LAC Med Berhad IPO's Analysis

LAC Med Berhad

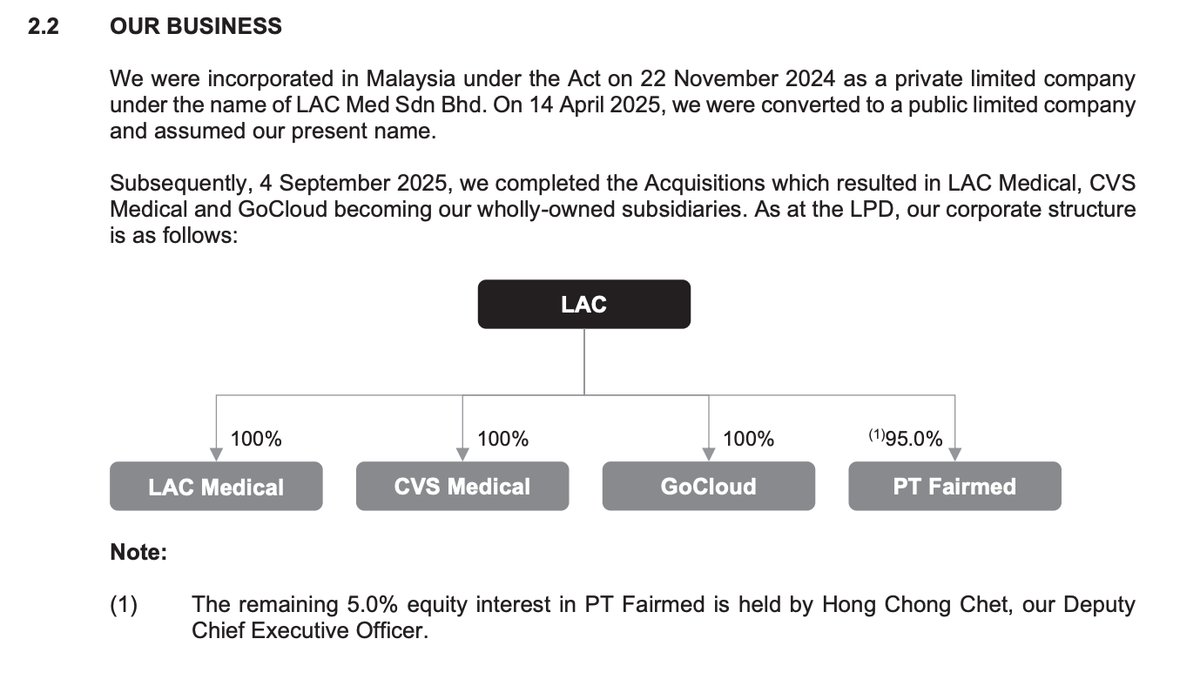

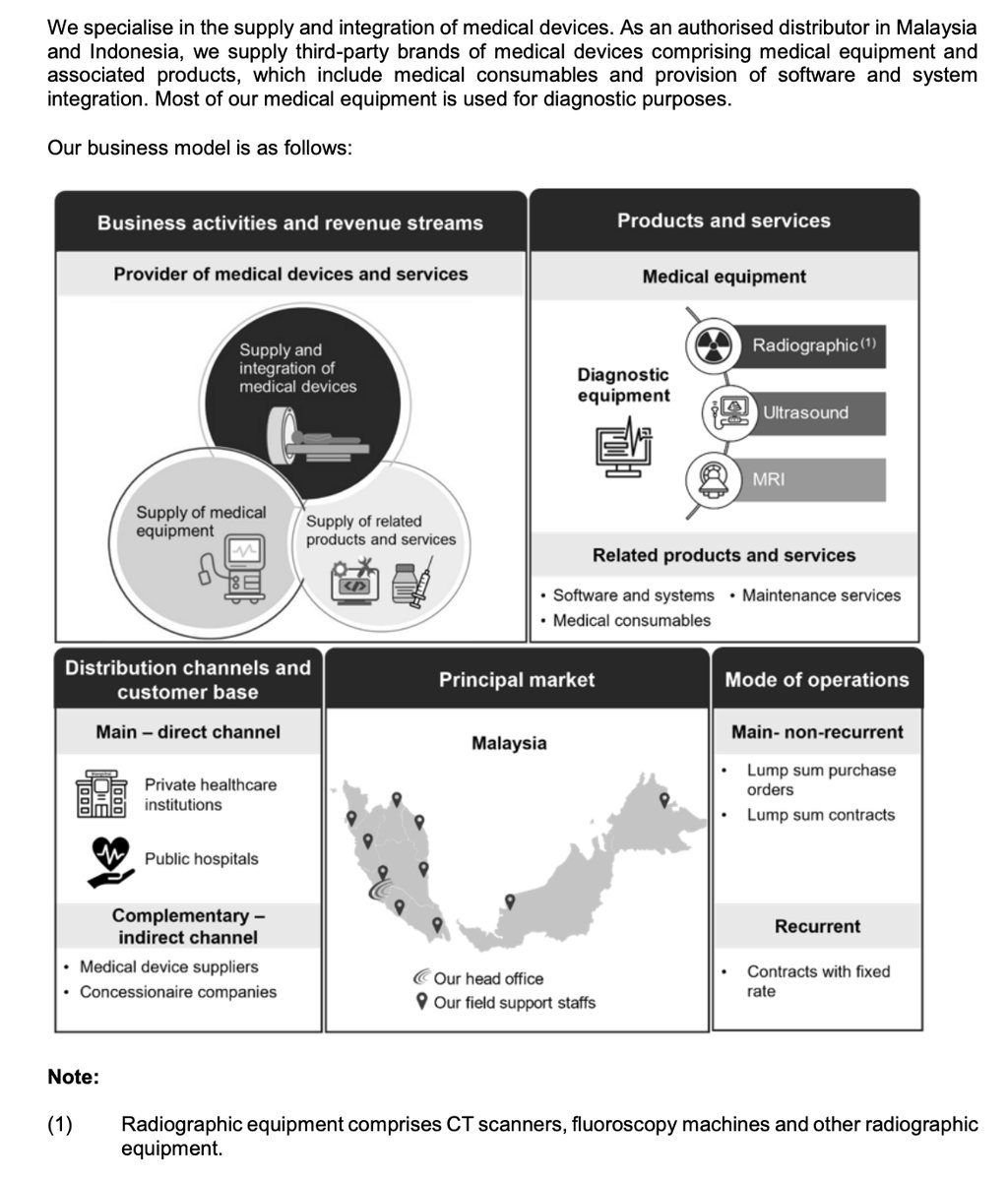

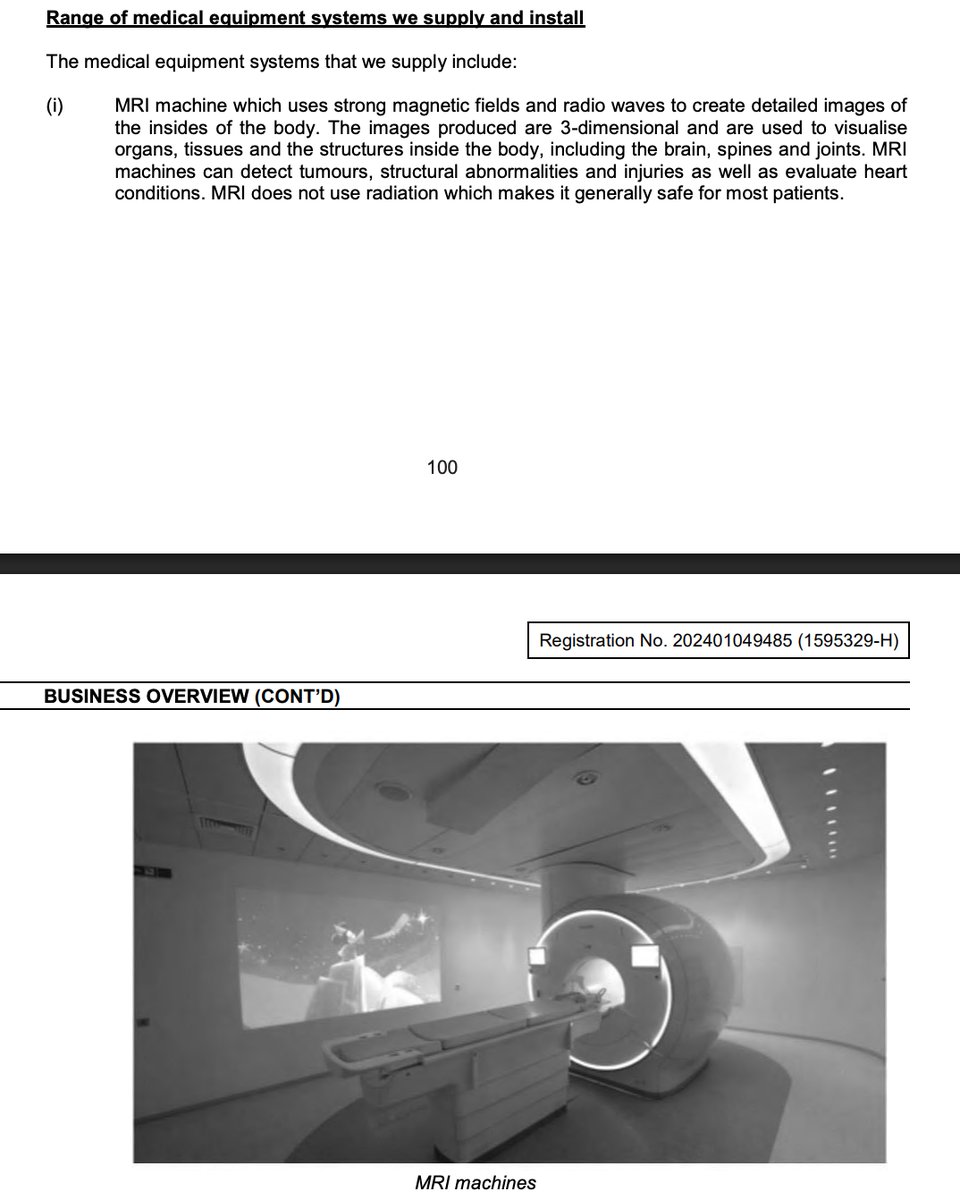

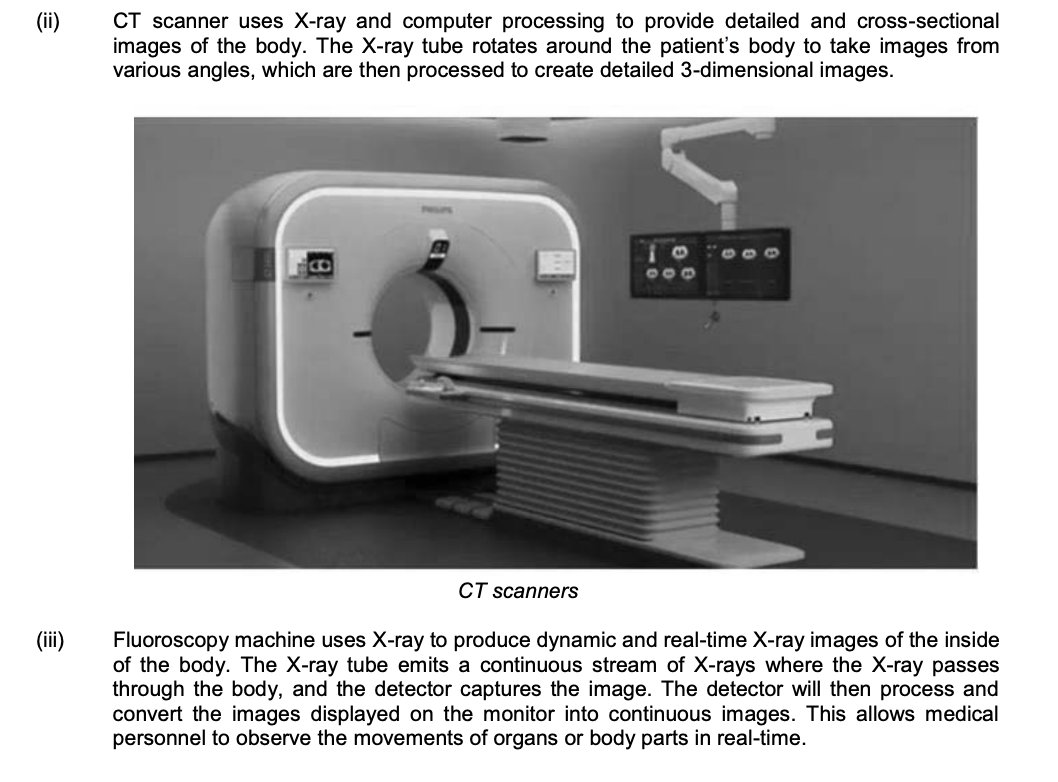

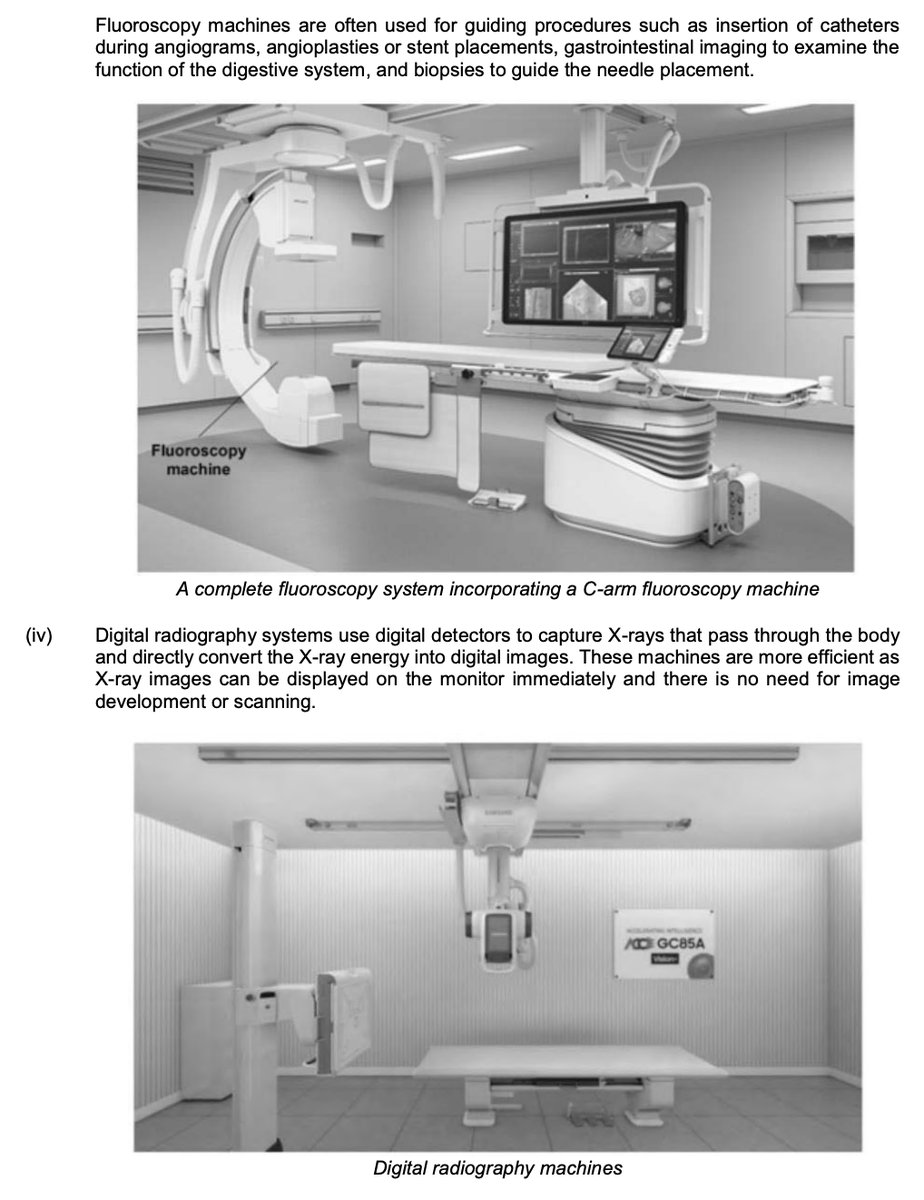

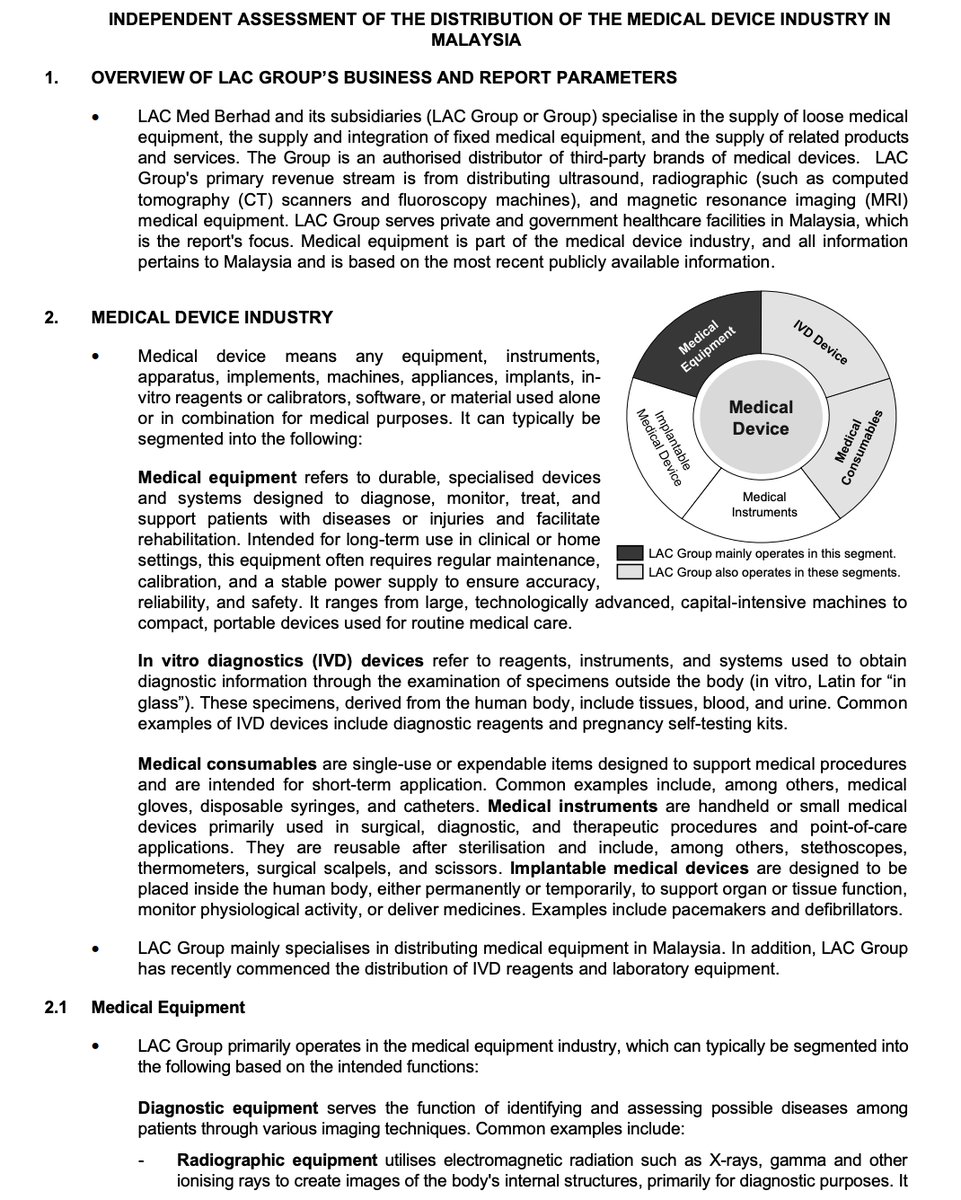

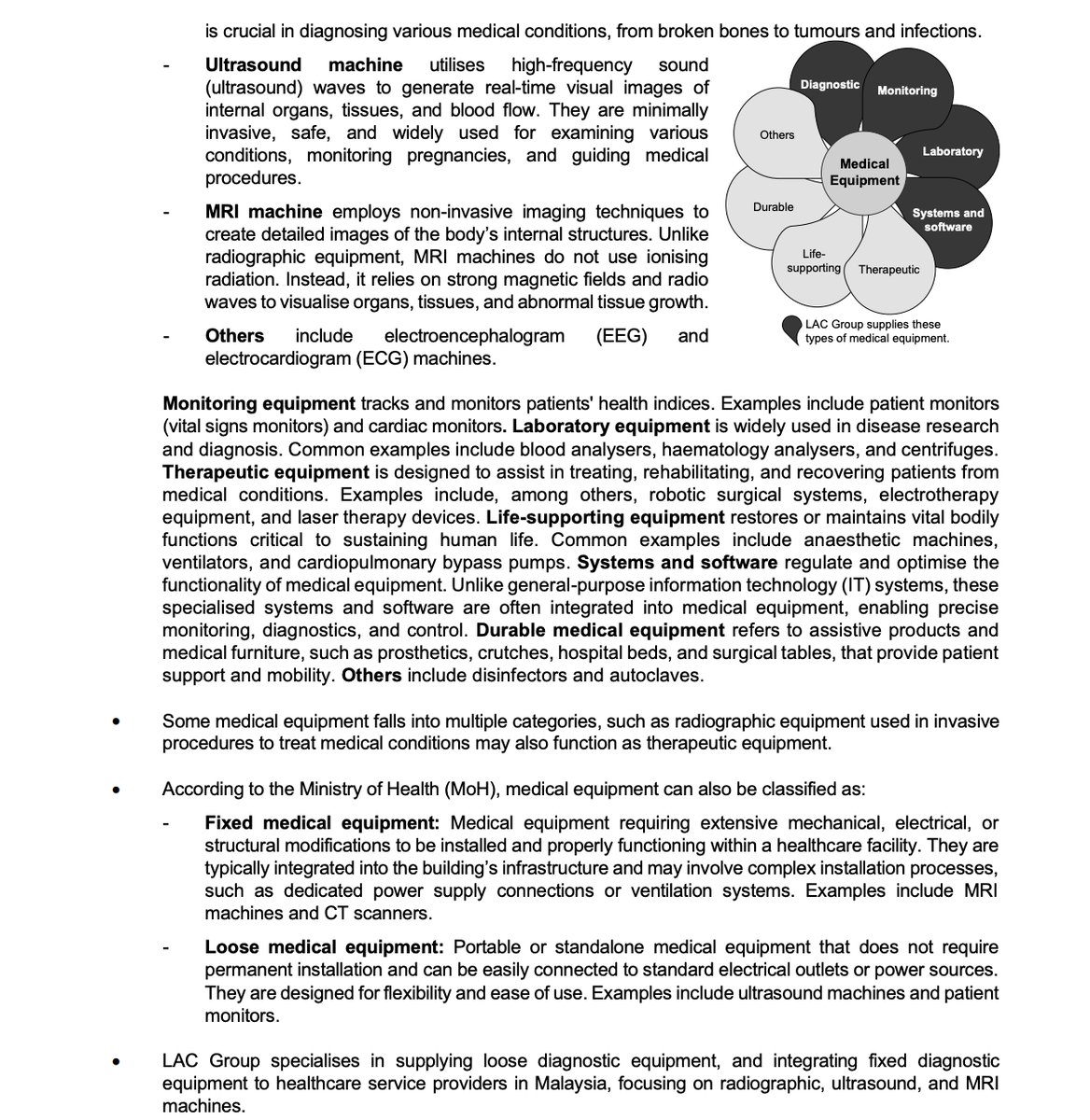

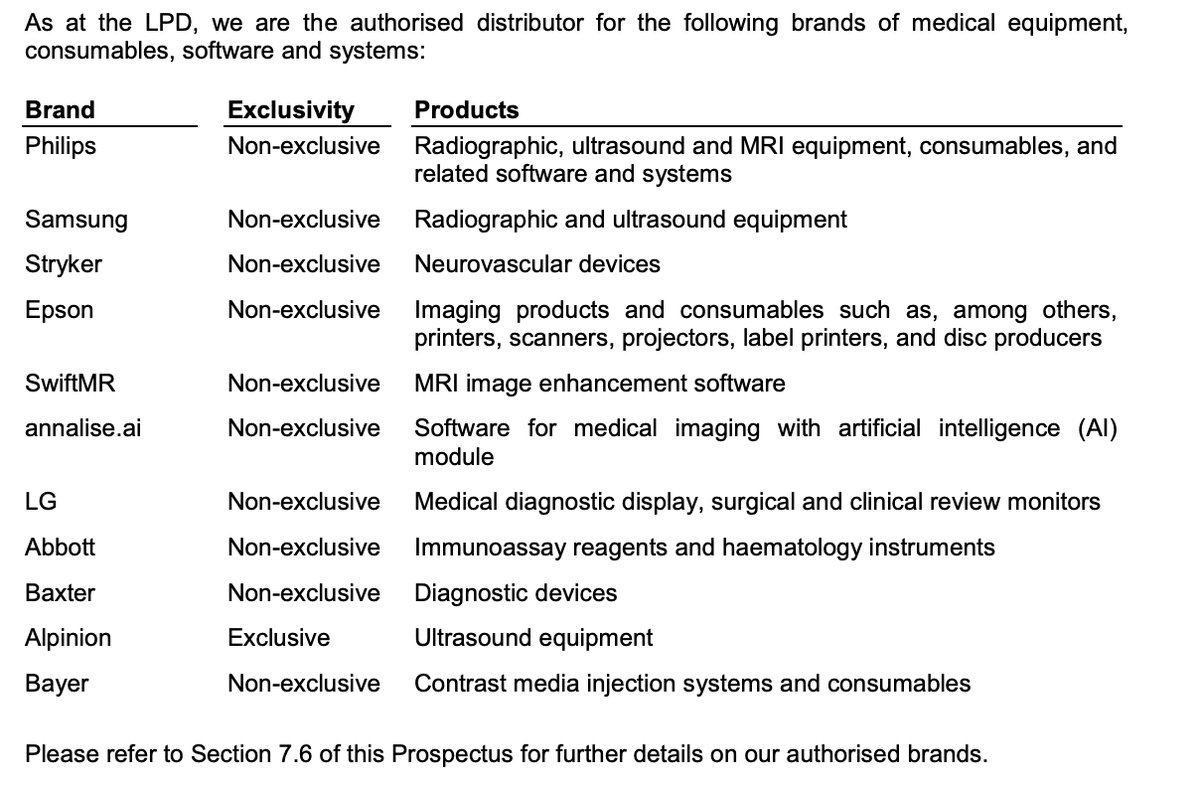

LAC Med Berhad, through its subsidiaries, specialises in the supply and integration of medical devices in Malaysia and Indonesia. The Group is an authorised distributor for third-party brands of medical devices, including medical equipment primarily used for diagnostic purposes, and associated products like medical consumables. It also provides software and system integration services. A key part of its business involves the provision of ICT products and services tailored for healthcare facilities. The company was incorporated in Malaysia in November 2024 and has since expanded its operations regionally with the establishment of PT Fairmed in Indonesia.

IPO Details

Strategic Overview & Data Visuals

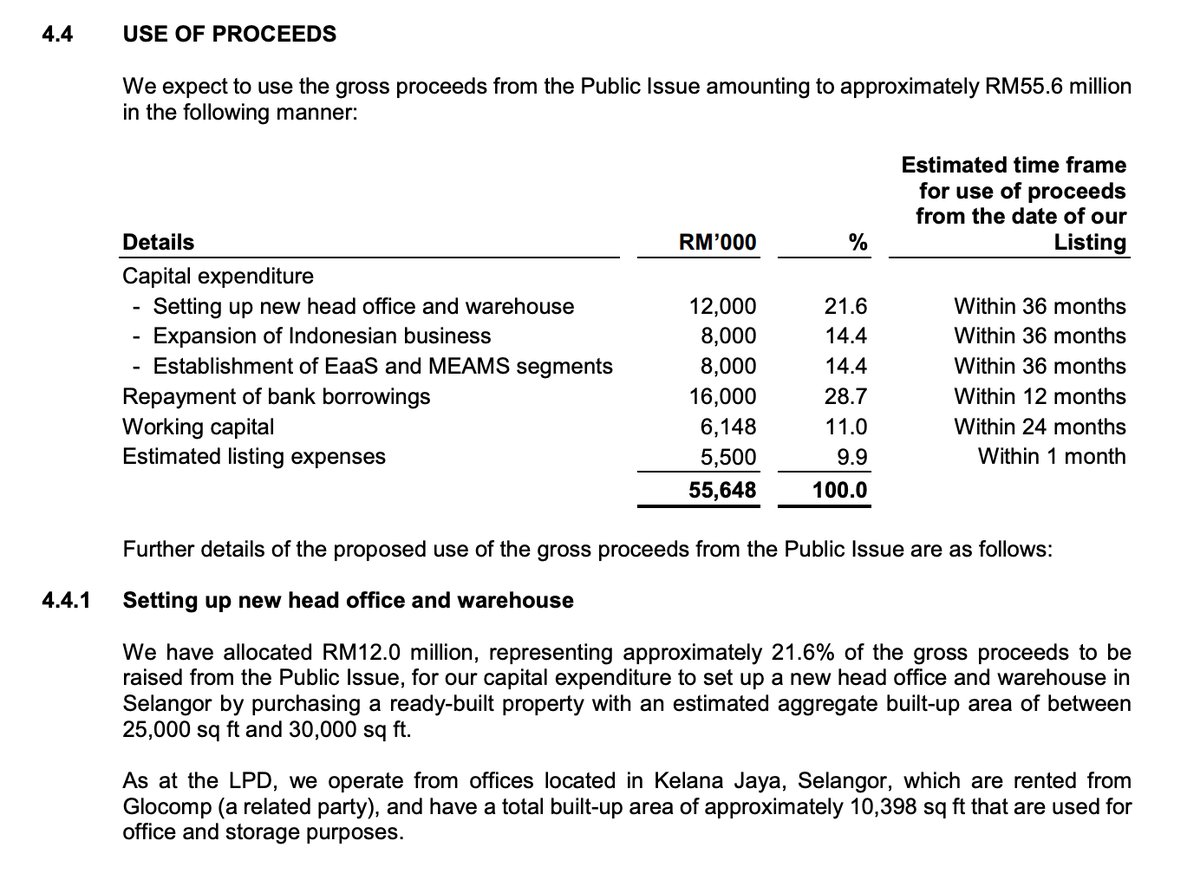

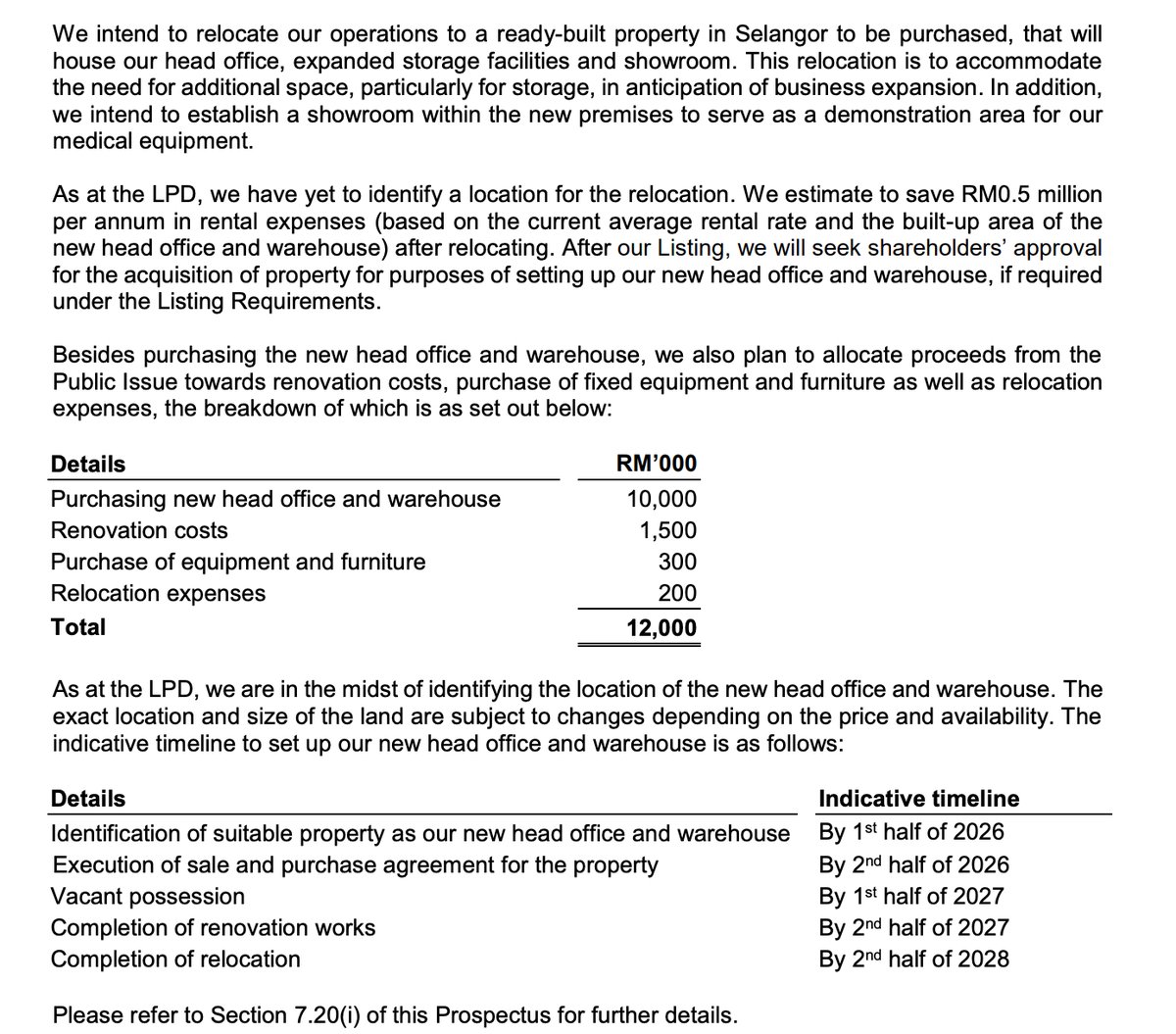

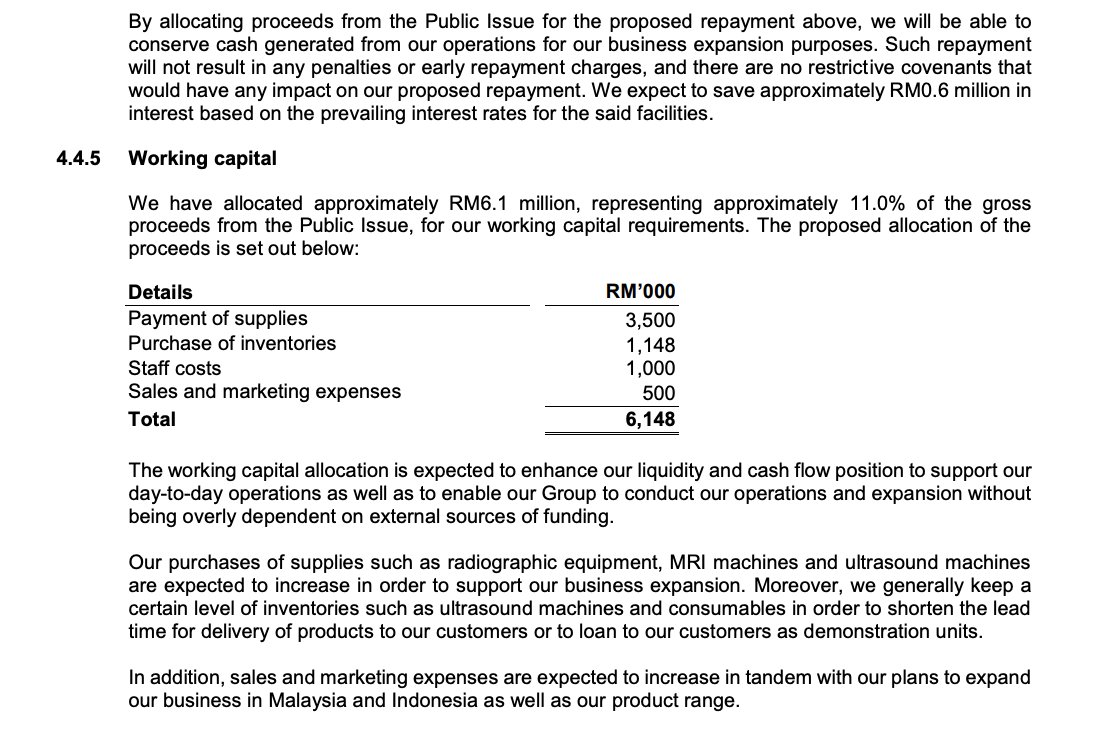

Utilisation of Proceeds

| Purpose | Amount (RM'000) | % | |

|---|---|---|---|

| Expansion | Setting up new head office and warehouse | 12,000 | 21.6 |

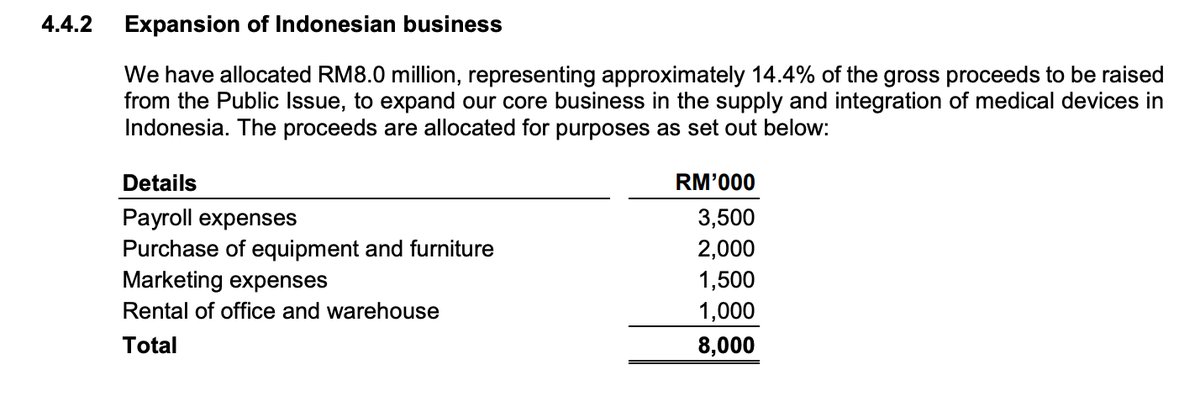

| Expansion | Expansion of Indonesian business | 8,000 | 14.4 |

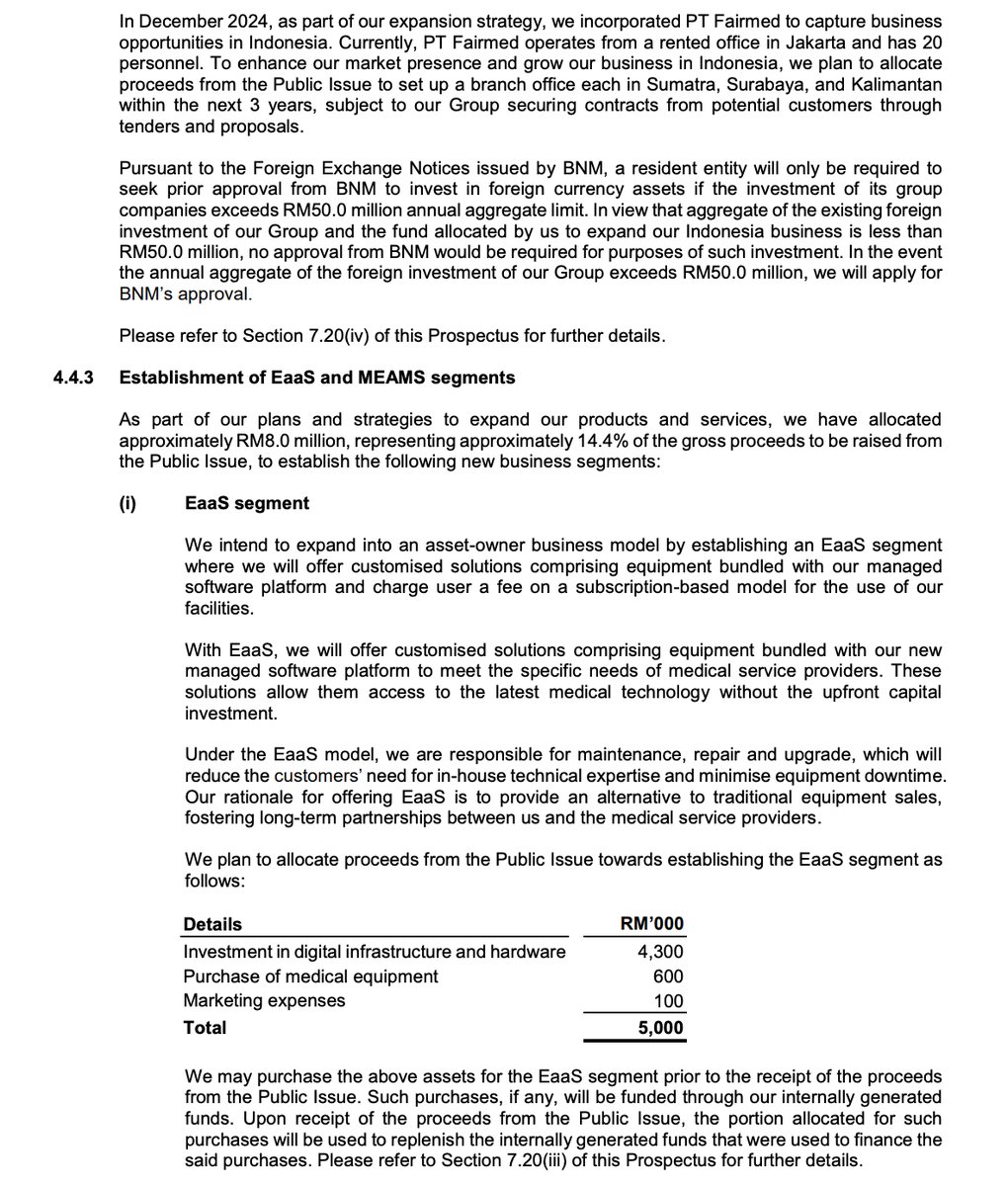

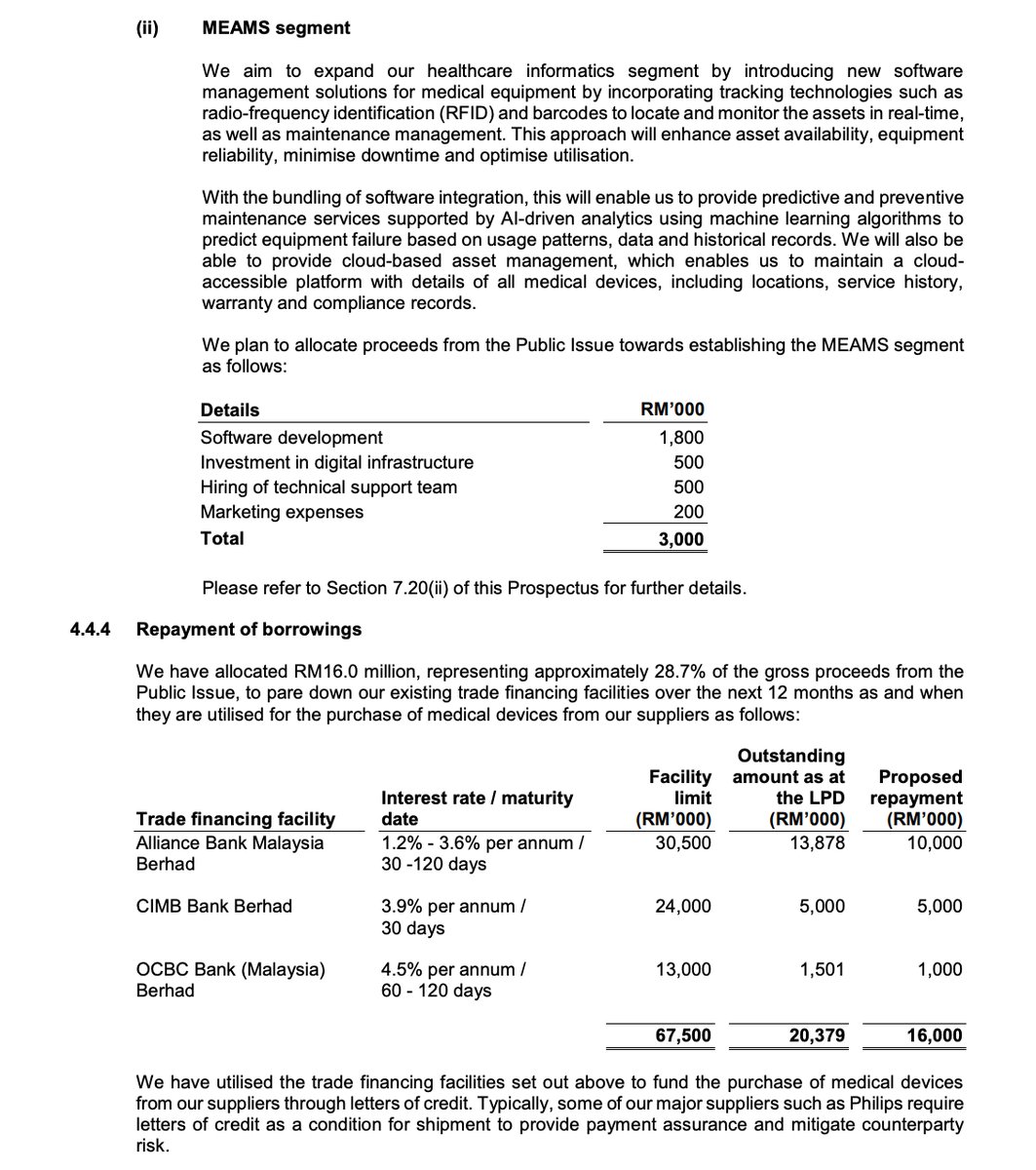

| Expansion | Establishment of EaaS and MEAMS segments | 8,000 | 14.4 |

| Working capital | Working capital | 6,148 | 11 |

| Listing expenses | Estimated listing expenses | 5,500 | 9.9 |

| Debt | Repayment of bank borrowings | 16,000 | 28.7 |

| Total | 55,648 | 100 | |

Analyst Highlights

| Date | Analyst Highlights |

|---|---|

|

10-Mar-2026

RHB |

|

|

19-Feb-2026

RHB |

|

|

25-Nov-2025

Mplus |

|

|

24-Nov-2025

TradeView |

|

|

21-Nov-2025

TA |

|

Utilisation of Proceeds

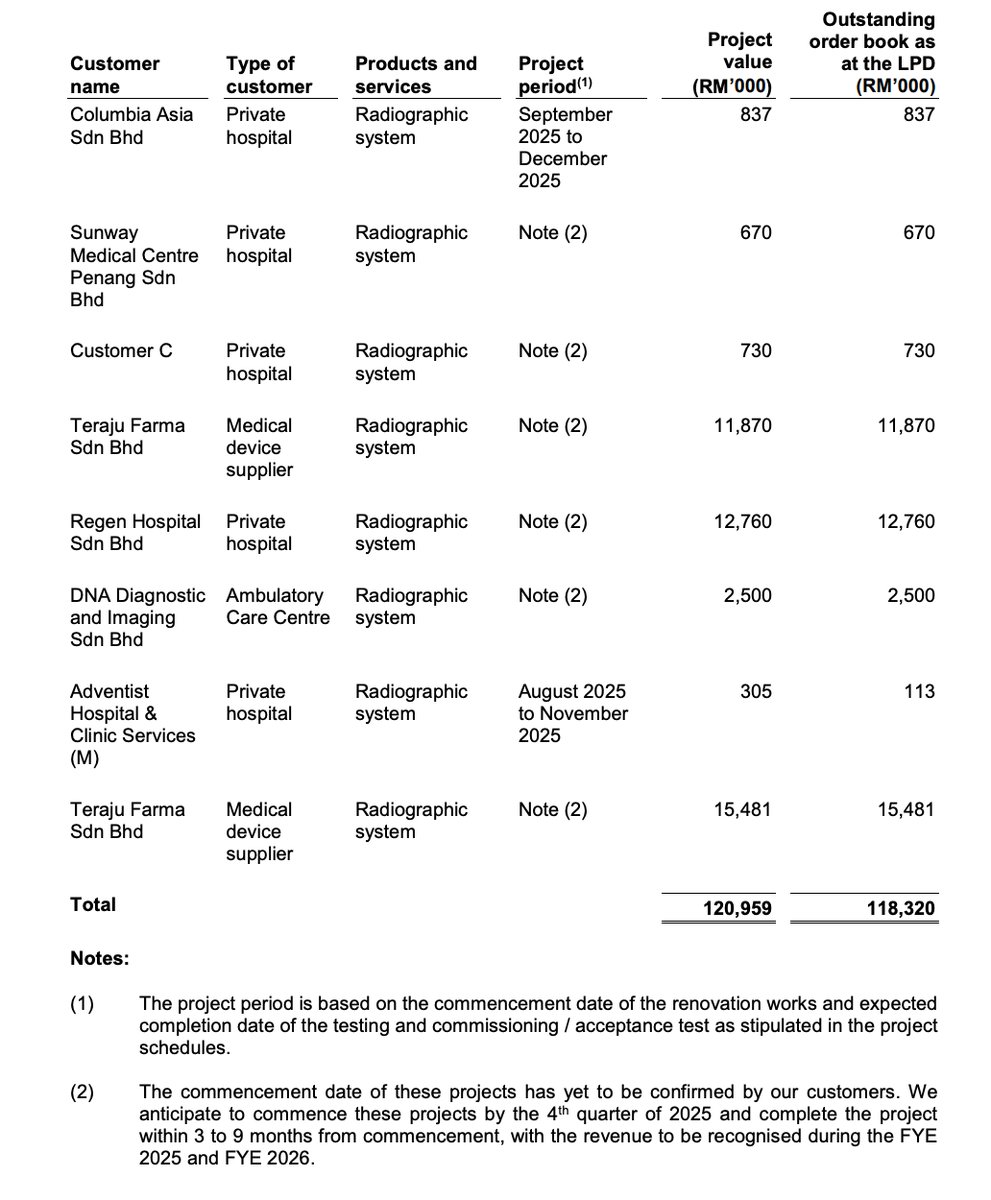

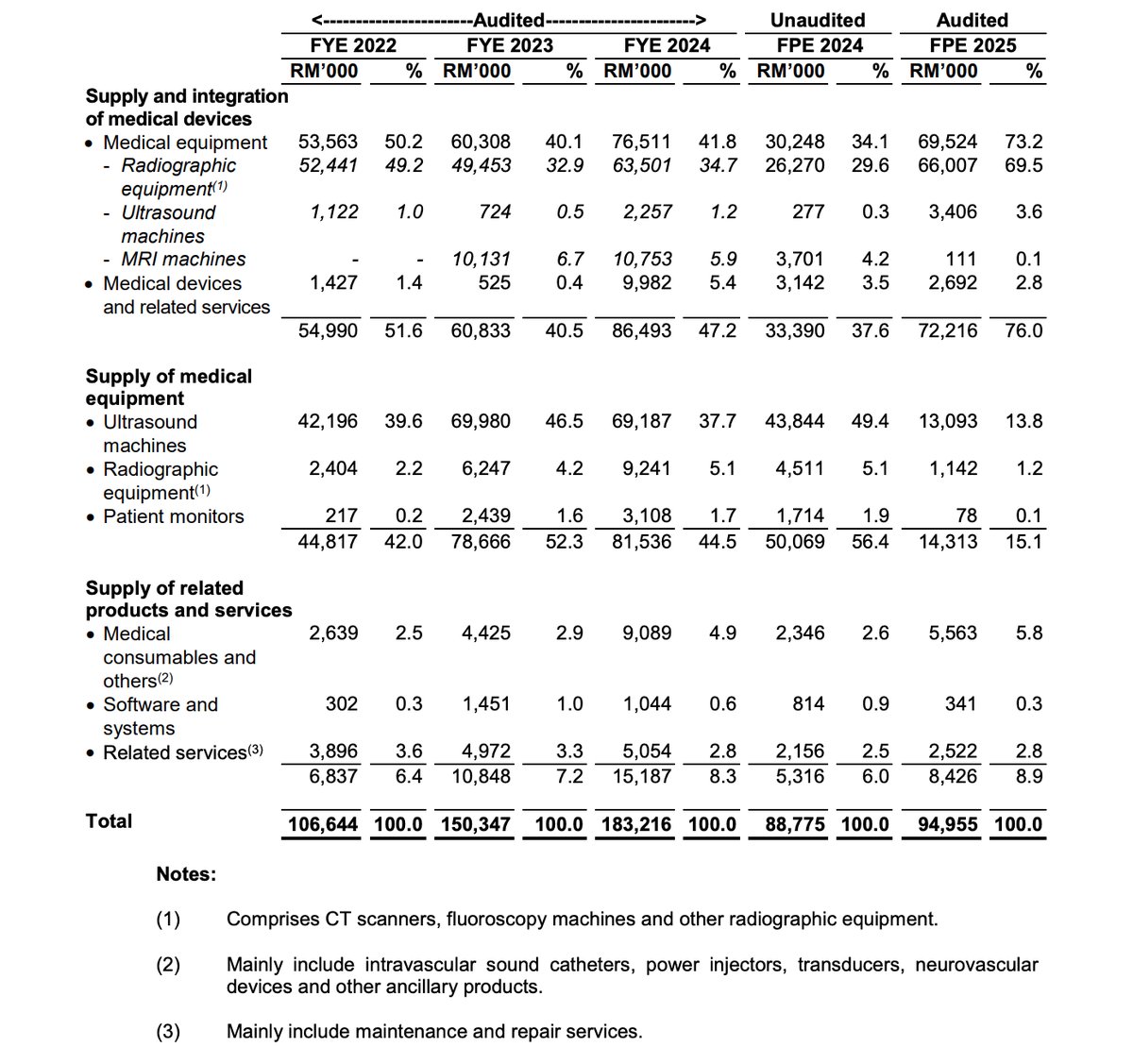

Business Segments

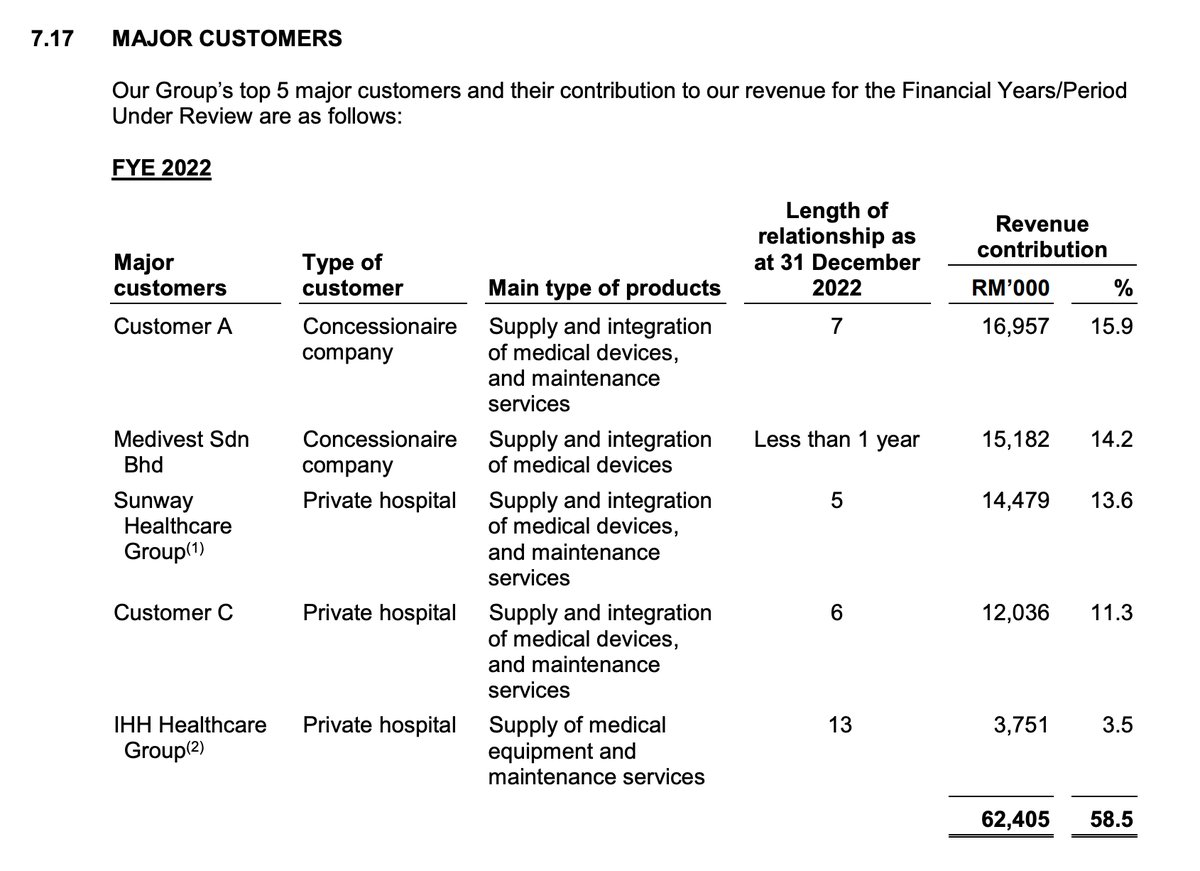

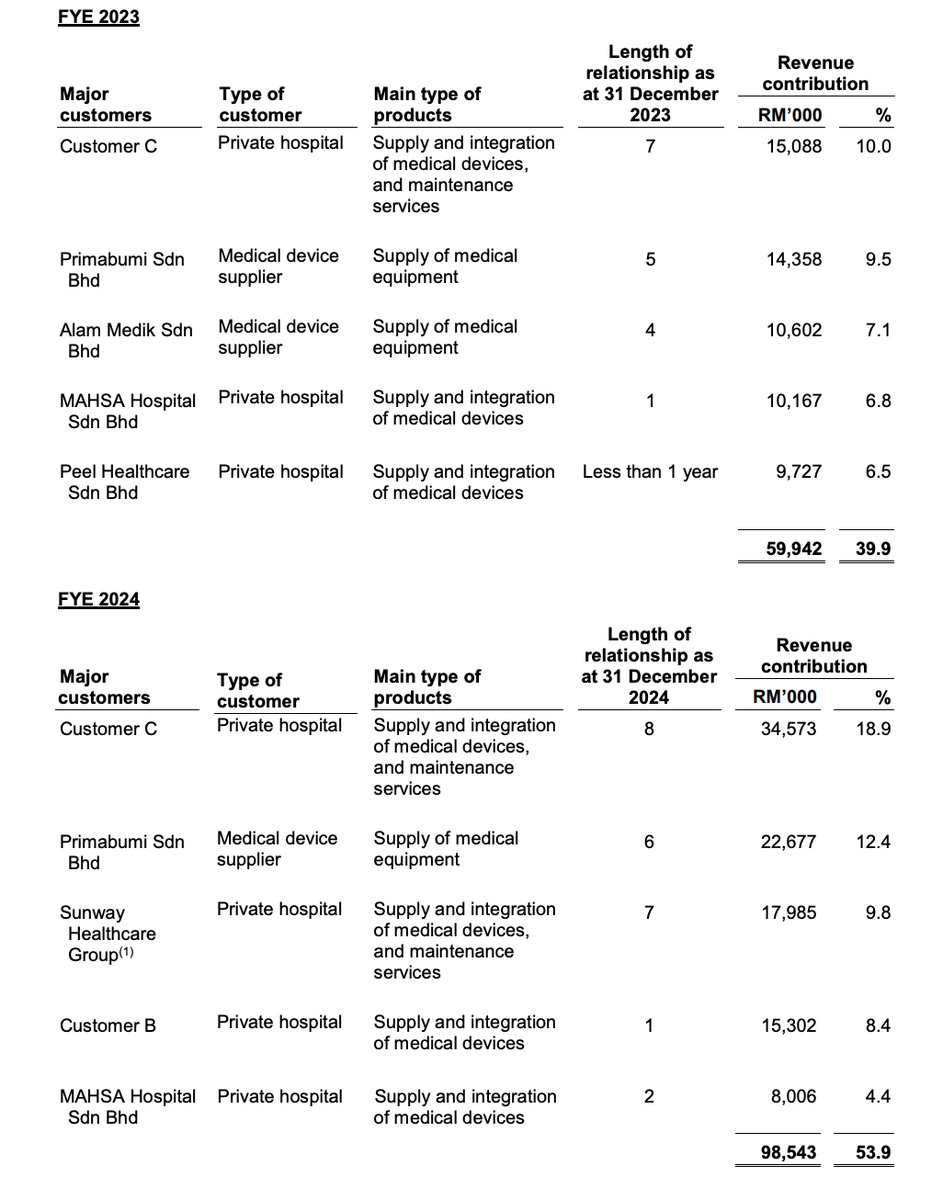

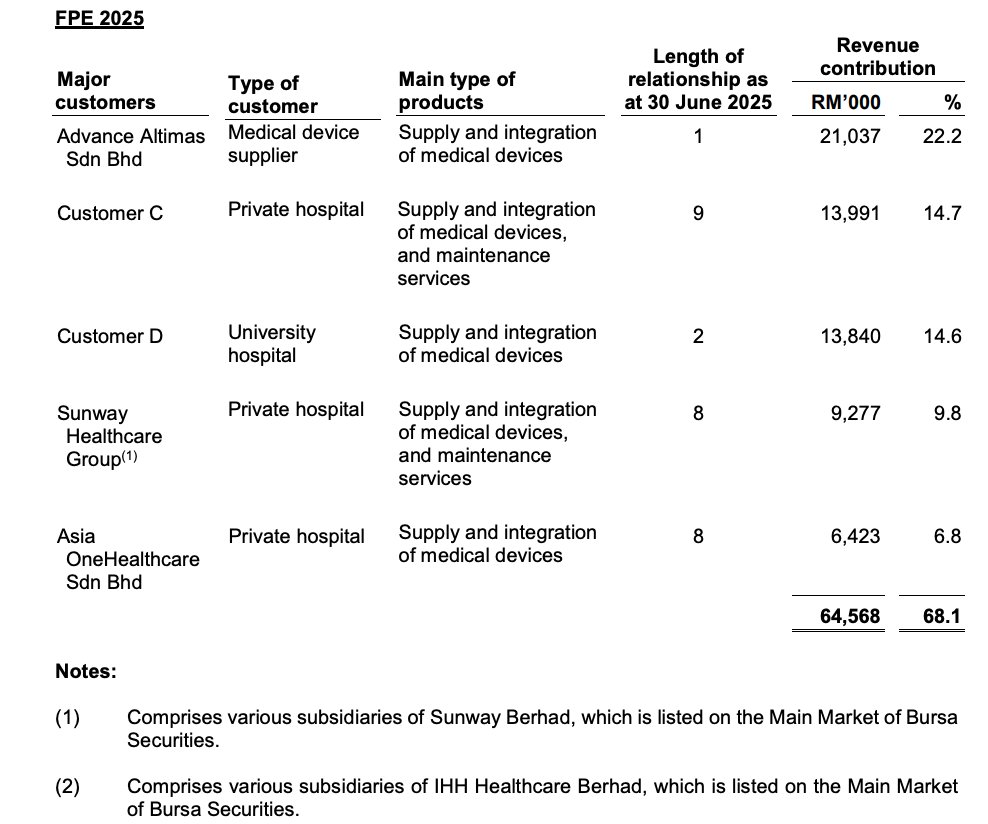

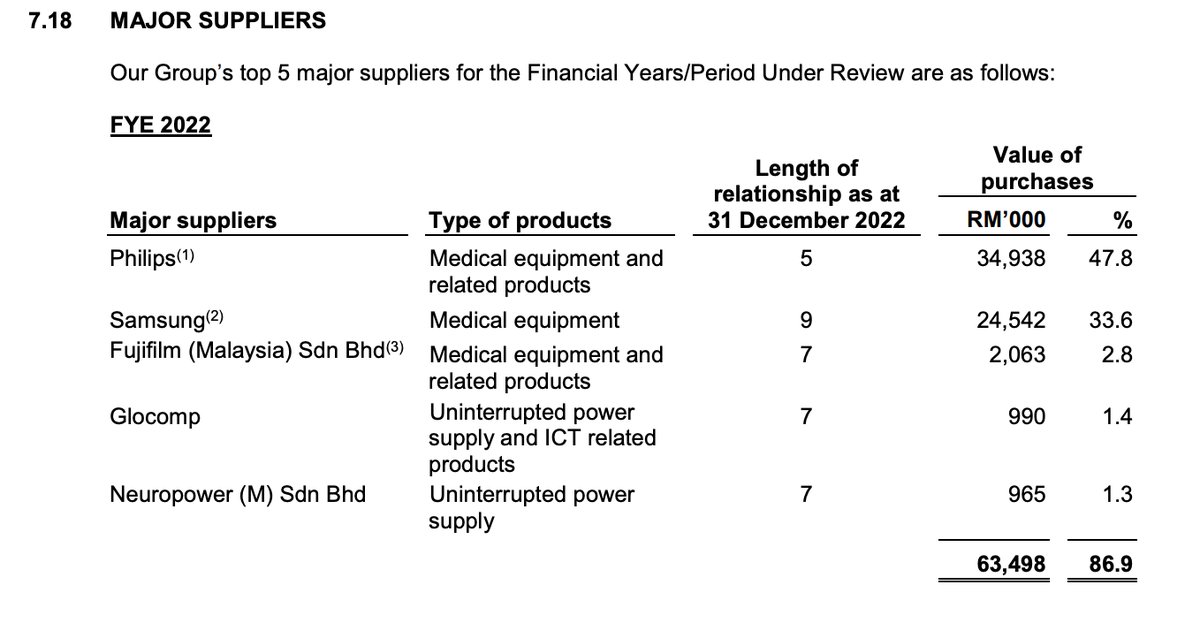

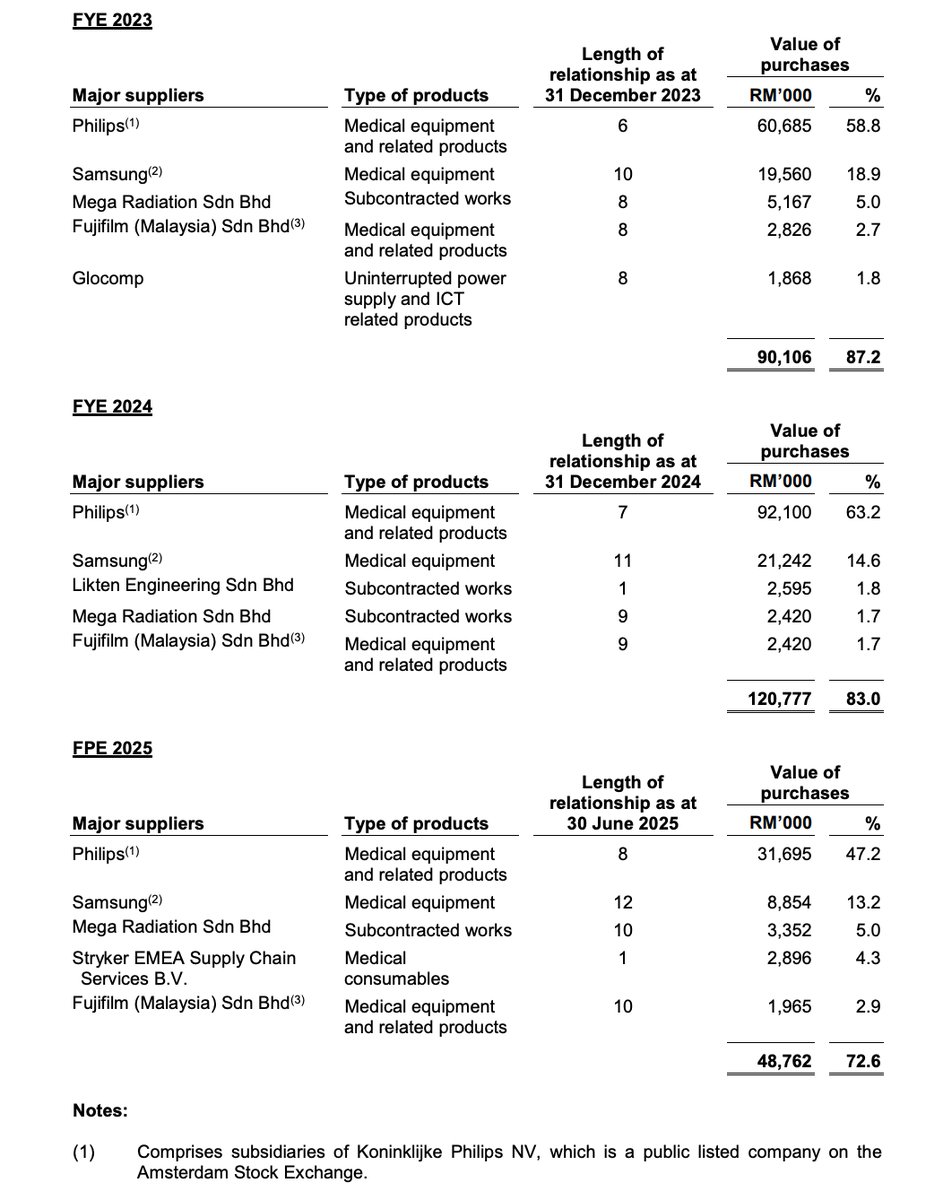

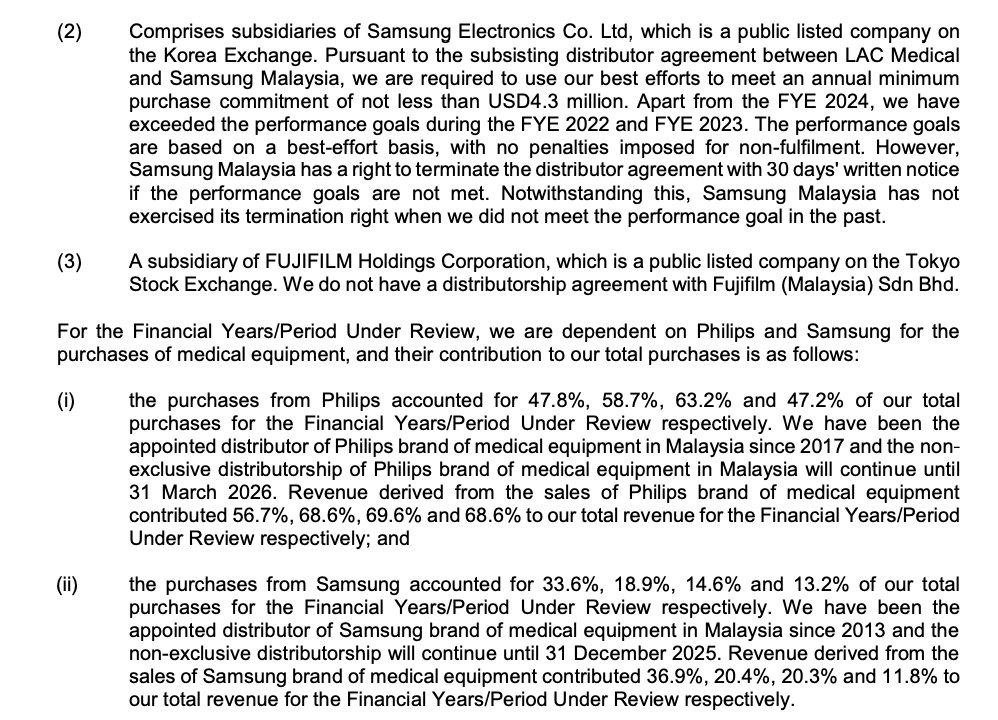

Major Customers

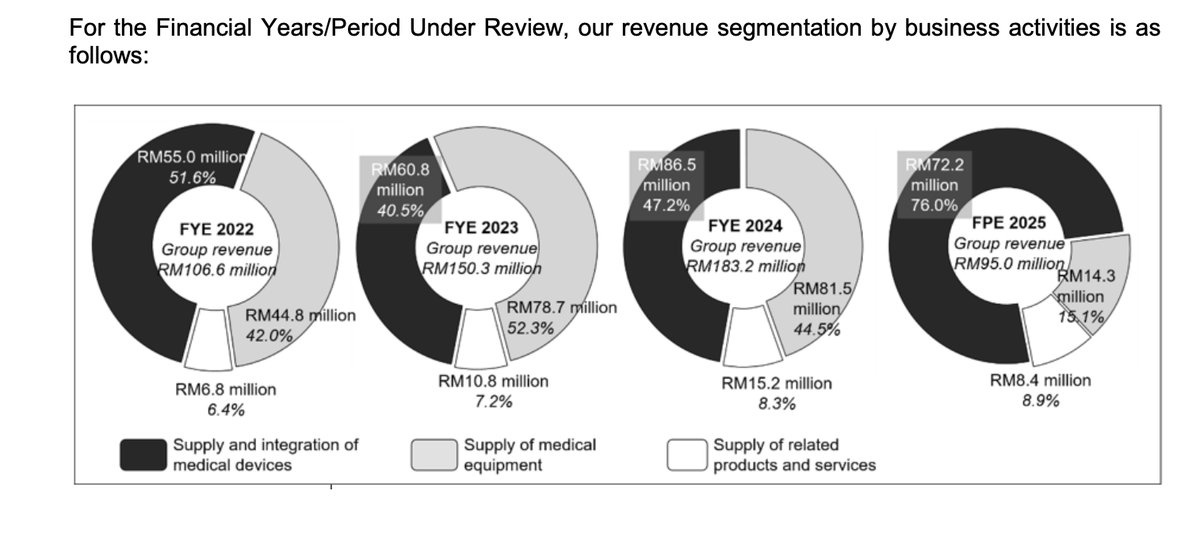

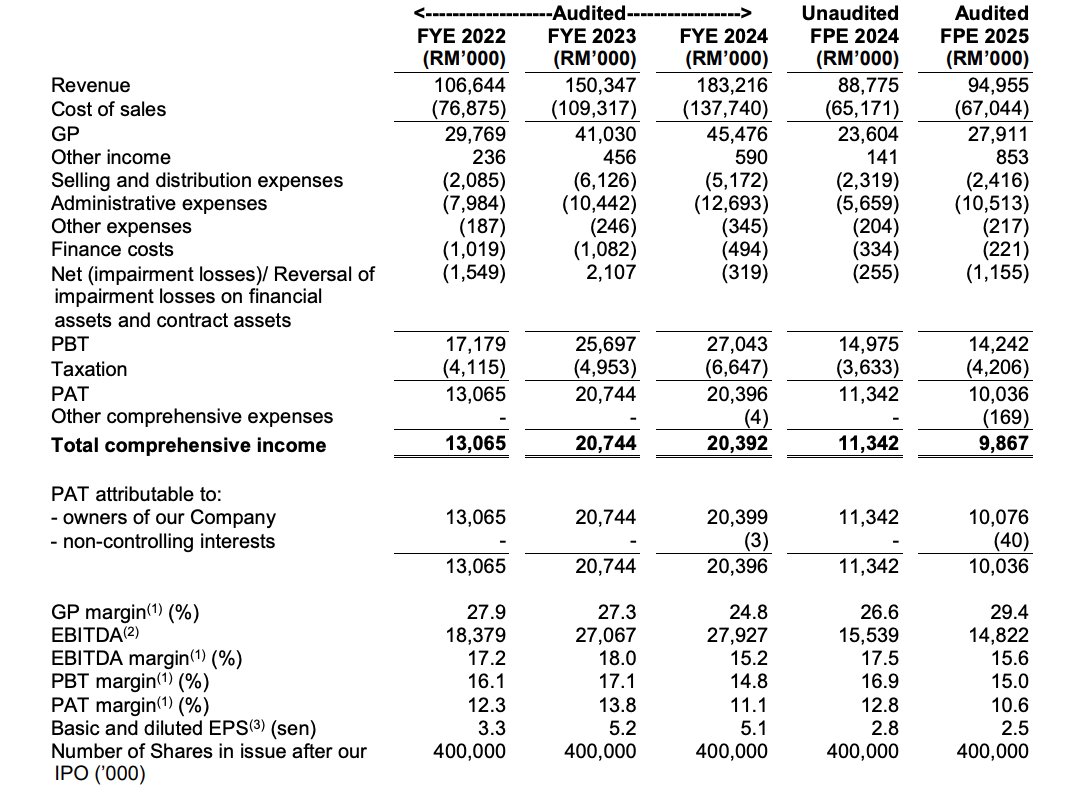

Revenue by Financial Year Ended

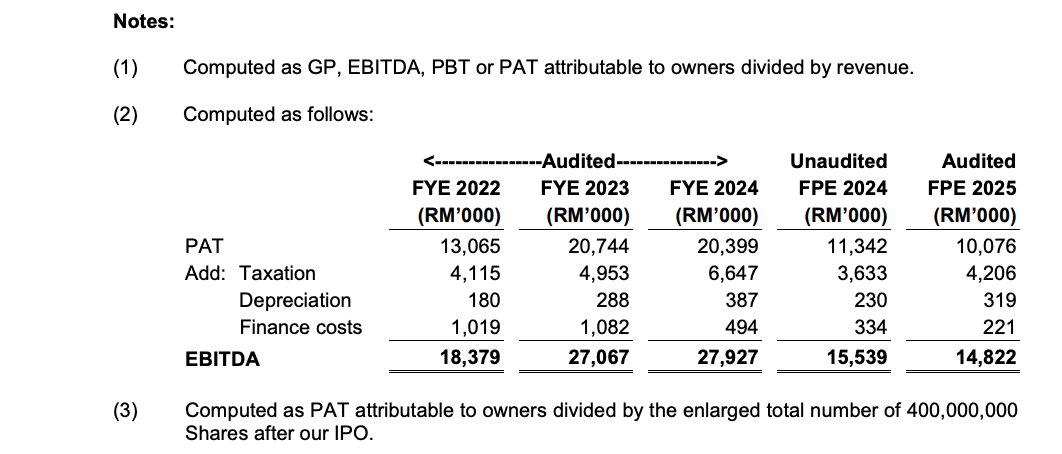

Profit After Tax (PAT) by Financial Year Ended

Revenue by Financial Period Ended

Profit After Tax (PAT) by Financial Period Ended

SWOT Analysis

Strengths

- Complex Integration Experts: Unlike peers who mostly sell "loose" units, LAC Med specializes in the difficult renovation and construction work required for heavy MRI/CT scanners, making them indispensable to hospitals.

- Top-Tier Brand Rights: They hold authorized distributorships for Philips and Samsung, giving them immediate credibility and access to best-in-class technology that UMC (Life Support focus) and BCMALL (Mixed focus) cannot offer in the exact same configuration.

- Unlimited Construction Capacity: With a CIDB Grade G7 license, LAC Med can bid for massive hospital renovation projects directly, capturing the profit margin on both the machinery and the construction work. In contrast, peers like BCMALL (without G7) likely cannot bid for the full infrastructure package, forcing them to outsource construction and split the project profits with third-party contractors.

Weaknesses

- Zero Manufacturing IP: Unlike UMC (which manufactures its own HydroX brand), LAC Med is a pure middleman. This results in lower profit margins (~11%) compared to UMC (~16.7%) and no ownership of intellectual property.

- Lumpy Project Revenue: Their current income depends on winning large, one-off construction tenders. If no new hospitals are built in a specific quarter, revenue drops, unlike UMC’s steady flow of consumables.

Opportunities

- Indonesia Market Expansion: Securing exclusive rights for Alpinion in Indonesia allows them to finally break their "Malaysia-only" ceiling and tap into a population of 284 million, a volume growth story BCMALL does not have.

- Recurring Revenue Shift: The launch of EaaS (Equipment-as-a-Service) and MEAMS (Asset Management Software) allows them to transition from "one-off sales" to "monthly subscriptions," stabilizing their cash flow.

- Displacing Weaker Rivals: With BCMALL suffering negative margins (-5.9%) and distracted by non-medical segments, LAC Med is well-positioned to aggressively capture their market share in the domestic diagnostic imaging space.

- Infrastructure Capex Boom: As government and private hospitals upgrade "heavy" infrastructure (Imaging Centers), LAC Med’s expertise in construction/integration makes them the preferred partner over "box-shifting" distributors.

Threats

- Territorial Growth Ceiling: Lacking proprietary products means they cannot scale globally like UMC; their maximum growth is strictly capped by the number of hospitals built in their specific licensed territories (Malaysia & Indonesia).

- Budget Cut Sensitivity: Selling massive capital equipment (MRI/CT) makes LAC Med more vulnerable to hospital budget cuts compared to UMC, which sells essential, lower-cost daily use items like patient monitors.

- Distribution Margin Squeeze: Without a manufacturing buffer like UMC, LAC Med is fully exposed to price hikes from principals (Philips/Samsung); they cannot offset rising costs by selling high-margin own-brand goods.

Key Highlights

Sorry, this feature only available for iSaham Pro

Conclusion

Sorry, this feature only available for iSaham Pro

LAC Med Berhad's Latest News