Foodie Media Berhad IPO's Analysis

Foodie Media Berhad

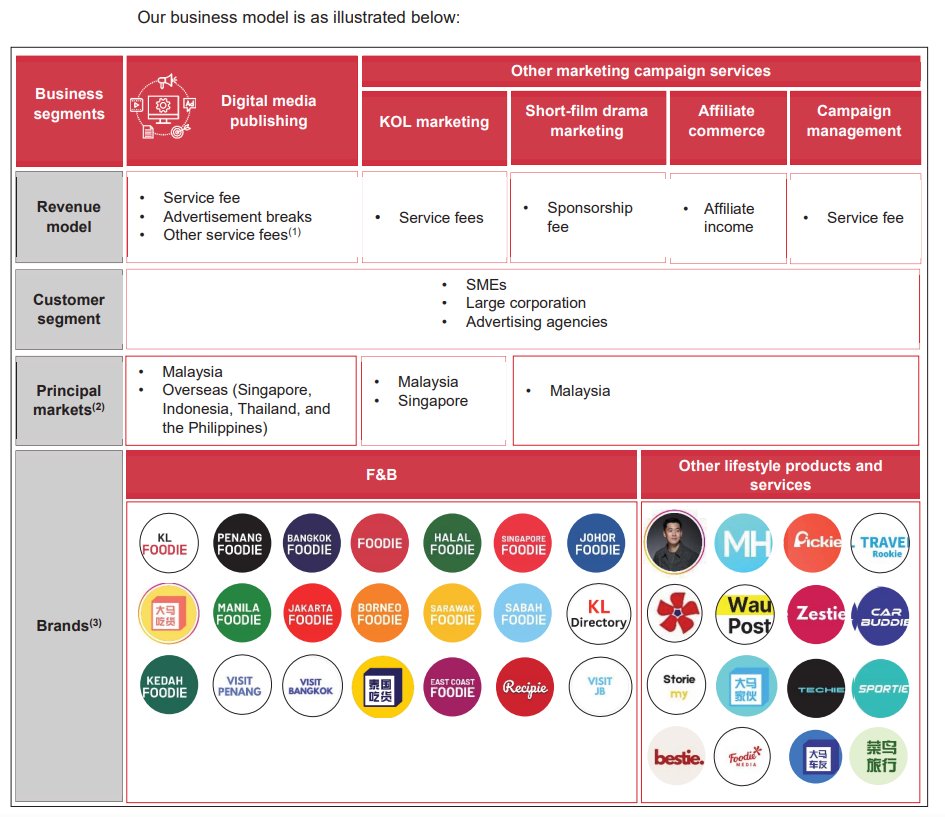

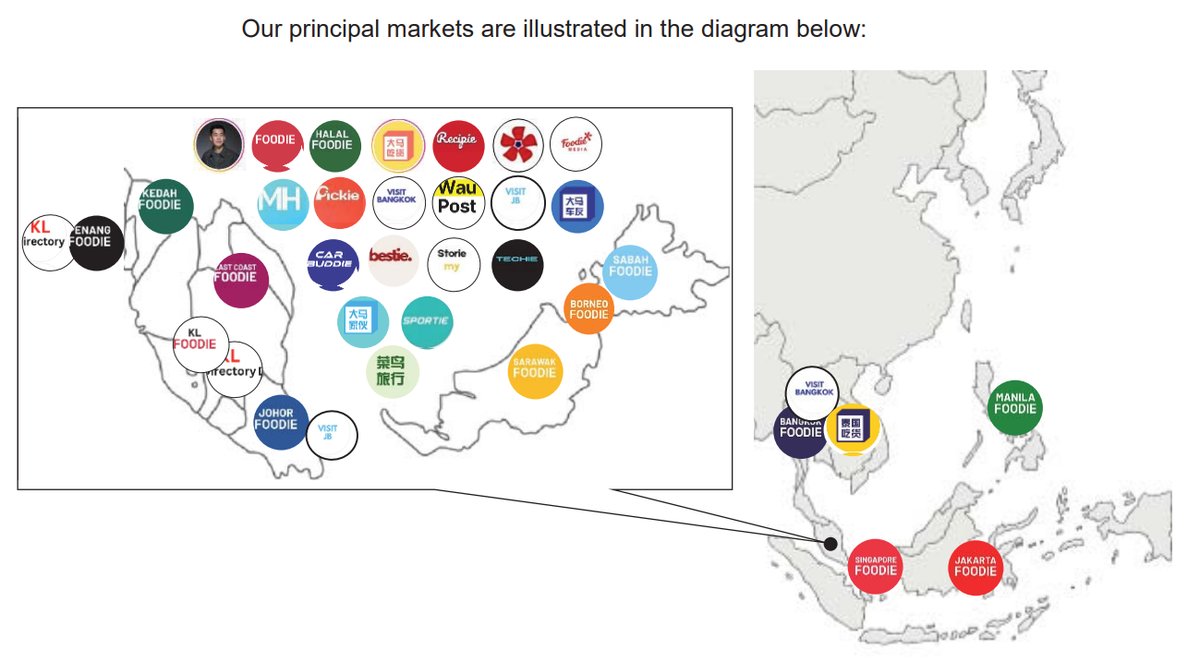

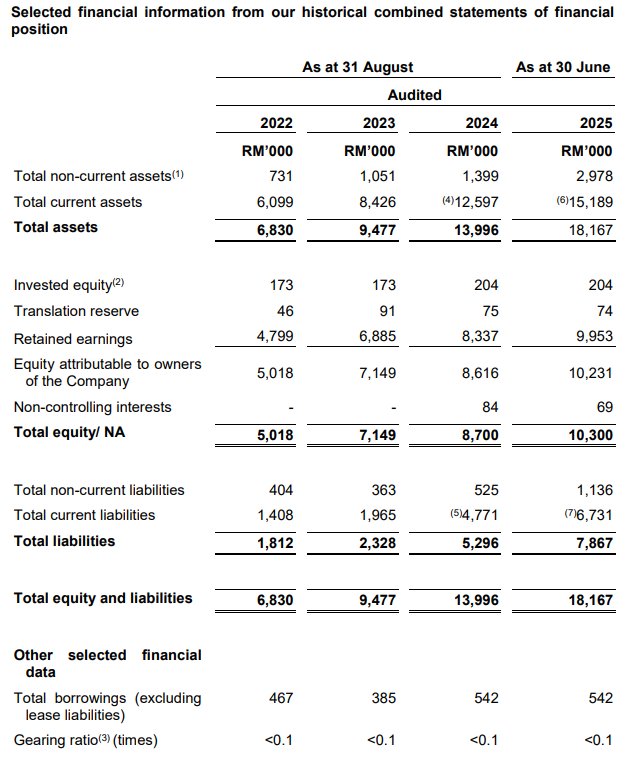

Foodie Media Berhad is primarily involved in the digital media publishing business, where it creates, produces, and publishes digital content on social media pages and blogs across various platforms like Facebook, Instagram, and TikTok. The company operates a portfolio of 37 lifestyle-focused brands across Southeast Asia, covering F&B, property, travel, and technology. In addition to digital media publishing, the Group provides other marketing campaign services, including Key Opinion Leader (KOL) marketing, short-film drama marketing, affiliate commerce, and campaign management services. Its subsidiaries, incorporated in Malaysia and Singapore, carry out these principal activities.

IPO Details

Strategic Overview & Data Visuals

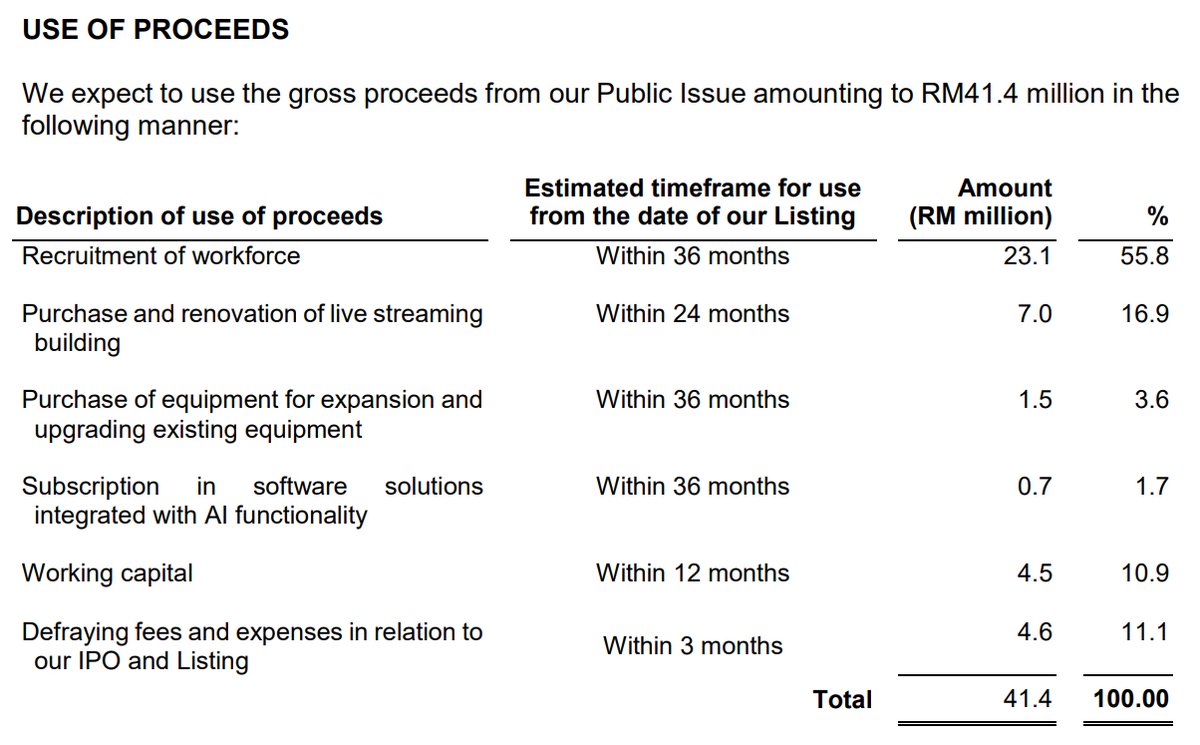

Utilisation of Proceeds

| Purpose | Amount (RM'000) | % | |

|---|---|---|---|

| Expansion | Recruitment of workforce | 23,100 | 55.8 |

| Expansion | Purchase and renovation of live streaming building | 7,000 | 16.9 |

| Expansion | Purchase of equipment for expansion and upgrading existing equipment | 1,500 | 3.6 |

| Expansion | Subscription in software solutions integrated with AI functionality | 700 | 1.7 |

| Working capital | Working capital | 4,500 | 10.9 |

| Listing expenses | Defraying fees and expenses in relation to our IPO and Listing | 4,600 | 11.1 |

| Total | 41,400 | 100 | |

Analyst Highlights

| Date | Analyst Highlights |

|---|---|

|

19-Nov-2025

RHB |

|

|

18-Nov-2025

Kenanga |

|

|

18-Nov-2025

Mplus |

|

|

18-Nov-2025

TA |

|

|

18-Nov-2025

TradeView |

|

Utilisation of Proceeds

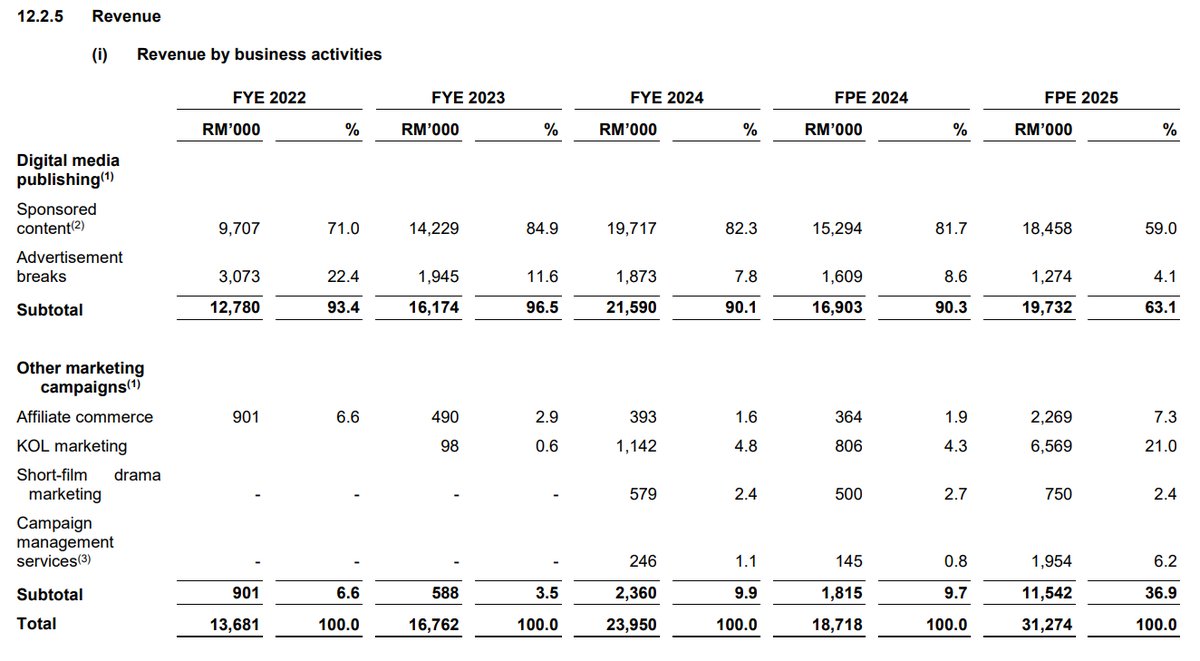

Business Segments

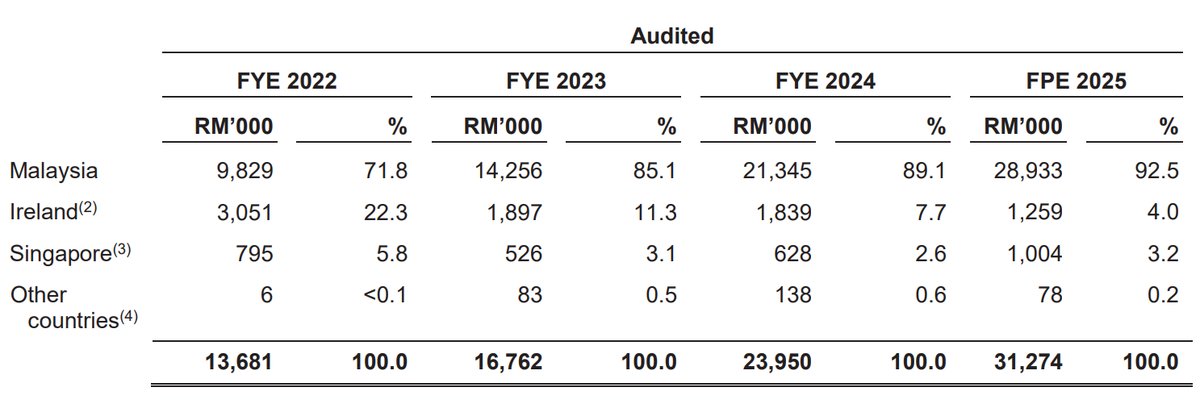

Geographical Segments

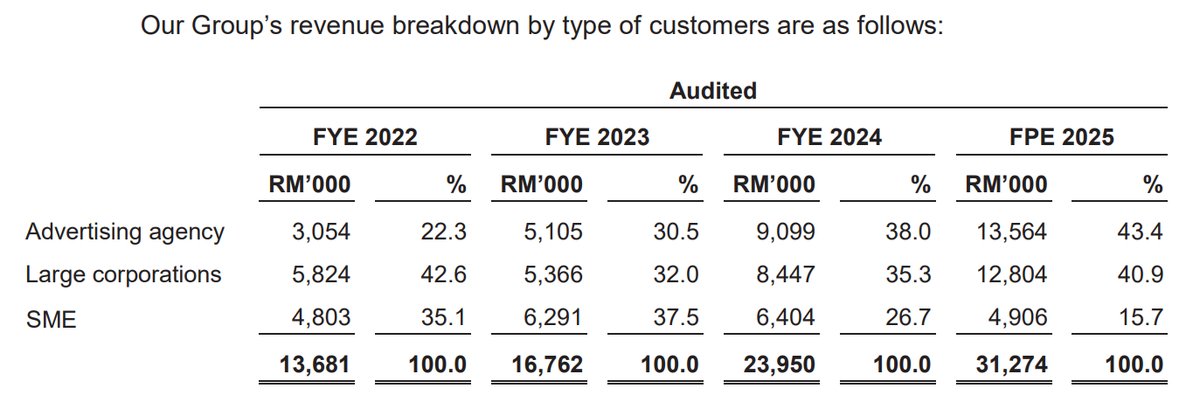

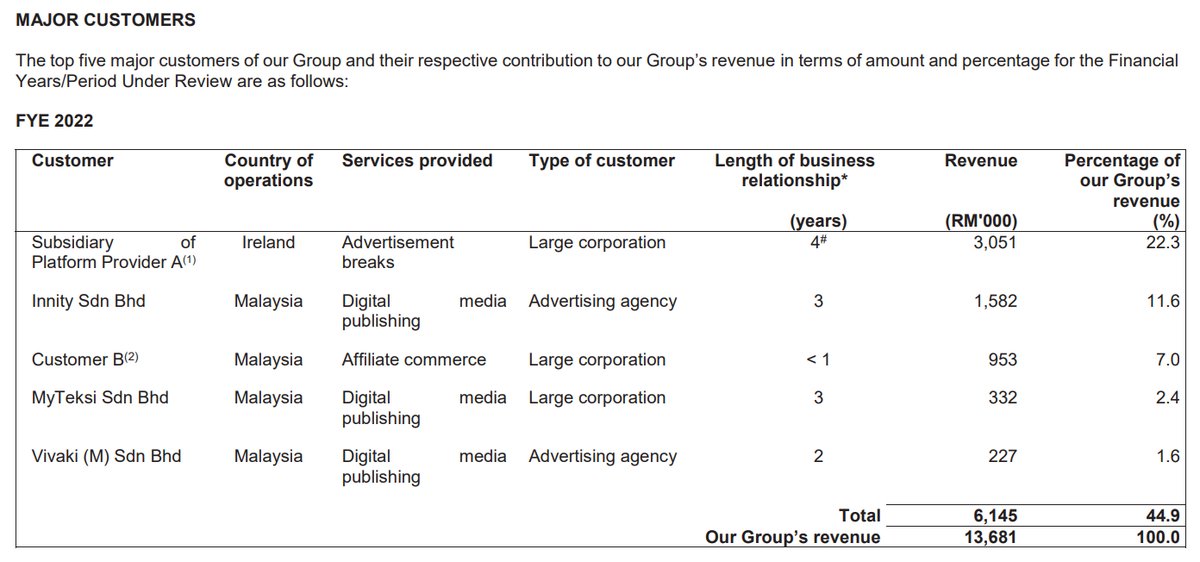

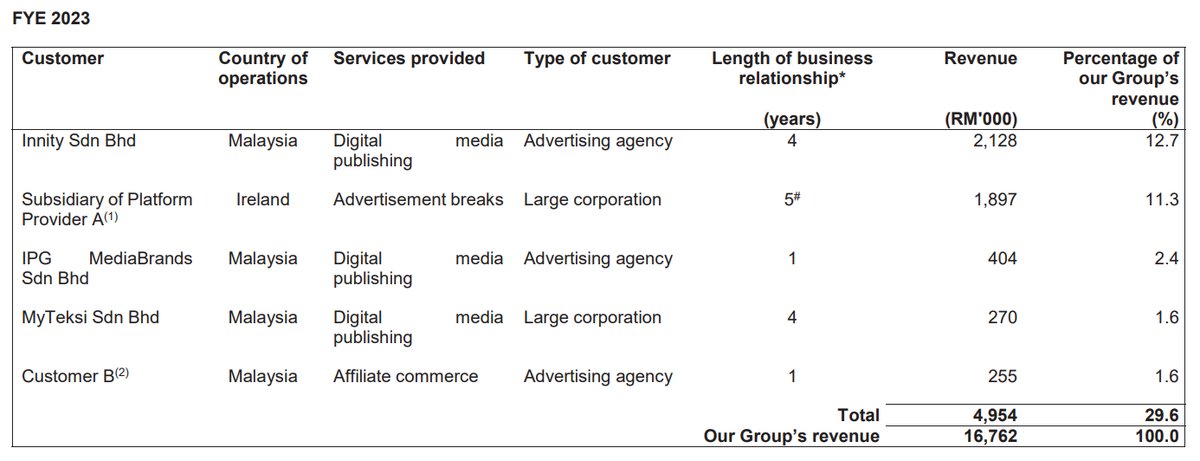

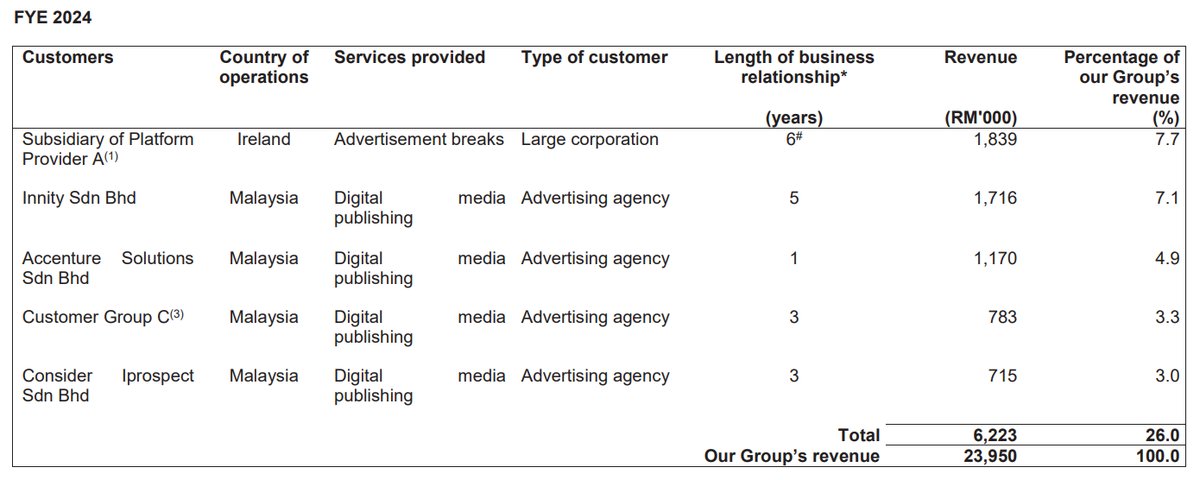

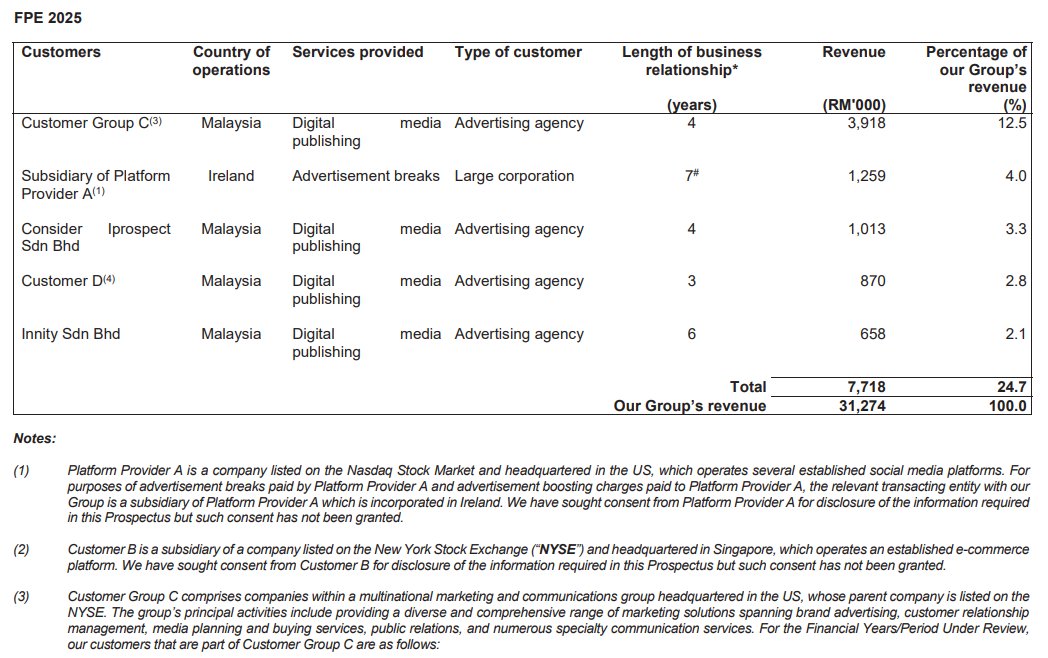

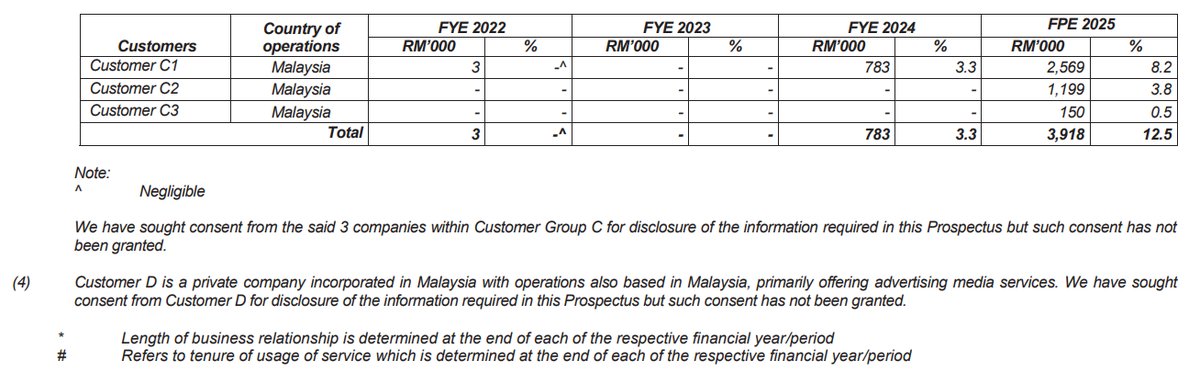

Major Customers

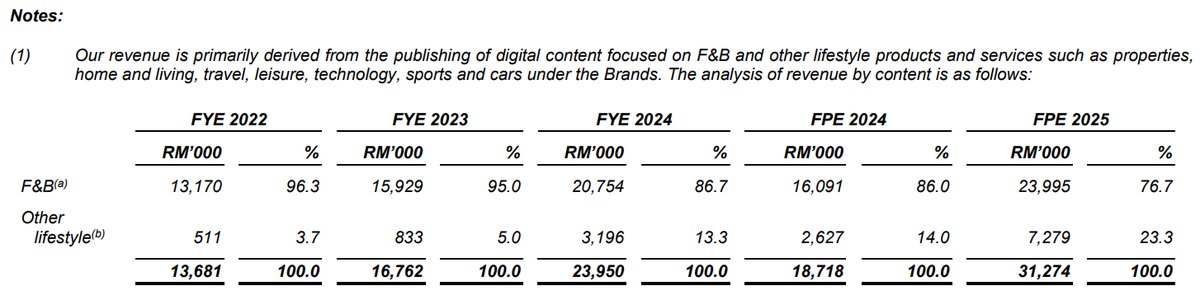

Revenue by Financial Year Ended

Profit After Tax (PAT) by Financial Year Ended

Revenue by Financial Period Ended

SWOT Analysis

Strengths

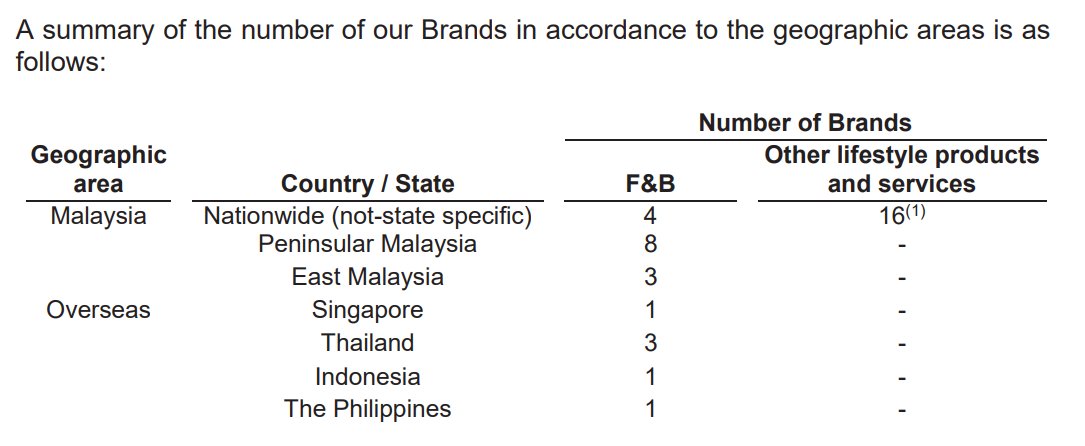

- Established Brand Portfolio: The company has developed a portfolio of 37 brands with a large combined follower base of approximately 46.0 million, making it the largest for lifestyle-focused digital content in Malaysia. This provides access to a wide audience for monetization.

- Well-Positioned in a Growing Industry: The company is well-positioned to capitalize on the rapidly growing digital media advertising industry in Malaysia, which saw a CAGR of 8.7% from 2019 to 2024. Its Malaysia Digital Status provides access to a network of local and international companies.

- Award-Winning Brands: Several of its brands, including Pinn Yang, Foodie, and KL Foodie, have received industry awards such as the Silver Creator Award from YouTube and Top Outstanding Social Media Gourmet Content Creator, which enhances brand credibility and attractiveness to clients.

- Diverse and Customizable Service Range: The company offers a wide range of services, including digital media publishing, KOL marketing, and affiliate commerce, which can be customized to meet the needs of various business sizes, from SMEs to large corporations, providing a strong value proposition.

Weaknesses

- Dependency on Third-Party Platforms: The business is highly dependent on third-party social media platforms, particularly Platform Provider A, where approximately 68.6% of its followers are located. Any changes to algorithms, monetization policies, or a platform ban could adversely affect business performance.

- No Long-Term Contracts: The company does not have long-term contracts with its customers, making its financial performance dependent on its ability to consistently secure new short-term projects. This exposes the business to revenue volatility.

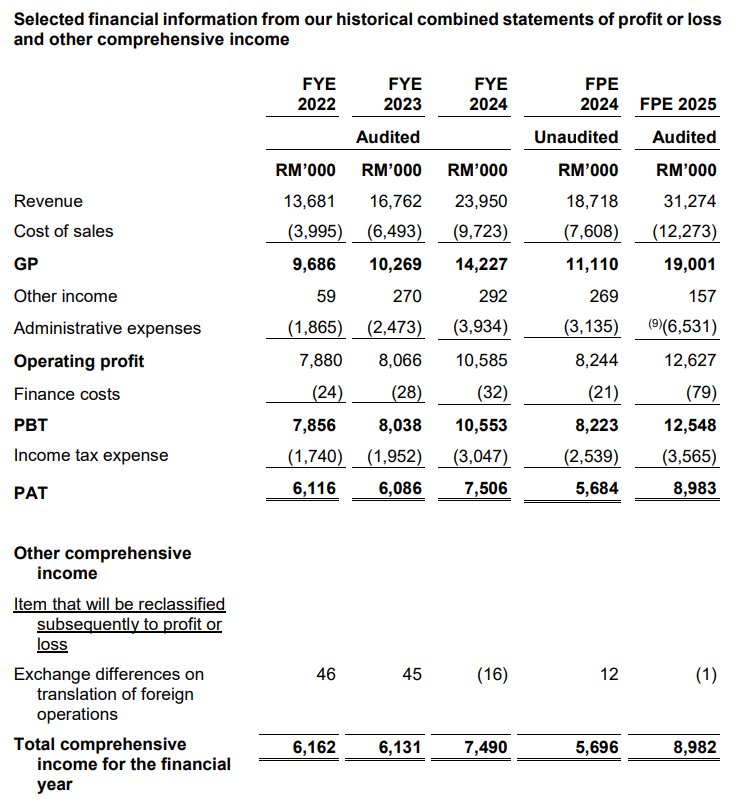

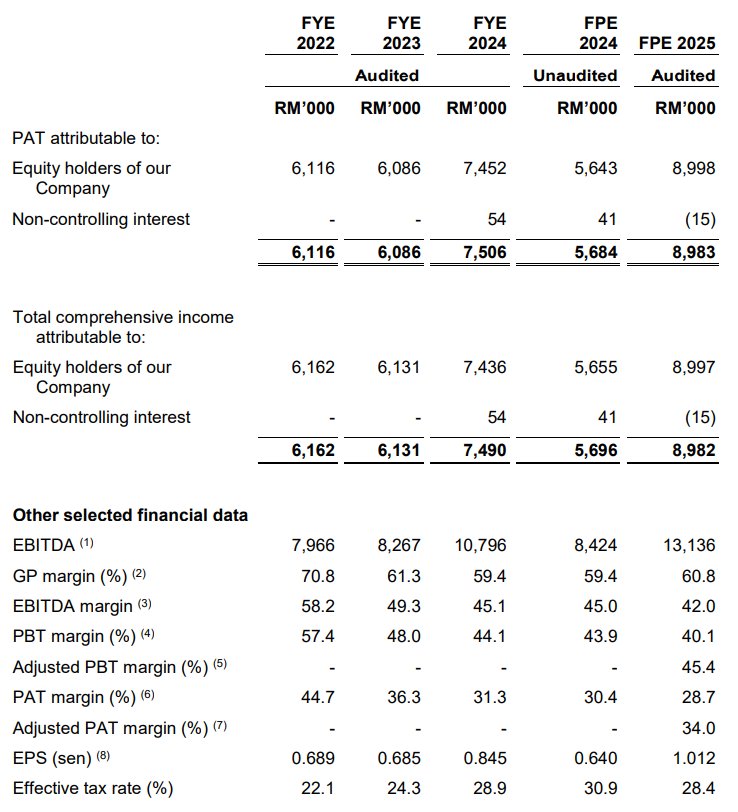

- Declining Profit Margins: While revenue has been growing, both Profit Before Tax (PBT) margin and Profit After Tax (PAT) margin have shown a declining trend from FYE 2022 to FPE 2025, indicating rising costs relative to revenue.

Opportunities

- Growth in Live Commerce: The company plans to grow its revenue from the live commerce selling segment, which is a rapidly growing market in Southeast Asia (92.5% CAGR from 2019-2024). Plans include acquiring new premises for up to 30 live streaming rooms and expanding the live commerce team.

- Expansion of Service Segments: The company intends to produce its own short-film dramas, a growing trend in digital advertising. This move could provide a new revenue stream and higher gross profit margins compared to engaging third-party producers.

- Workforce and Technology Expansion: A significant portion of the IPO proceeds (55.8%) is allocated for workforce expansion across content production, KOL management, and other areas. The company also plans to invest in software solutions with AI-integrated functionalities to enhance operational efficiency.

- Development of New Brands: The company plans to develop up to 5 new brands focusing on beauty, health, wellness, and luxury goods. This diversification can attract new audience segments and revenue streams.

Threats

- Intense Industry Competition: The digital media advertising industry is highly competitive with a low barrier to entry. The company faces competition from other industry players, and new competitors with more financial resources could emerge, potentially leading to price wars.

- Regulatory Risks: The business is subject to regulatory changes, such as the requirement for social media platforms to obtain an ASP(C) License in Malaysia. Failure by these platforms to comply could disrupt the company's primary channels for content distribution.

- Cybersecurity Breaches: The business is exposed to cybersecurity risks, including hacking and social media account impersonation. A successful breach could lead to loss of control over its social media pages, reputational harm, and potential lawsuits.

- Negative Publicity: The company's brands are critical to its success. Any negative publicity, public criticism, or viral negative content, regardless of authenticity, could damage the brands' reputation, leading to a decline in follower growth and audience confidence.

Key Highlights

Sorry, this feature only available for iSaham Pro

Conclusion

Sorry, this feature only available for iSaham Pro

Foodie Media Berhad's Latest News