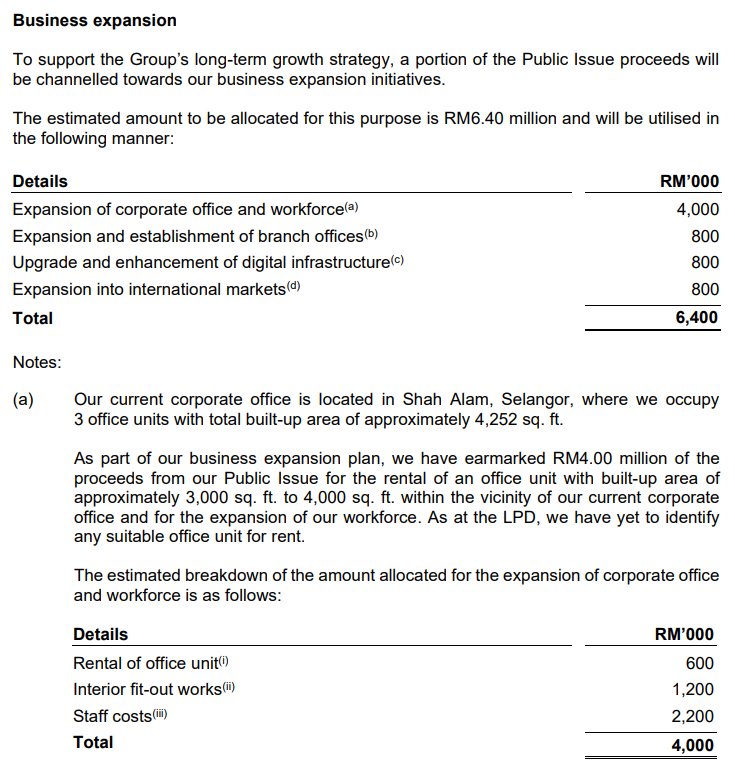

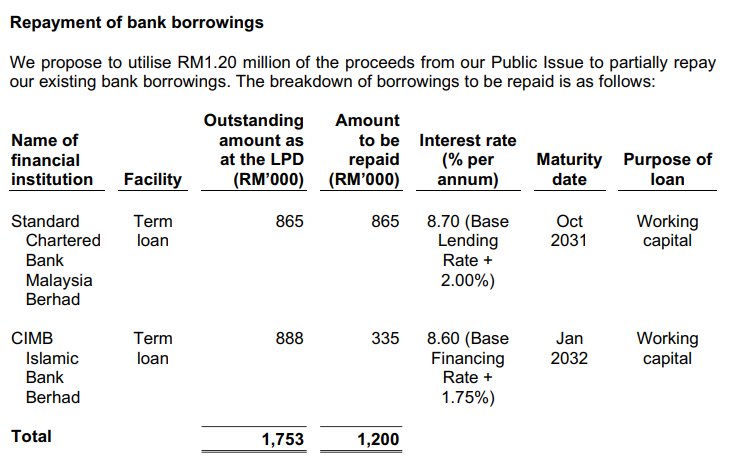

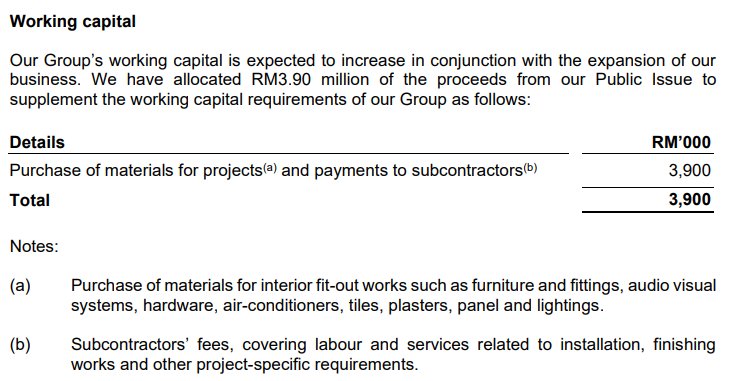

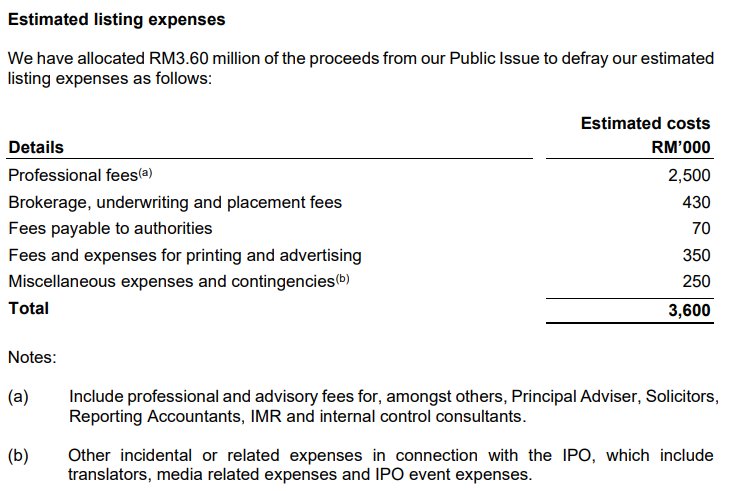

Utilisation of Proceeds

| Purpose | Amount (RM'000) | % | |

|---|---|---|---|

| Expansion | Business expansion | 6,400 | 35.36 |

| Working capital | Working capital | 3,900 | 21.55 |

| Others | Performance bonds for interior fit-out projects | 3,000 | 16.57 |

| Listing expenses | Estimated listing expenses | 3,600 | 19.89 |

| Debt | Repayment of bank borrowings | 1,200 | 6.63 |

| Total | 18,100 | 100 | |

Comparable Companies (Peers Similarity)

| Company | % | Source | Note |

|---|---|---|---|

| SAG | 95 | IMR | B2B commercial interior fit-out and turnkey services. |

| FIHB | 65 | IMR | Luxury hotel fit-out with in-house furniture manufacturing. |

| EXSIMHB | 50 | Researcher | Captive residential fit-out and hospitality management operator. |

Analyst Highlights

| Date | Analyst Highlights |

|---|---|

|

05-Mar-2026

Mercury |

|

|

04-Mar-2026

TA |

|

Utilisation of Proceeds

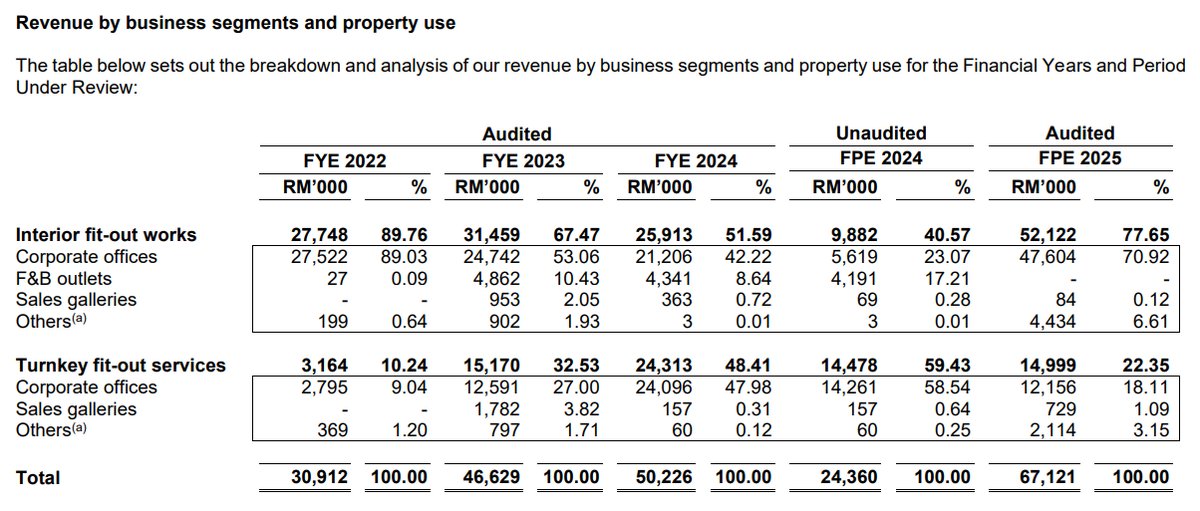

Business Segments

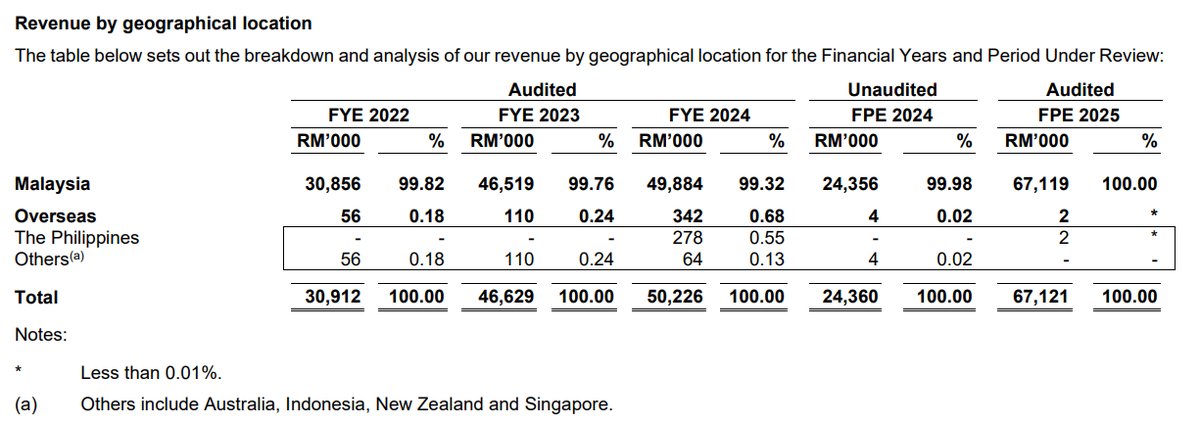

Geographical Segments

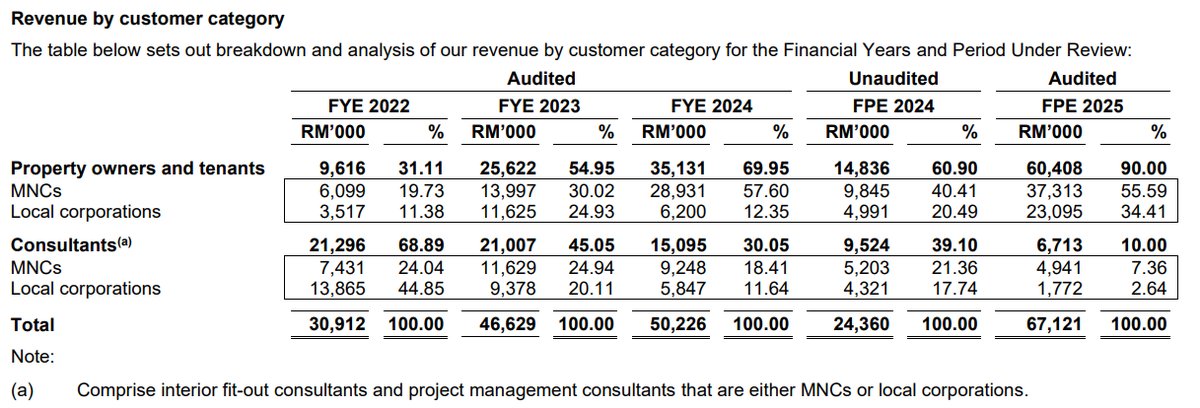

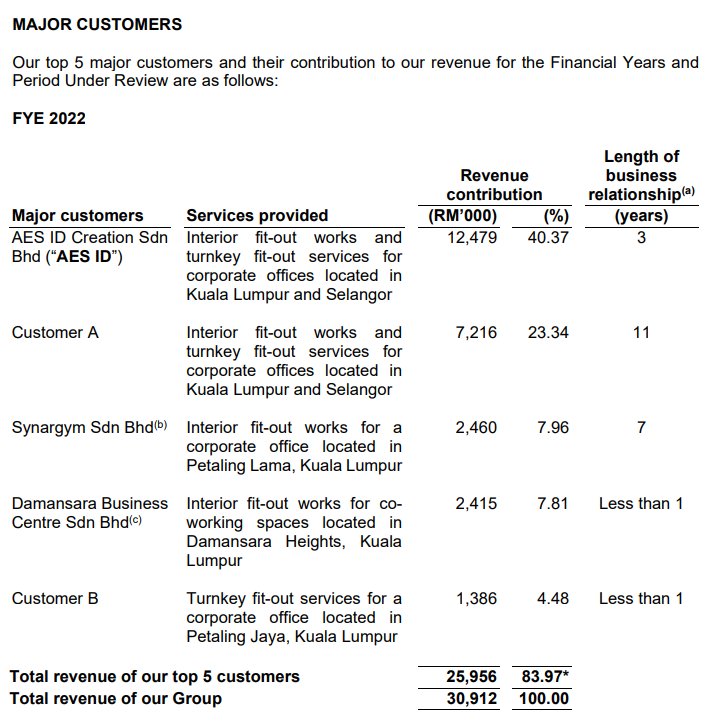

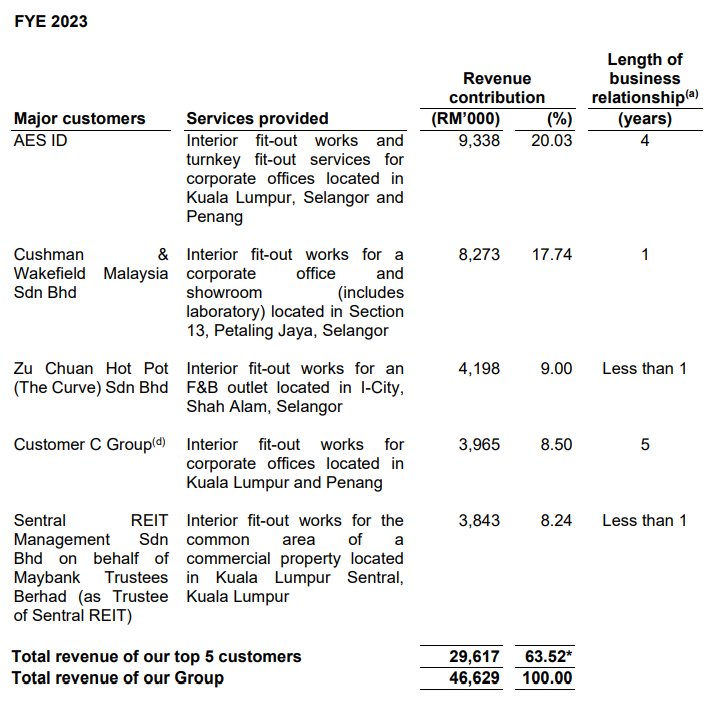

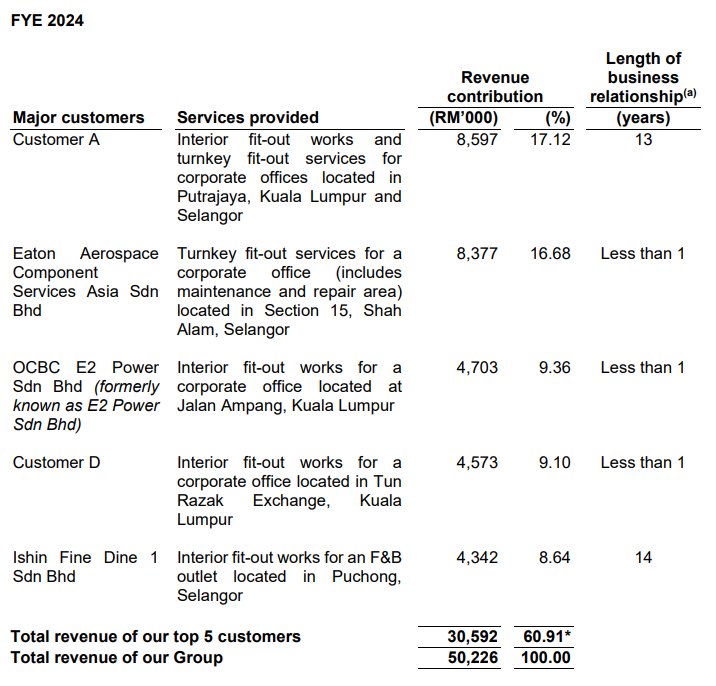

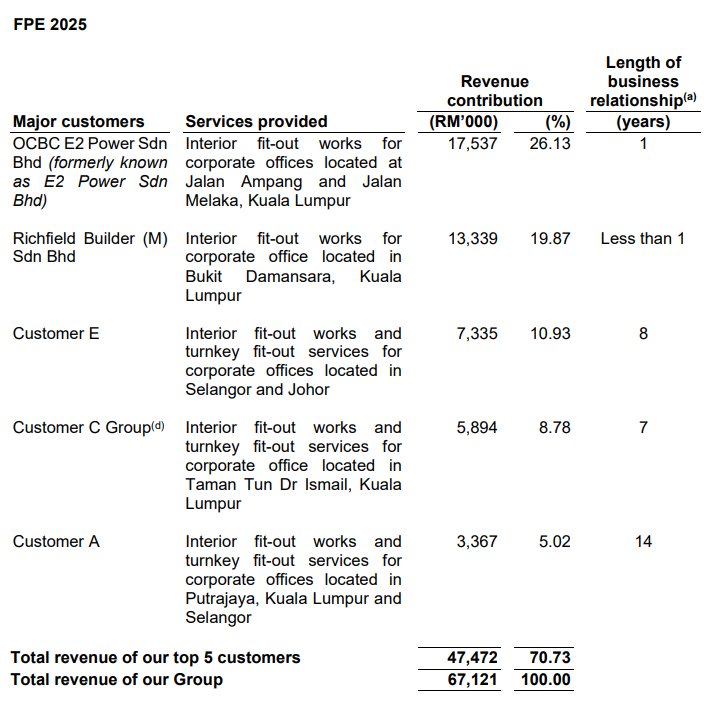

Major Customers

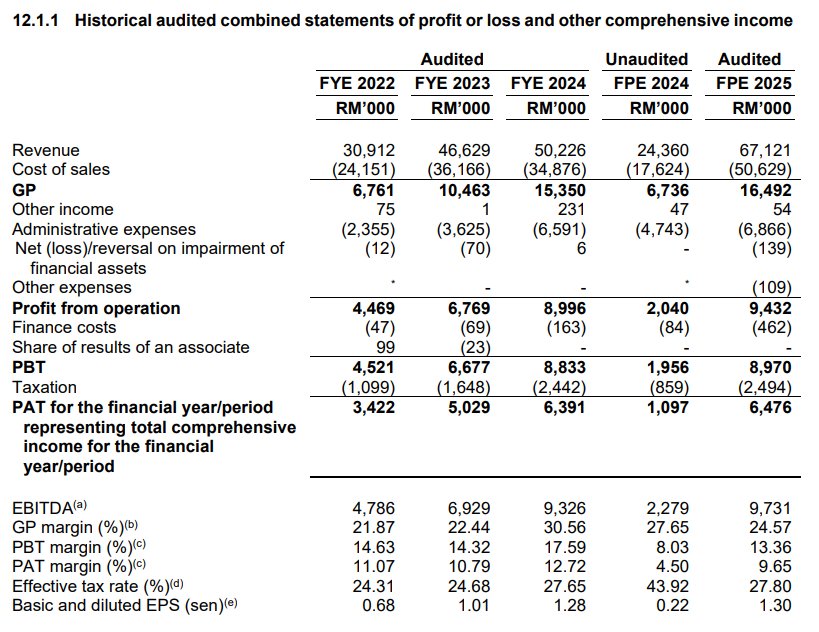

Revenue by Financial Year Ended

Profit After Tax (PAT) by Financial Year Ended

Revenue by Financial Period Ended

Profit After Tax (PAT) by Financial Period Ended

SWOT Analysis

Strengths

- High Growth Trajectory: Revenue for the first 9 months of FPE2025 (RM67.1m) has already surpassed the full-year FY2024 revenue, indicating explosive momentum and successful project execution.

- Strong MNC Clientele: Serving a growing list of 28 Multi-National Corporations, up from 13 in FY22, which validates execution quality and reduces counterparty payment risk.

- Asset-Light Model: High reliance on subcontractors (approx. 77% of costs) enables operational flexibility and scalability without the burden of heavy fixed overheads.

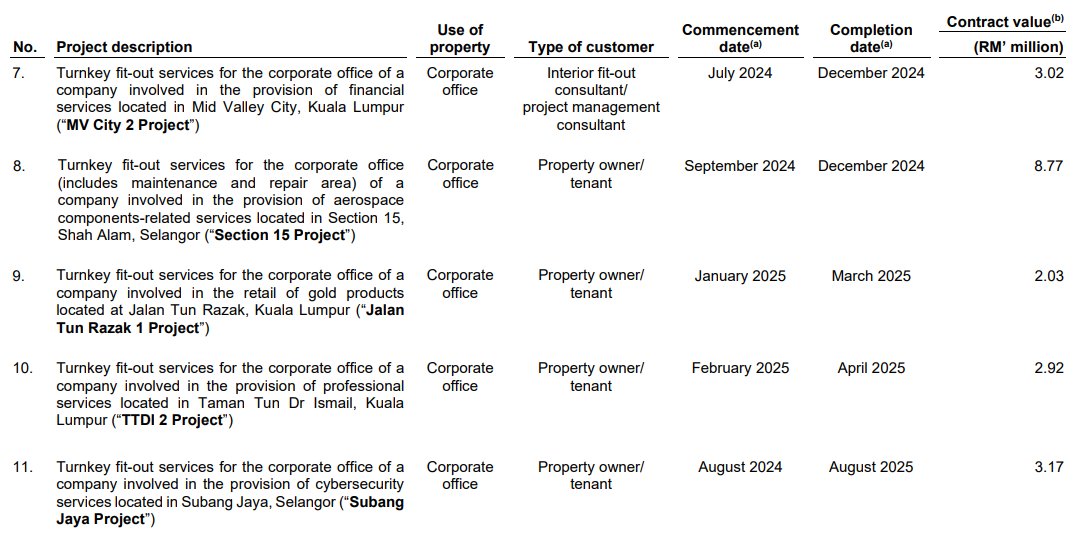

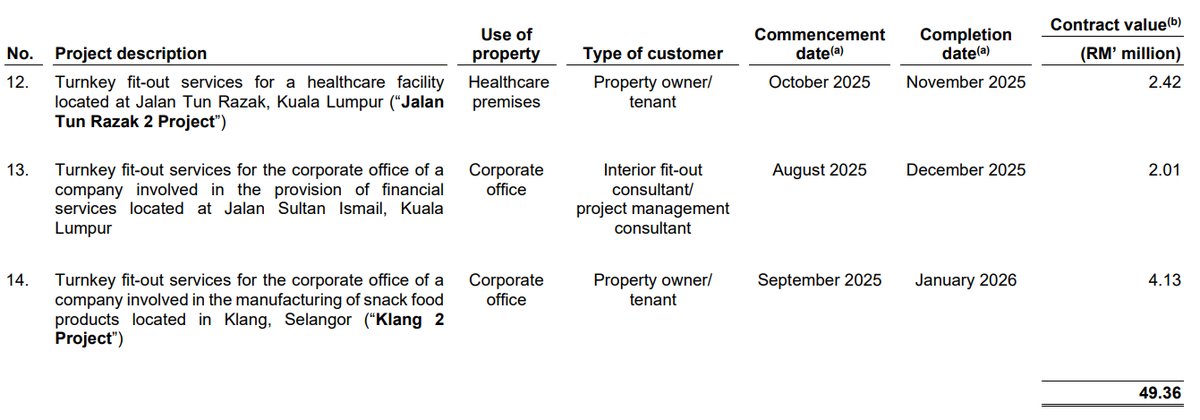

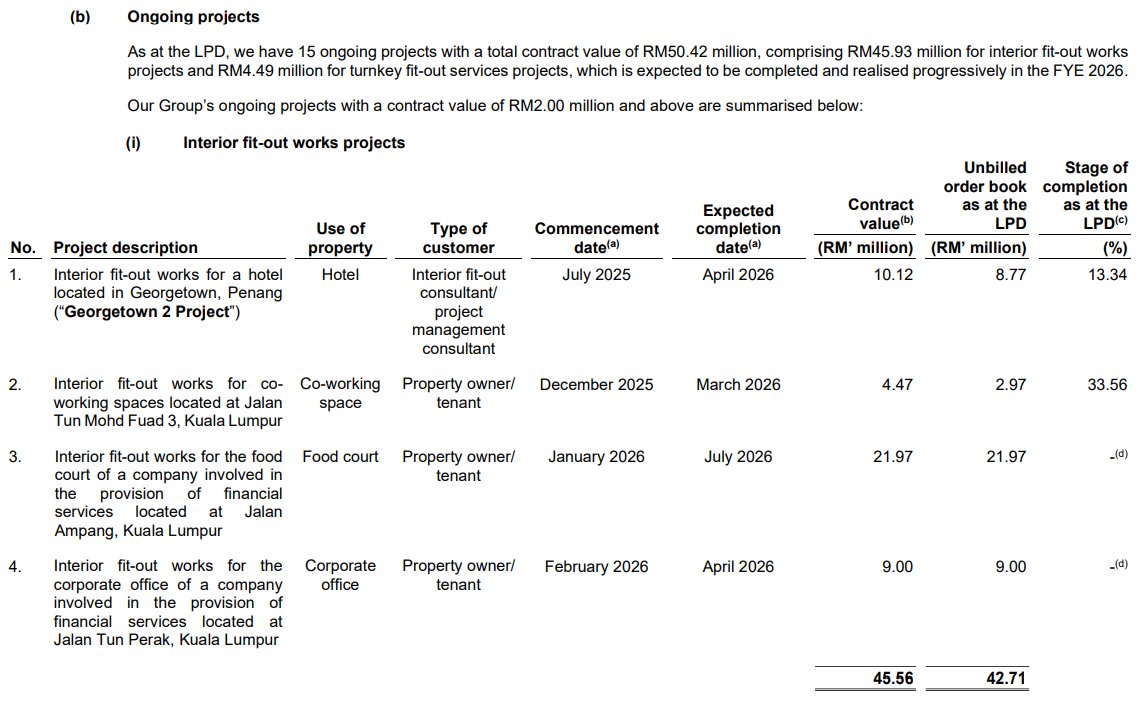

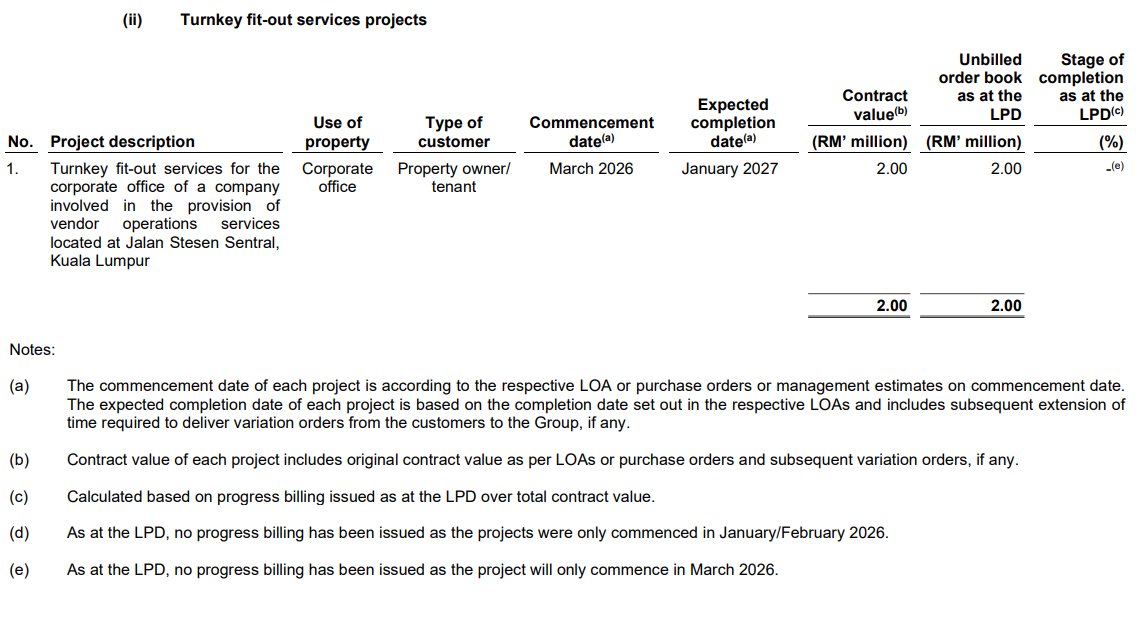

- Healthy Orderbook: An unbilled orderbook of RM66.3 million provides a 1.32x cover on FY2024 revenue, ensuring clear earnings visibility for the upcoming year.

Weaknesses

- Customer Concentration: The top 5 customers contribute a significant 60-80% of total revenue, posing a considerable risk to earnings if a key account is lost.

- Short Project Cycles: Projects have short tenures of 2-6 months, requiring constant and successful replenishment of the orderbook to sustain revenue momentum.

Opportunities

- Rising FDI Inflow: Increased foreign direct investment into Malaysia, particularly for data centers and regional HQs, directly drives demand for high-specification corporate office fit-outs.

- Regional Expansion: Planned entry into the Philippines and Indonesia markets presents a significant new avenue for growth beyond the domestic market.

- Green Building Demand: Growing corporate demand for sustainable and LEED-certified office spaces creates a niche market opportunity that aligns with the company's capabilities.

Threats

- Economic Cyclicality: As office fit-outs are discretionary corporate spending, an economic slowdown could lead to project delays or budget cuts, directly impacting revenue.

- Input Cost Volatility: Fluctuations in material prices and subcontractor labour costs could compress margins, especially on contracts that are fixed-price.

- Subcontractor Reliability: Heavy dependence on subcontractors means any failure on their part to deliver on quality or time directly impacts Adnex's project execution and reputation.

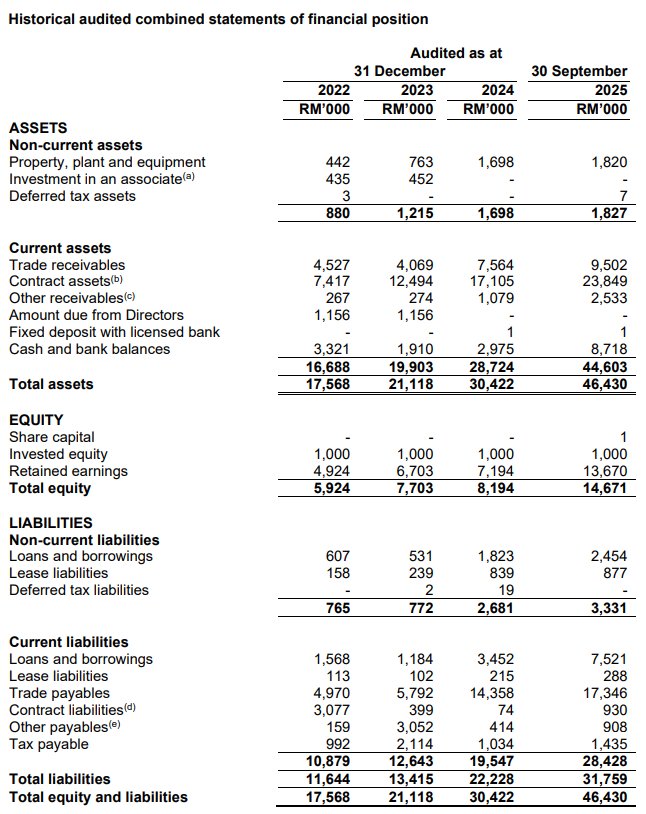

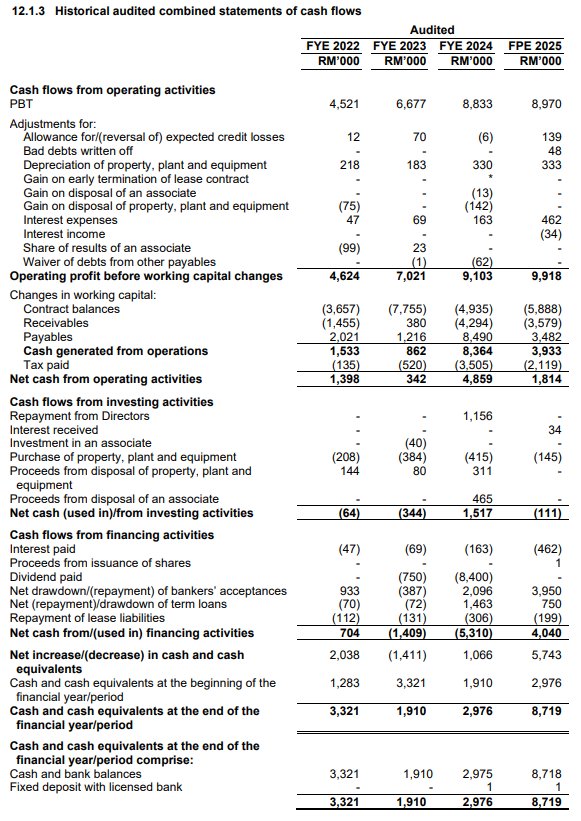

Key Highlights

Sorry, this feature only available for iSaham Pro

Conclusion

Sorry, this feature only available for iSaham Pro

Adnex Group Berhad's Latest News