Orkim Berhad IPO's Analysis

Orkim Berhad

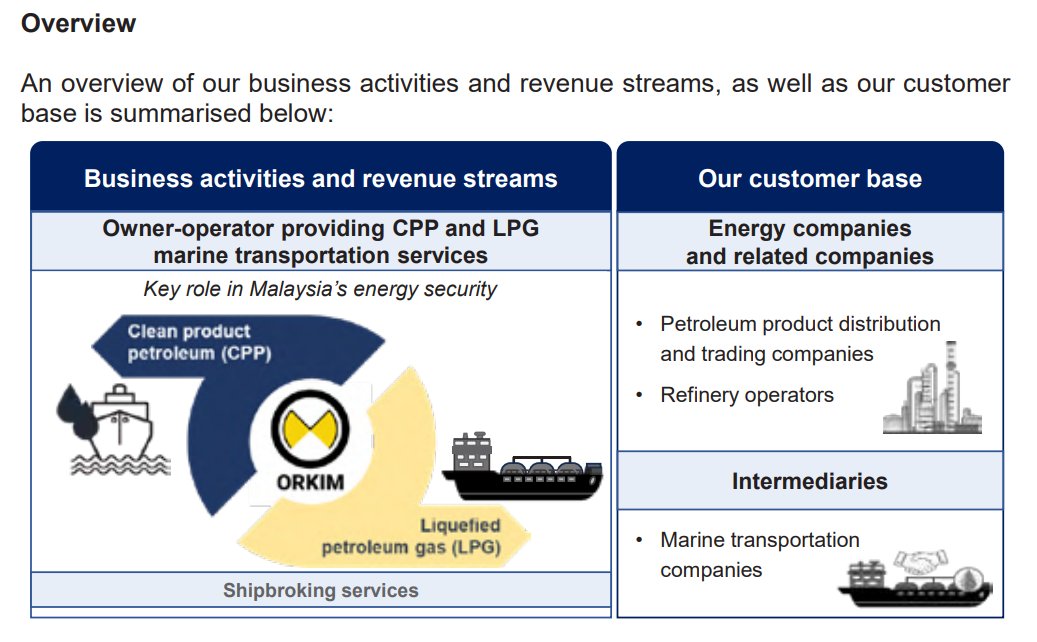

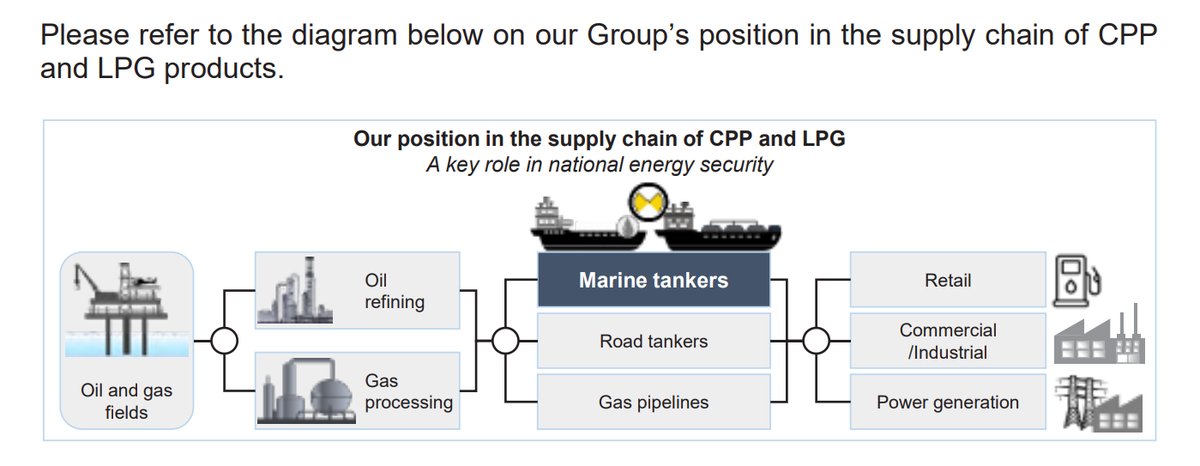

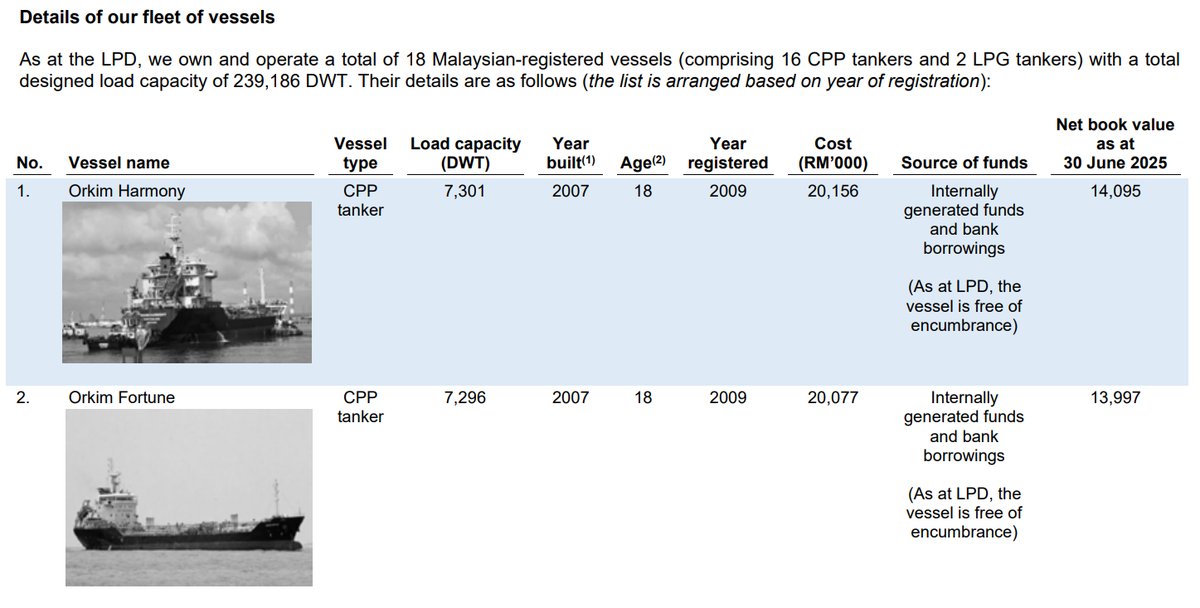

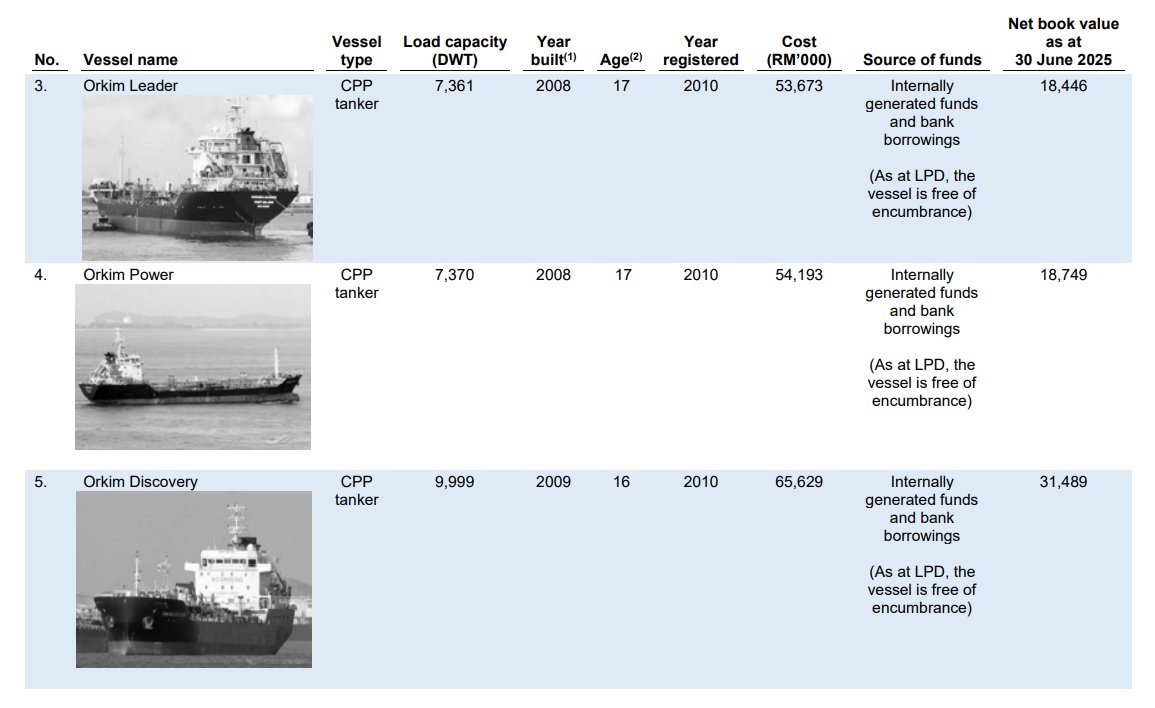

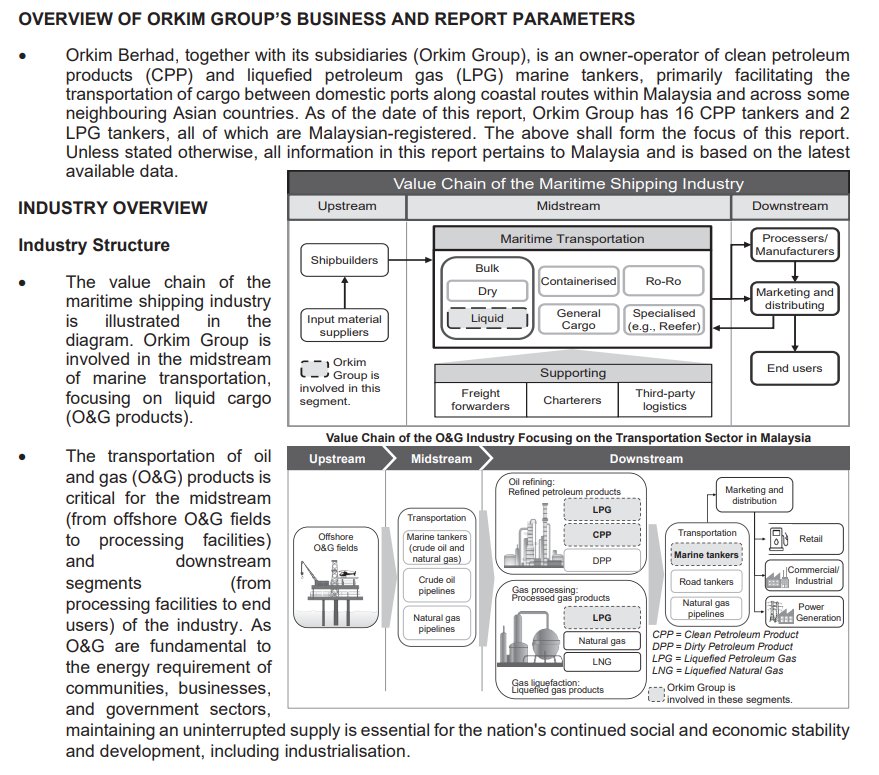

Orkim Berhad is an owner-operator of marine vessels, specifically product tankers and LPG tankers, providing marine transportation services for Clean Petroleum Products (CPP) and Liquefied Petroleum Gas (LPG). The company's principal activities, conducted through its subsidiaries, involve owning, chartering, and operating these vessels, as well as managing shipping property, freight contracting, and transport business. Its primary market is Malaysia, facilitating cargo transport along coastal routes and to neighboring Asian countries like Singapore. The fleet is crucial to Malaysia's energy supply chain, transporting refined products such as gasoline, diesel, and jet fuel from refineries to distribution points. The company also engages in shipbroking and provides third-party ship management services.

IPO Details

Strategic Overview & Data Visuals

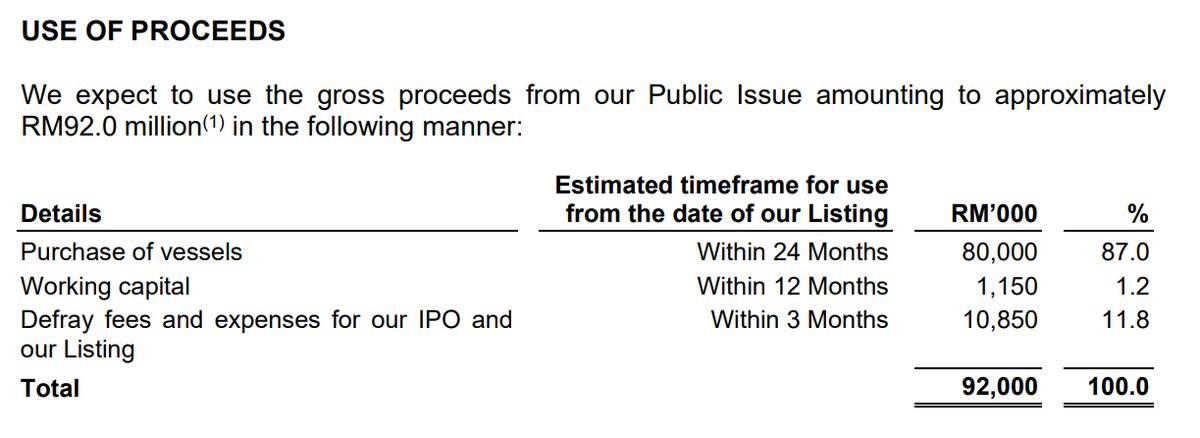

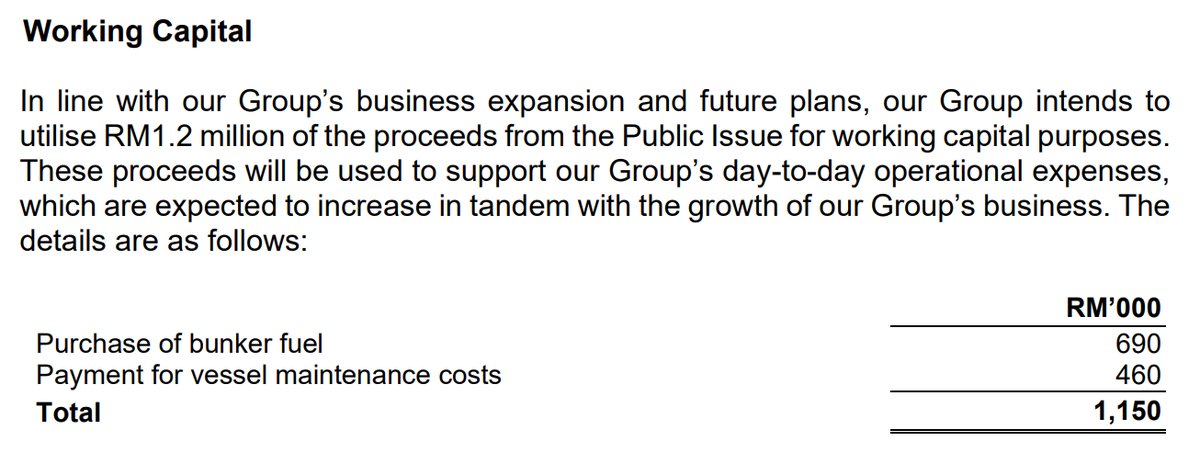

Utilisation of Proceeds

| Purpose | Amount (RM'000) | % | |

|---|---|---|---|

| Expansion | Purchase of Vessels | 80,000 | 87 |

| Working capital | Working capital | 1,150 | 1.2 |

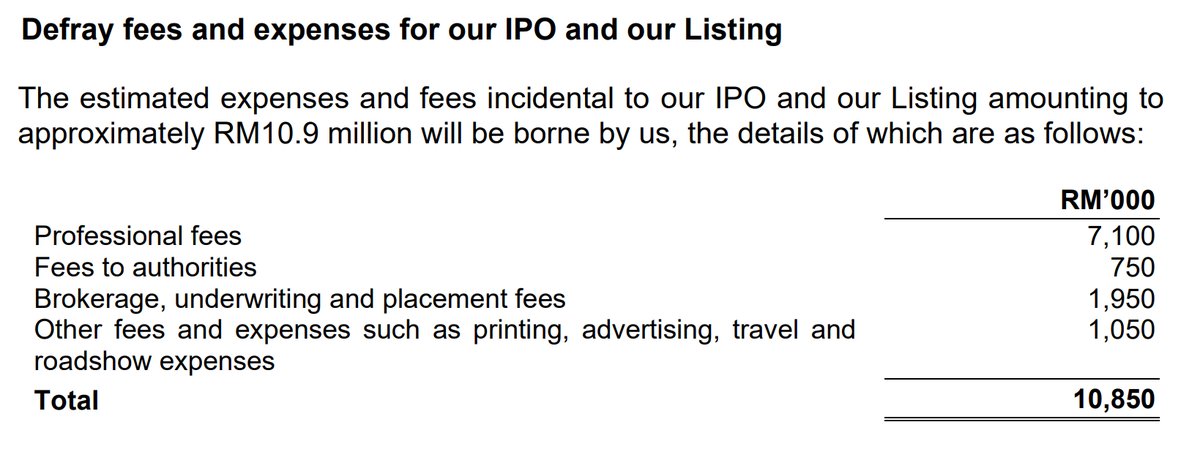

| Listing expenses | Defray fees and expenses for our IPO and our Listing | 10,850 | 11.8 |

| Total | 92,000 | 100 | |

Analyst Highlights

| Date | Analyst Highlights |

|---|---|

|

26-Nov-2025

Mplus |

|

|

25-Nov-2025

TA |

|

Utilisation of Proceeds

Business Segments

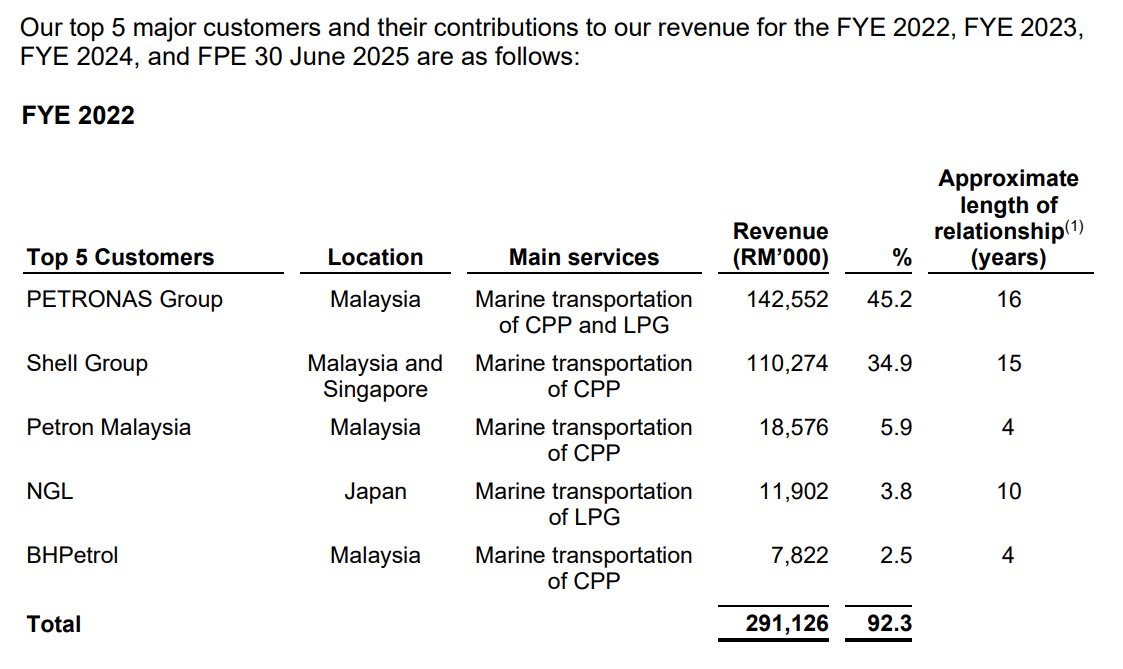

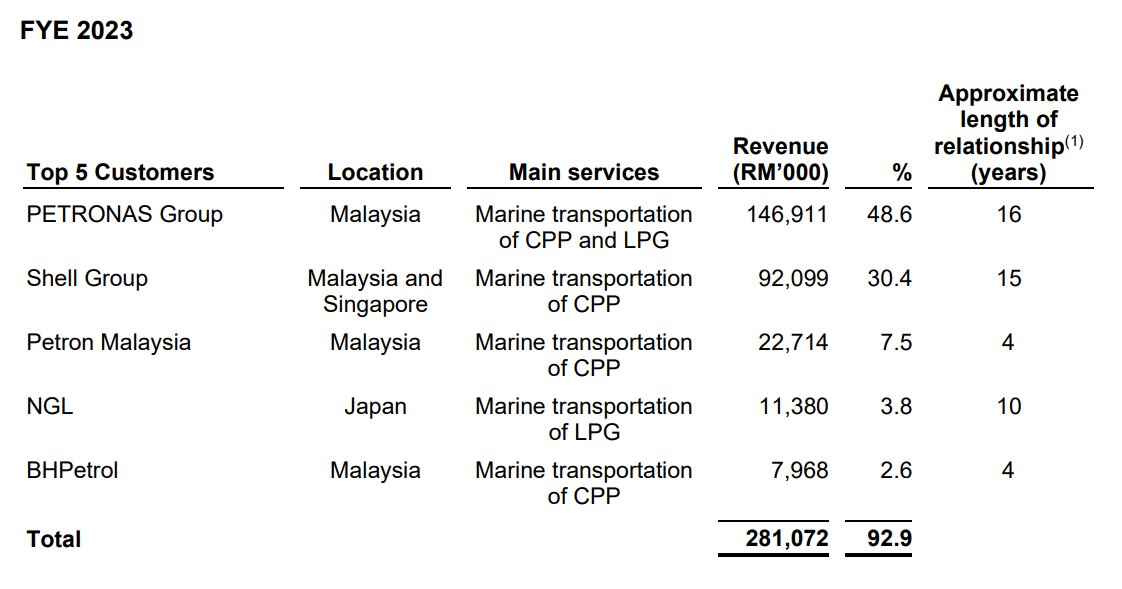

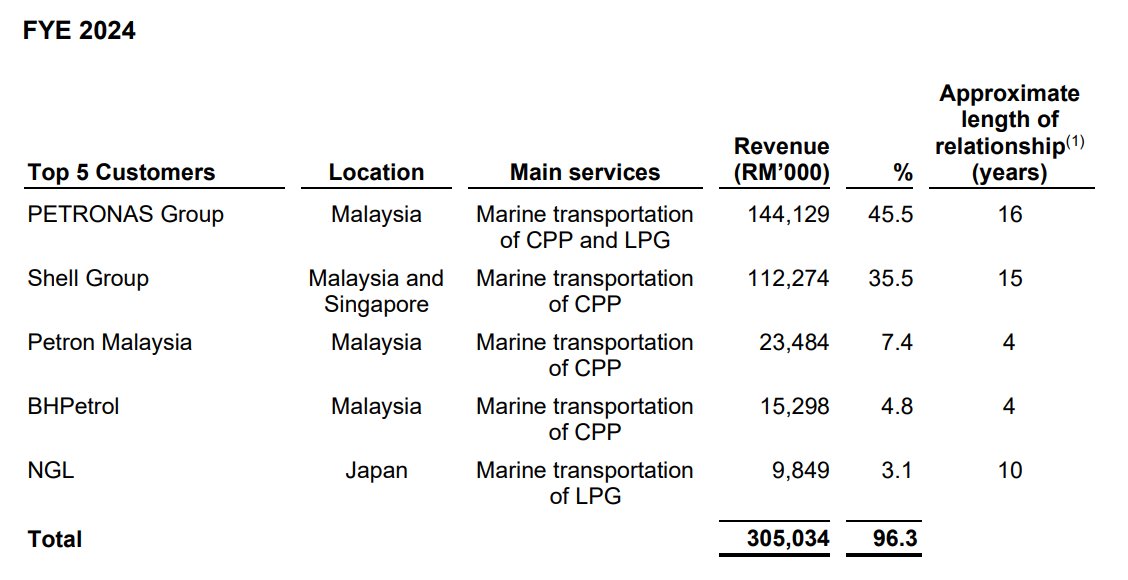

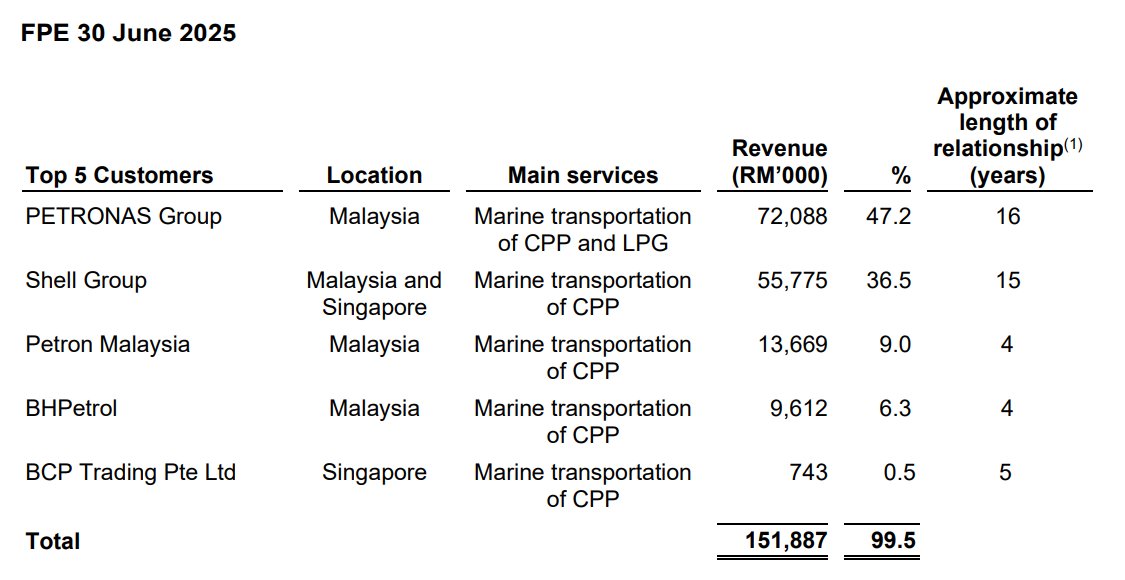

Major Customers

Revenue by Financial Year Ended

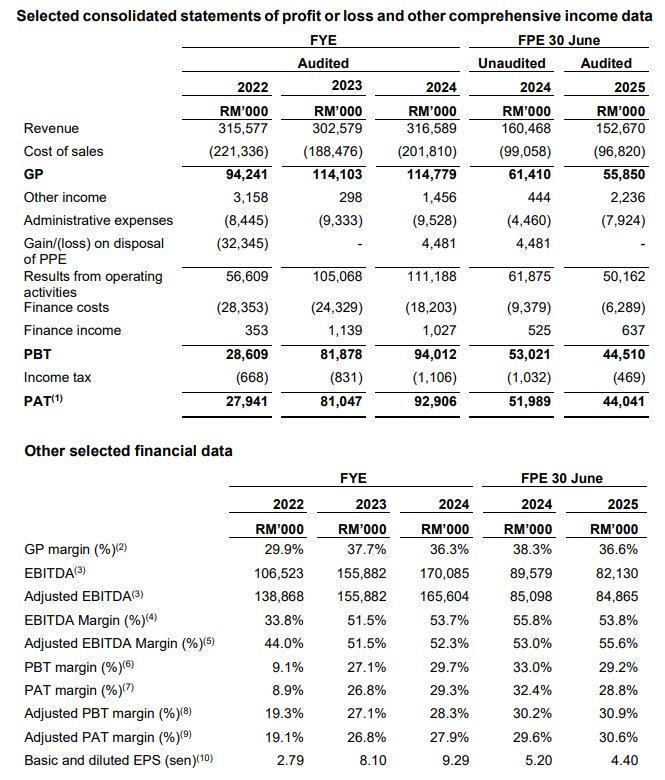

Profit After Tax (PAT) by Financial Year Ended

Revenue by Financial Period Ended

Profit After Tax (PAT) by Financial Period Ended

SWOT Analysis

Strengths

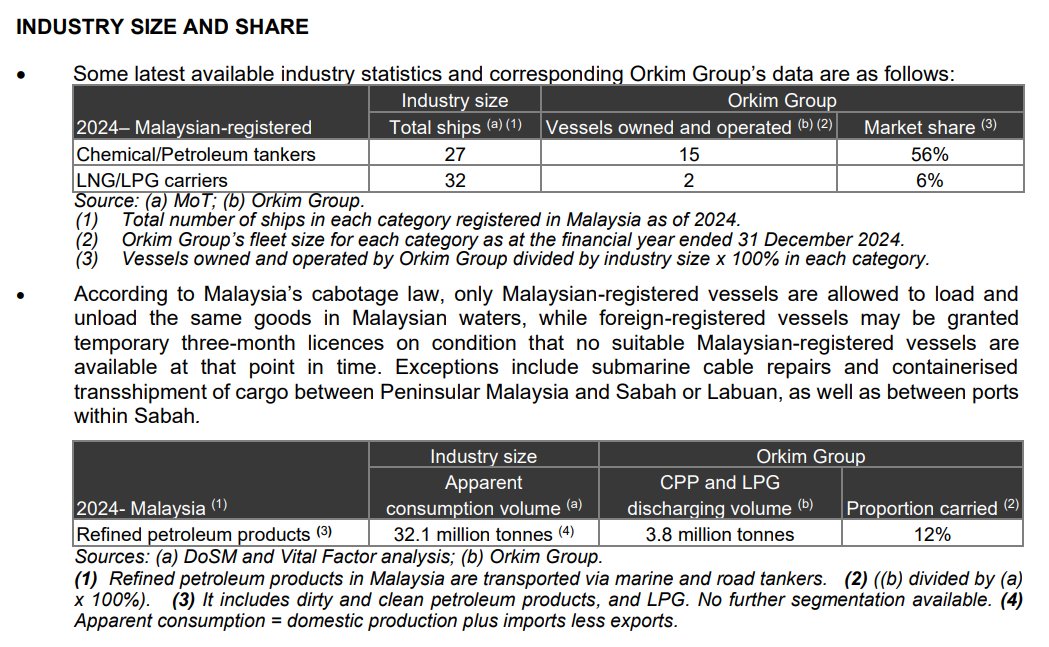

- Dominant Market Share: Orkim commands a 56% market share of Malaysian-registered clean petroleum product (CPP) tankers, operating 15 out of 27 such vessels in 2024. This dominant position creates significant barriers to entry for competitors and solidifies its role in national energy security.

- Superior Profit Margins: Orkim boasts a Net Profit Margin (NPM) of 29.3% (FY2024), significantly outperforming peers like Shin Yang Group (~8.7%) and Marine & General (~13.4%). This is largely driven by its efficient cost structure and full income tax exemption under Section 54A of the Income Tax Act.

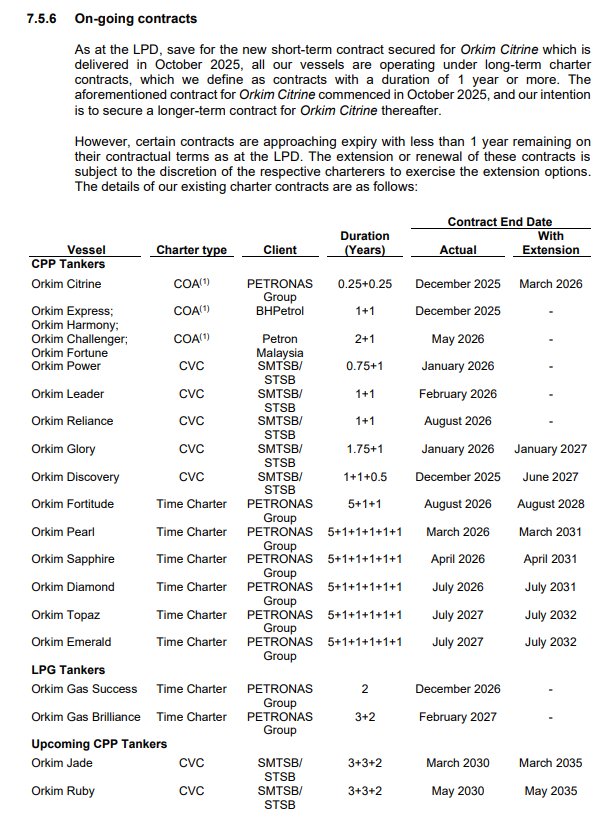

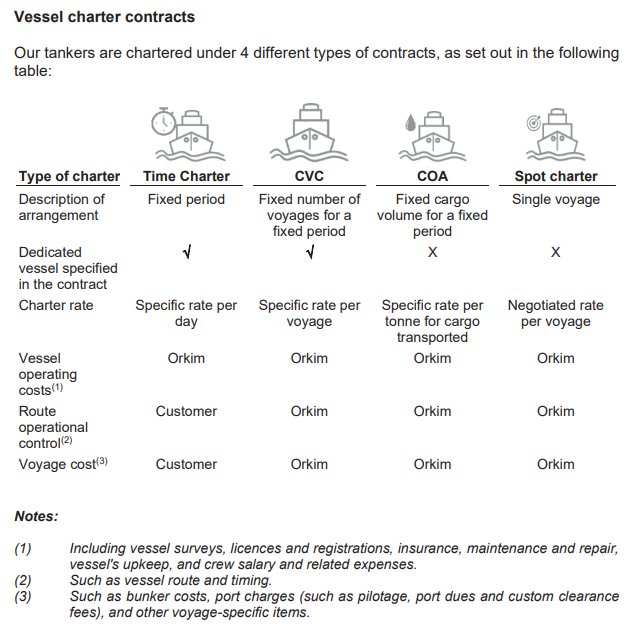

- High Recurring Revenue: 95.2% of revenue (FPE 2025) is derived from long-term contracts (Time Charter, CVC, COA), providing exceptional earnings visibility compared to peers reliant on volatile spot charter rates. The company holds 17 subsisting long-term contracts.

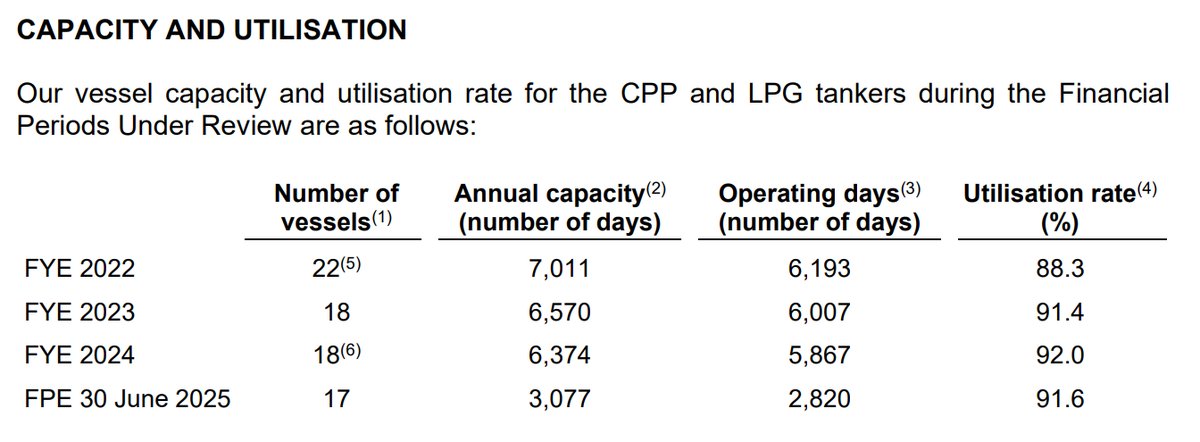

- Young Vessel Fleet: The fleet has an average age of 12 years, which is relatively young for the industry (typical lifespan 25-30 years). This reduces immediate maintenance CAPEX risks and ensures better compliance with strict oil major requirements compared to aging competitor fleets.

Weaknesses

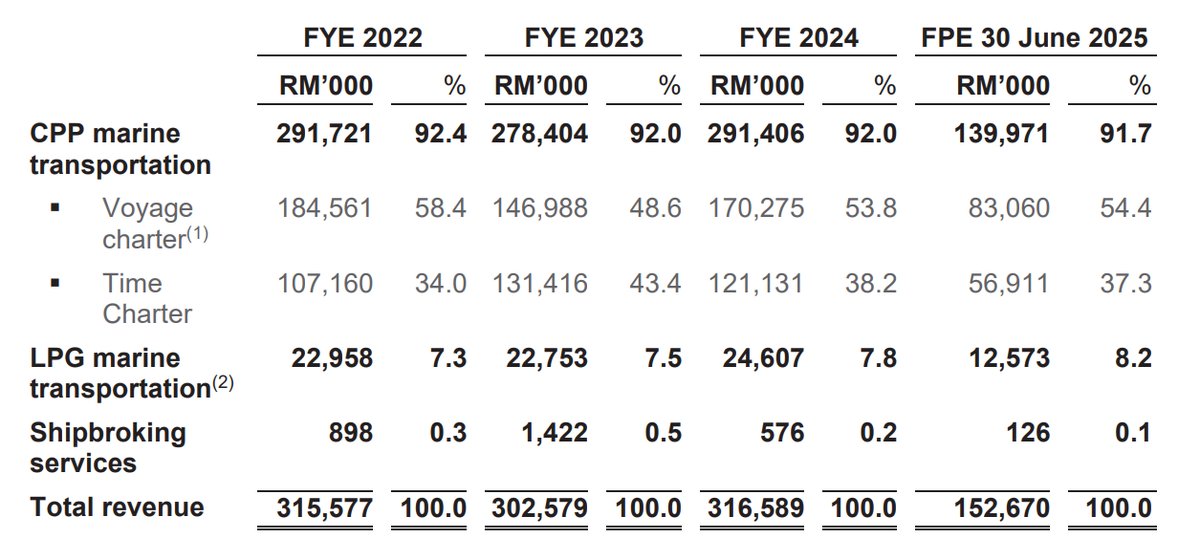

- High Customer Concentration: The Group is heavily dependent on two major customers, the PETRONAS Group and Shell Group, which collectively contributed 83.8% of total revenue in FPE 2025. Loss of either customer would be catastrophic to financial performance.

- Stagnant Revenue Growth: Top-line revenue has been flat over the last three years (FY22: RM315.6M vs FY24: RM316.6M), indicating the company is currently a 'cash cow' rather than a high-growth business. FPE 2025 revenue actually declined by 4.9% YoY due to vessel disposal.

- Reliance on Tax Exemption: The robust PAT margins are heavily reliant on the shipping income tax exemption valid until YA 2026. With an effective tax rate of only ~1.2%, any change in government policy or failure to renew this exemption would cause net profit to plummet by over 20%.

Opportunities

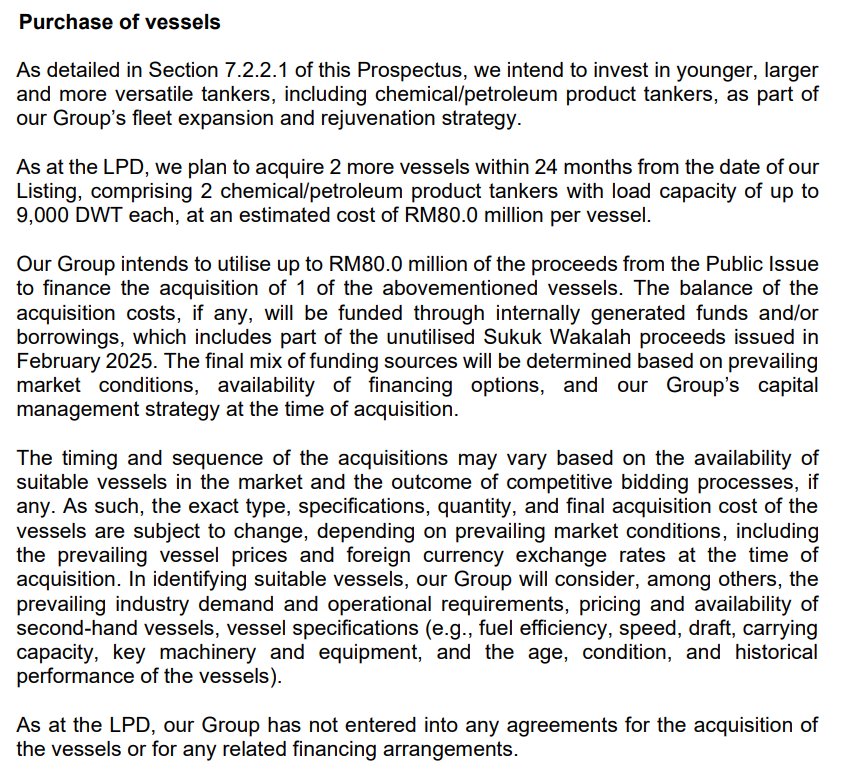

- Chemical Tanker Expansion: IPO proceeds are allocated to acquire new chemical/petroleum product tankers. Moving into higher-value chemical transport allows diversification beyond standard CPP/LPG and captures demand from the growing petrochemical sector (e.g., Pengerang Integrated Petroleum Complex).

- Cabotage Policy Protection: The reinstatement of the cabotage policy exemption revocation in 2024 strengthens protection for Malaysian-registered vessels, potentially increasing domestic market share as foreign vessels face stricter licensing requirements.

- Fleet Modernization: Allocation of RM50 million for fleet modernization (Green shipping) aligns Orkim with future ESG requirements, potentially allowing them to command premium charter rates from multinational oil majors focused on Scope 3 emissions.

Threats

- Bunker Price Volatility: While CVC/COA contracts have pass-through mechanisms, spot charters (though a small portion) expose the company to bunker price fluctuations. A sharp rise in global oil prices could compress margins on non-indexed revenue streams.

- Interest Rate Risk: With a gearing ratio of 0.7x and RM375.6 million in borrowings (including a significant fixed-rate Sukuk but also floating rate term loans), the company remains sensitive to interest rate hikes which could increase finance costs.

- Decarbonization Regulations: Stricter IMO regulations (EEXI, CII) may force earlier retirement of older vessels or necessitate expensive retrofitting, impacting future cash flows and capital expenditure requirements beyond current projections.

Key Highlights

Sorry, this feature only available for iSaham Pro

Conclusion

Sorry, this feature only available for iSaham Pro

Orkim Berhad's Latest News