Kee Ming Group Berhad IPO's Analysis

Kee Ming Group Berhad

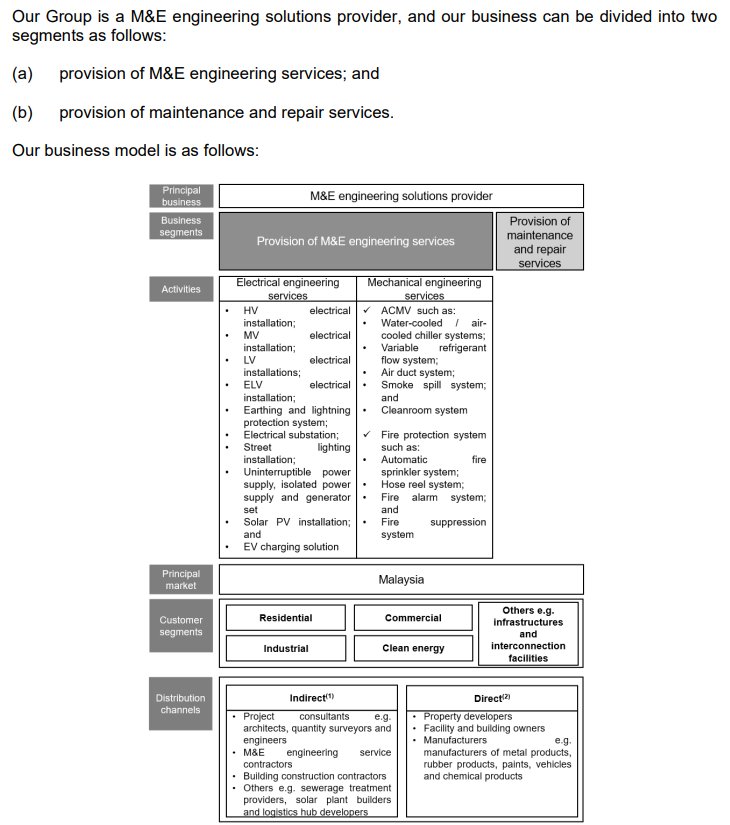

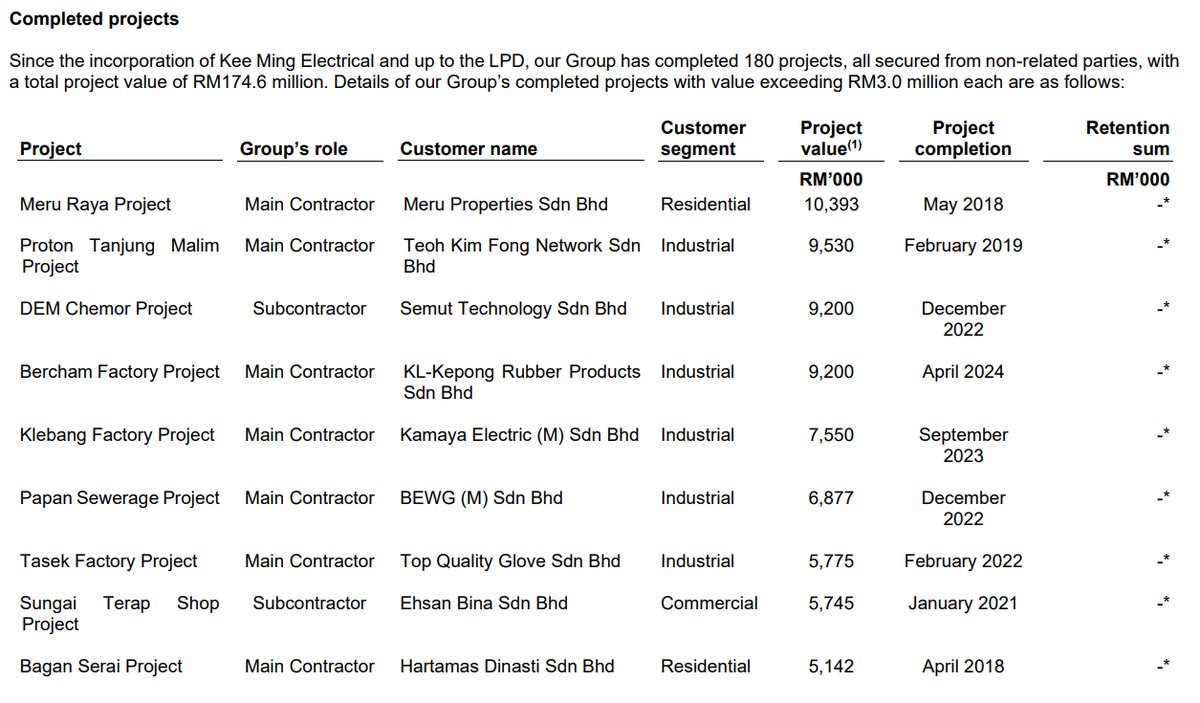

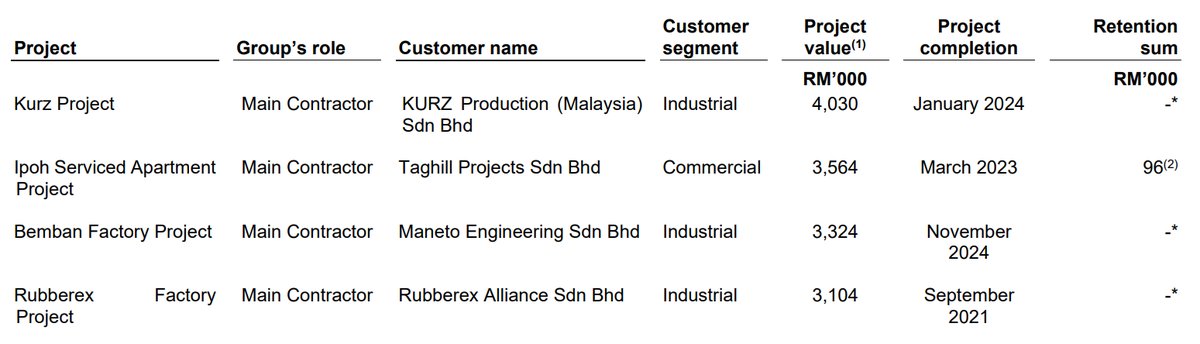

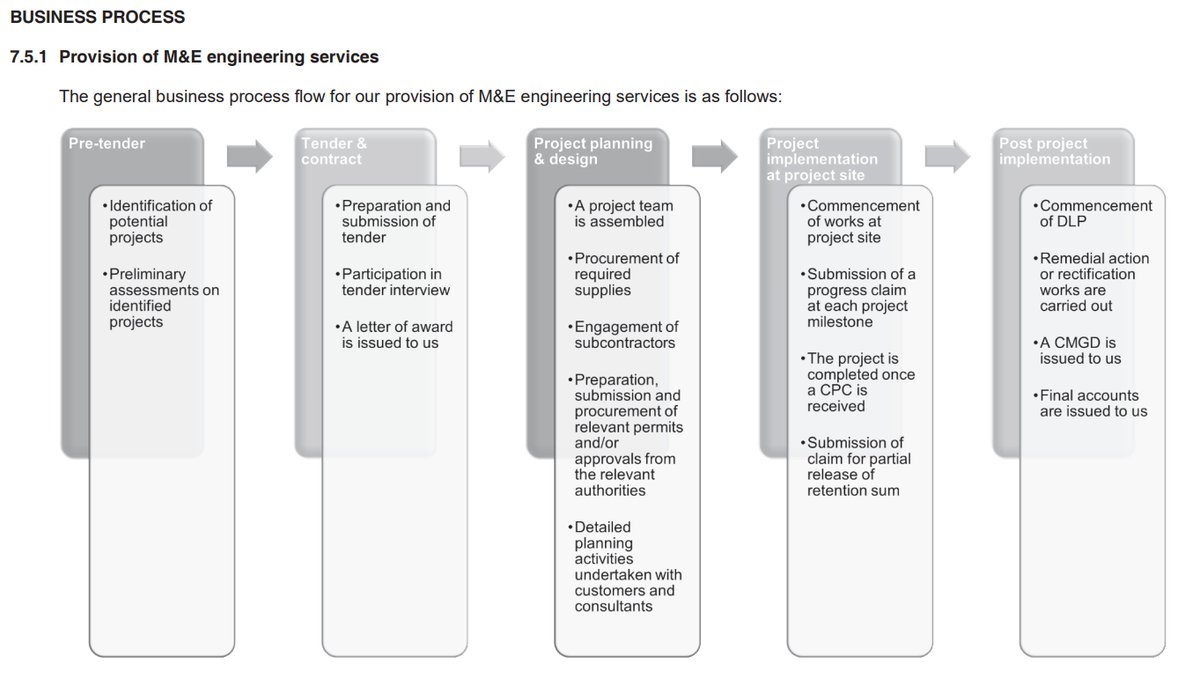

Kee Ming Group Berhad, through its subsidiary Kee Ming Electrical, is a Mechanical and Electrical (M&E) engineering solutions provider in Malaysia. The Group's principal activities involve the provision of M&E engineering services and maintenance and repair services. It has approximately 13 years of operating history, undertaking projects for both public and private sectors across industrial, commercial, residential, and clean energy segments. The services include the design, supply, installation, testing, and commissioning of a wide range of electrical systems (HV, MV, LV, ELV), mechanical systems (ACMV, fire protection), and other solutions like solar PV and EV charging installations.

IPO Details

Strategic Overview & Data Visuals

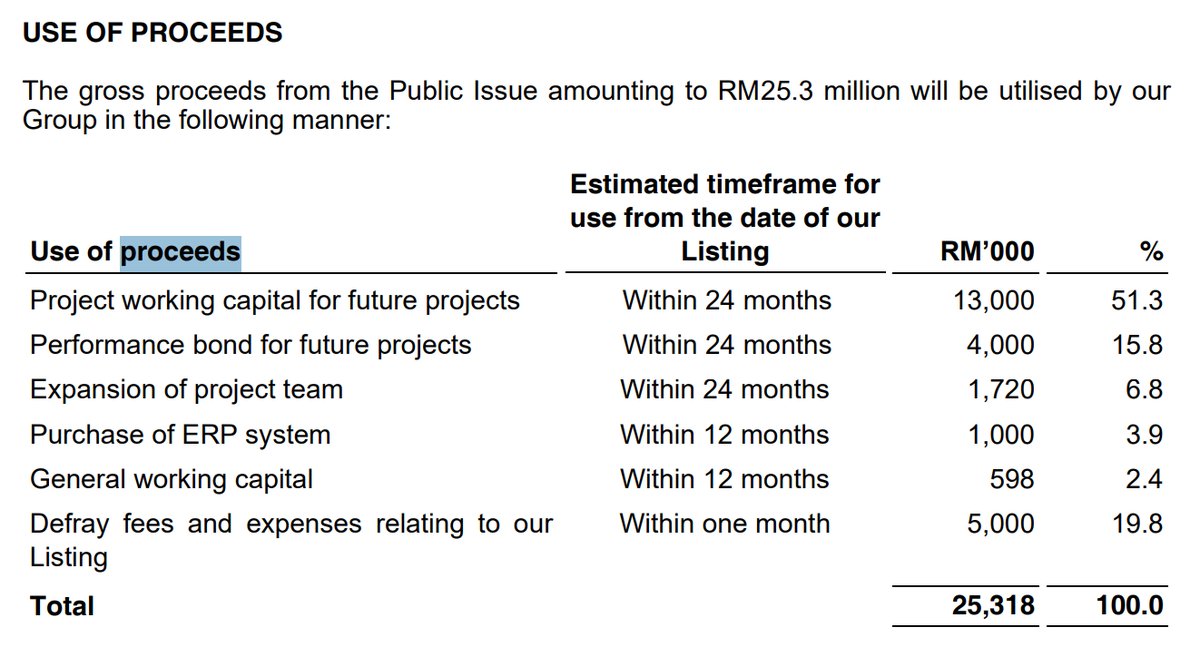

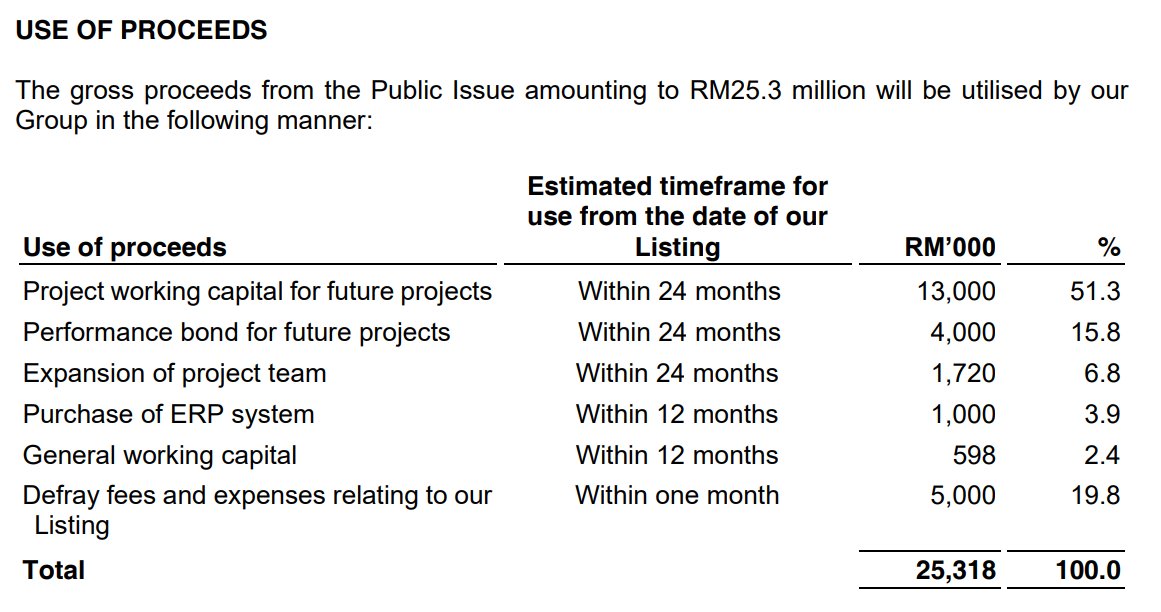

Utilisation of Proceeds

| Purpose | Amount (RM'000) | % | |

|---|---|---|---|

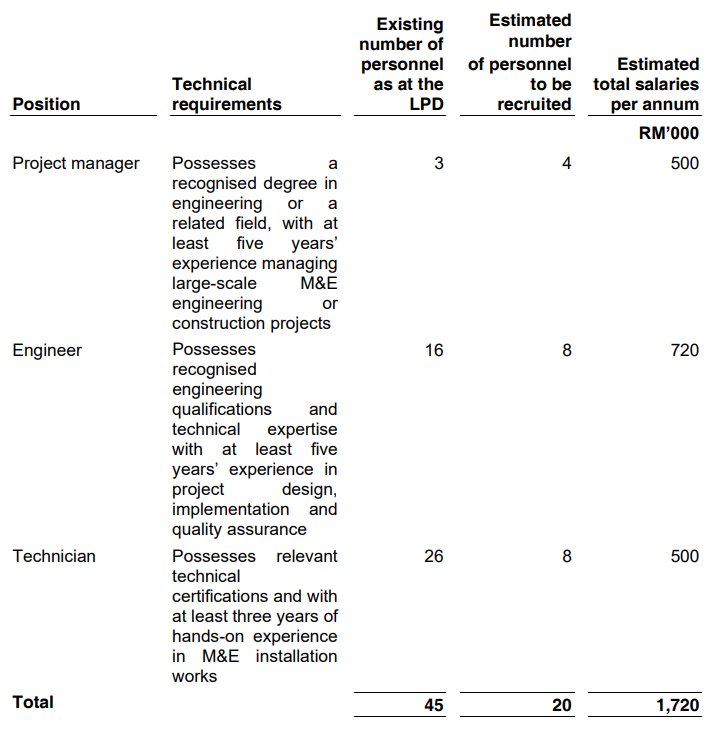

| Expansion | Expansion of project team | 1,720 | 6.8 |

| Expansion | Purchase of ERP system | 1,000 | 3.9 |

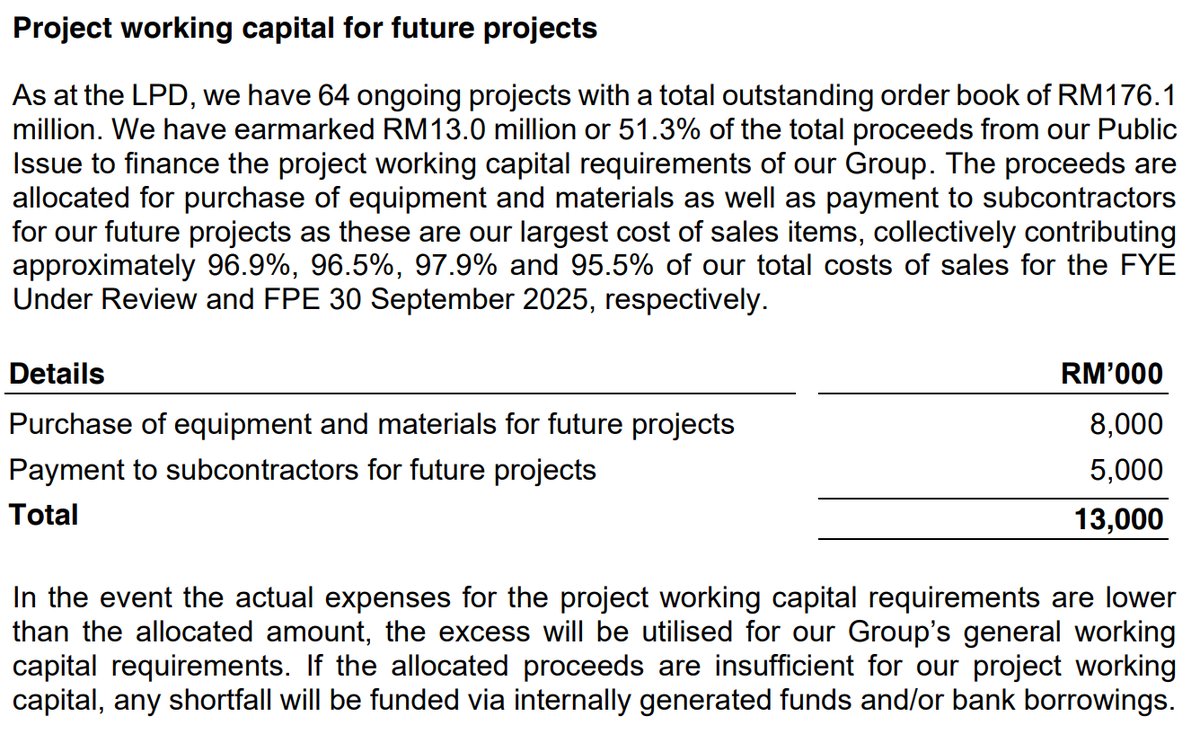

| Working capital | Project working capital for future projects | 13,000 | 51.3 |

| Working capital | General working capital | 598 | 2.4 |

| Others | Performance bond for future projects | 4,000 | 15.8 |

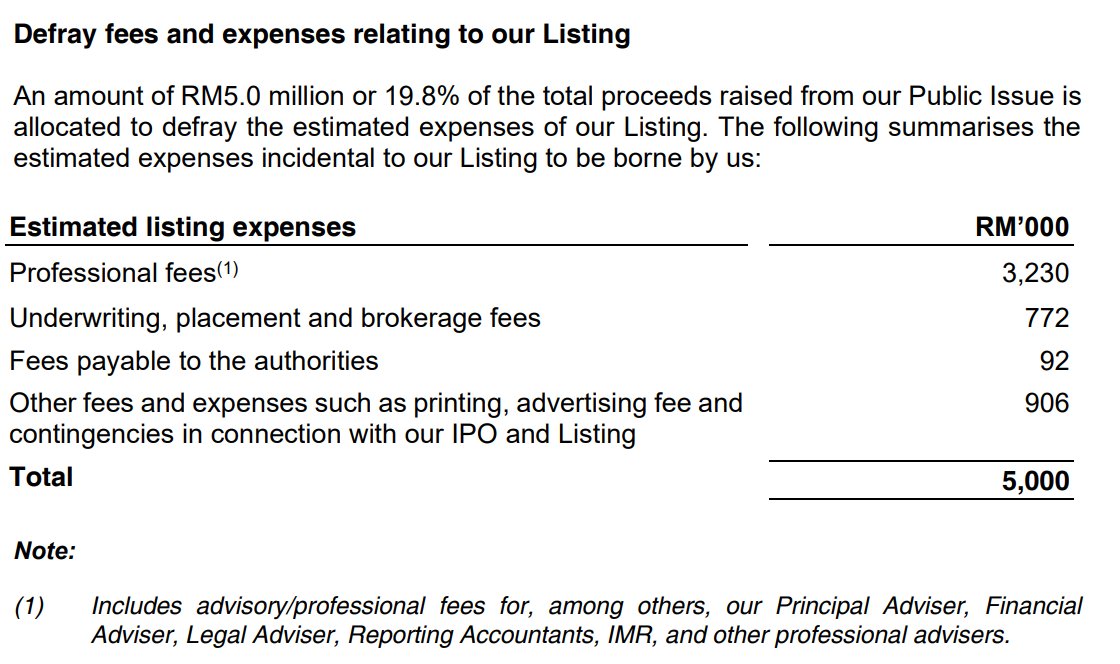

| Listing expenses | Defray fees and expenses relating to our Listing | 5,000 | 19.8 |

| Total | 25,318 | 100 | |

Analyst Highlights

| Date | Analyst Highlights |

|---|---|

|

27-Jan-2026

Public Invest |

|

|

27-Jan-2026

Mplus |

|

|

26-Jan-2026

Apex |

|

|

26-Jan-2026

RHB |

|

Utilisation of Proceeds

Business Segments

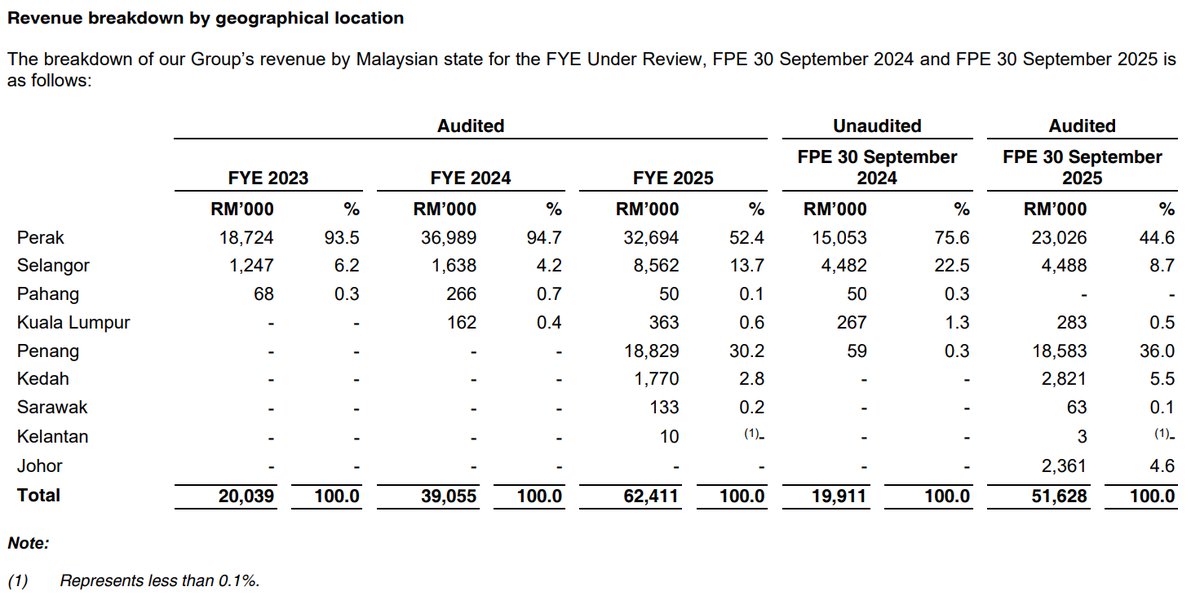

Geographical Segments

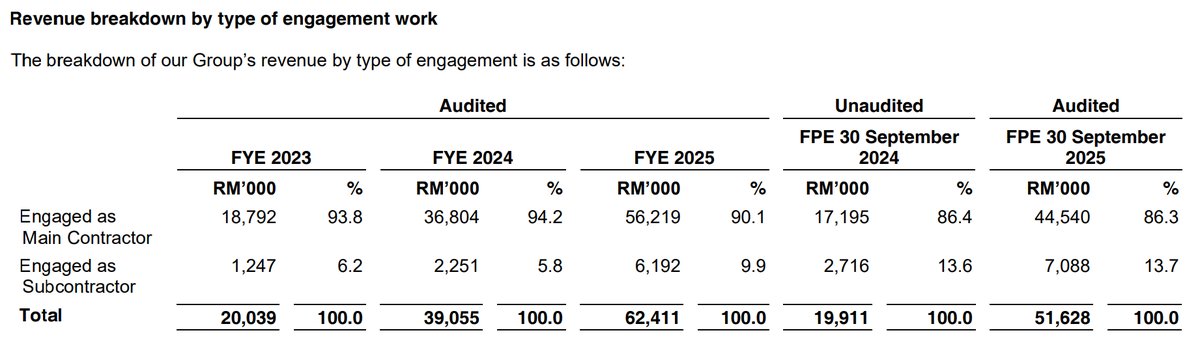

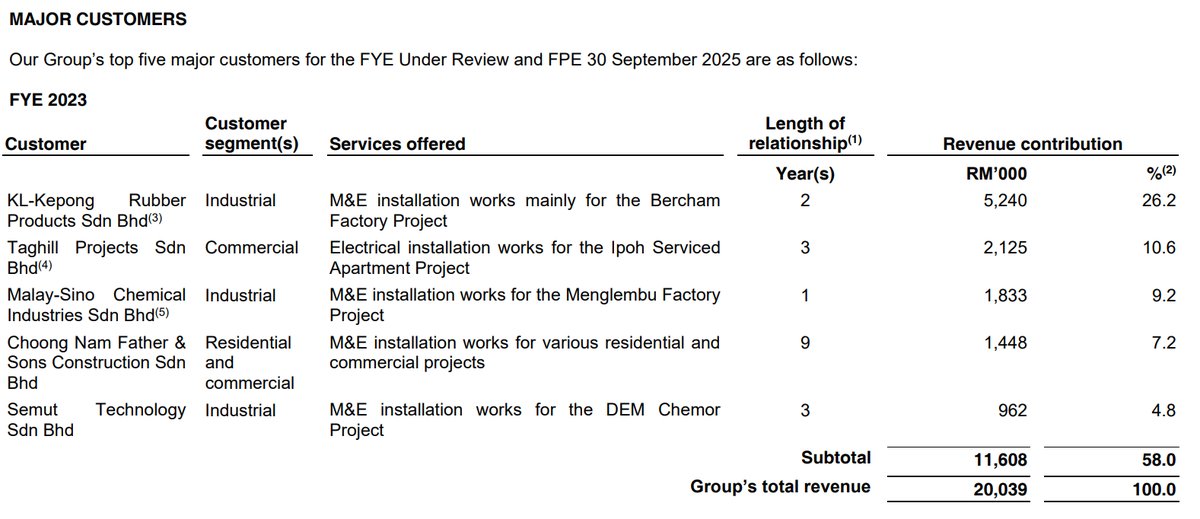

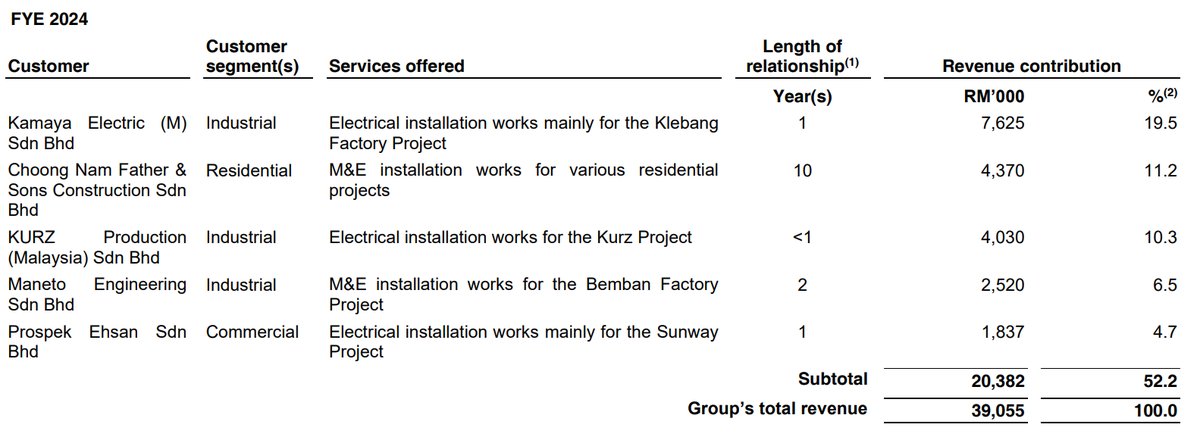

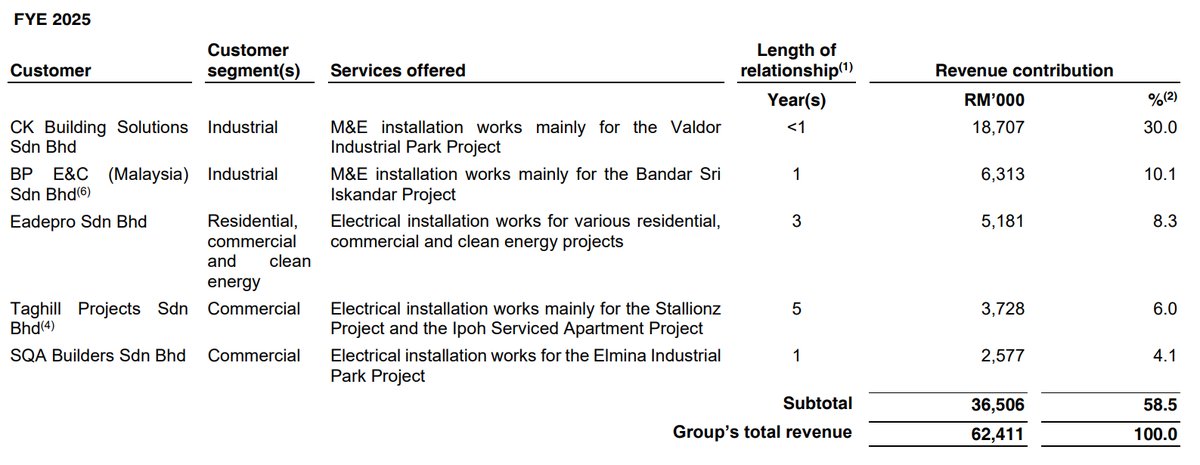

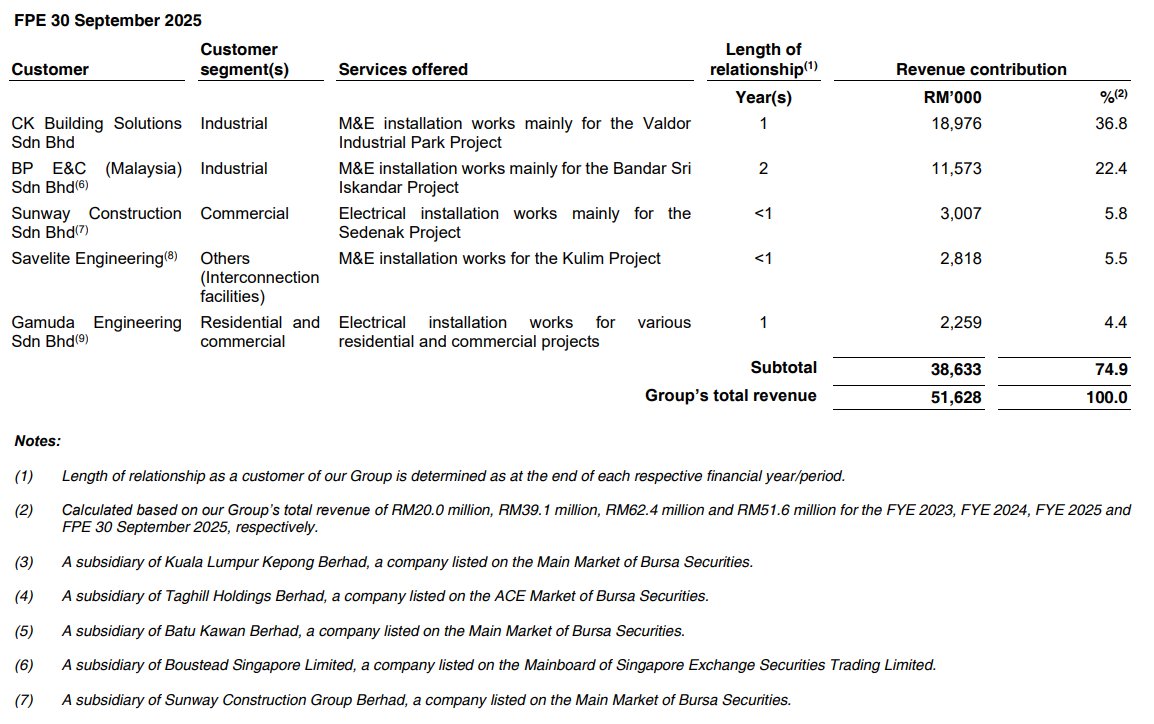

Major Customers

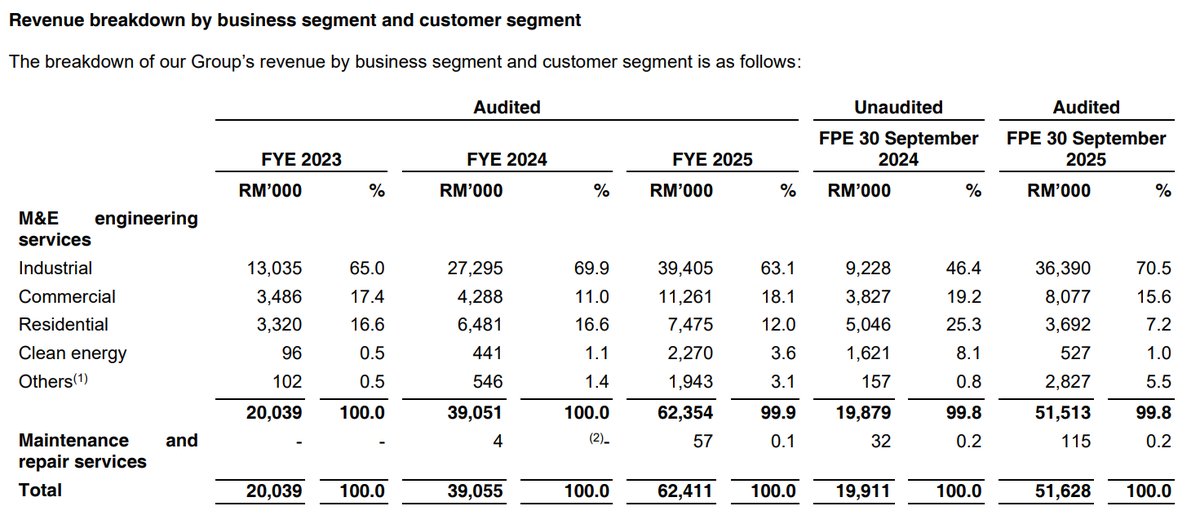

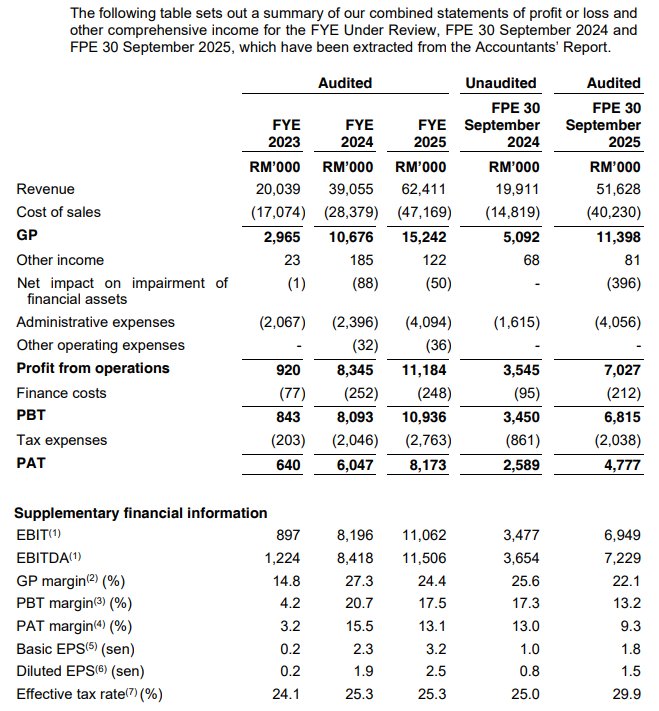

Revenue by Financial Year Ended

Profit After Tax (PAT) by Financial Year Ended

Revenue by Financial Period Ended

Profit After Tax (PAT) by Financial Period Ended

SWOT Analysis

Strengths

- Strategic Solarvest Backing: A 23.85% equity stake by Solarvest Holdings Berhad provides strategic access to high-growth renewable energy projects like solar farms and EV charging infrastructure.

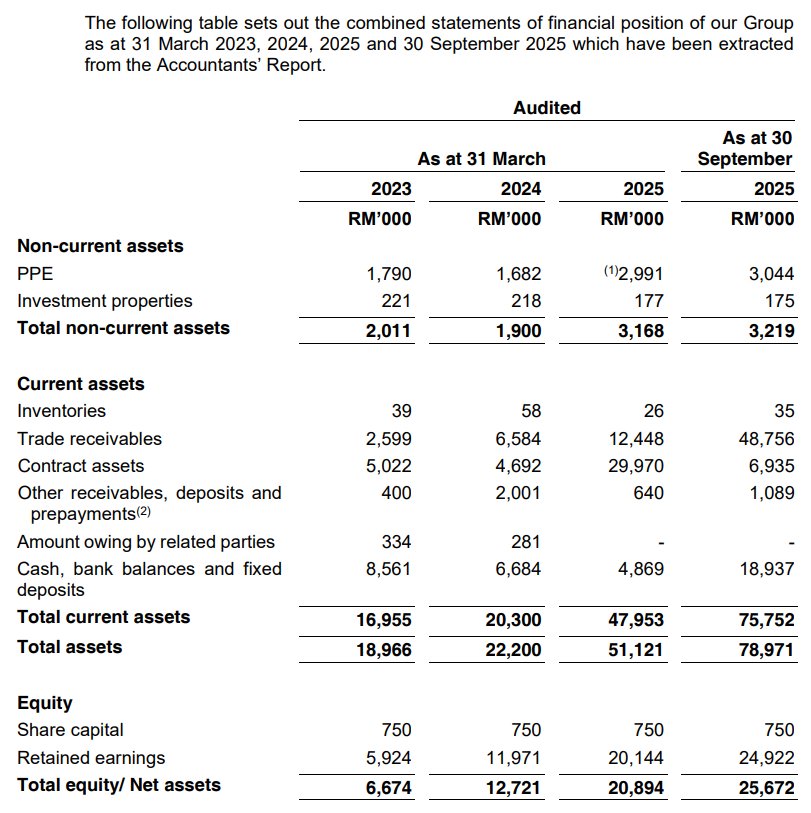

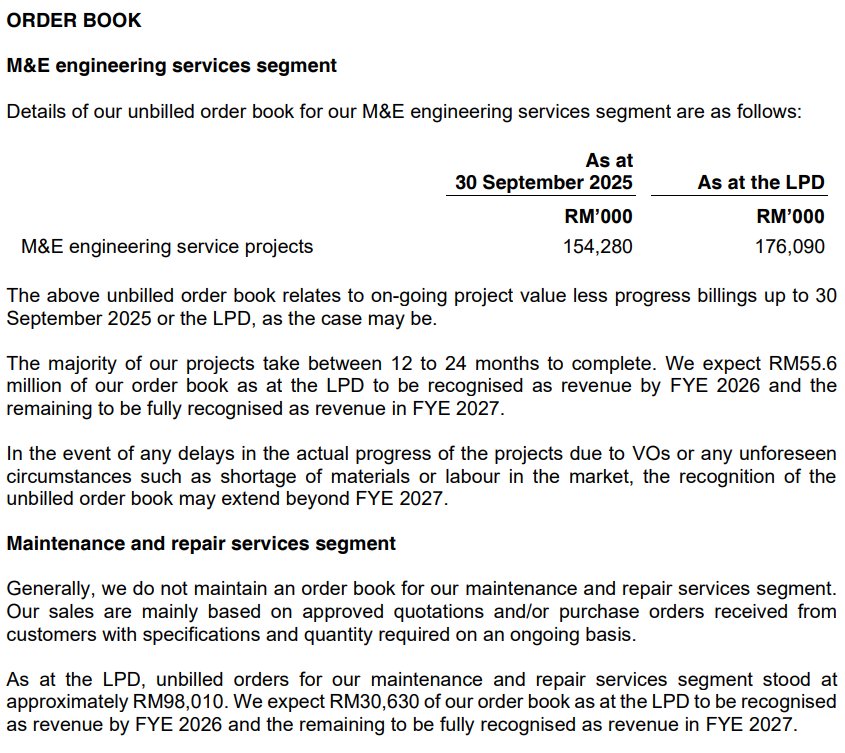

- Robust Orderbook: An unbilled order book of RM176.1 million provides strong earnings visibility, representing a 2.82x cover ratio over its FYE 2025 revenue.

- Strong Profitability: Achieved a high PAT margin of 13.1% in FYE 2025, outperforming the typically low single-digit margins of the construction and engineering sector.

- High-Value Project Capability: Possesses G7 Contractor and Class A Electrical Contractor licenses, enabling it to tender for projects of unlimited value, including large-scale public and private works.

Weaknesses

- High Customer Concentration: Significant reliance on a small number of clients, with the top 5 customers contributing 74.9% of revenue in FPE Sept 2025, posing a risk if a key contract is lost.

- Capital Intensive Operations: The business model requires high working capital, with 51.3% (RM13.0 million) of IPO proceeds allocated to fund project execution.

Opportunities

- Renewable Energy Pivot: The national push for renewable energy (e.g., NETR, LSS programmes) creates significant demand for Kee Ming's expertise in High Voltage interconnection facilities for solar farms.

- Data Centre Expansion: Malaysia's growth as a regional data centre hub presents a major opportunity for specialised M&E services, including HV substations and cooling systems.

- Industrial Hub Growth: Expansion into high-growth industrial areas like Penang and Selangor allows the company to tap into a larger pool of industrial and commercial projects.

Threats

- Premium IPO Valuation: The IPO is priced at a Hybrid PE of ~12.9x, a premium to direct peers like West River (9.5x), creating pressure to deliver on high growth expectations to justify the valuation.

- Material Price Volatility: Profit margins are exposed to fluctuations in the prices of key raw materials such as copper and steel, which can impact project costs and profitability.

- Foreign Labour Dependency: Reliance on foreign workers for project execution poses a risk from potential changes in government labour policies or supply shortages, which could lead to project delays.

Key Highlights

Sorry, this feature only available for iSaham Pro

Conclusion

Sorry, this feature only available for iSaham Pro

Kee Ming Group Berhad's Latest News