SBS Nexus Berhad IPO's Analysis

SBS Nexus Berhad

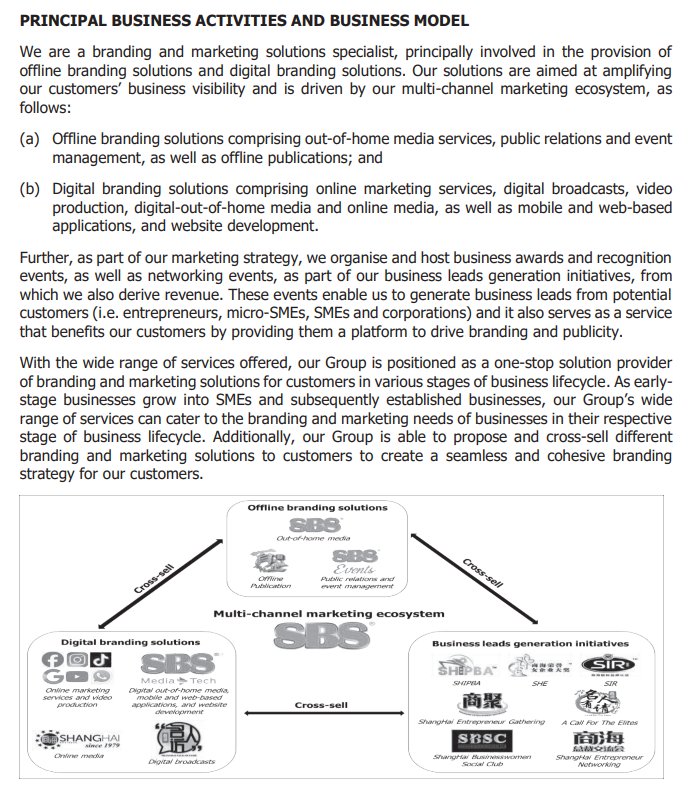

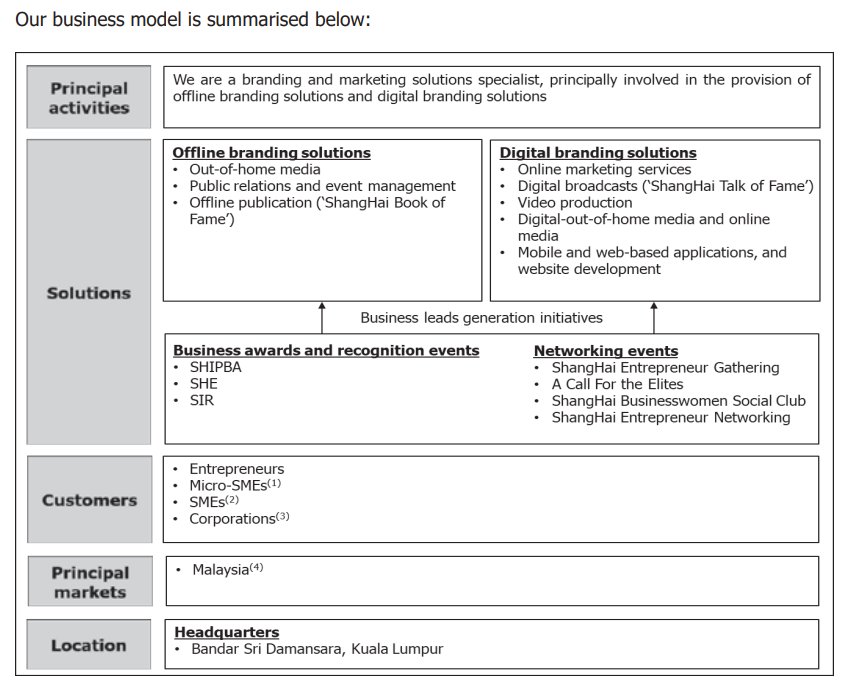

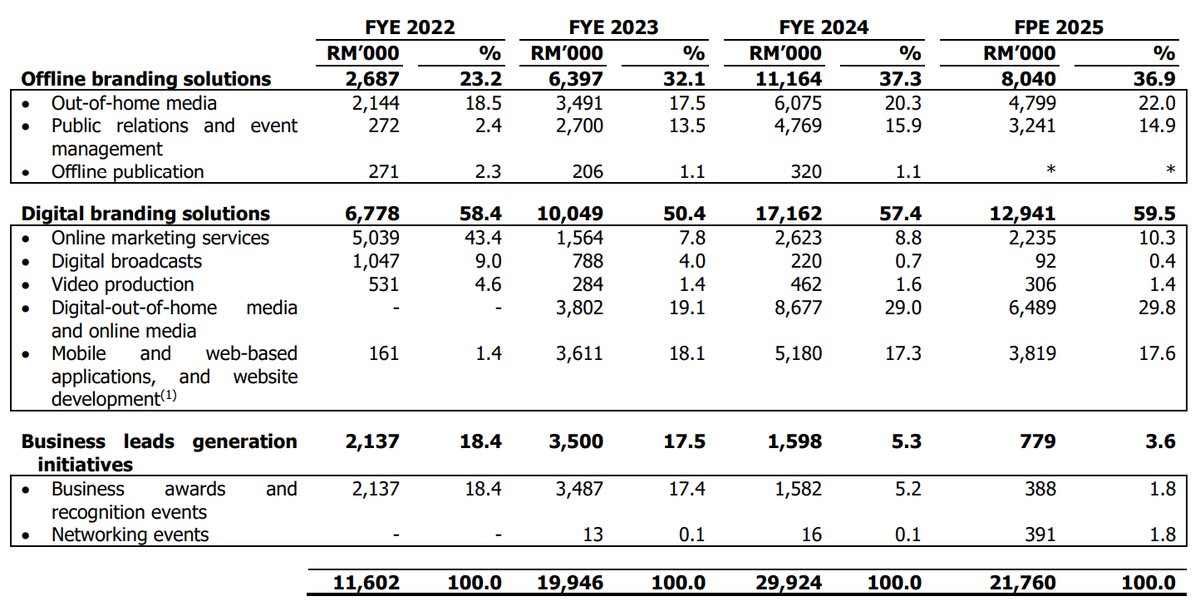

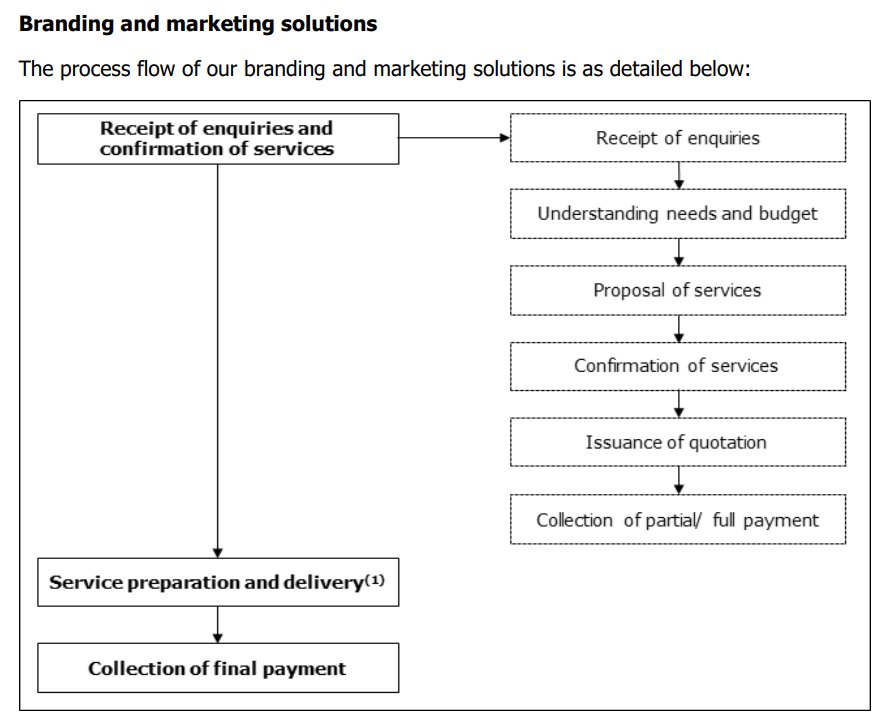

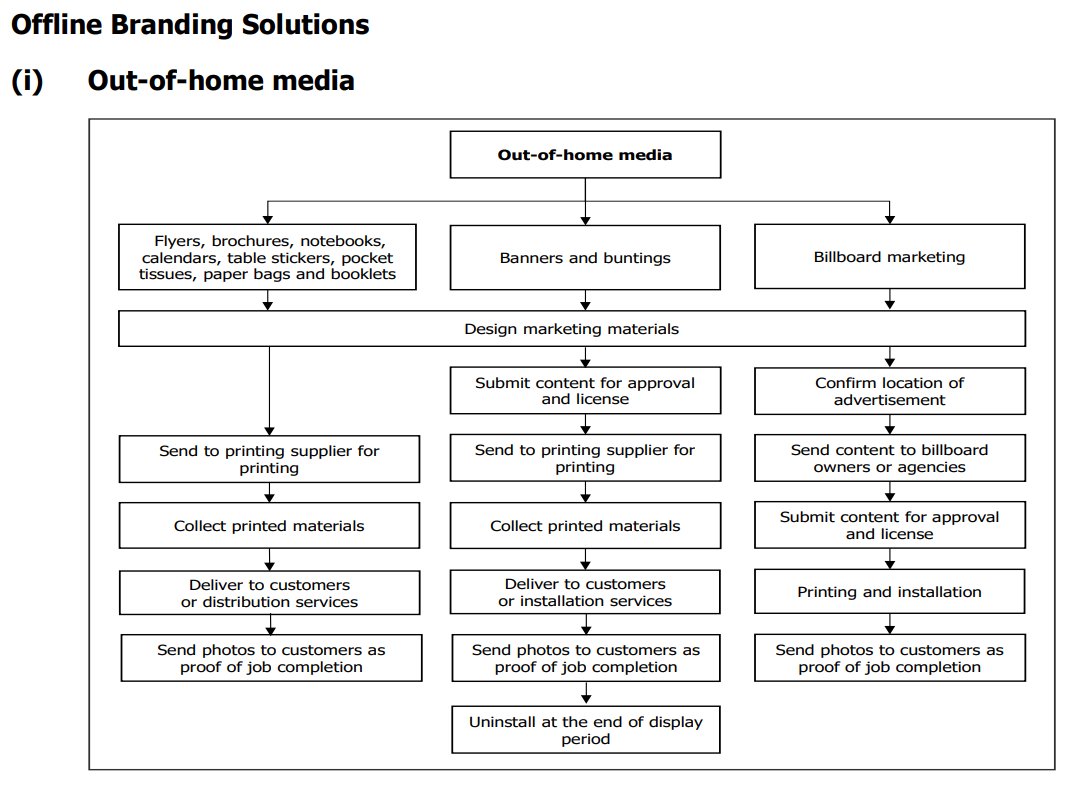

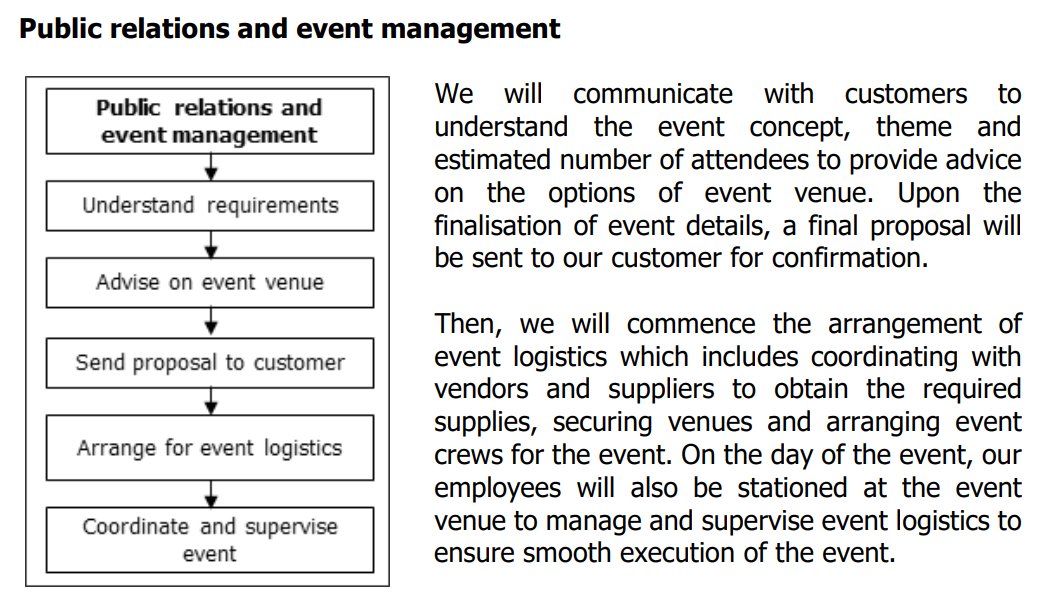

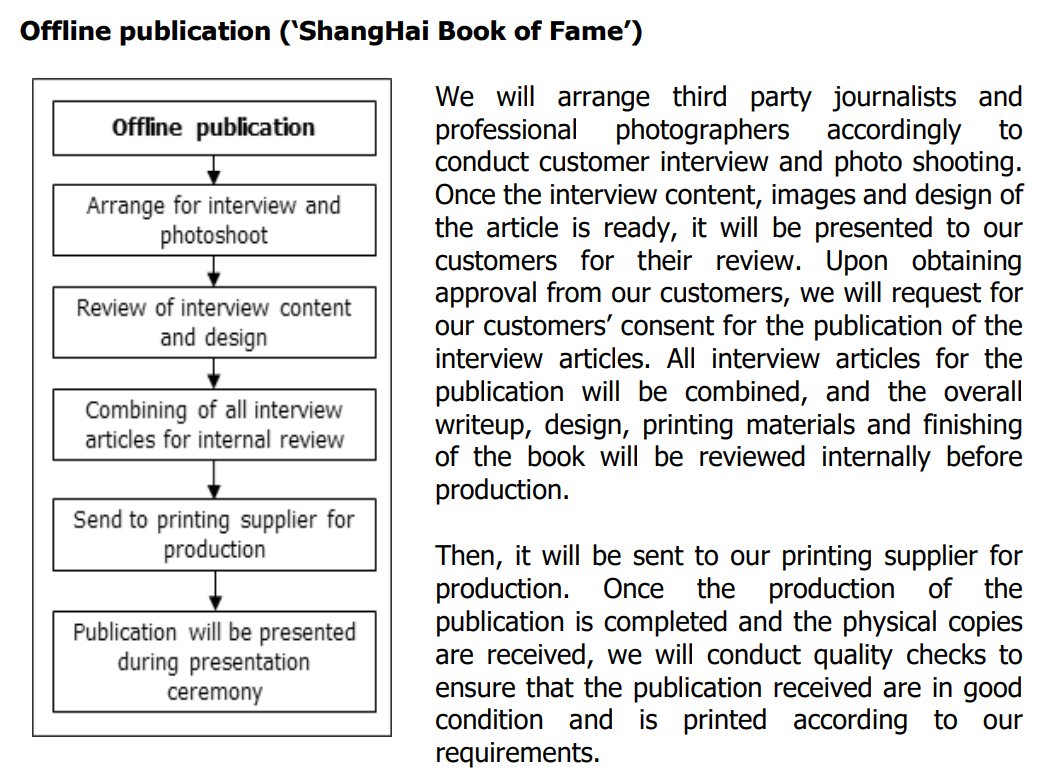

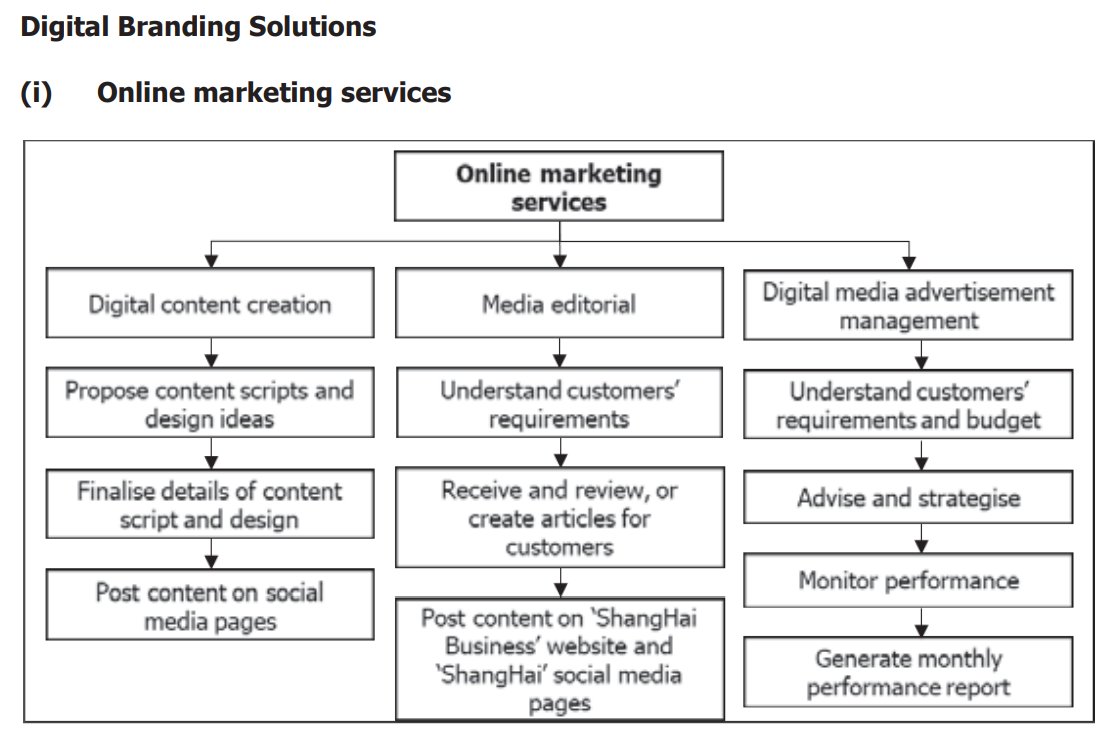

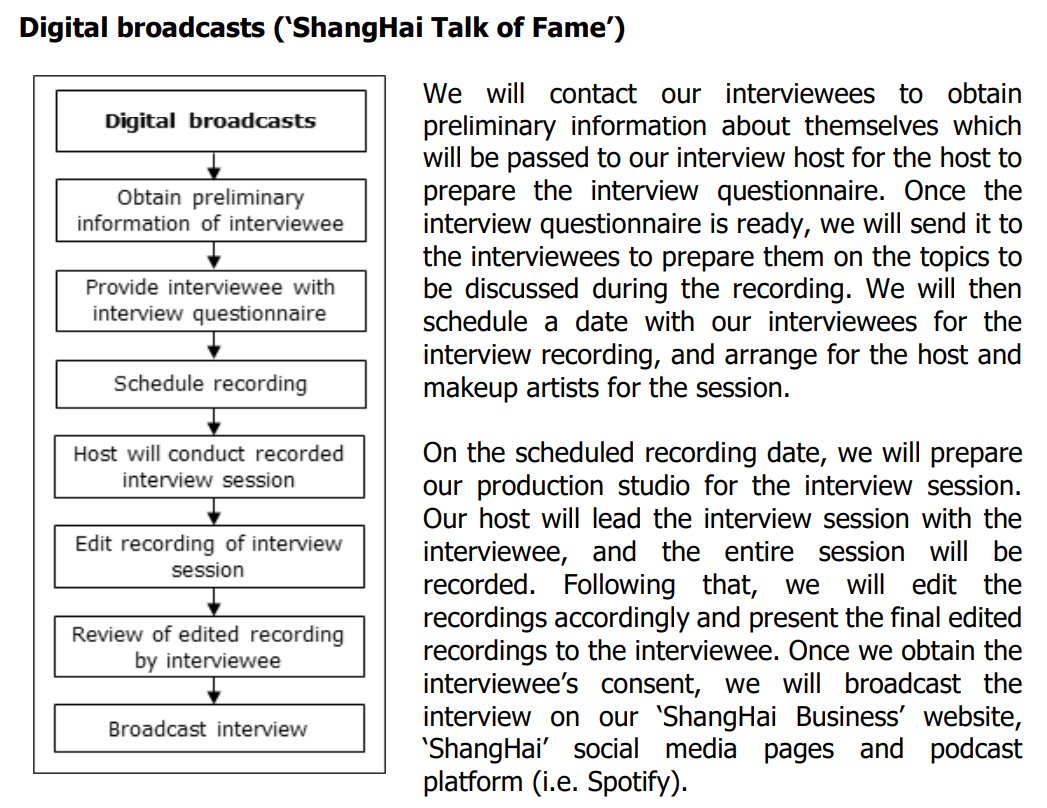

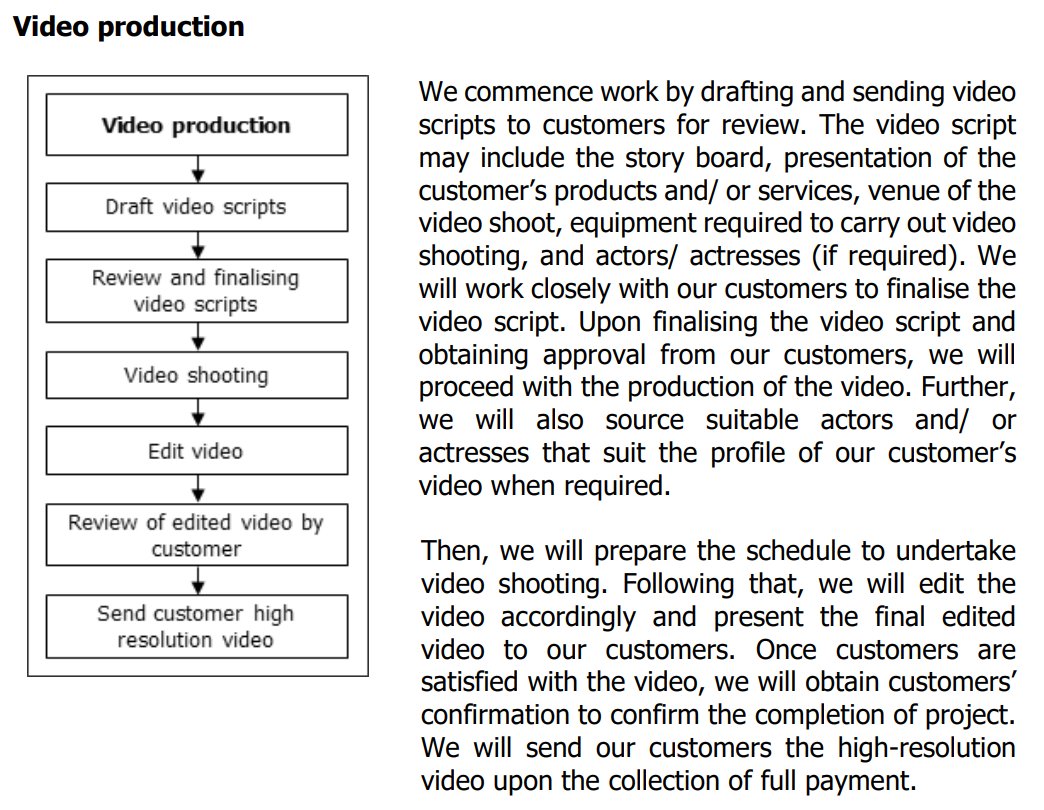

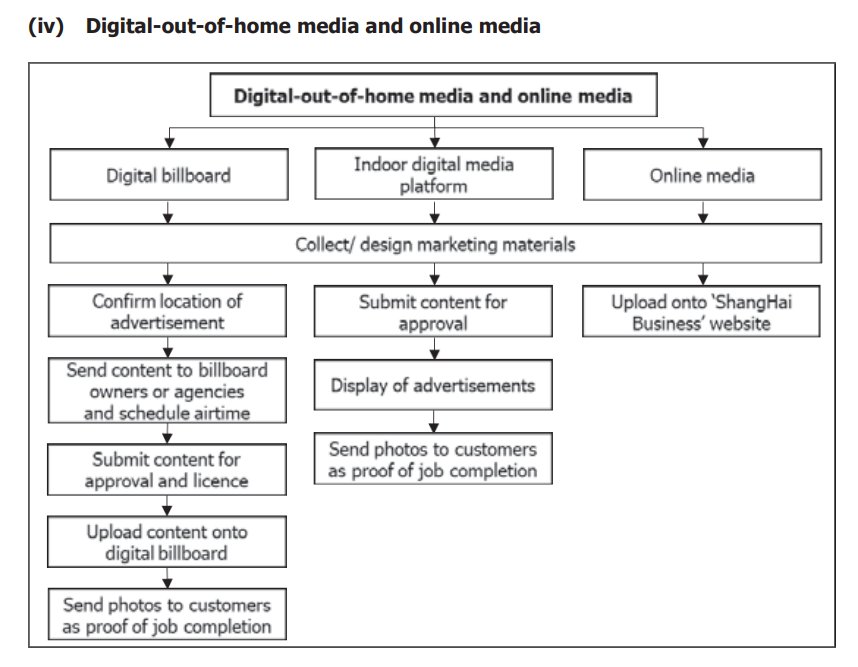

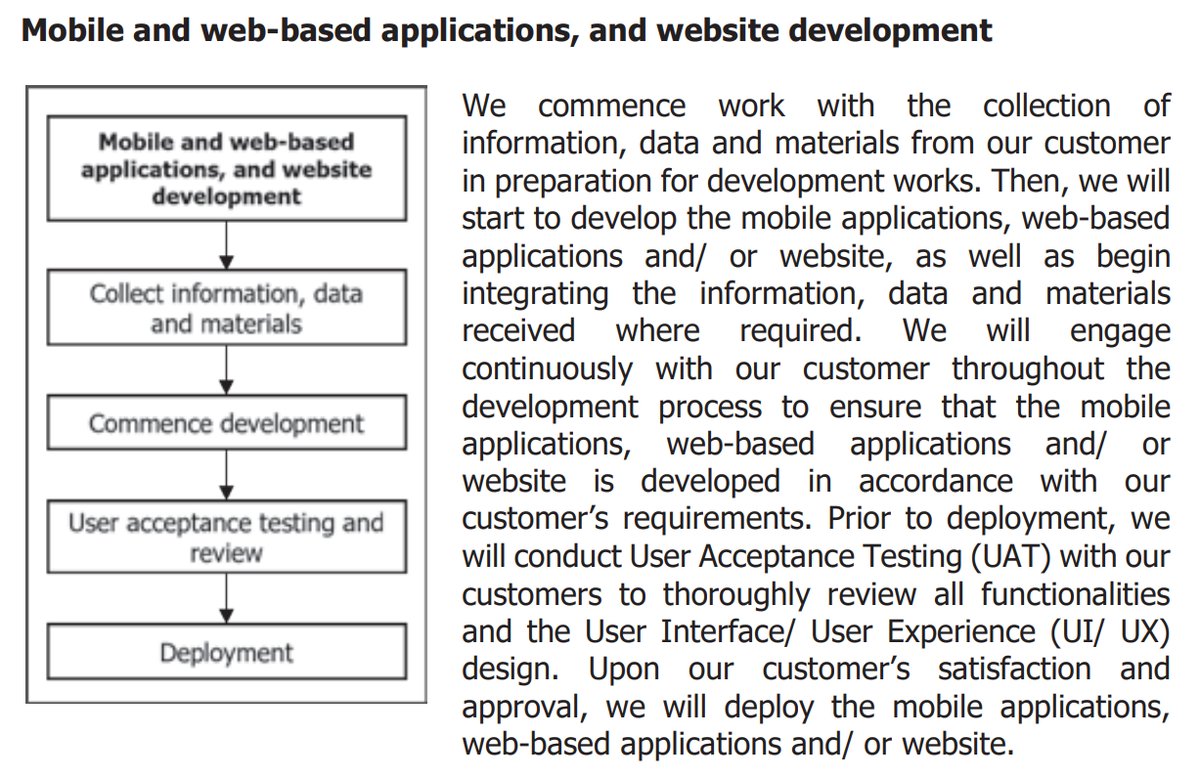

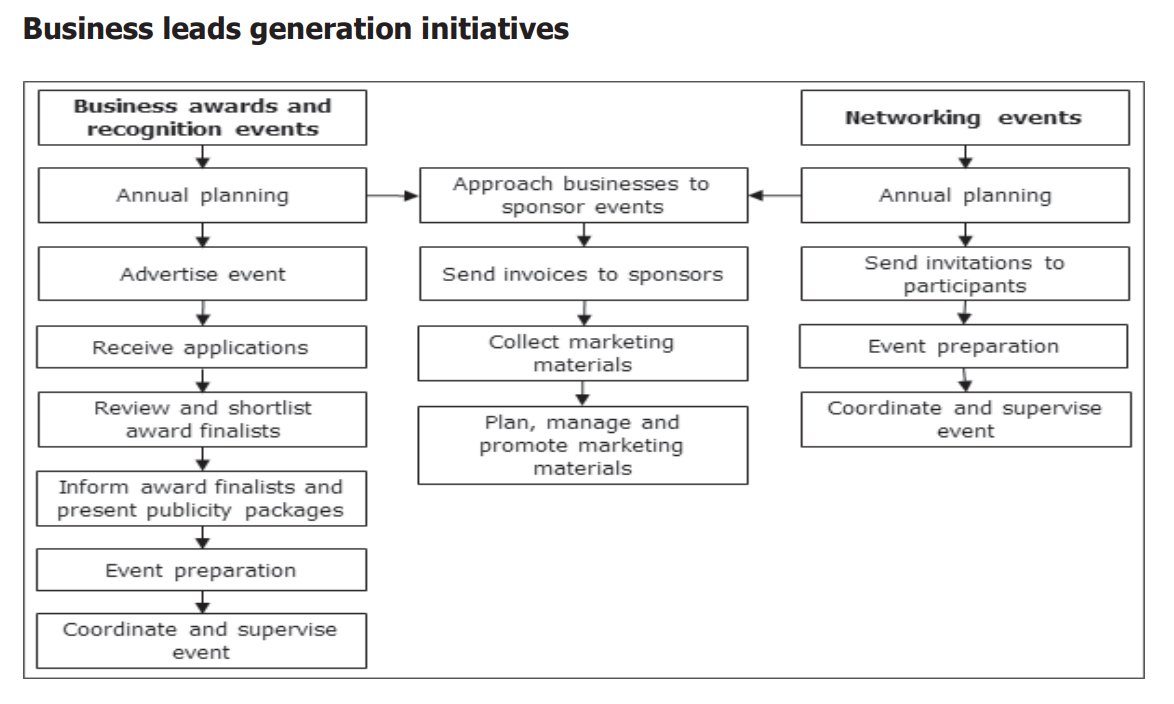

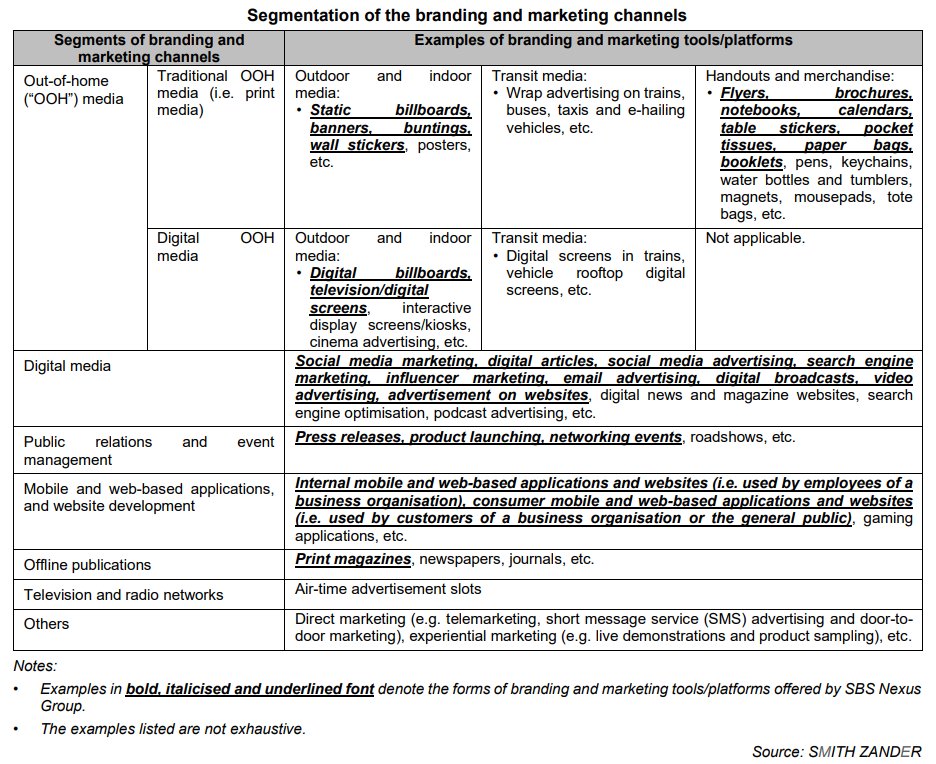

SBS Nexus Berhad is a branding and marketing solutions specialist based in Malaysia. Through its subsidiaries, the company provides offline branding solutions (including out-of-home media, public relations, event management, and offline publications) and digital branding solutions (including online marketing, digital broadcasts, video production, digital out-of-home media, and mobile/web application development). The group also organises business awards and networking events under its 'ShangHai' brand to generate business leads.

IPO Details

Market:

ACE

Principal Adviser:

M & A Securities Sdn Bhd

Issuing House:

Tricor Investor & Issuing House (TIIH)

Shariah Status:

SC (Yes)

Listing Price:

0.25

MITI allocation?:

Yes

Closing Date:

07-Jan-2026

Balloting Date:

09-Jan-2026

Listing Date:

20-Jan-2026

Oversubscription rate:

22.28x

Average Analysts FV

:

Mplus (0.34), Public Invest (0.27), TA (0.29), RHB (0.31)

iSaham IPO Score

:

Market Cap:

122.50 M

Number of Shares:

490.00 M

( info)

Median Sectors PE:

N/A

Median Peers PE:

Strategic Overview & Data Visuals

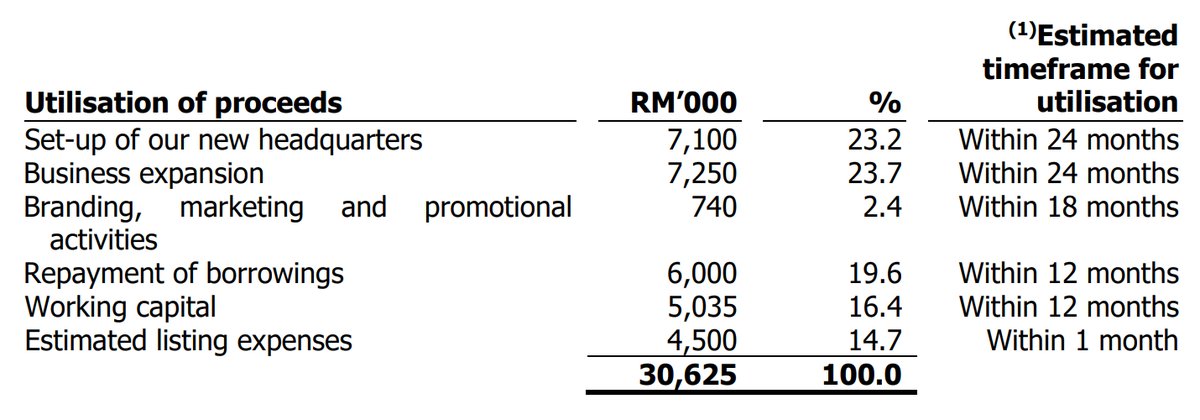

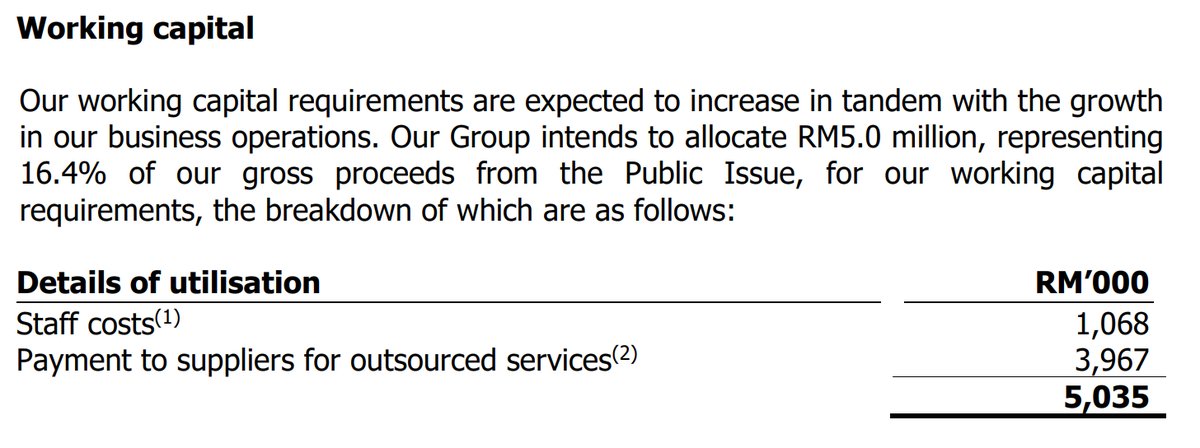

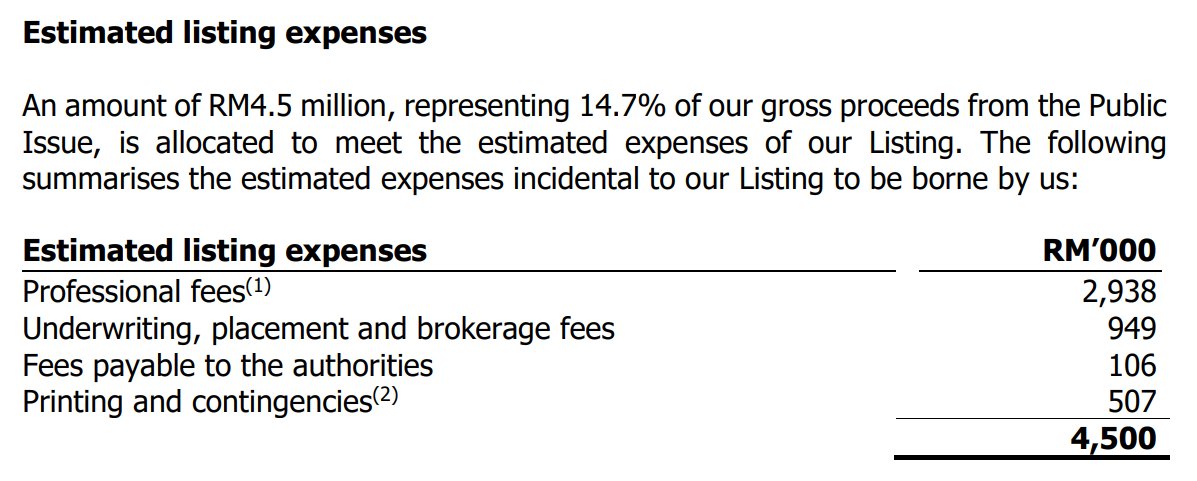

Utilisation of Proceeds

| Purpose | Amount (RM'000) | % | |

|---|---|---|---|

| Expansion | Set-up of our new headquarters | 7,100 | 23.2 |

| Expansion | Business expansion | 7,250 | 23.7 |

| Working capital | Branding, marketing and promotional activities | 740 | 2.4 |

| Working capital | Working capital | 5,035 | 16.4 |

| Listing expenses | Estimated listing expenses | 4,500 | 14.7 |

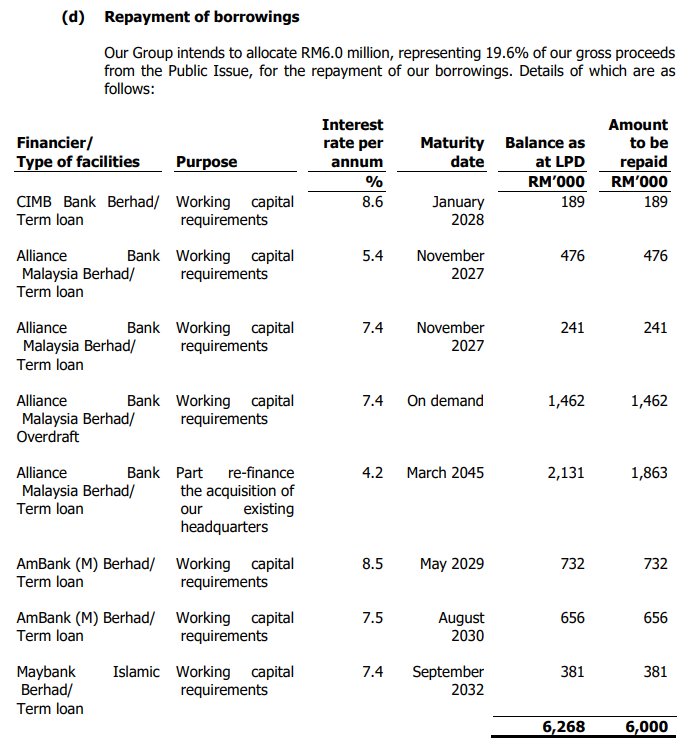

| Debt | Repayment of borrowings | 6,000 | 19.6 |

| Total | 30,625 | 100 | |

Analyst Highlights

| Date | Analyst Highlights |

|---|---|

|

07-Jan-2026

RHB |

|

|

06-Jan-2026

TA |

|

|

05-Jan-2026

Public Invest |

|

|

05-Jan-2026

Mplus |

|

Utilisation of Proceeds

Business Segments

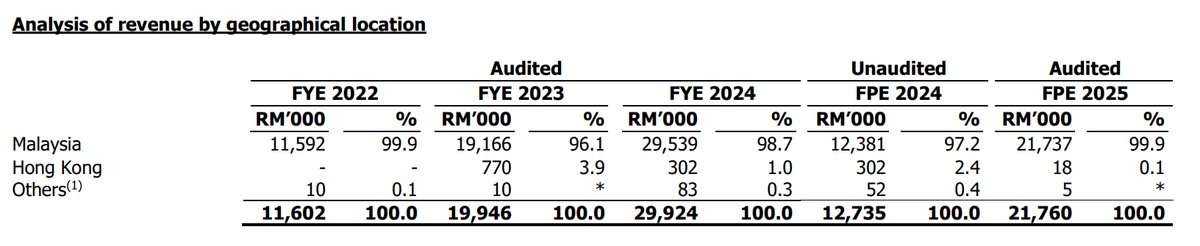

Geographical Segments

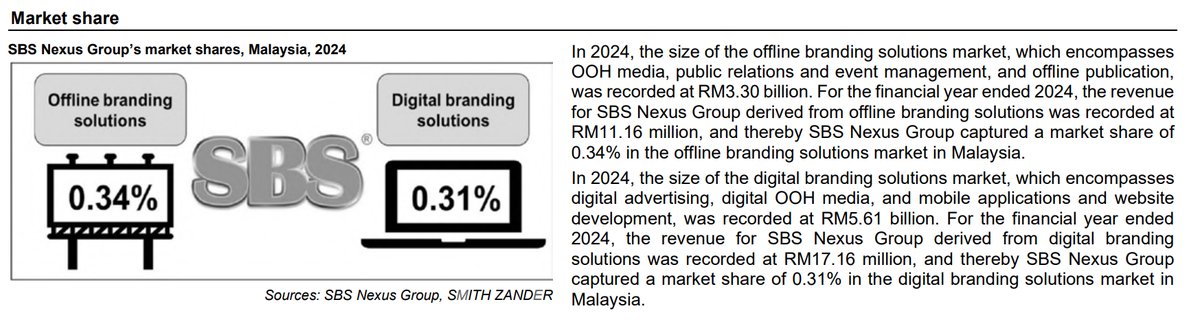

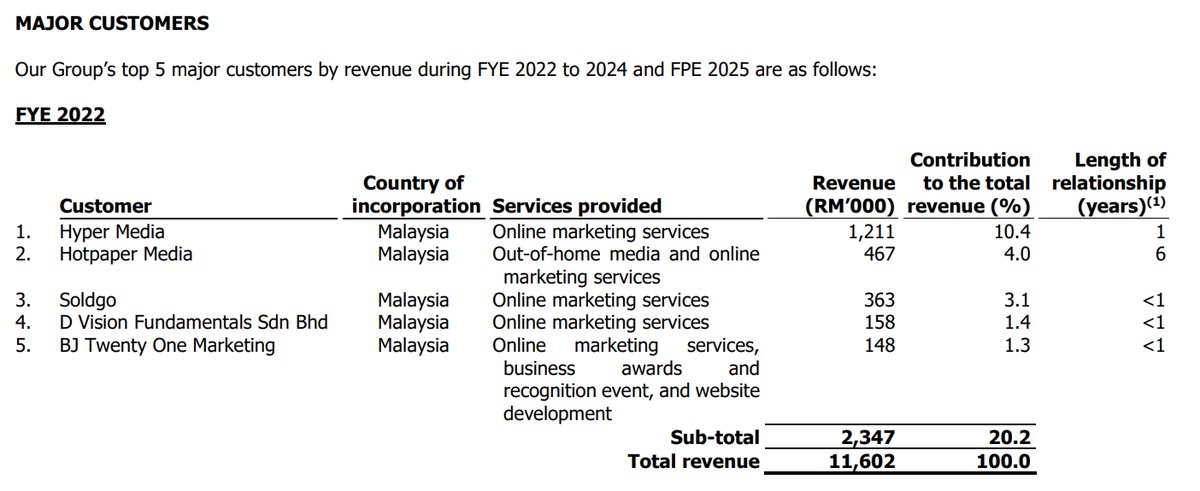

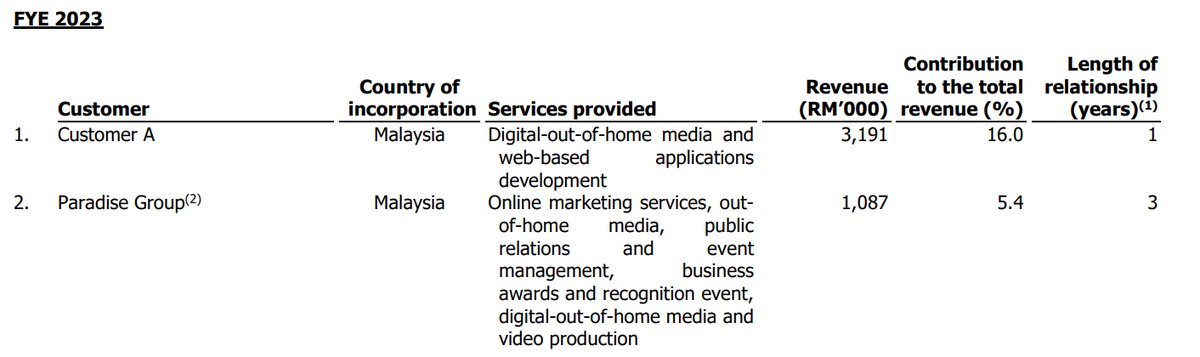

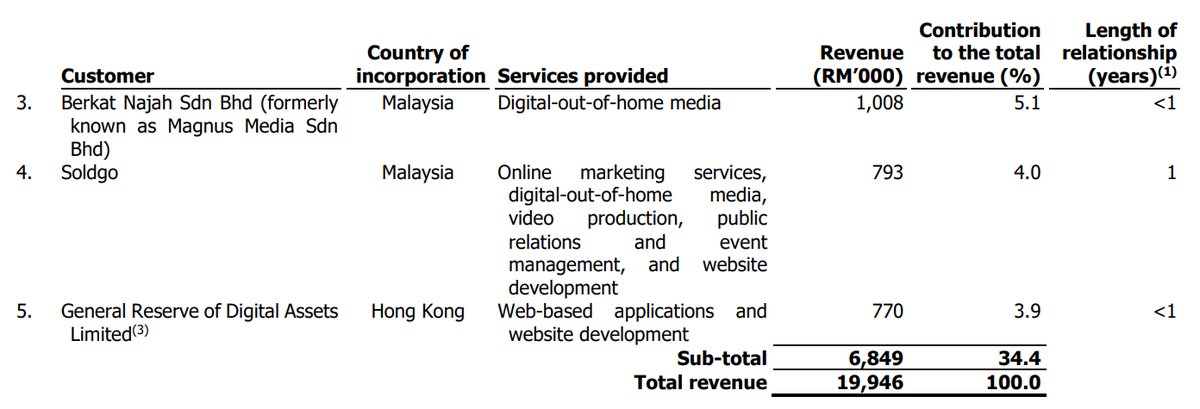

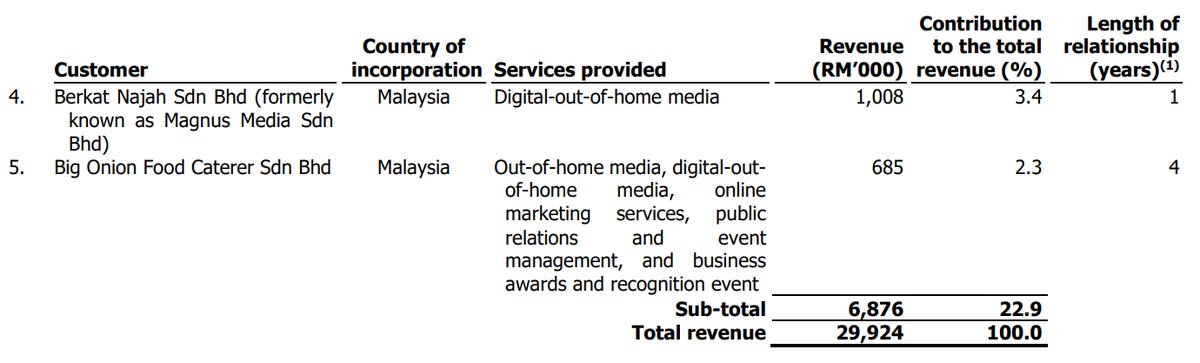

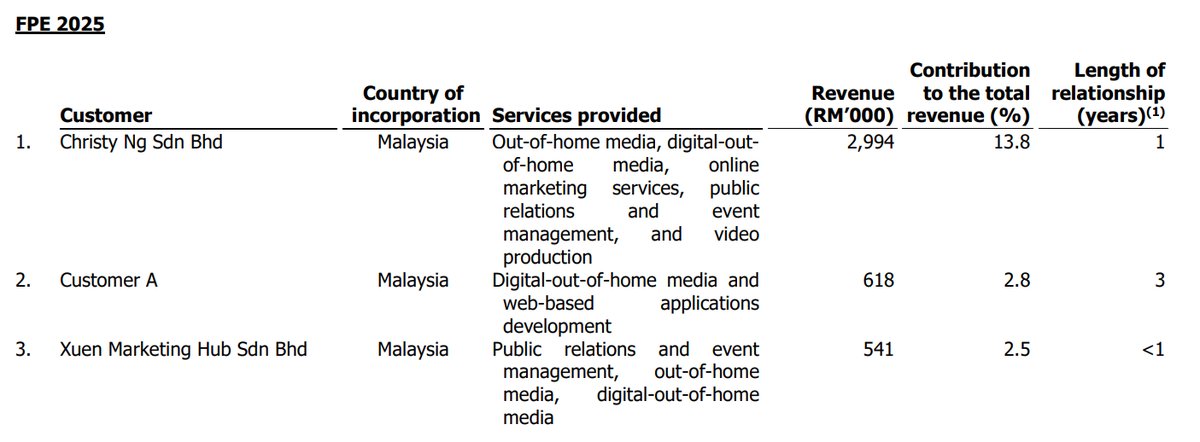

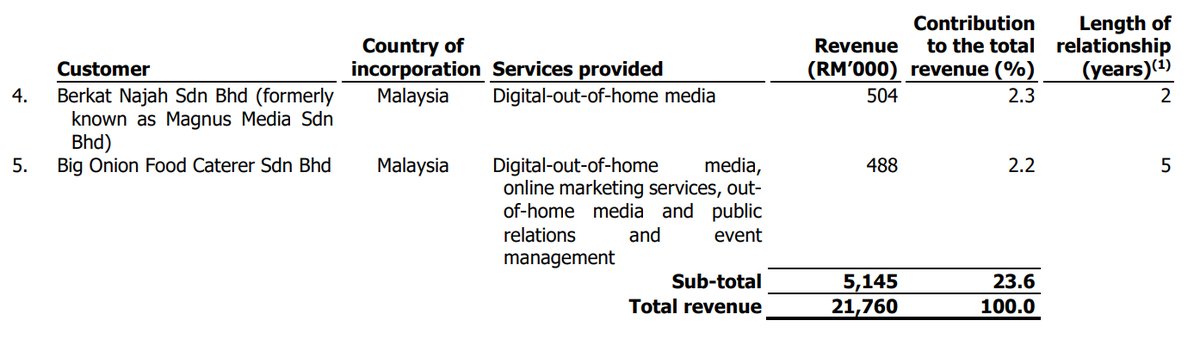

Major Customers

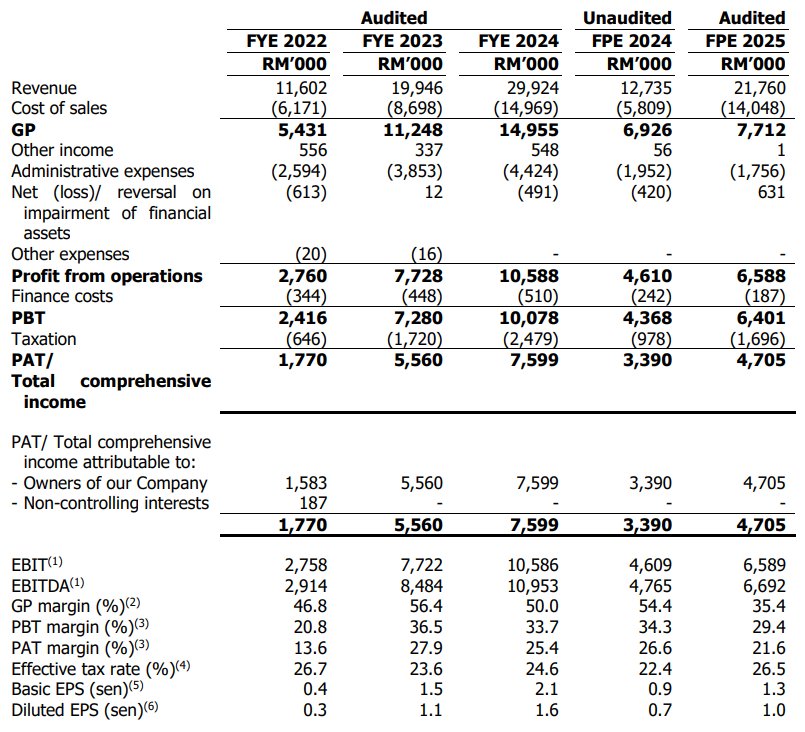

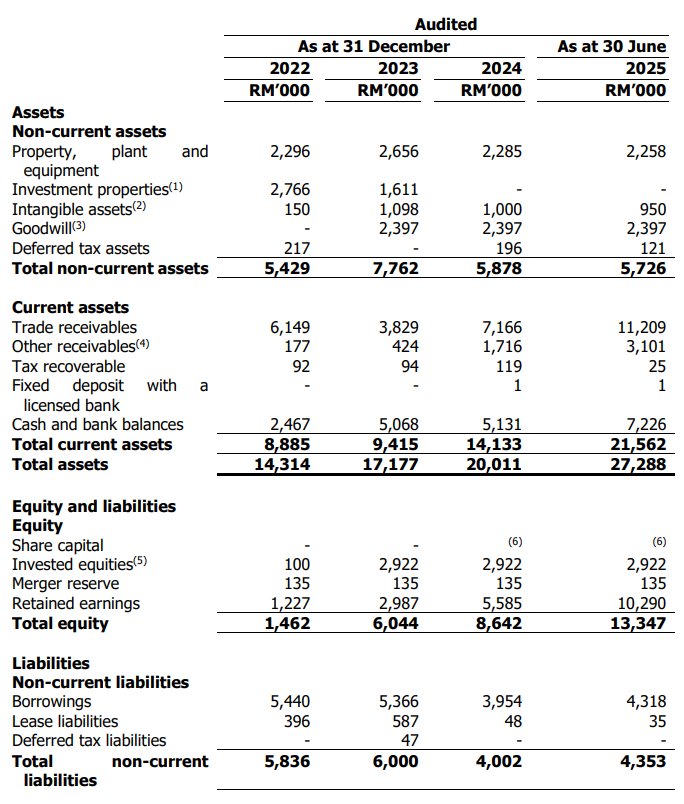

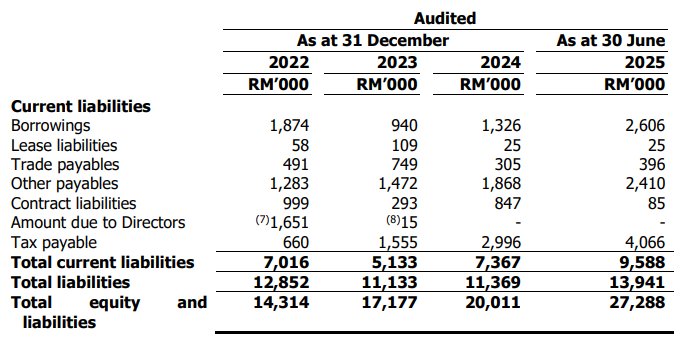

Revenue by Financial Year Ended

Profit After Tax (PAT) by Financial Year Ended

Revenue by Financial Period Ended

Profit After Tax (PAT) by Financial Period Ended

SWOT Analysis

Strengths

- High Profit Margins: Maintains superior PAT margins (21-25%) compared to traditional media peers like Star Media Group (low single digits), driven by its integrated solutions and premium 'ShangHai' branded events.

- Integrated Business Ecosystem: Synergy between offline, digital, and leads generation (awards/networking) allows for effective cross-selling to SMEs, creating a sticky ecosystem unlike pure-play advertising providers.

- Diversified Customer Base: No significant customer concentration risk, with the top customer contributing only 13.8% of revenue in FPE 2025, ensuring revenue stability.

Weaknesses

- No Long-Term Contracts: Revenue is project-based and transactional, providing less earnings visibility and stability compared to peers who may have long-term media buying contracts or recurring subscriptions.

- Reliance on Outsourcing: Heavy dependence on third-party suppliers for key functions like printing and event logistics, which compressed margins in FPE 2025 and poses operational risks.

Opportunities

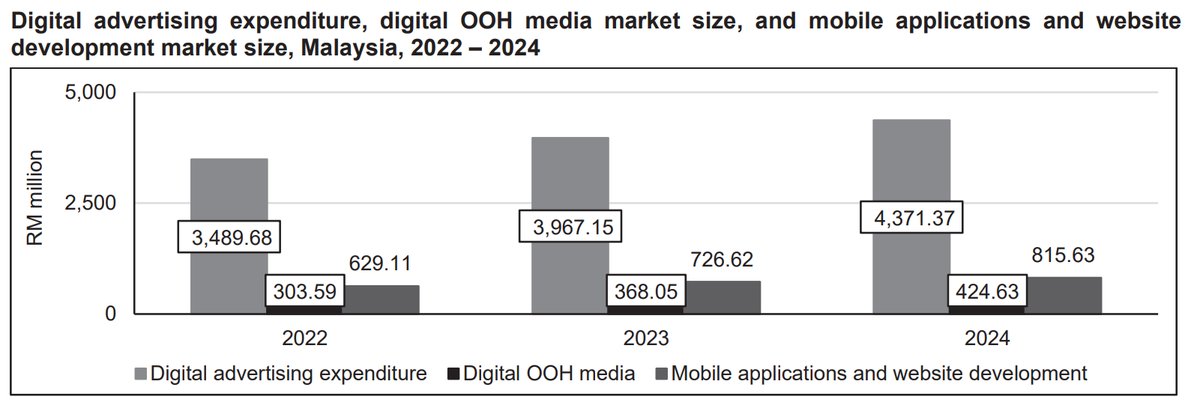

- Malay Market Expansion: The plan to replicate its successful business club model for the Malay-speaking SME community under 'MyUsahawanMedia' opens up a significantly larger demographic and market segment.

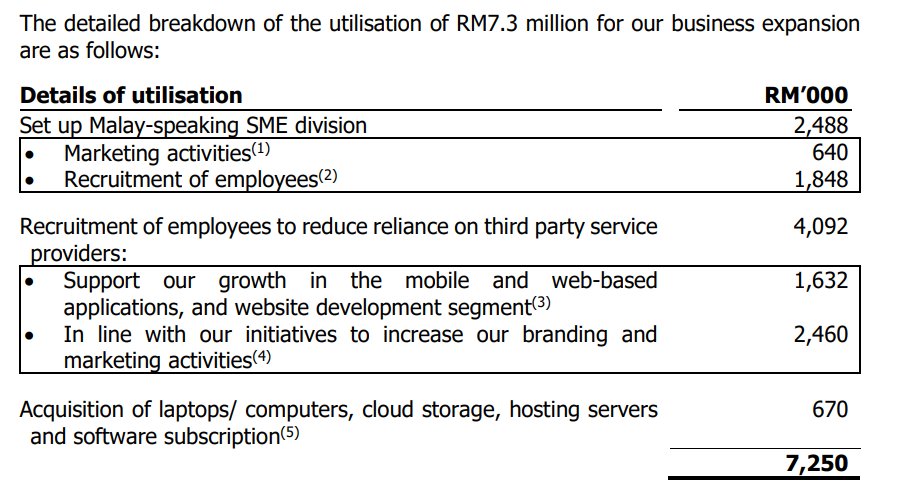

- Margin Improvement: IPO proceeds allocated for a new headquarters with in-house production studios will reduce outsourcing costs, addressing a key weakness and potentially improving future profit margins.

Threats

- Economic Downturn Sensitivity: As a branding service provider, revenue is highly sensitive to SME advertising budgets, which are typically among the first to be cut during economic slowdowns.

- Brand Reputation Risk: The business model heavily leverages the 'ShangHai' brand equity for its high-margin events. Any negative perception or loss of prestige could severely impact business leads and profitability.

Key Highlights

Sorry, this feature only available for iSaham Pro

Conclusion

Sorry, this feature only available for iSaham Pro

SBS Nexus Berhad's Latest News