Guan Huat Seng Holdings Berhad IPO's Analysis

Guan Huat Seng Holdings Berhad

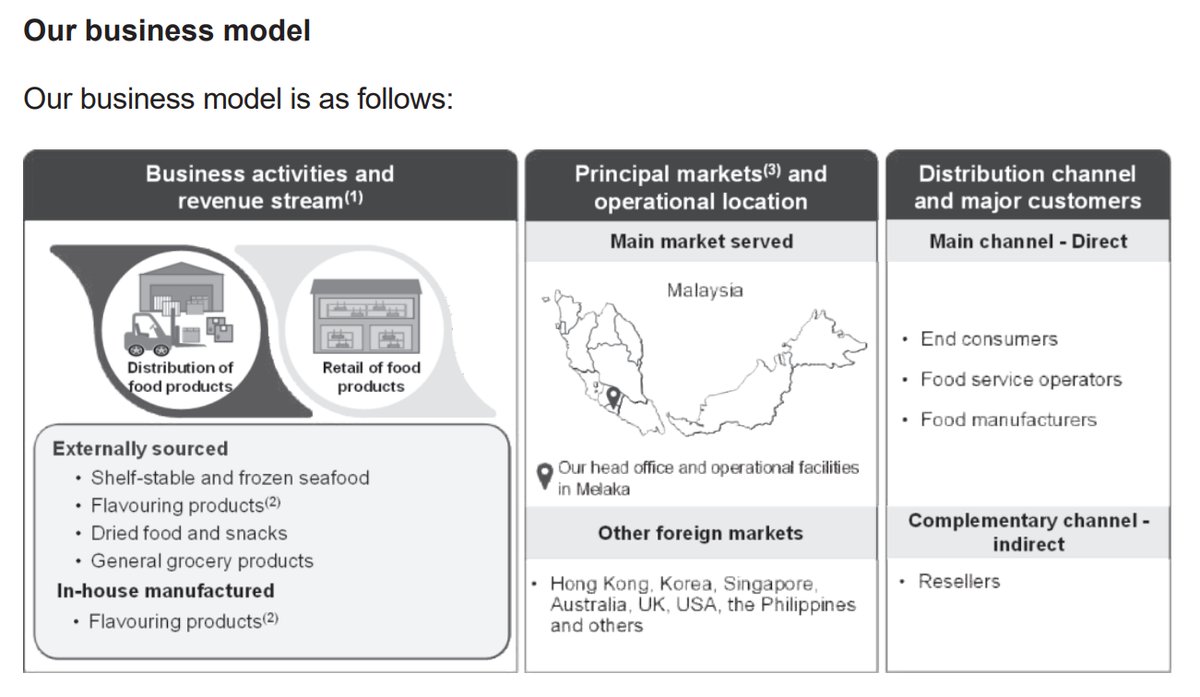

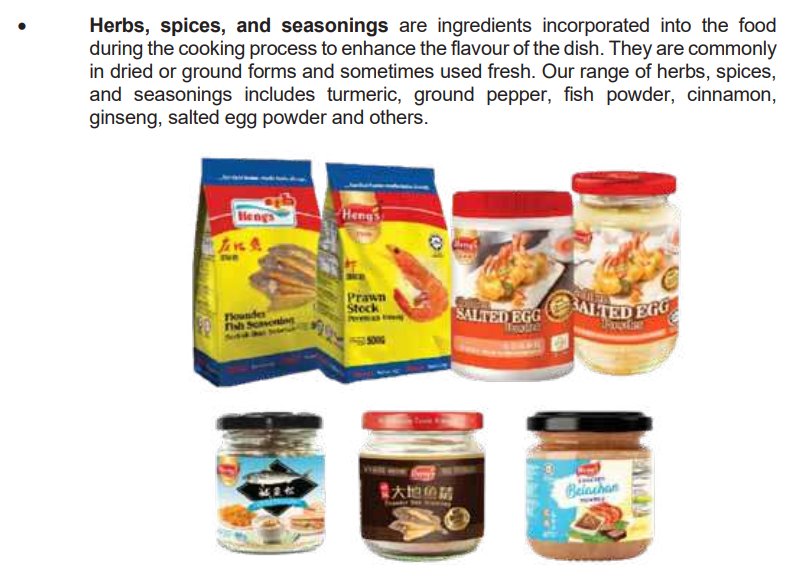

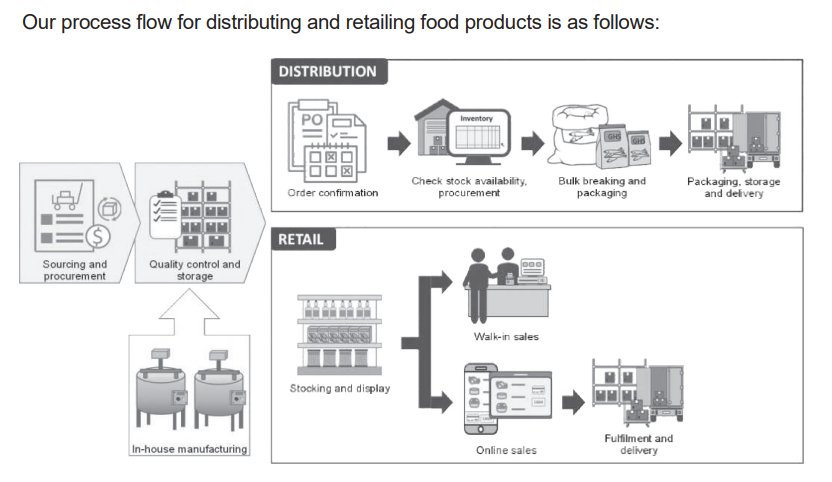

Guan Huat Seng Holdings Berhad is involved in the distribution and retail of food products including shelf-stable and frozen seafood, flavouring products, dried food and snacks, and general grocery products through its subsidiaries GHS Heng Kee and GHS Food Industries. The Group also manufactures flavouring products such as condiments, sauces and pastes, herbs, spices and seasonings at its facilities in Melaka, Malaysia.

IPO Details

Market:

ACE

Principal Adviser:

TA Securities Holdings Berhad

Issuing House:

Malaysian Issuing House (MIH)

Shariah Status:

SC (No)

Listing Price:

0.25

MITI allocation?:

Yes

Closing Date:

09-Jan-2026

Balloting Date:

13-Jan-2026

Listing Date:

22-Jan-2026

Oversubscription rate:

4.78x

Average Analysts FV

:

Mplus (0.29)

iSaham IPO Score

:

Market Cap:

118.38 M

Number of Shares:

473.50 M

( info)

Median Sectors PE:

N/A

Median Peers PE:

Strategic Overview & Data Visuals

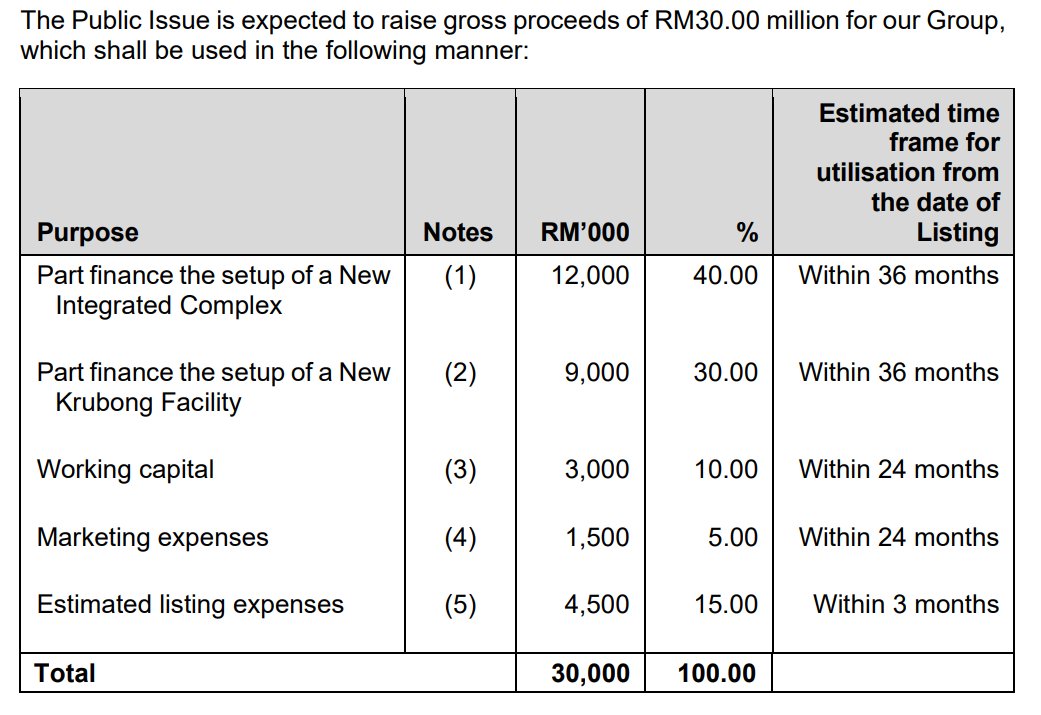

Utilisation of Proceeds

| Purpose | Amount (RM'000) | % | |

|---|---|---|---|

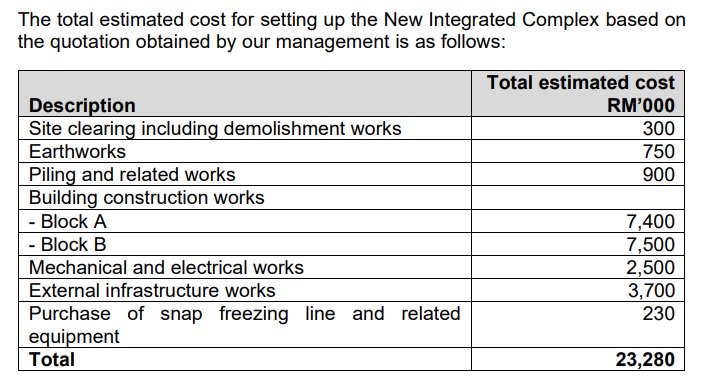

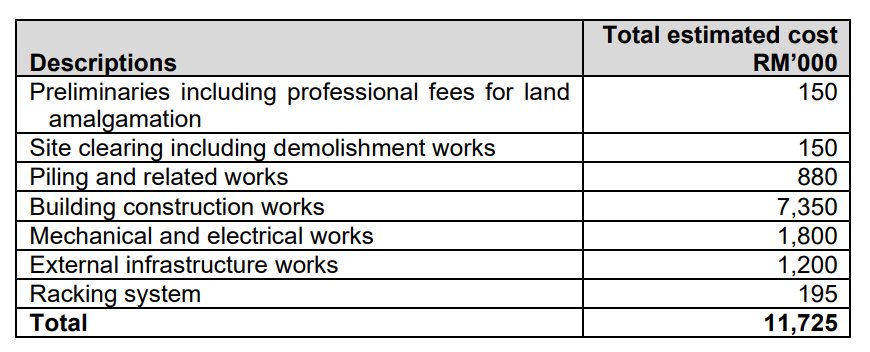

| Expansion | Part finance the setup of a New Integrated Complex | 12,000 | 40 |

| Expansion | Part finance the setup of a New Krubong Facility | 9,000 | 30 |

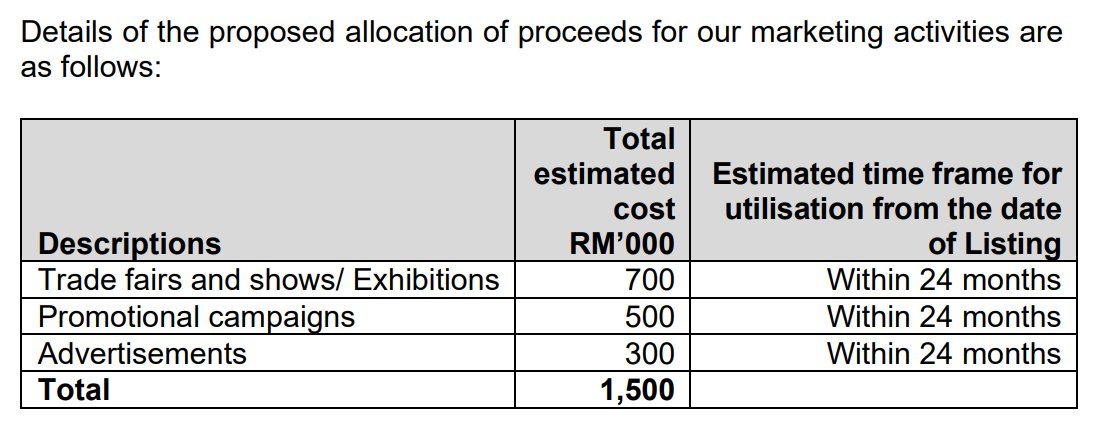

| Expansion | Marketing expenses | 1,500 | 5 |

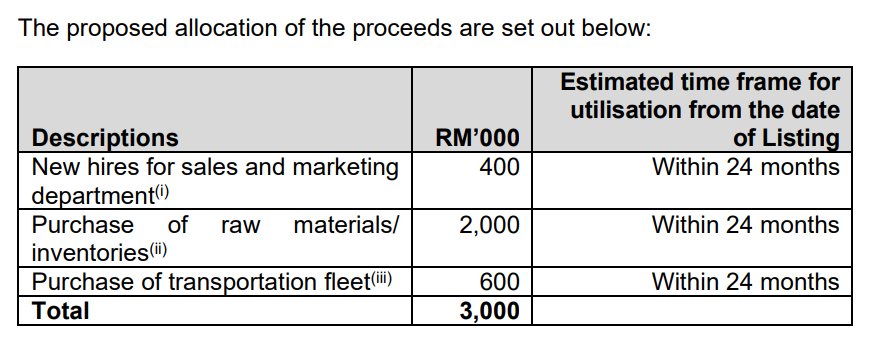

| Working capital | Working capital | 3,000 | 10 |

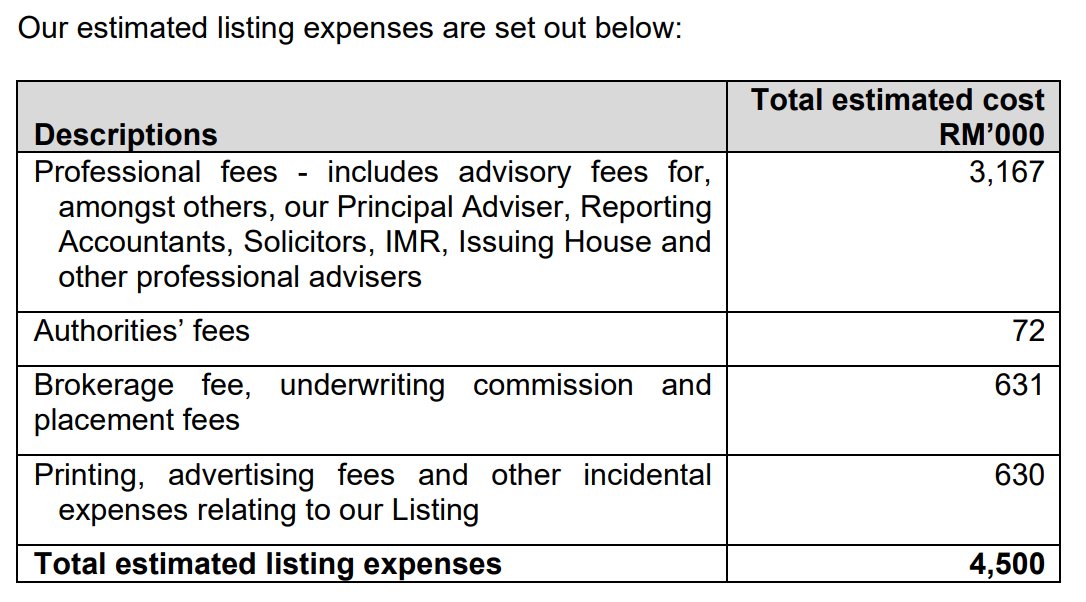

| Listing expenses | Estimated listing expenses | 4,500 | 15 |

| Total | 30,000 | 100 | |

Analyst Highlights

| Date | Analyst Highlights |

|---|---|

|

09-Jan-2026

Mplus |

|

Utilisation of Proceeds

Business Segments

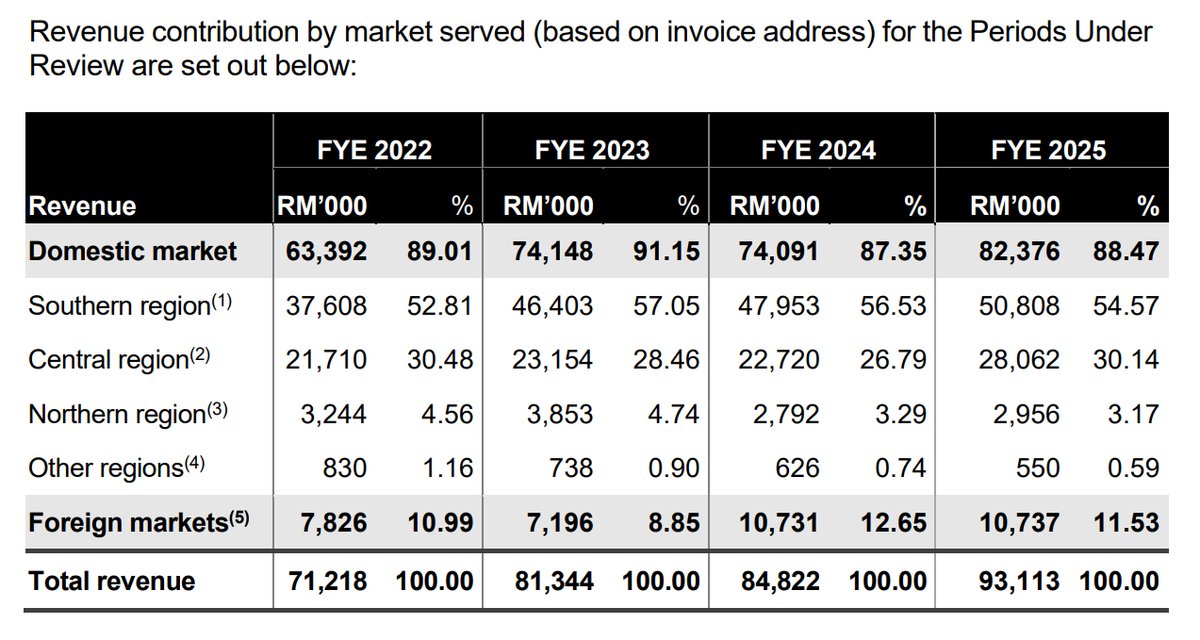

Geographical Segments

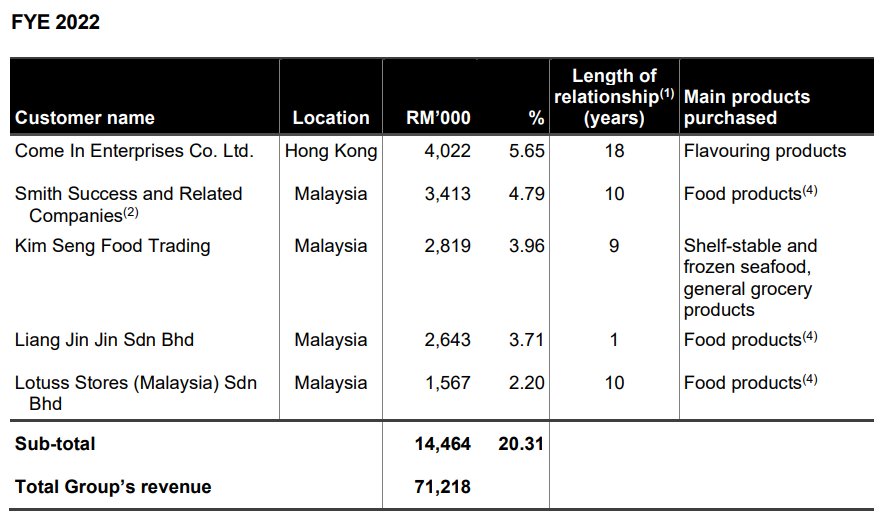

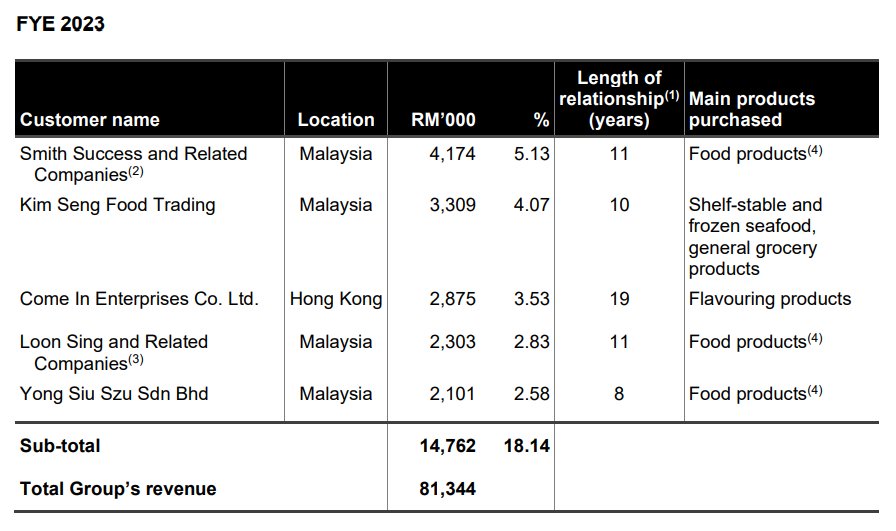

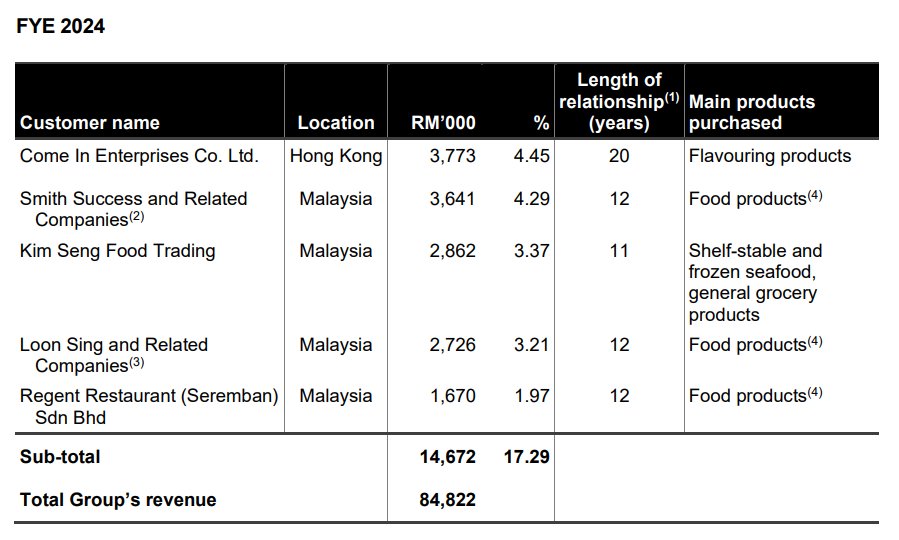

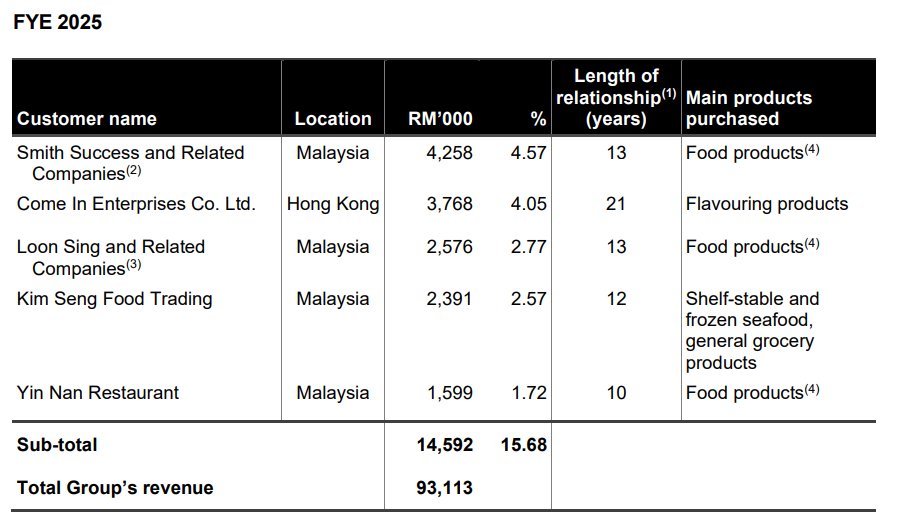

Major Customers

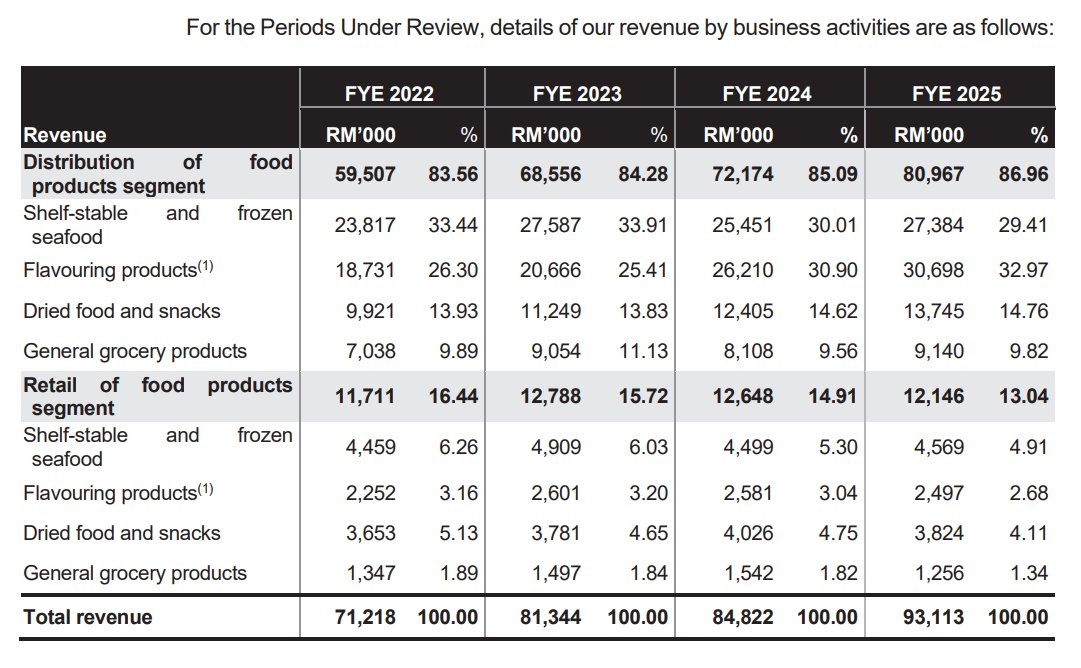

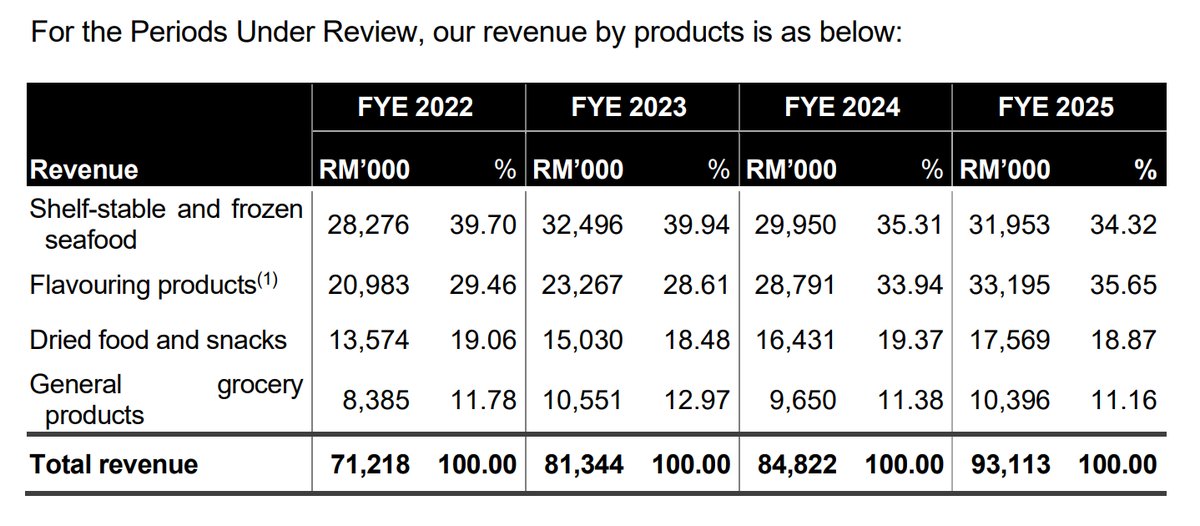

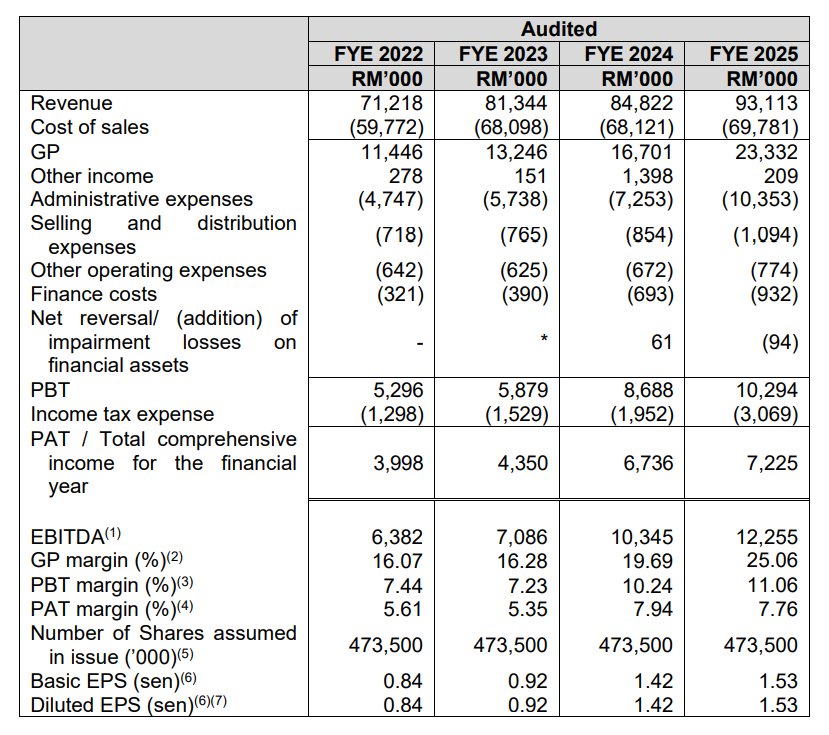

Revenue by Financial Year Ended

Profit After Tax (PAT) by Financial Year Ended

SWOT Analysis

Strengths

- Integrated Business Model: Combines manufacturing, distribution, and retail, achieving superior net profit margins (7.8%) compared to pure distributors like Kim Teck Cheong (~2-3%).

- Established House Brands: Proprietary brands like 'Heng's' and 'Makbest' contribute approximately 30% of revenue, providing better margins and brand equity than third-party products.

- Diversified Customer Base: Low customer concentration risk, with the top 5 customers accounting for only 15.7% of total revenue, mitigating dependency on any single client.

Weaknesses

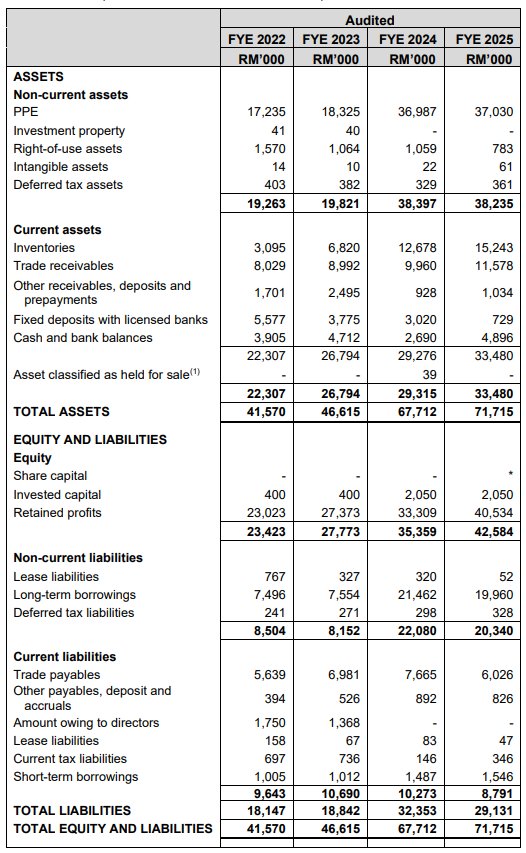

- Rising Inventory Days: Inventory turnover period has increased significantly from 18 days (FYE2022) to a projected 73 days (FYE2025), indicating potential working capital inefficiency.

- Negligible Market Share: Holds a very small market presence (<1%) within the highly fragmented Malaysian food distribution industry, which limits pricing power and economies of scale.

Opportunities

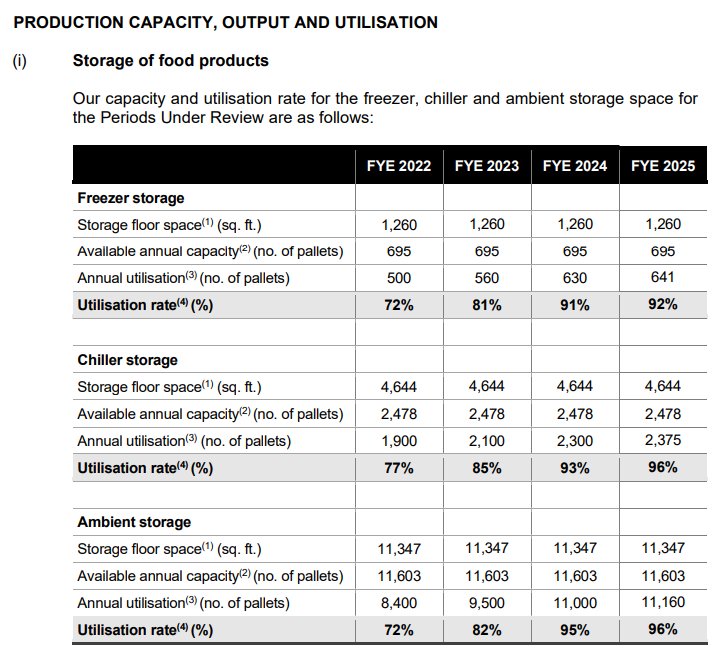

- Capacity Expansion: IPO proceeds are allocated to new facilities to resolve current capacity constraints, where effective utilisation is at 96%, and support future product range expansion.

- Tourism Recovery: The retail segment, located in the tourist hub of Melaka, is well-positioned to benefit from the external factor of a resurgence in domestic and international tourism.

Threats

- Input Cost Volatility: Profitability is exposed to fluctuations in raw material prices and foreign exchange rates, as approximately 40% of purchases are denominated in foreign currency.

- Intense Competition: Operates in a low-barrier industry with numerous established competitors, including Kim Teck Cheong, Harrisons, and Rex Industry, which pressures market share and margins.

Key Highlights

Sorry, this feature only available for iSaham Pro

Conclusion

Sorry, this feature only available for iSaham Pro

Guan Huat Seng Holdings Berhad's Latest News