Sunway Healthcare Holdings Berhad IPO's Analysis

Sunway Healthcare Holdings Berhad

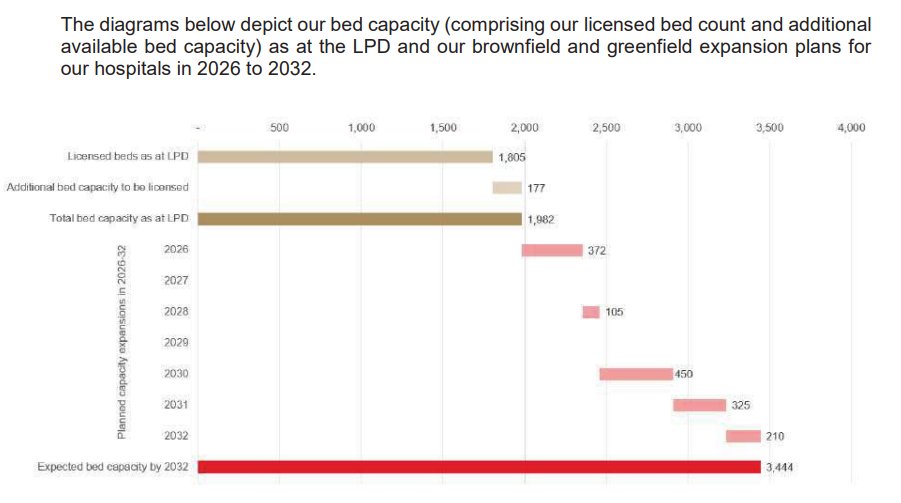

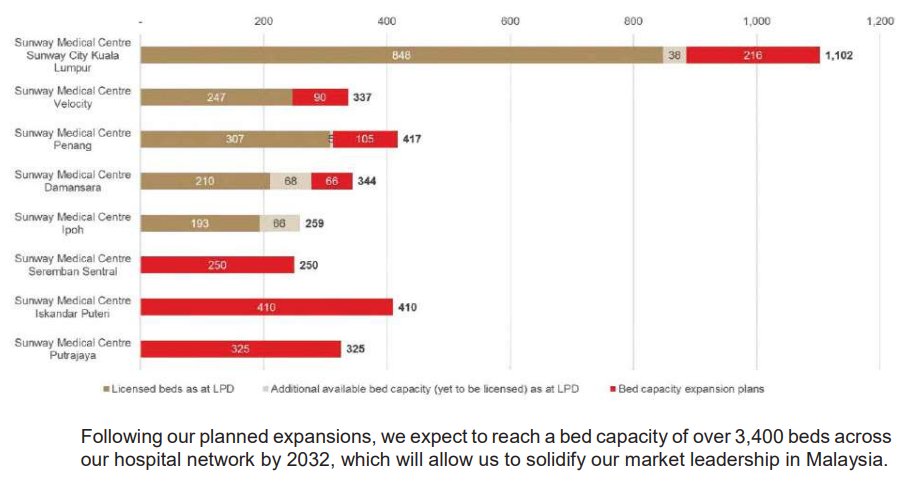

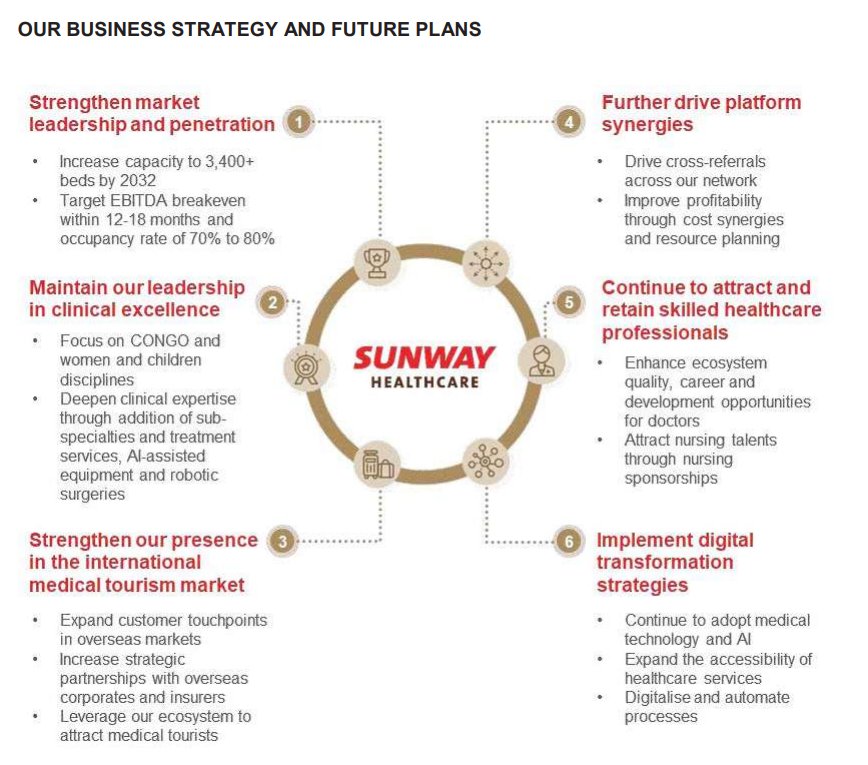

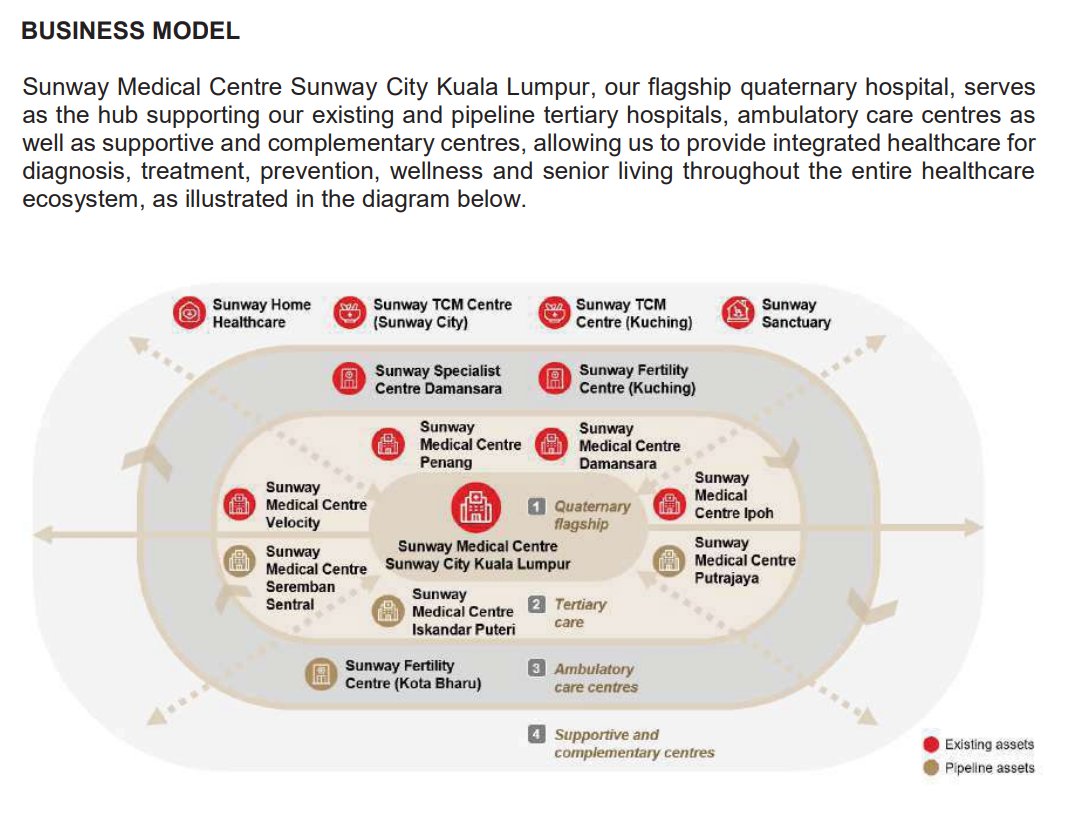

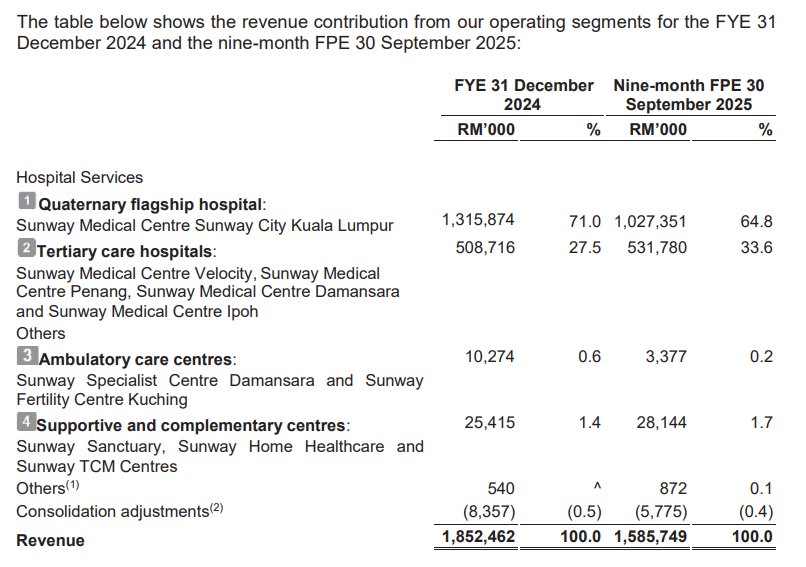

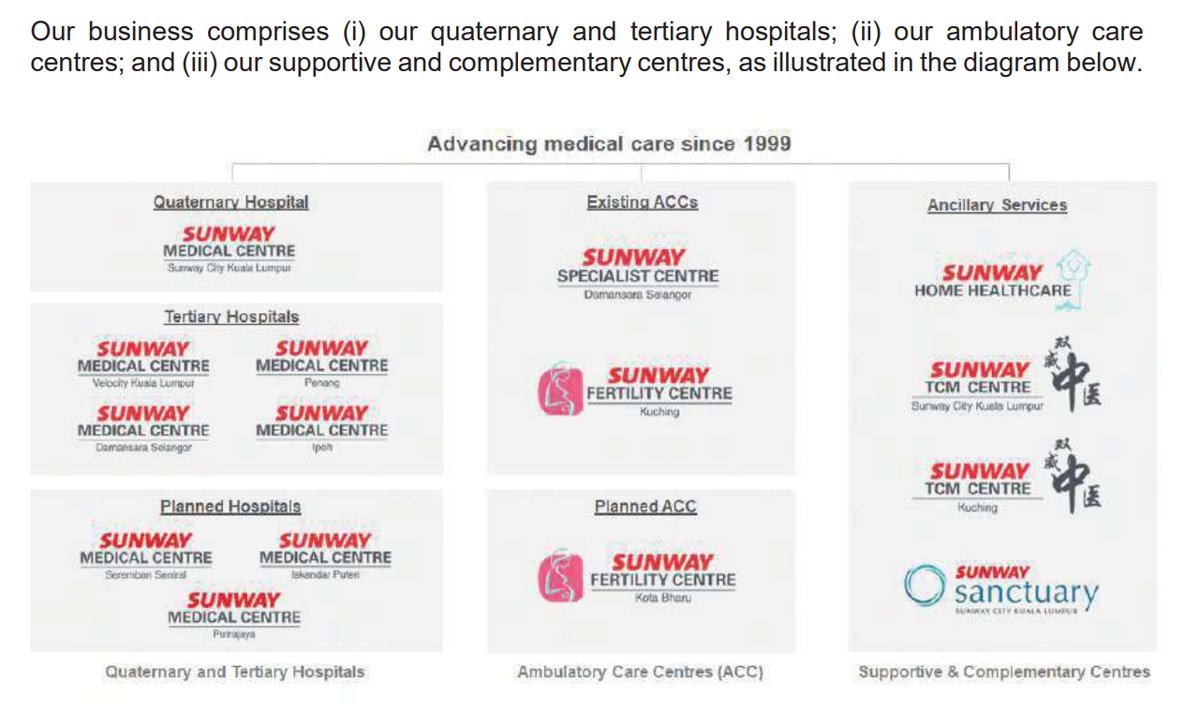

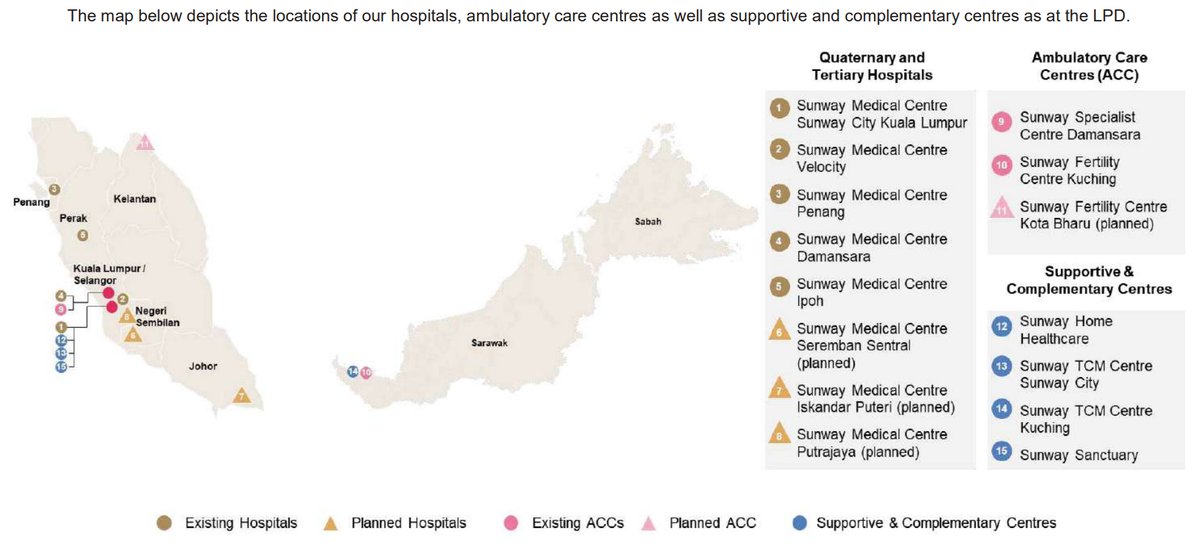

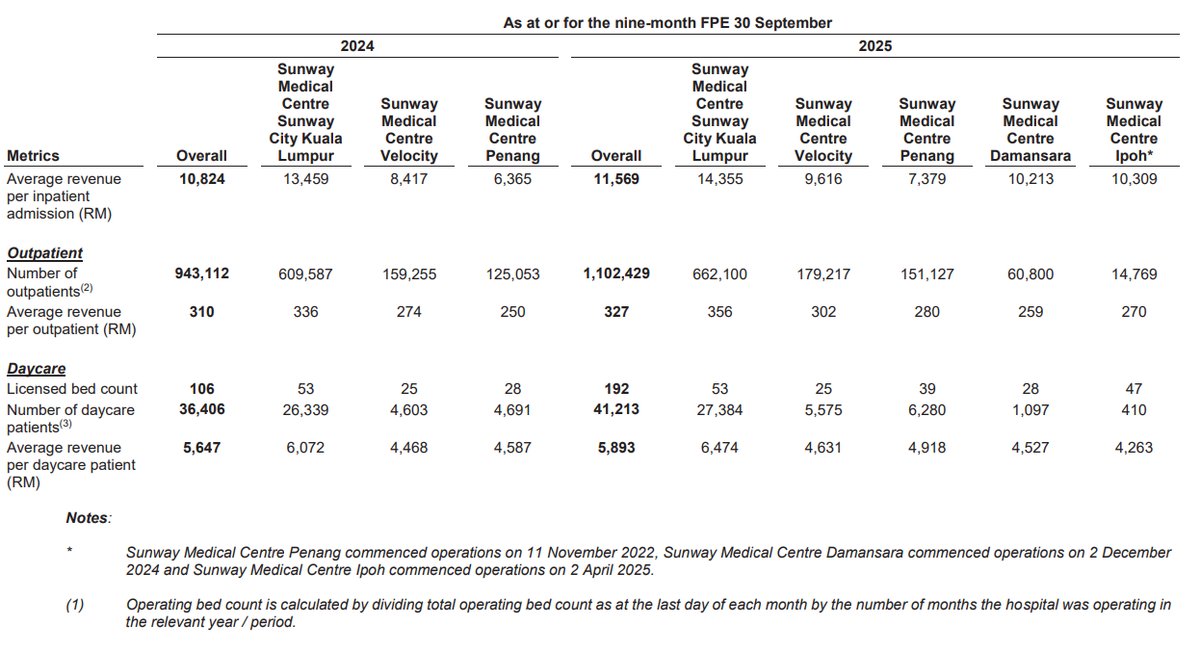

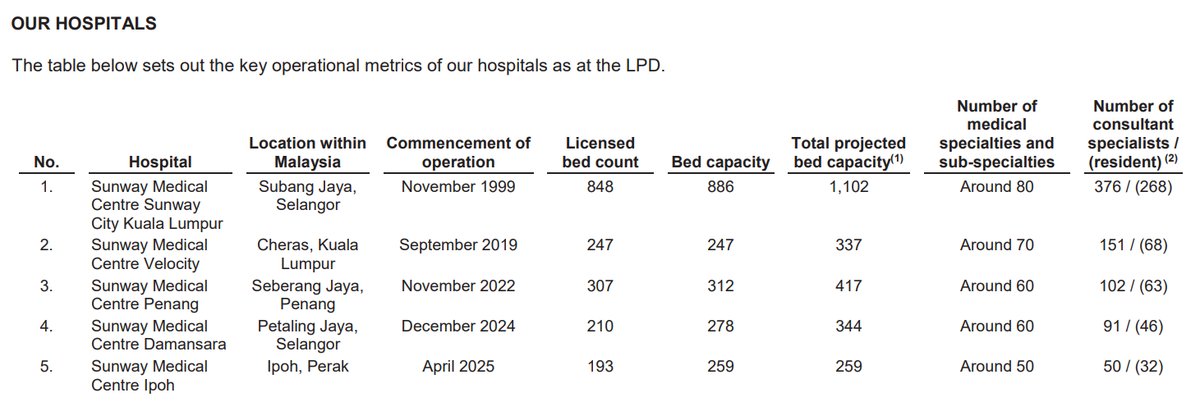

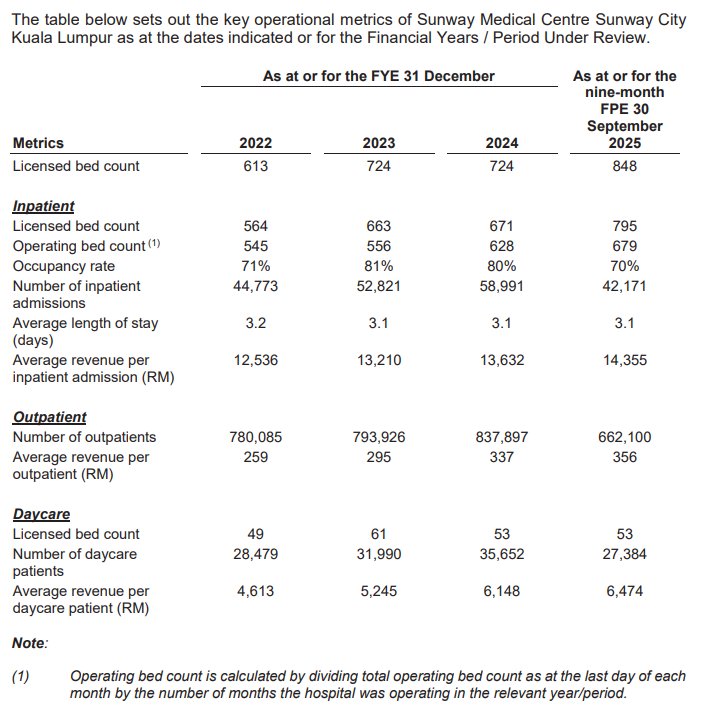

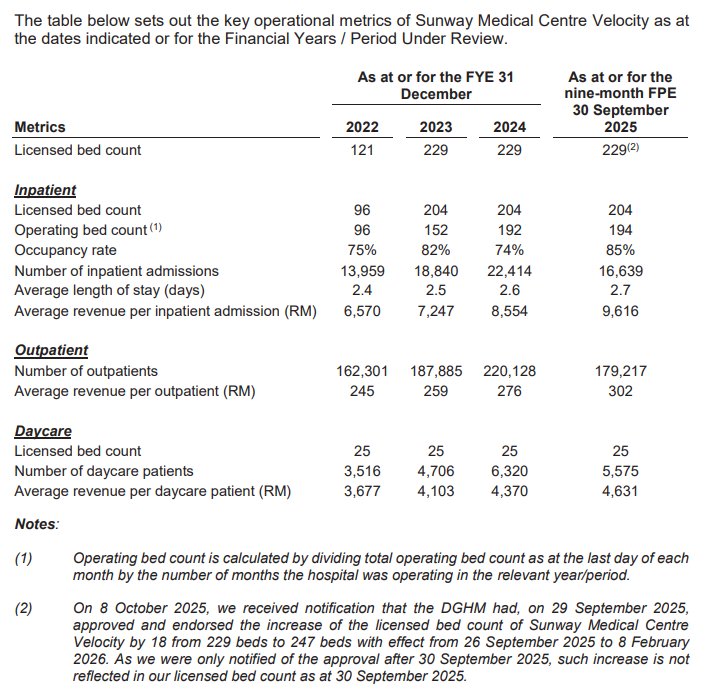

Sunway Healthcare Holdings Berhad (SHH) is one of Malaysia's largest private hospital groups, providing a full lifecycle of care. Its flagship, Sunway Medical Centre Sunway City Kuala Lumpur, is a quaternary hospital and one of the largest in Southeast Asia. The network also includes four tertiary hospitals in key urban areas. Beyond hospital operations, SHH operates ancillary healthcare businesses, including ambulatory care centres (Sunway Specialist Centre and Sunway Fertility Centre), and supportive care facilities like Sunway TCM Centres, Sunway Home Healthcare, and the Sunway Sanctuary integrated senior living facility. The company is focused on expanding its footprint in Malaysia through both brownfield expansions of existing hospitals and greenfield development of new tertiary hospitals in underserved regions.

IPO Details

- Healthcare (23.2)

- Health Care Providers (37.5)

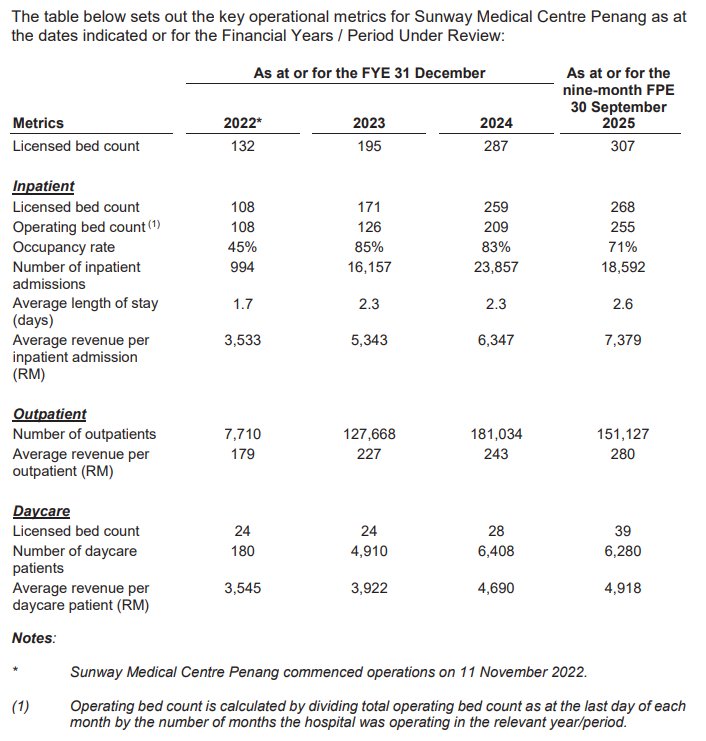

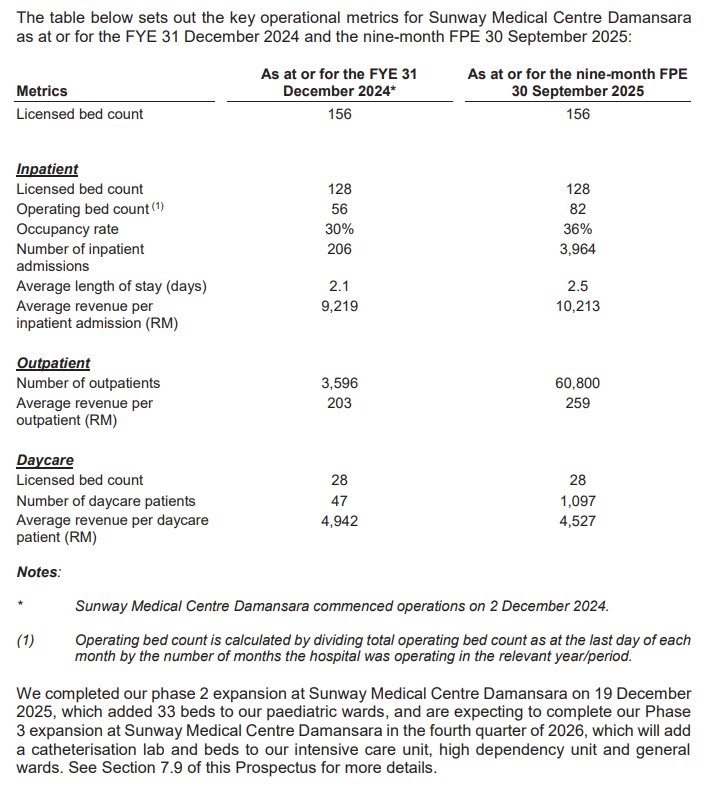

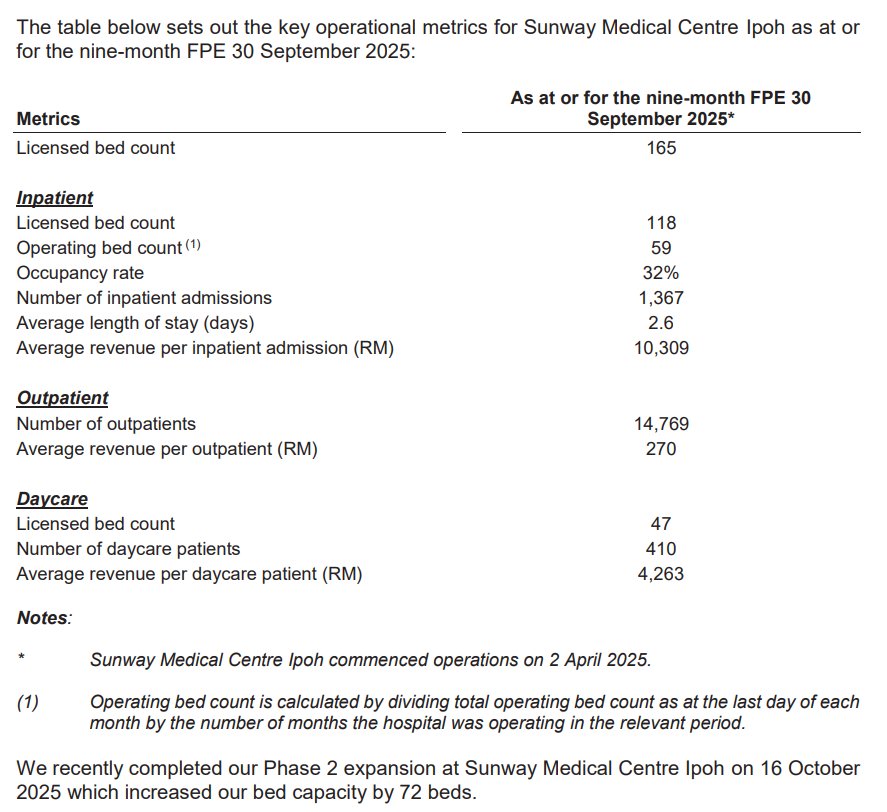

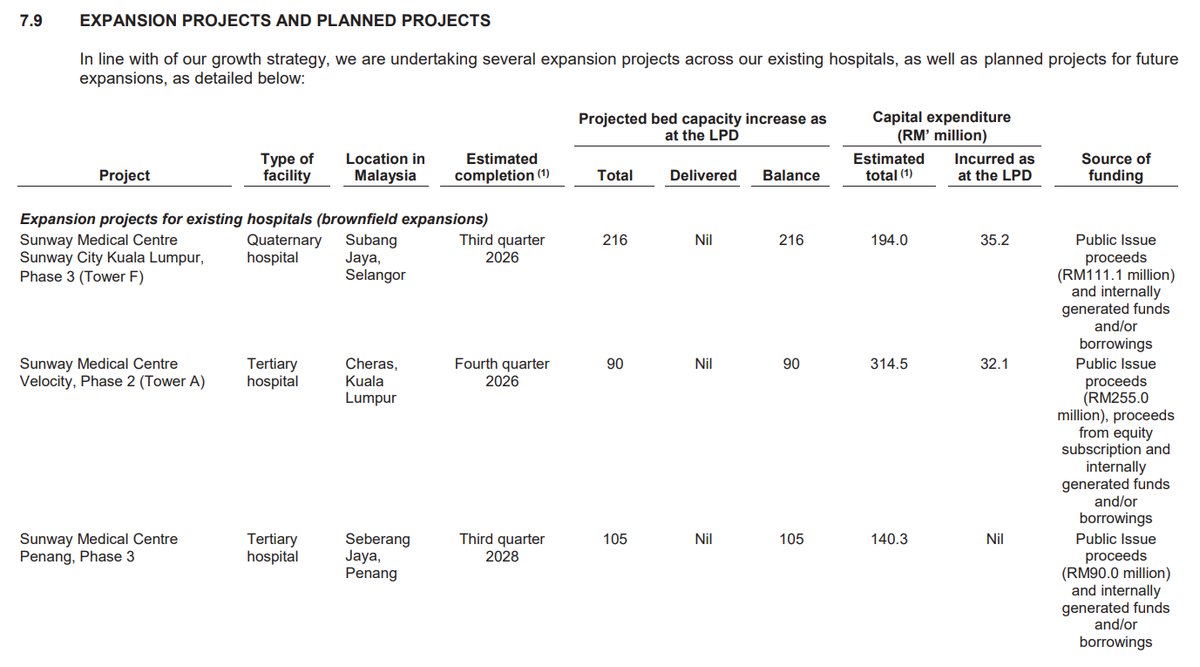

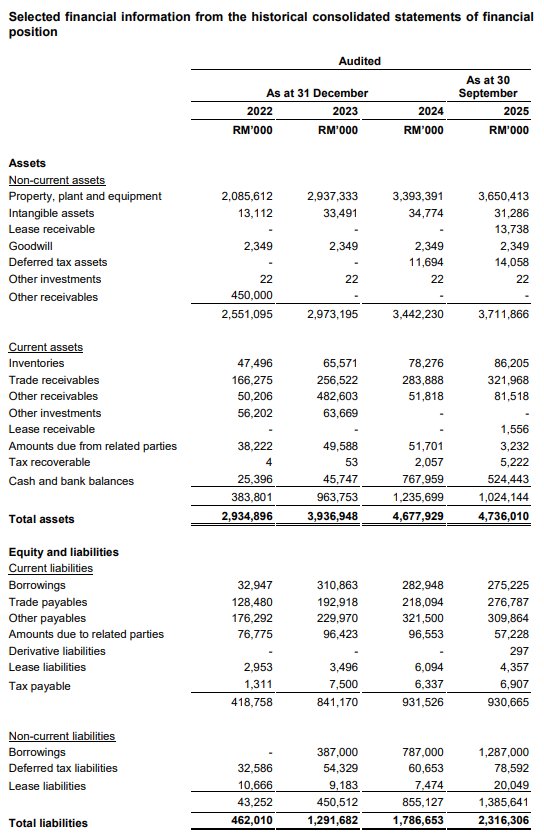

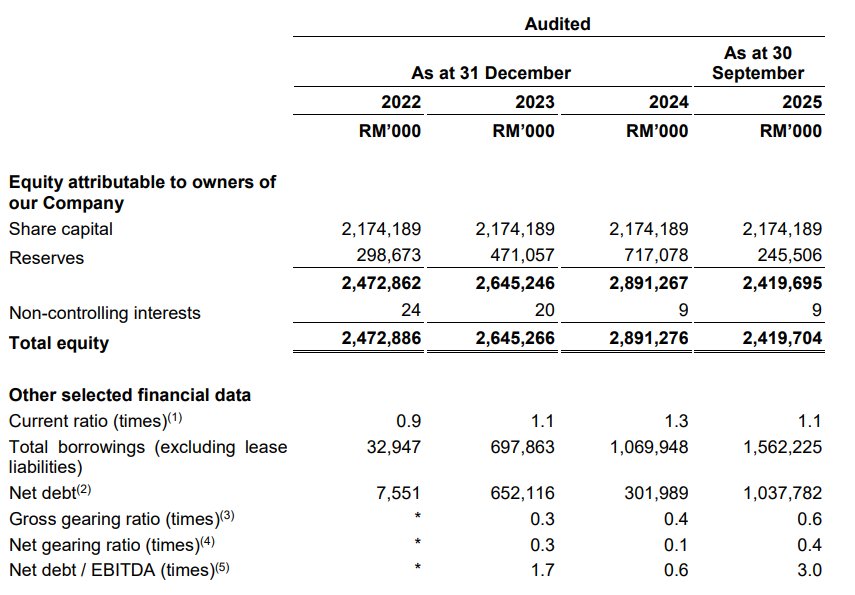

Strategic Overview & Data Visuals

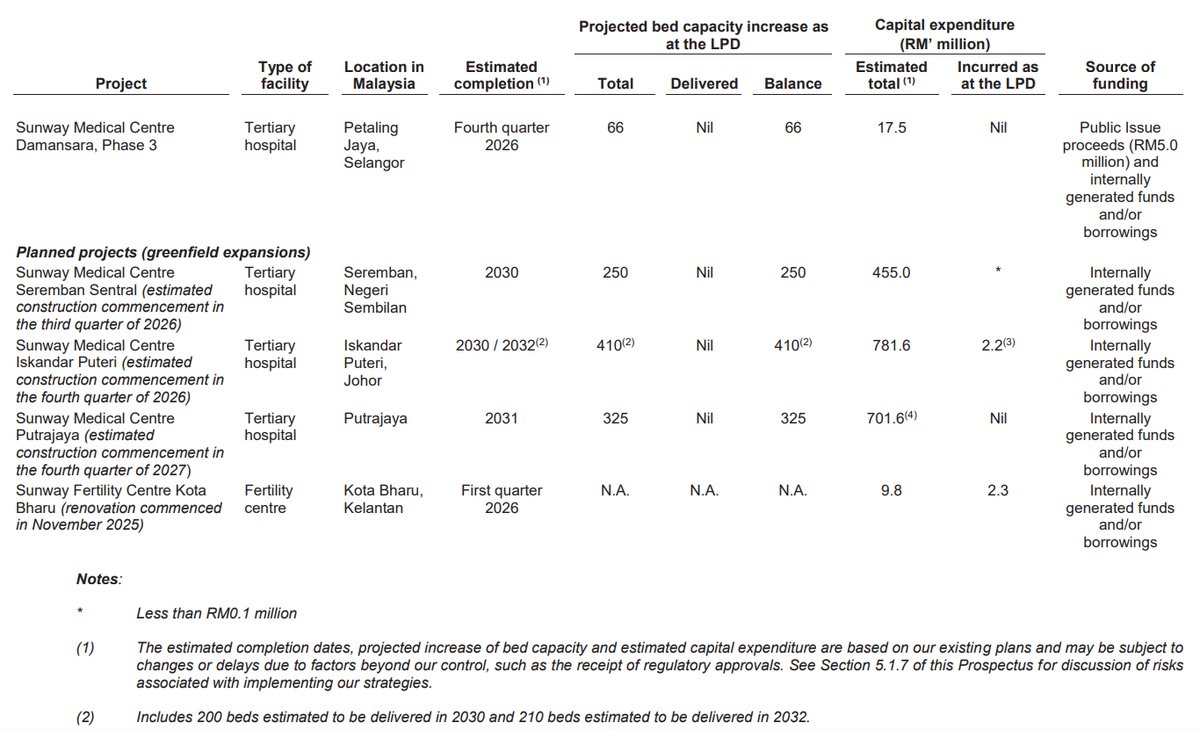

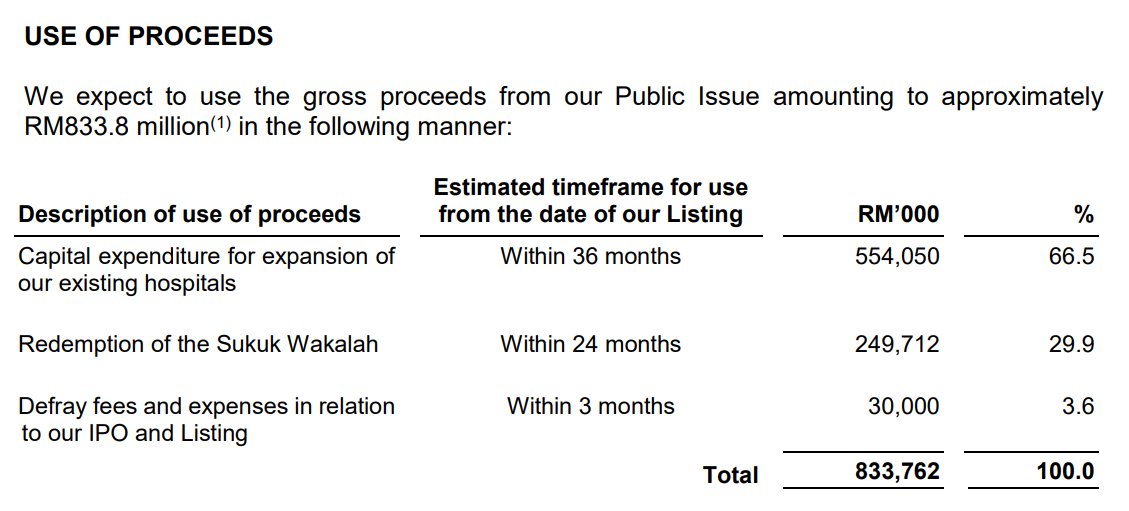

Utilisation of Proceeds

| Purpose | Amount (RM'000) | % | |

|---|---|---|---|

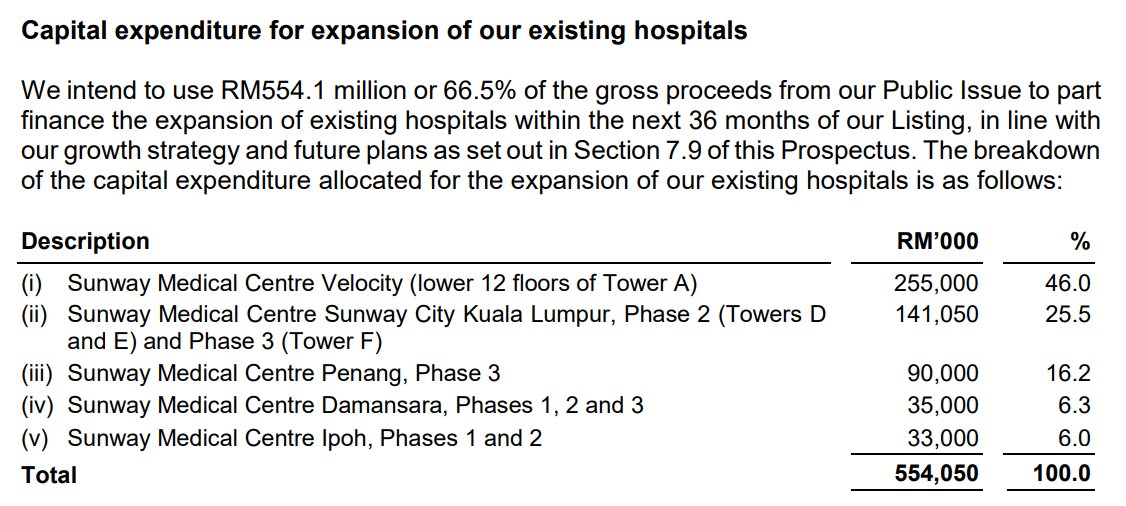

| Expansion | Capital expenditure for expansion of our existing hospitals | 554,050 | 66.5 |

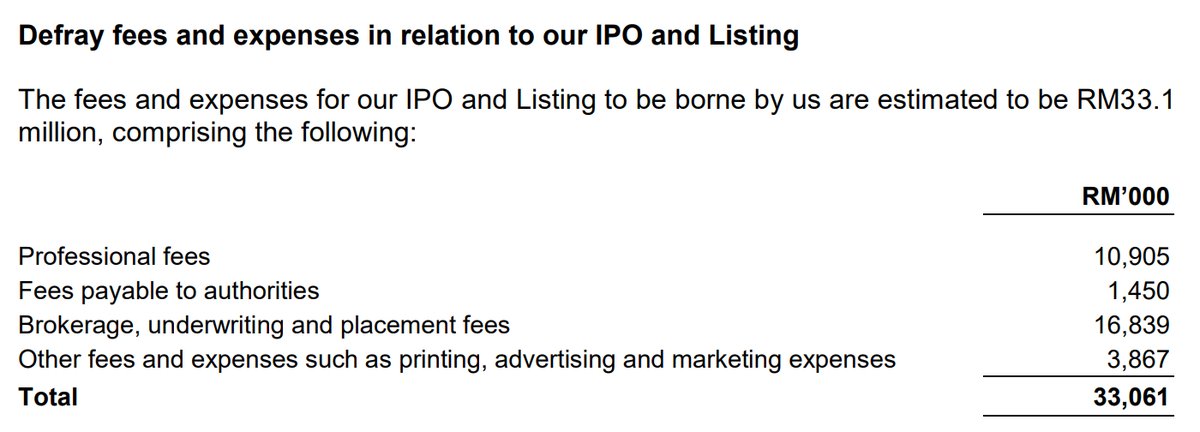

| Listing expenses | Defray fees and expenses in relation to our IPO and Listing | 30,000 | 3.6 |

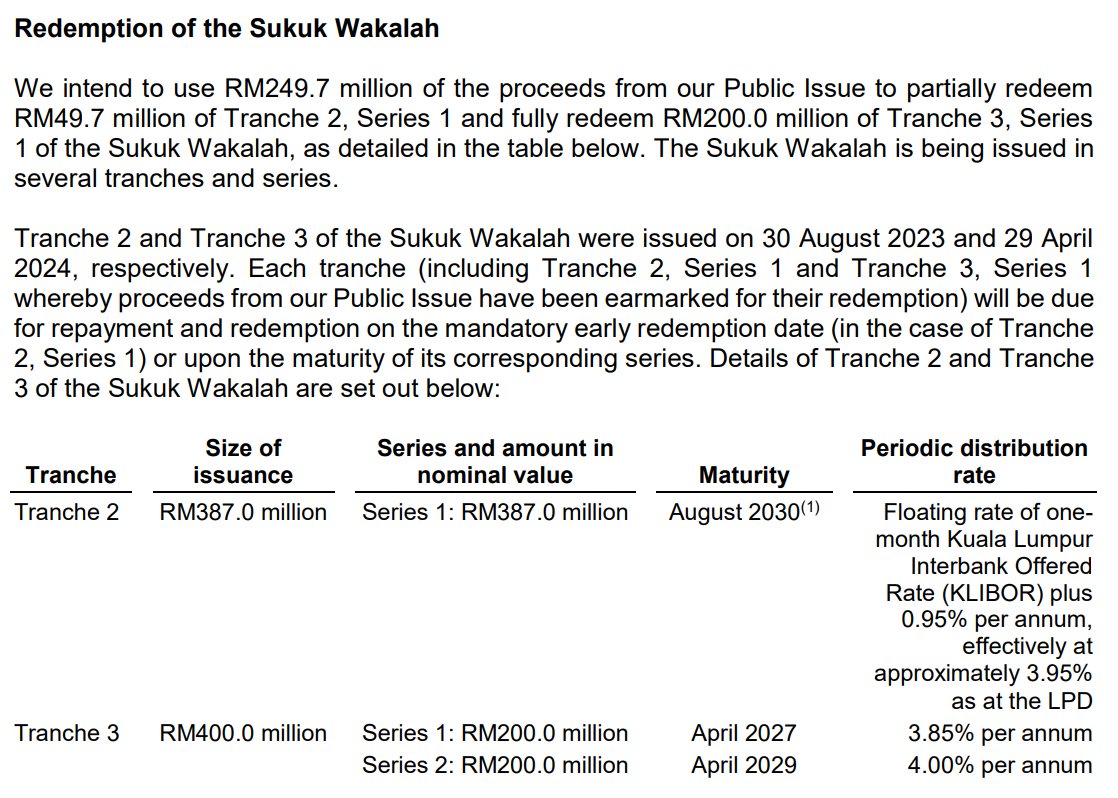

| Debt | Redemption of the Sukuk Wakalah | 249,712 | 29.9 |

| Total | 833,762 | 100 | |

Analyst Highlights

| Date | Analyst Highlights |

|---|---|

|

05-Mar-2026

TradeView |

|

|

05-Mar-2026

Mplus |

|

|

04-Mar-2026

TA |

|

|

04-Mar-2026

Public Invest |

|

Utilisation of Proceeds

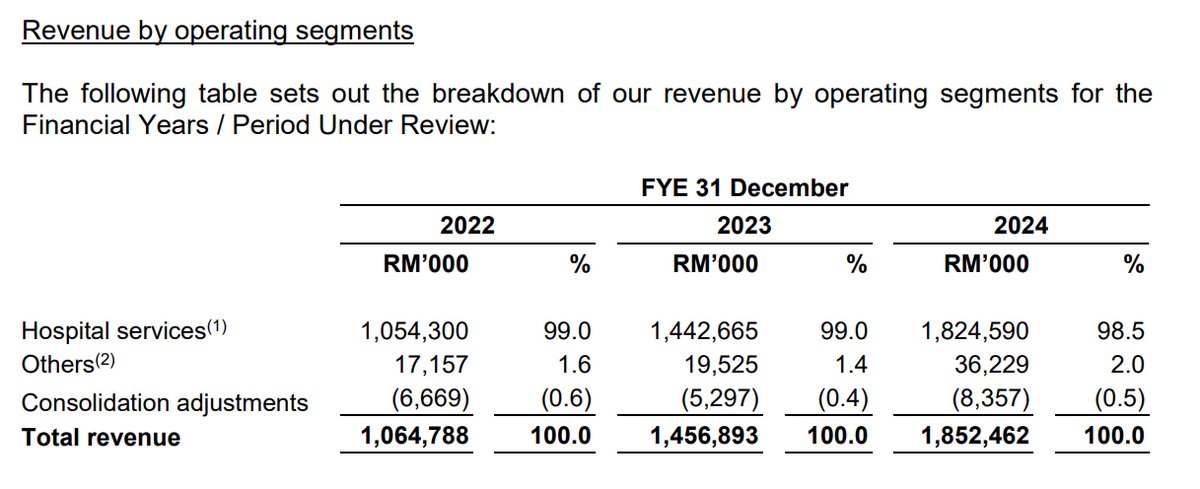

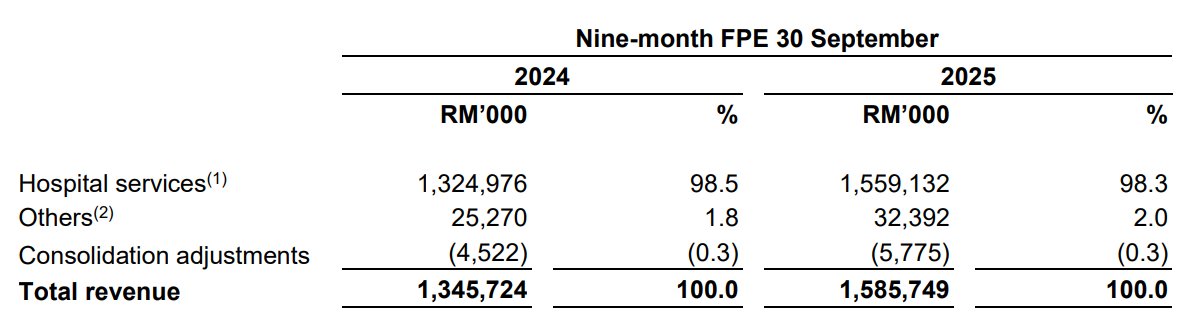

Business Segments

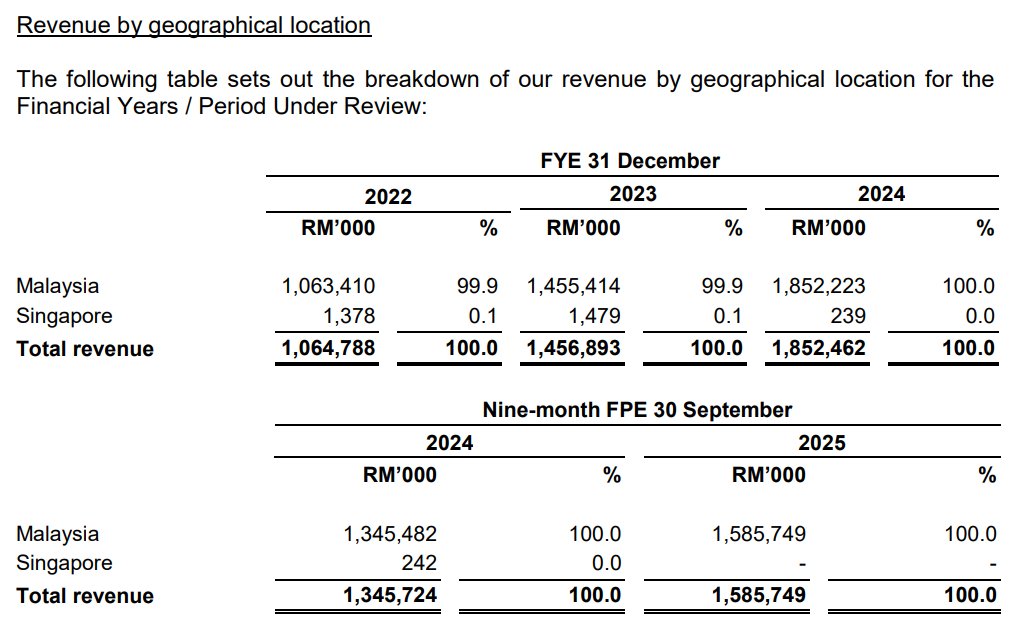

Geographical Segments

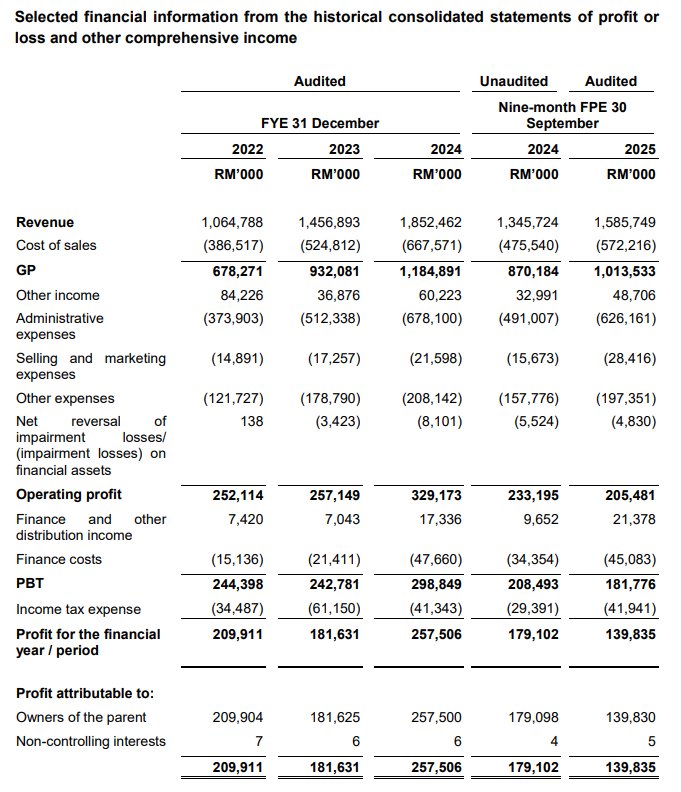

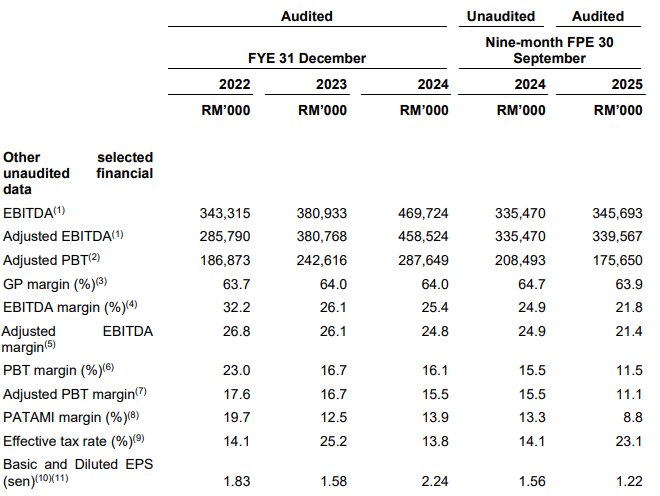

Revenue by Financial Year Ended

Profit After Tax (PAT) by Financial Year Ended

Revenue by Financial Period Ended

Profit After Tax (PAT) by Financial Period Ended

SWOT Analysis

Strengths

- Integrated Township Ecosystem: Hospitals are embedded within Sunway's townships, creating a captive market and synergies for medical tourism with co-located hotels and retail, a unique advantage over standalone competitors.

- High Revenue Intensity: Focus on high-complexity Quaternary and Tertiary care results in higher revenue per patient and stronger margins compared to general hospital peers.

- Strong Institutional Backing: Backed by GIC, Singapore’s Sovereign Wealth Fund, which validates the company's quality and provides financial credibility for future growth and potential regional expansion.

Weaknesses

- Extreme Valuation Premium: Listing at a Hybrid PE ratio of 76.41x, a premium of over 100% compared to established peers like IHH Healthcare (~34.5x) and KPJ Healthcare (~35.5x), leaving little room for error.

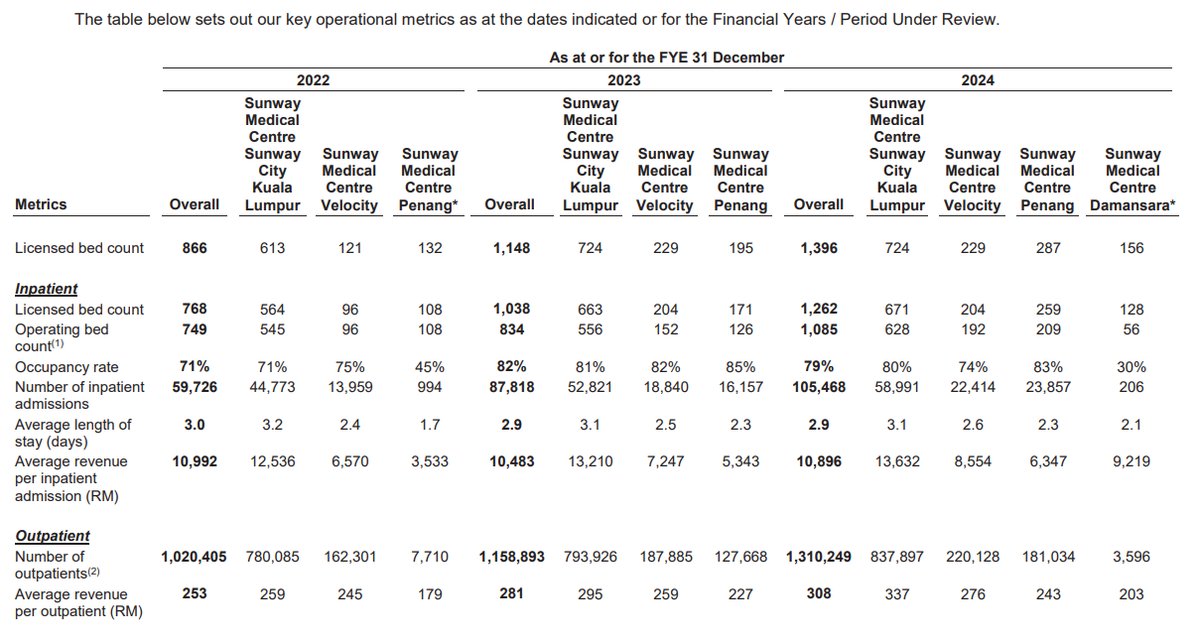

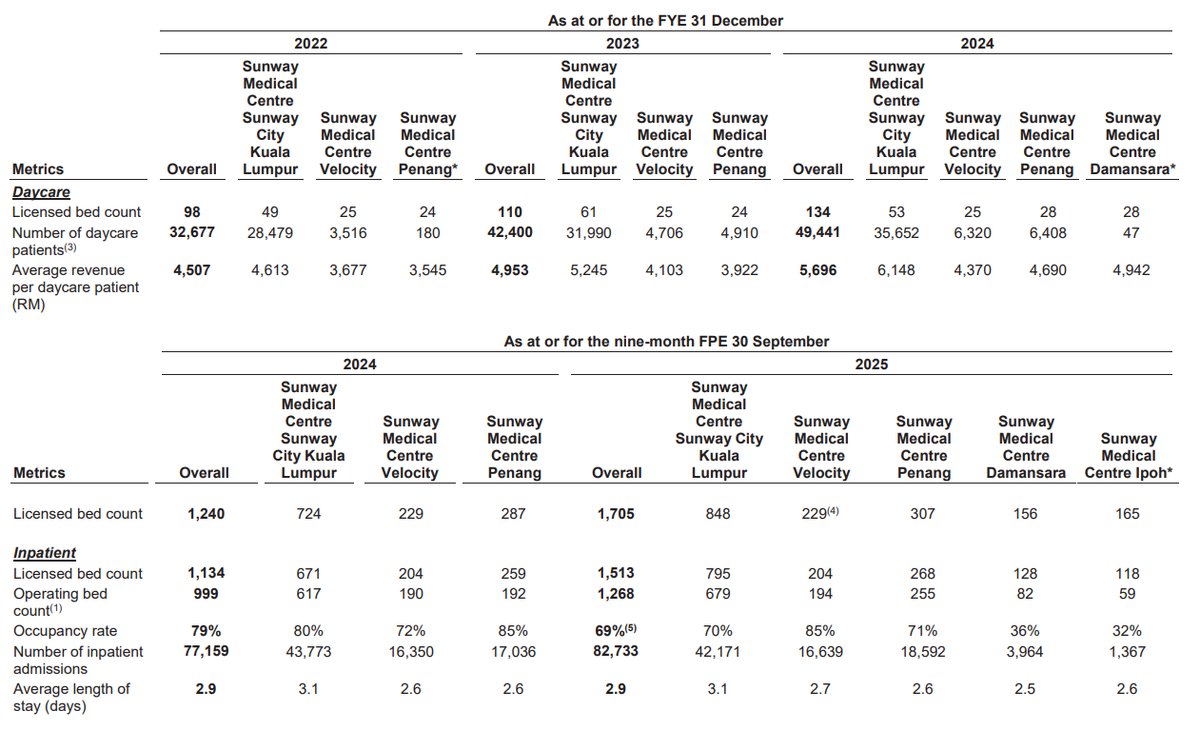

- Flagship Hospital Dependency: The Sunway City Kuala Lumpur hospital contributes approximately 64.8% of group revenue, posing a significant concentration risk to earnings if its operations are disrupted.

- Short-Term Earnings Drag: Aggressive expansion and gestation costs from new hospitals have caused a 21.9% drop in recent profits, suppressing short-term returns and making the high valuation appear even more stretched.

Opportunities

- Medical Tourism Growth: Positioned to capture the recovery in medical tourism, leveraging Malaysia's cost-competitiveness and quality of care to attract patients from Indonesia and Singapore.

- Ageing Demographics: Malaysia's shift towards an aged nation status will drive intrinsic demand for specialised healthcare services like geriatric care and chronic disease management, which SHH is equipped to provide.

- Cross-Border Market Tapping: The upcoming hospital in Iskandar Puteri, Johor, provides a strategic entry point to tap into the Singaporean patient market, capitalizing on significant cost arbitrage.

Threats

- Healthcare Talent Shortage: An acute shortage of nurses and specialist doctors in Malaysia could drive up staff costs and constrain the operational capacity and ramp-up speed of new hospitals.

- Increased Competition: Regulatory changes effective September 2024 lower the barriers to entry for new private hospitals, which could intensify competition from new market players in the long term.

- Insurance and Cost Pressures: Rising medical inflation may lead insurance providers to tighten claim policies or increase premiums, potentially impacting patient volumes and revenue streams.

Key Highlights

Sorry, this feature only available for iSaham Pro

Conclusion

Sorry, this feature only available for iSaham Pro

Sunway Healthcare Holdings Berhad's Latest News