PSP Energy Berhad IPO's Analysis

PSP Energy Berhad

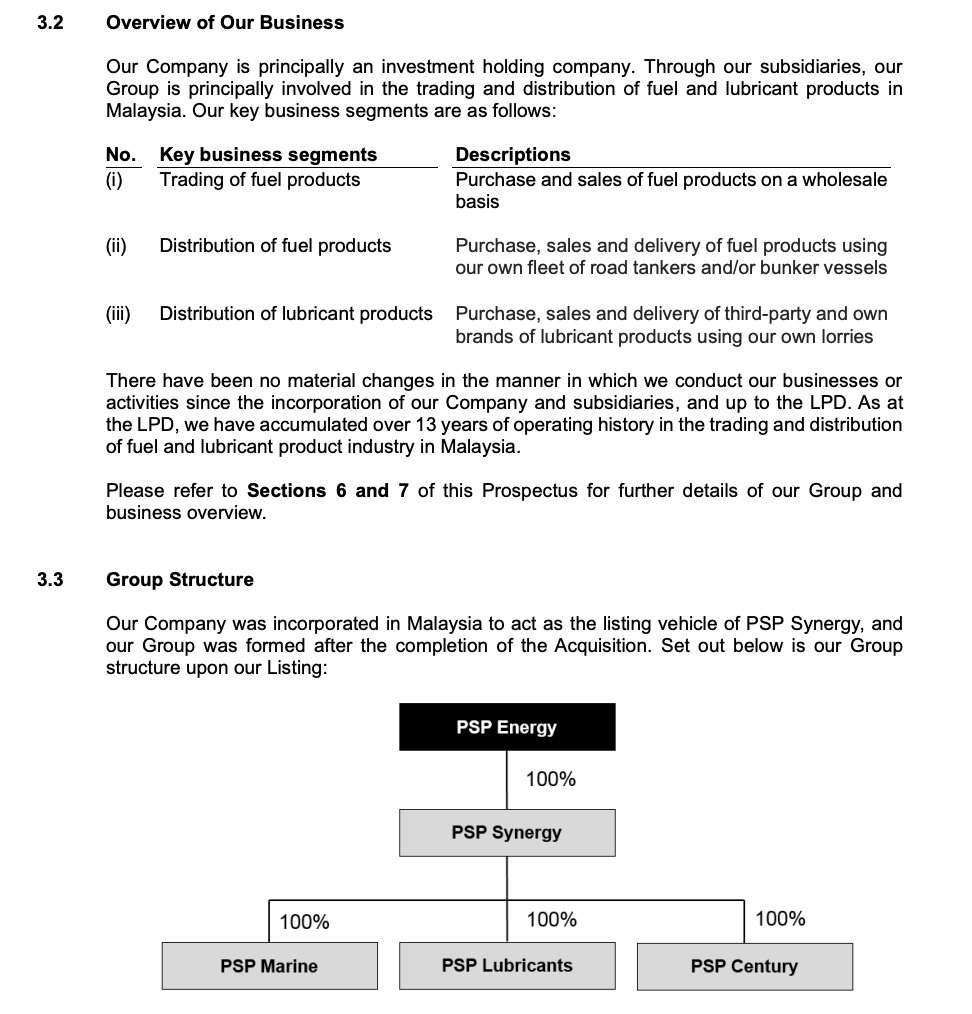

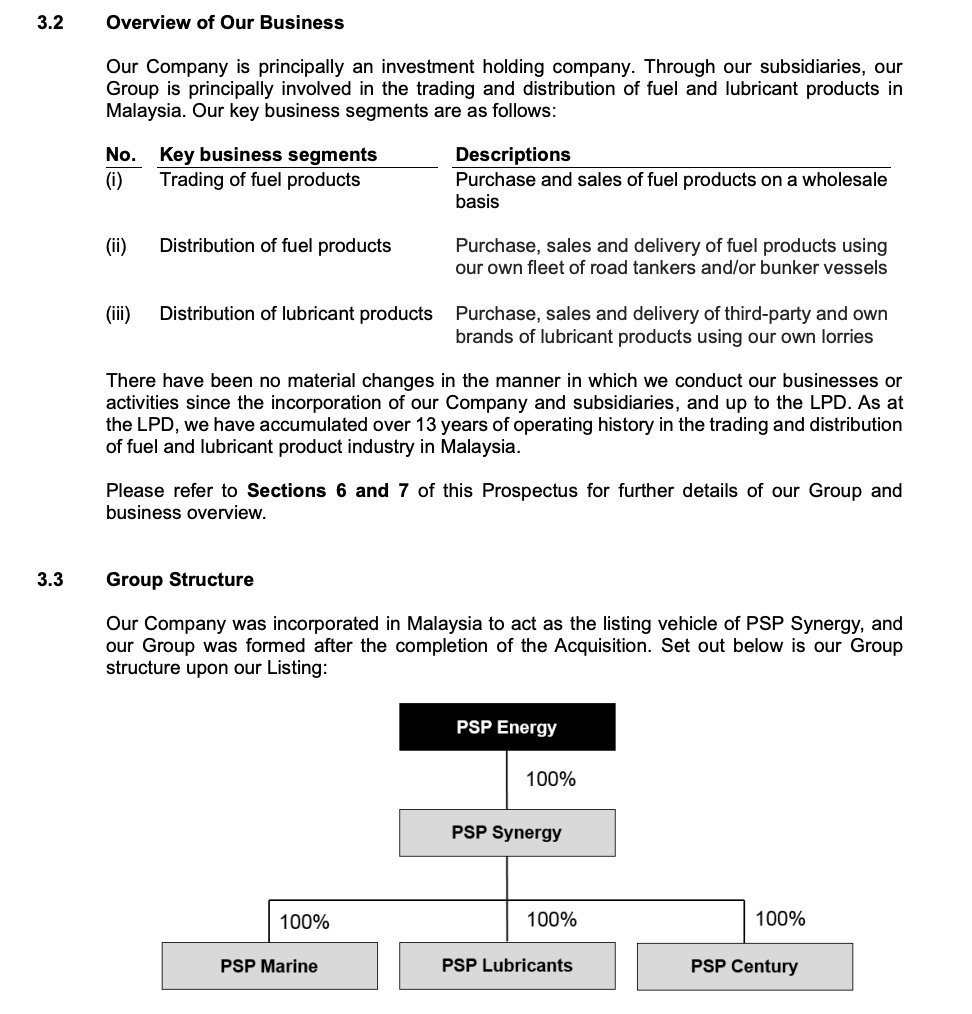

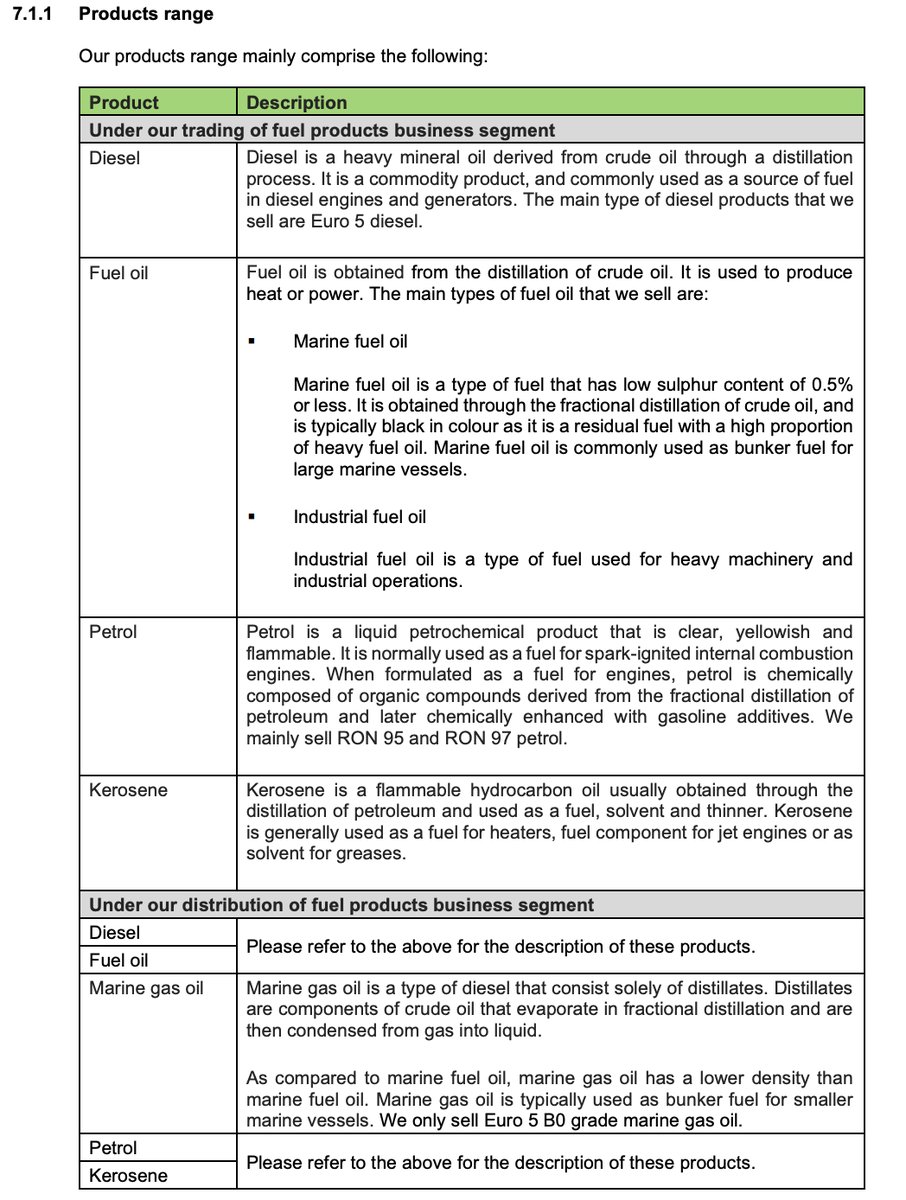

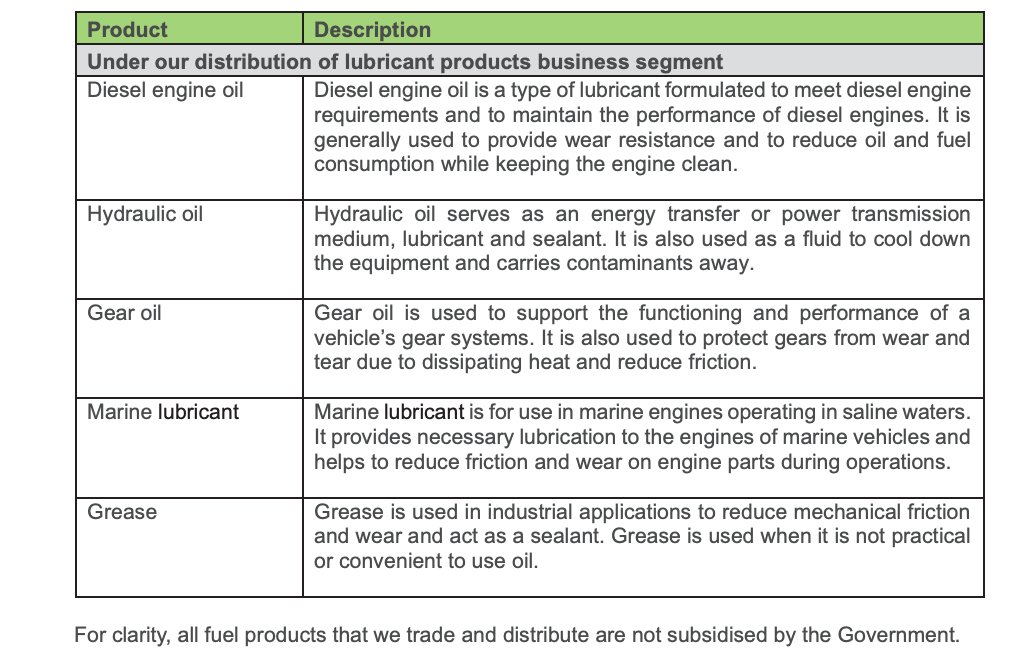

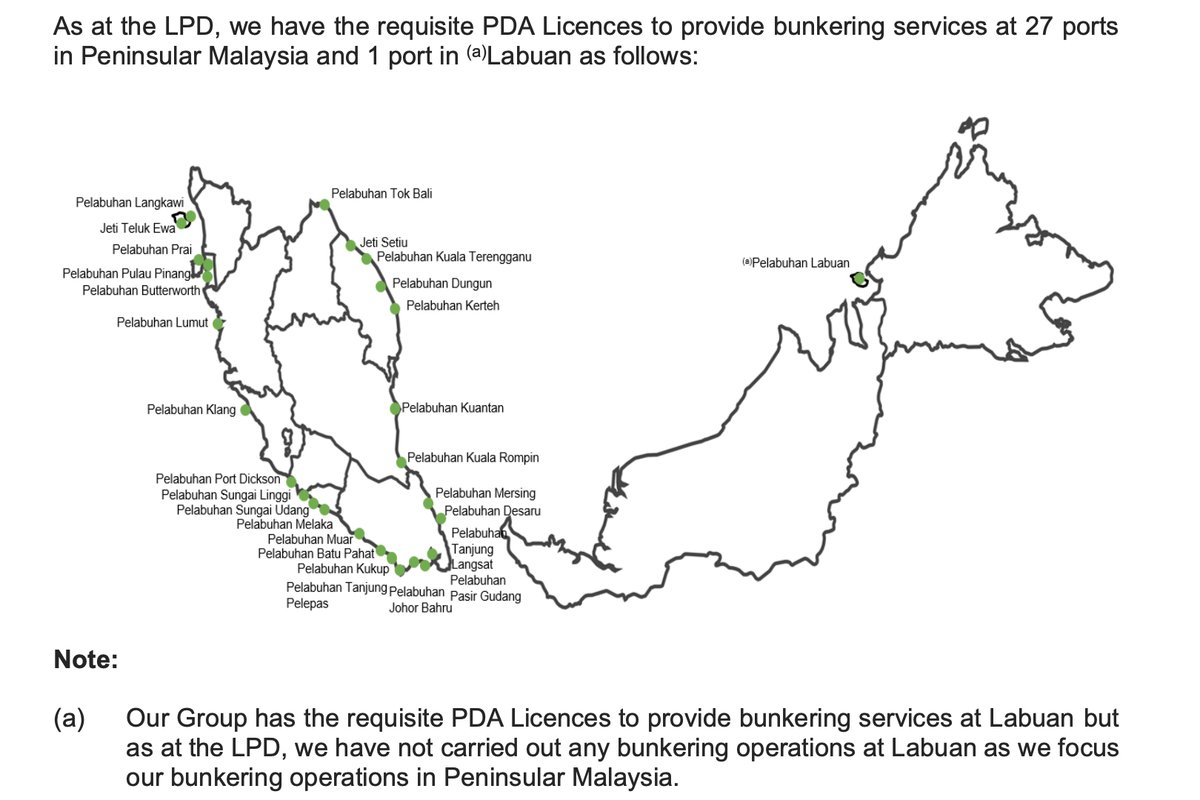

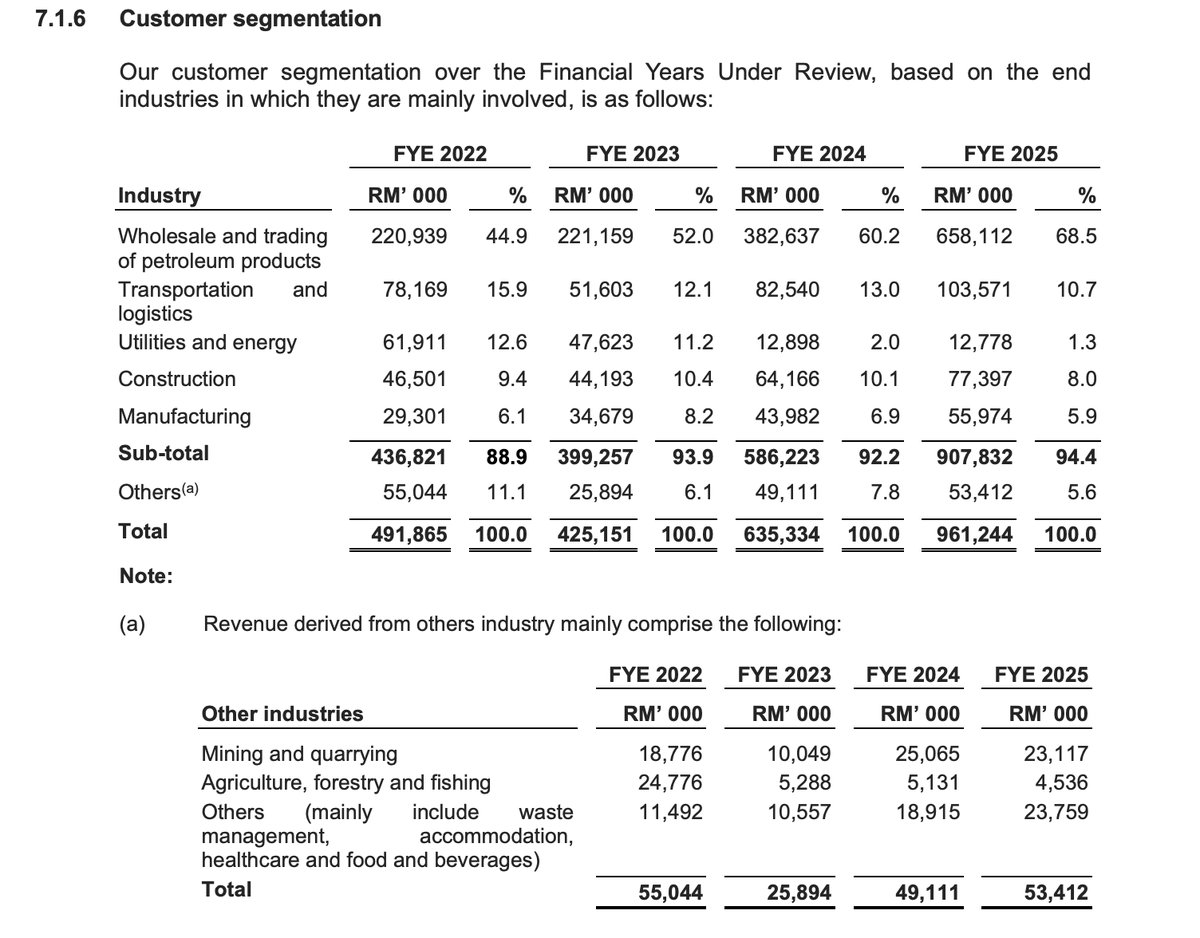

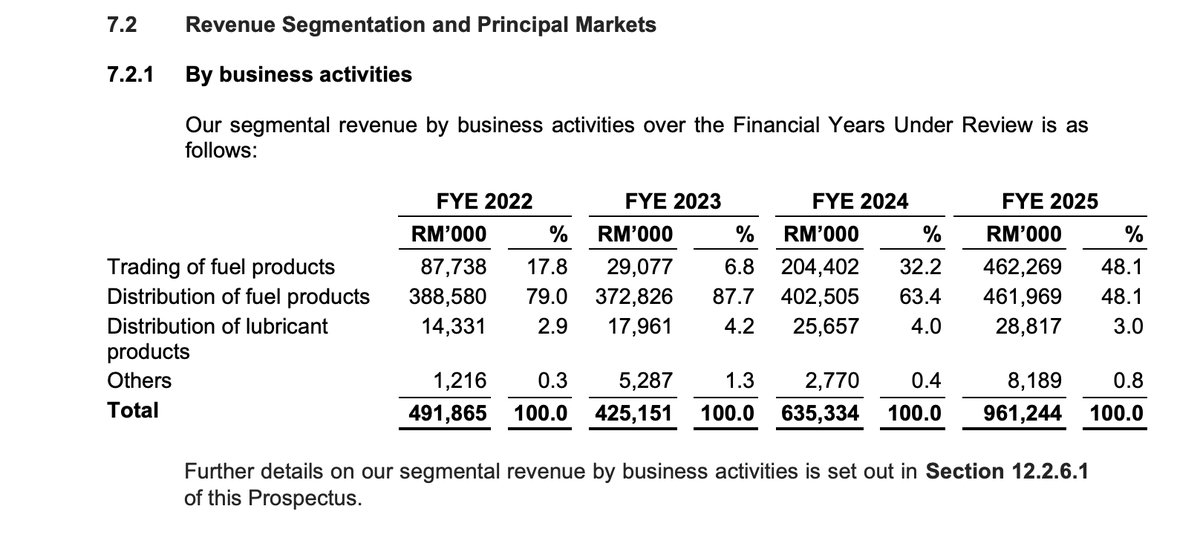

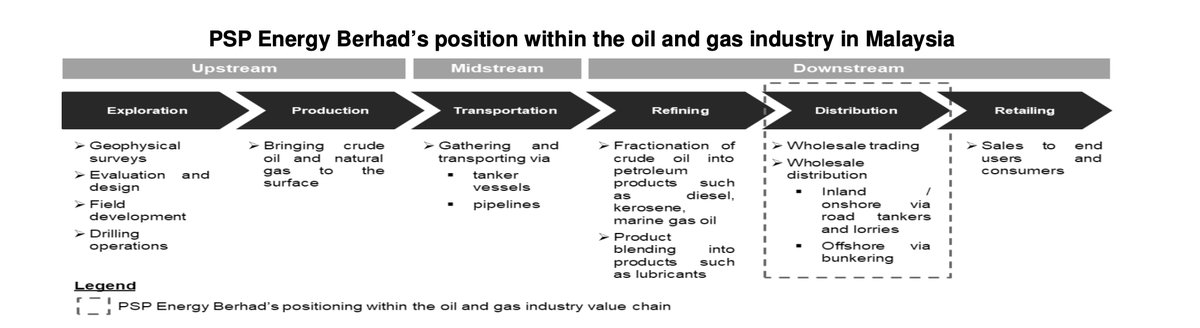

PSP Energy Berhad, through its subsidiaries, is principally involved in the trading and distribution of fuel and lubricant products in Malaysia. The Group's key business segments include the wholesale trading of fuel products; the distribution of fuel products using its own fleet of road tankers and bunker vessels; and the distribution of both third-party and its own brand of lubricant products. The company has over 13 years of operating history and serves a diverse customer base across industries like wholesale petroleum trading, transportation, logistics, utilities, energy, construction, and manufacturing. Its operations are supported by its own assets, including licensed storage plants, a fleet of road tankers, and bunker vessels for ship-to-ship bunkering services.

IPO Details

Strategic Overview & Data Visuals

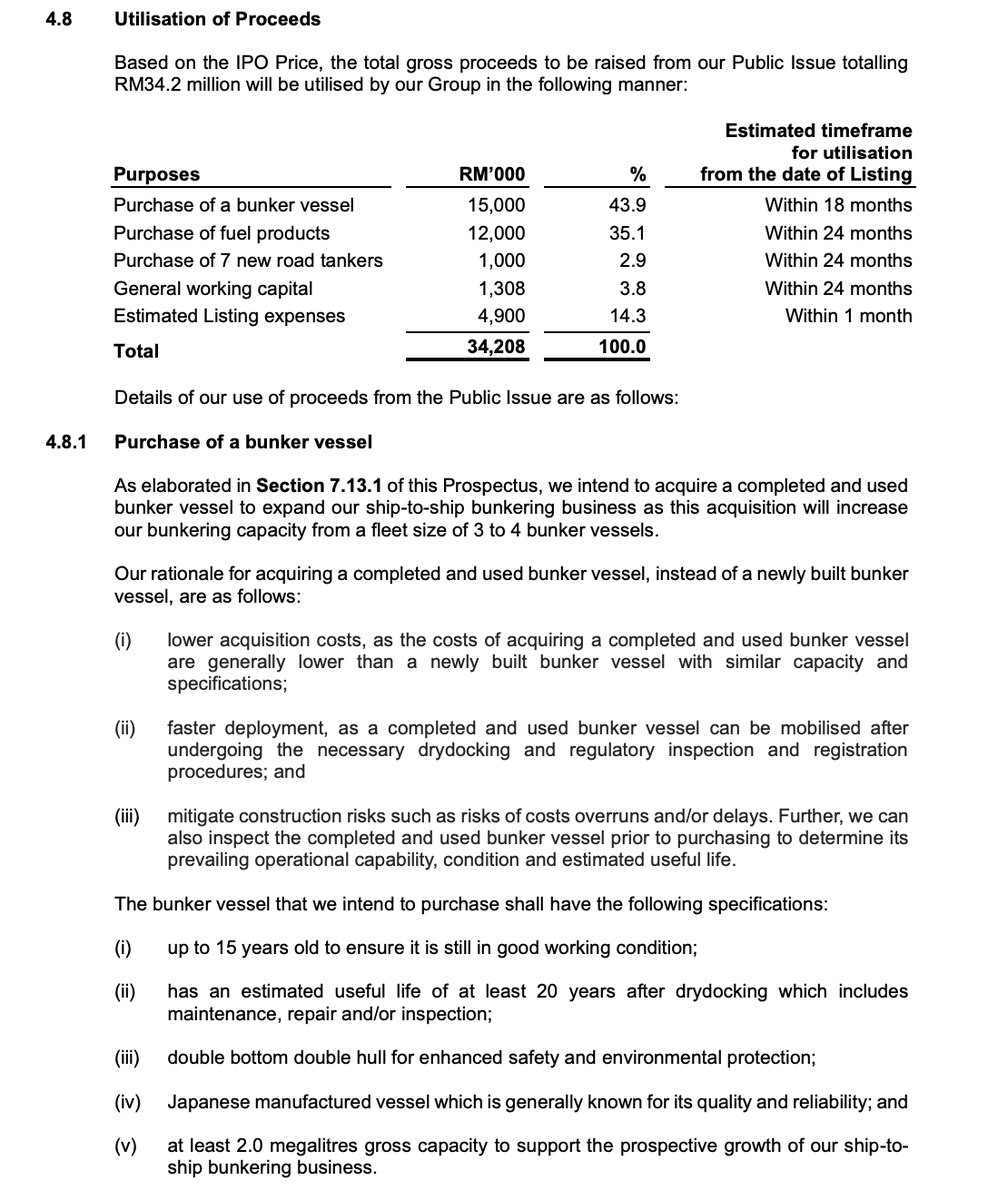

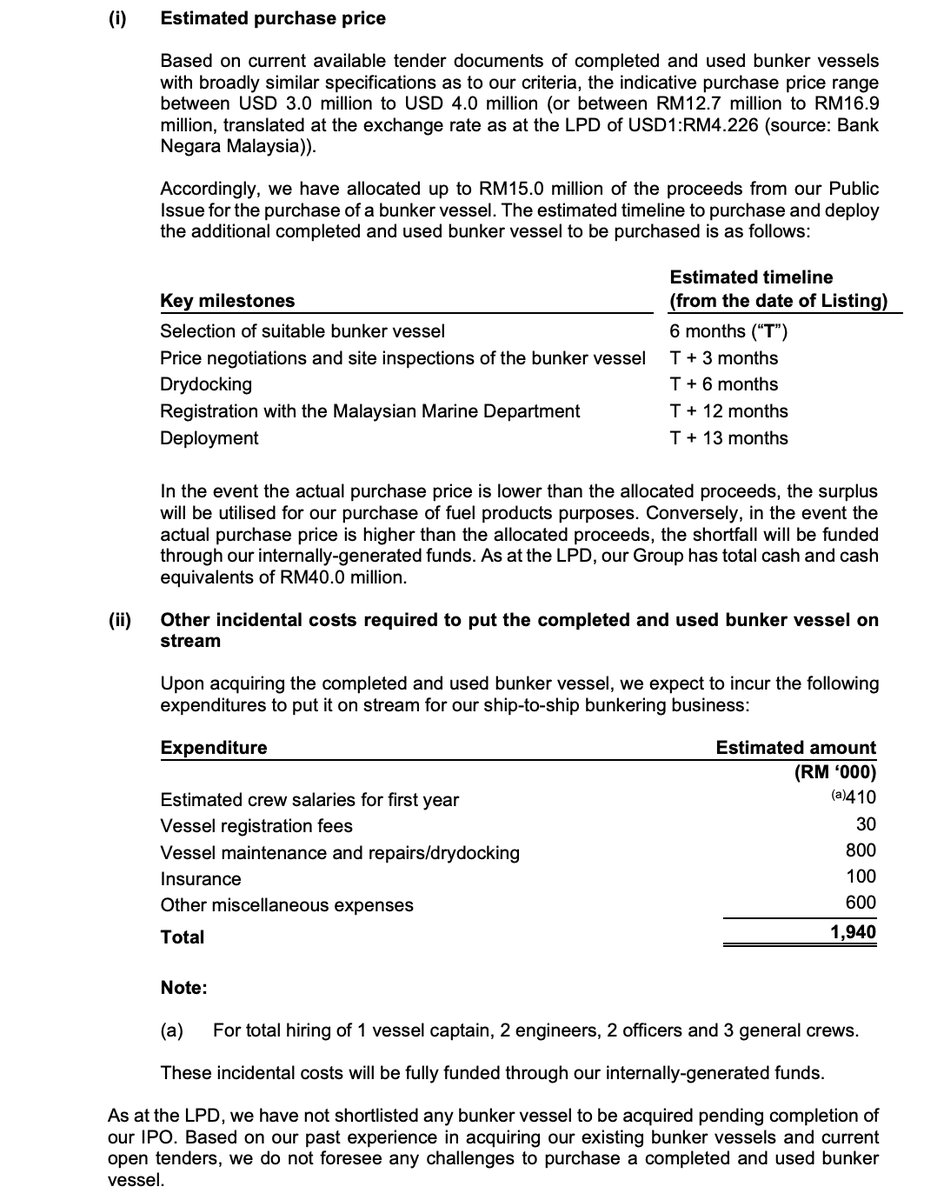

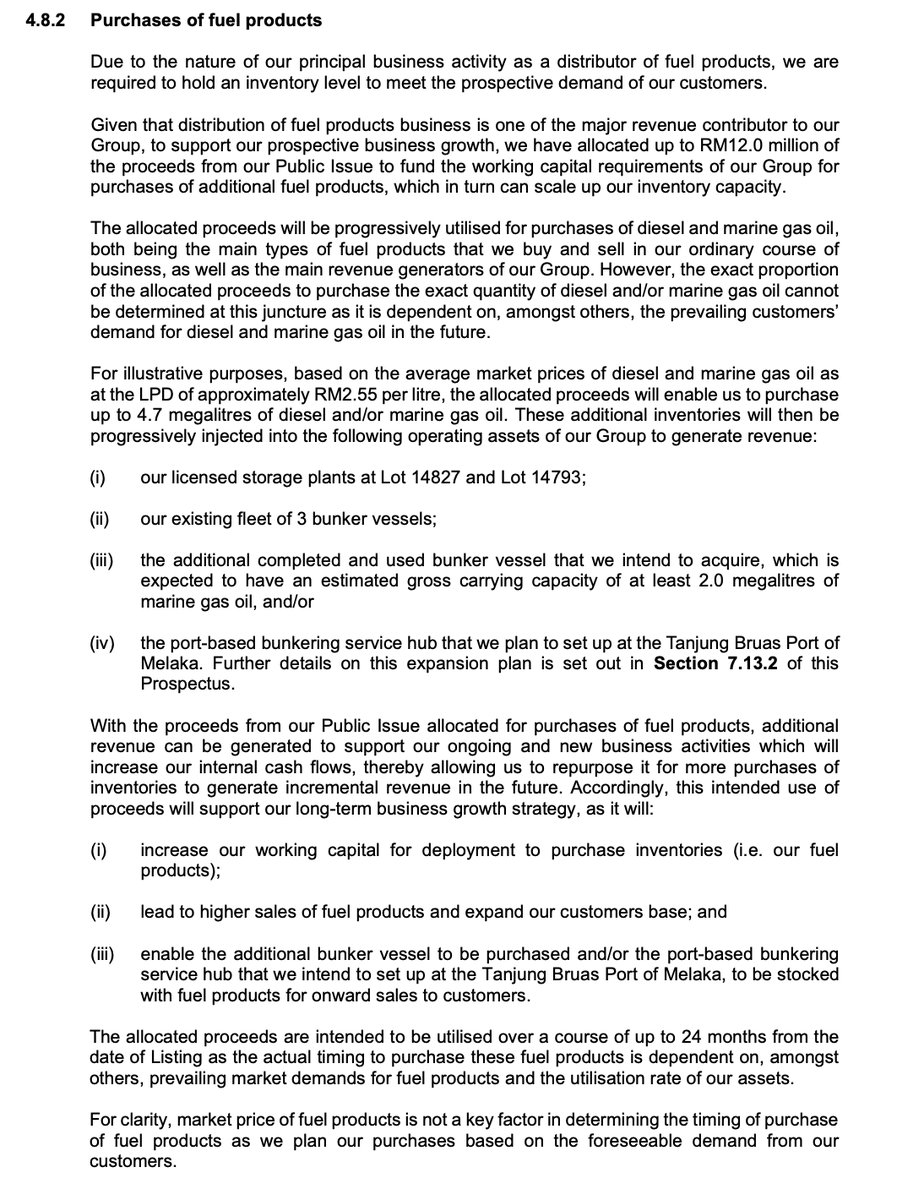

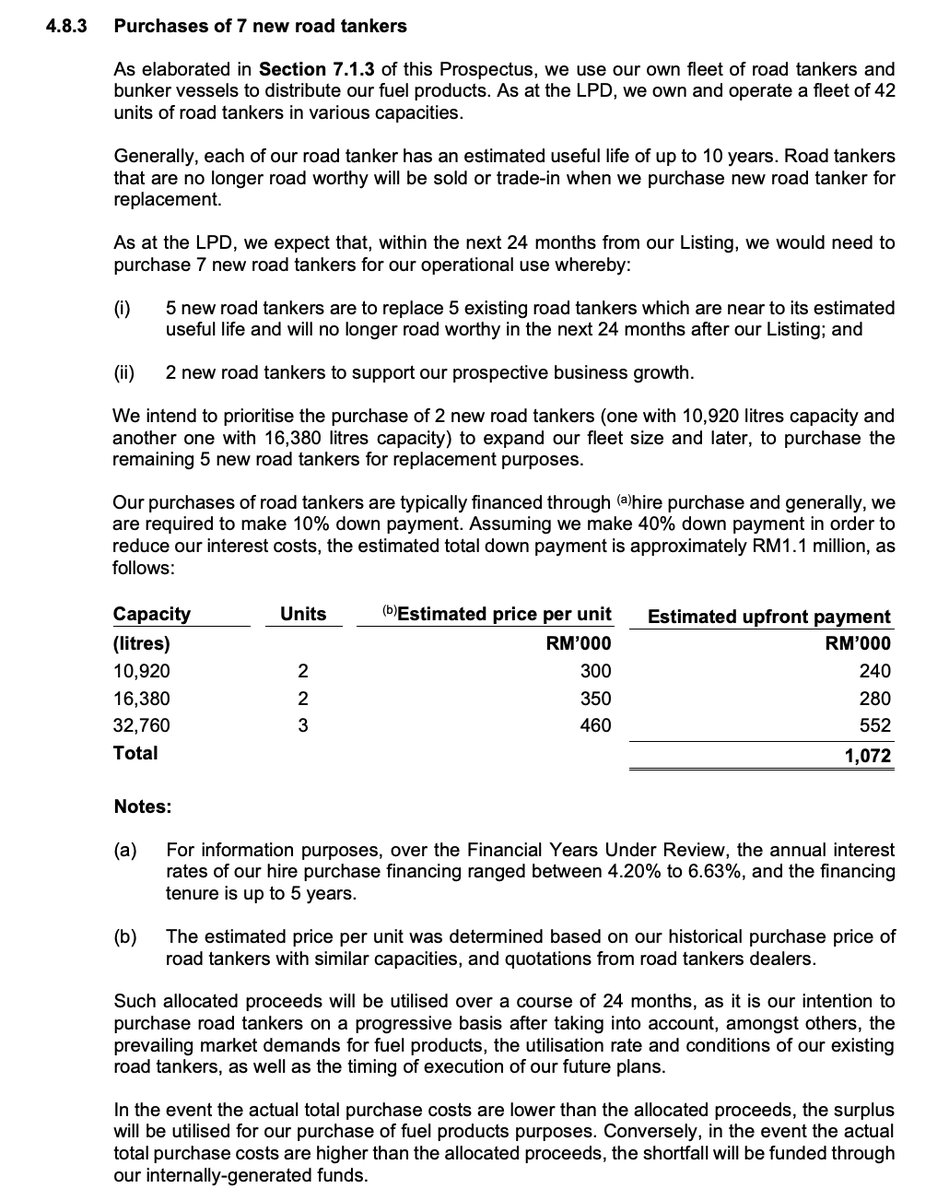

Utilisation of Proceeds

| Purpose | Amount (RM'000) | % | |

|---|---|---|---|

| Expansion | Purchase of a bunker vessel | 15,000 | 43.9 |

| Expansion | Purchase of 7 new road tankers | 1,000 | 2.9 |

| Working capital | Purchase of fuel products | 12,000 | 35.1 |

| Working capital | General working capital | 1,308 | 3.8 |

| Listing expenses | Estimated Listing expenses | 4,900 | 14.3 |

| Total | 34,208 | 100 | |

Analyst Highlights

| Date | Analyst Highlights |

|---|---|

|

21-Nov-2025

Mplus |

|

Utilisation of Proceeds

Business Segments

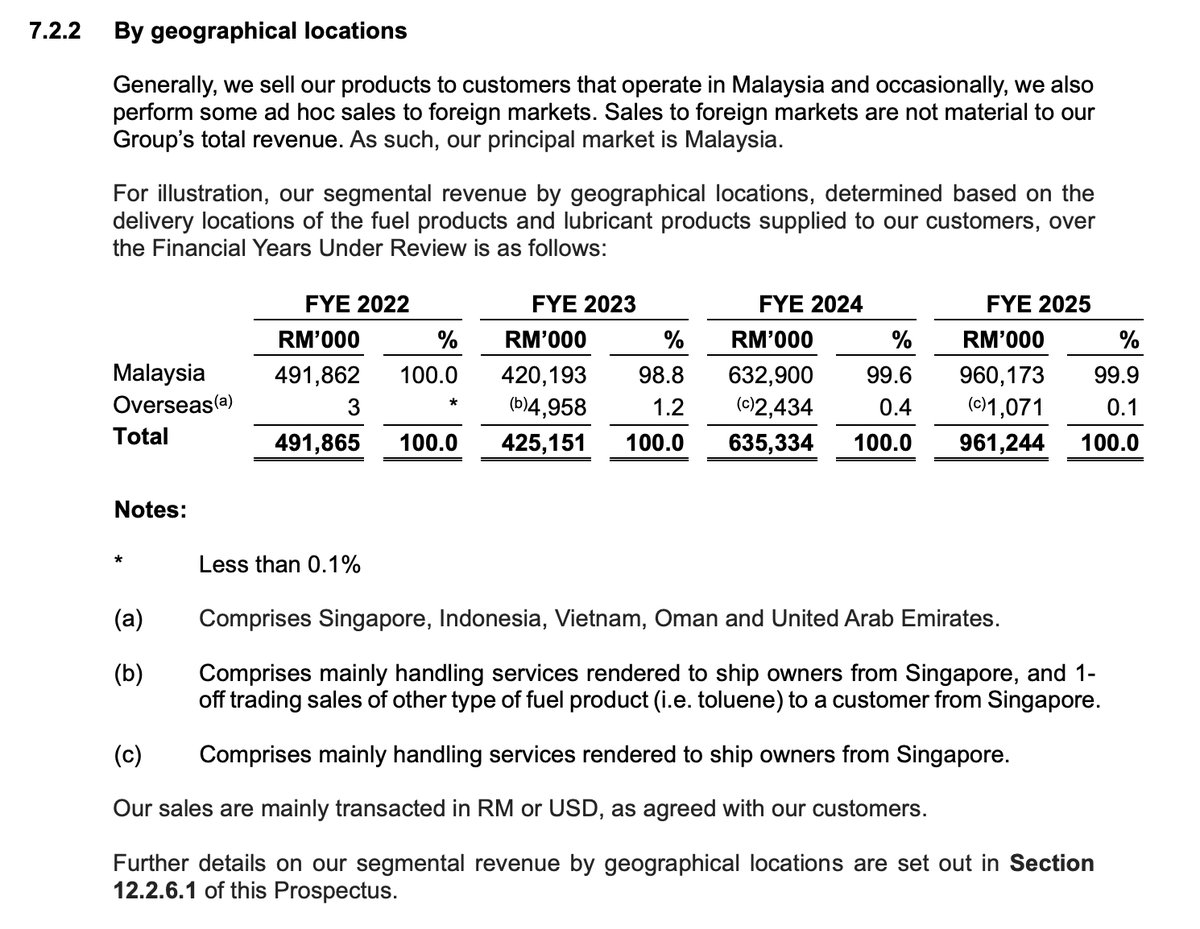

Geographical Segments

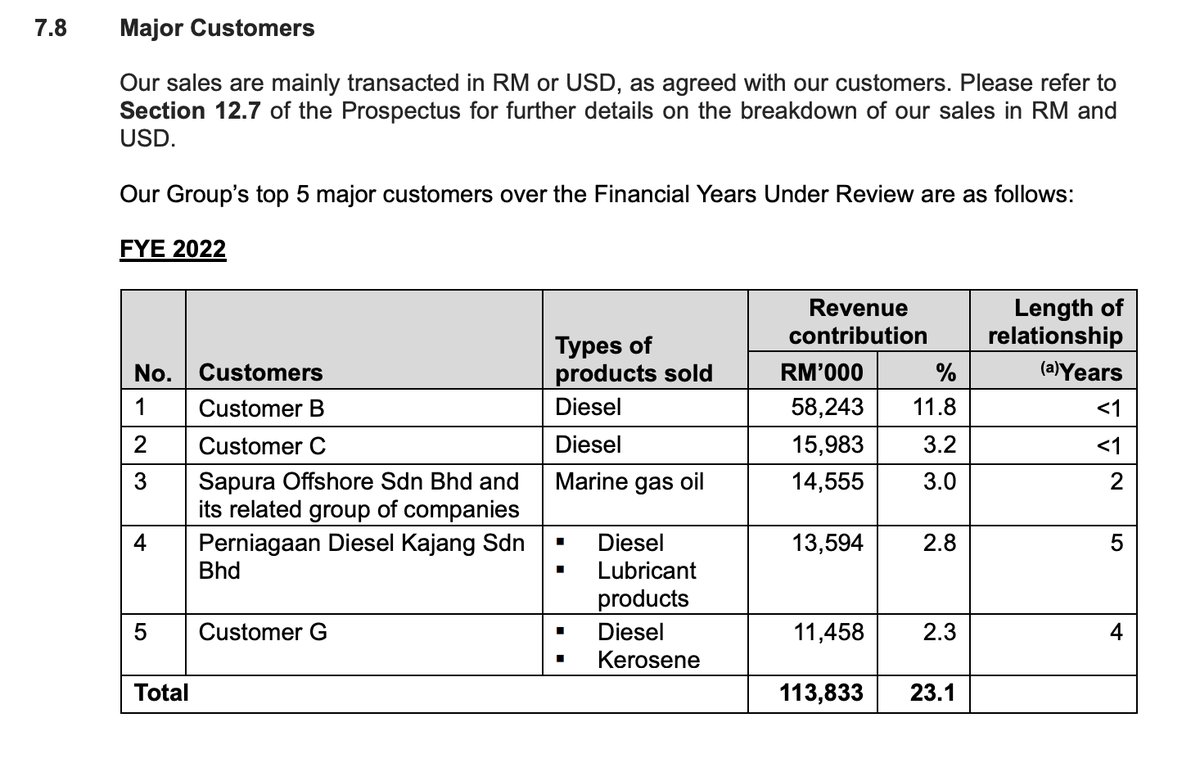

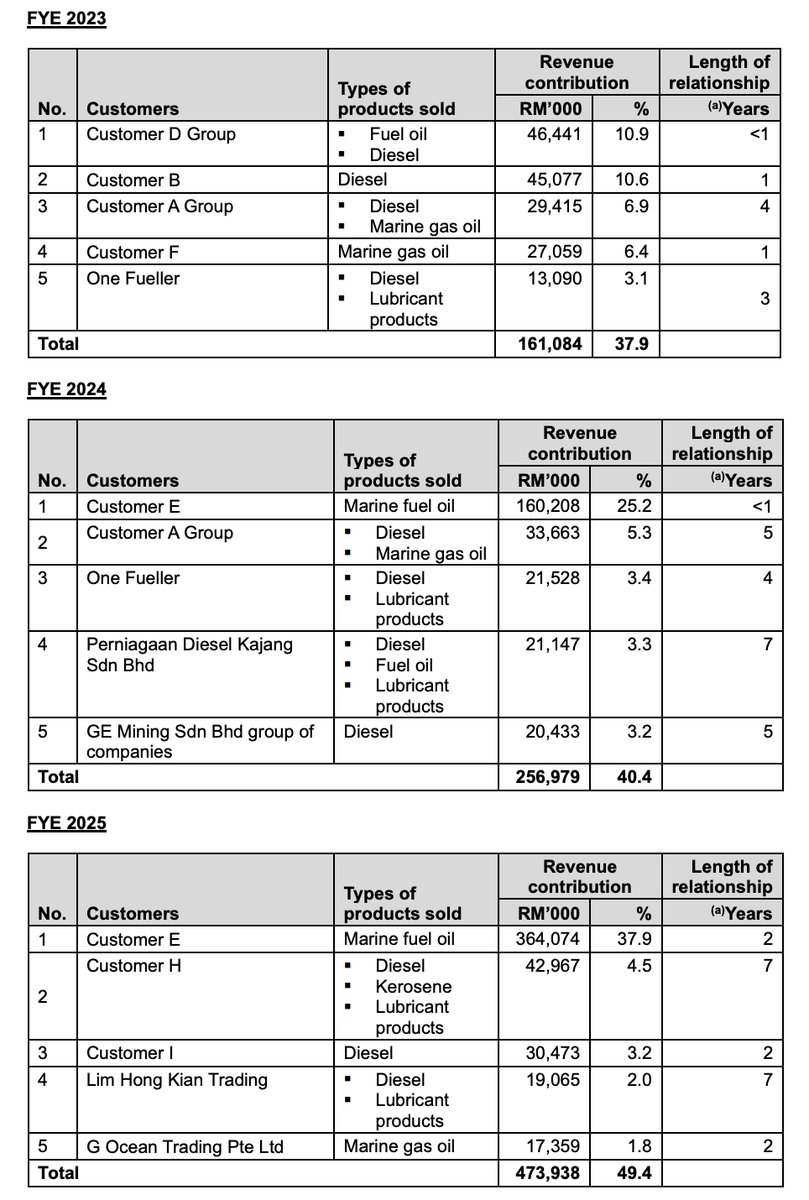

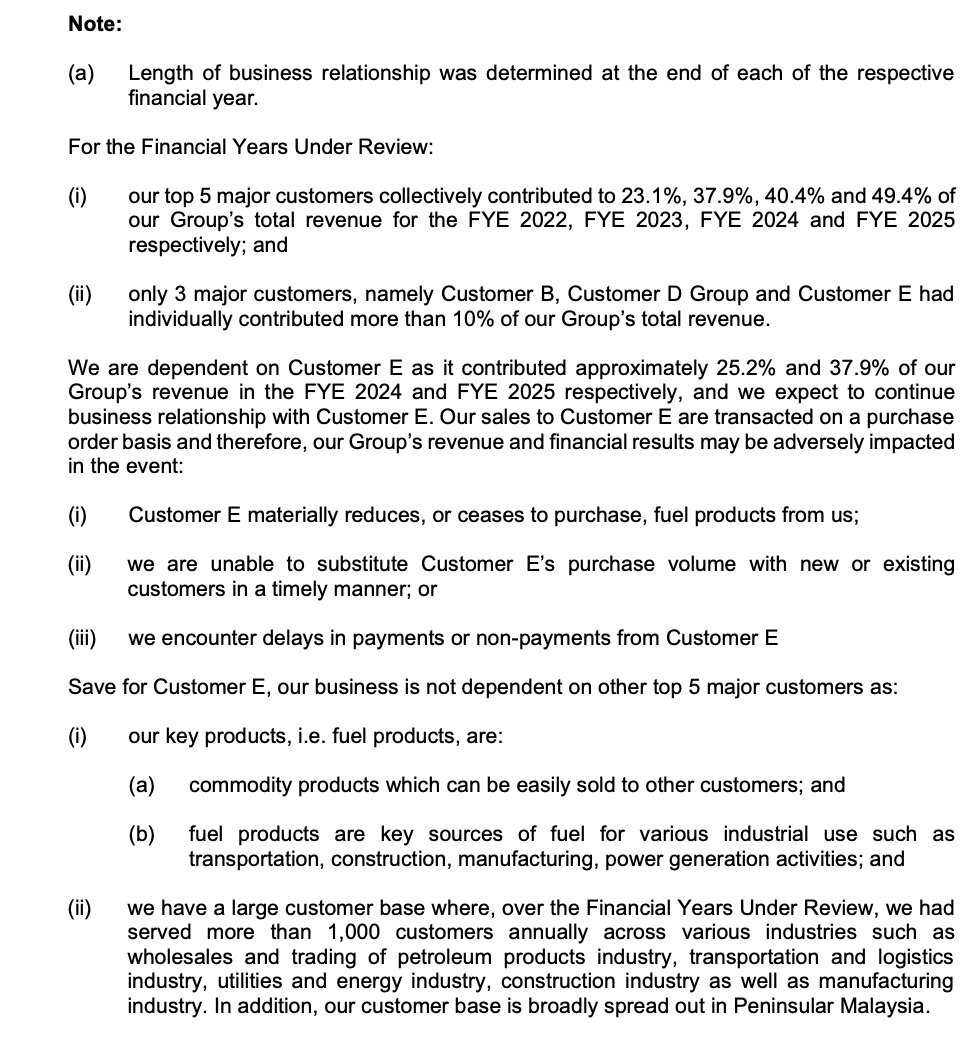

Major Customers

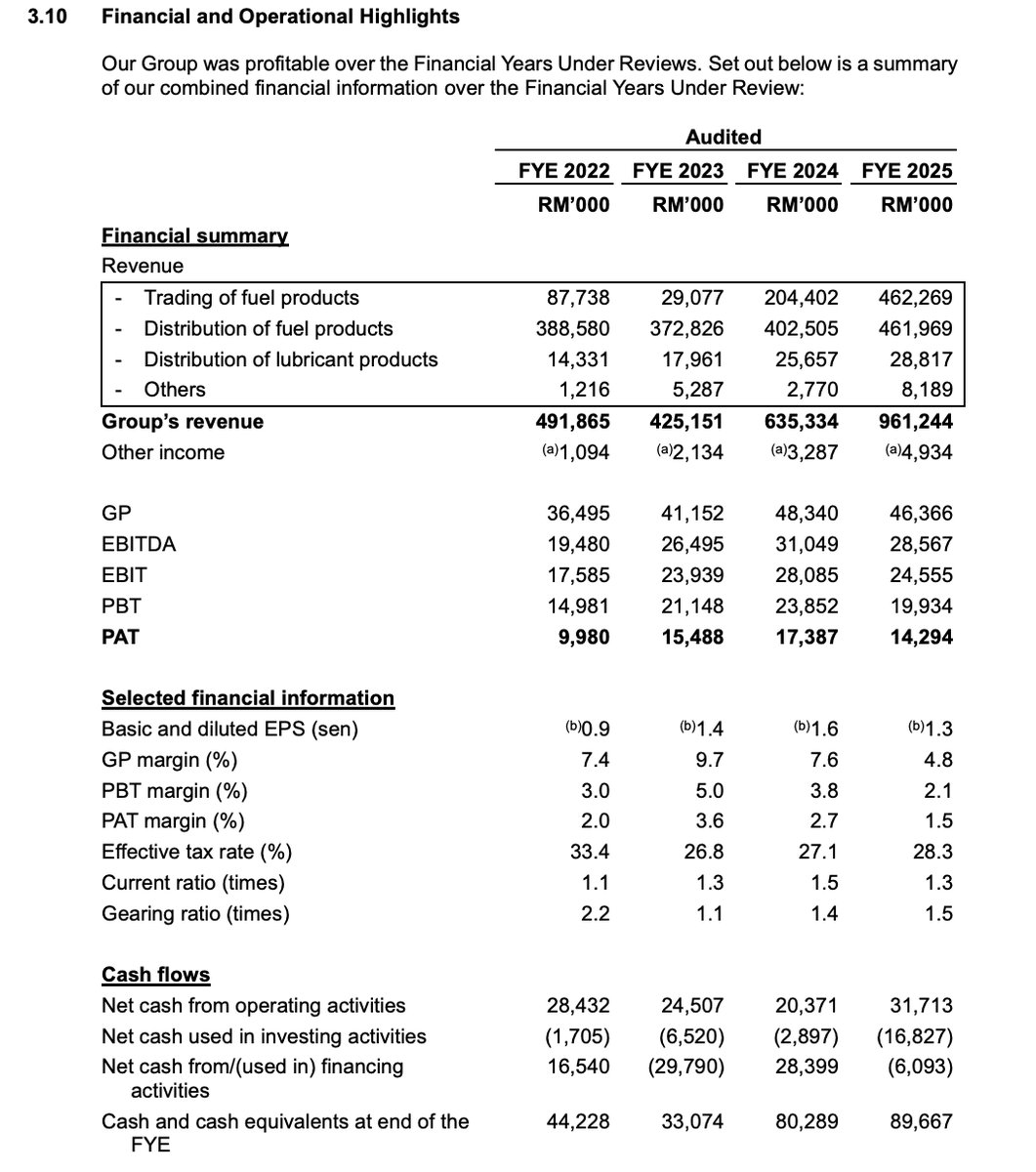

Revenue by Financial Year Ended

Profit After Tax (PAT) by Financial Year Ended

SWOT Analysis

Strengths

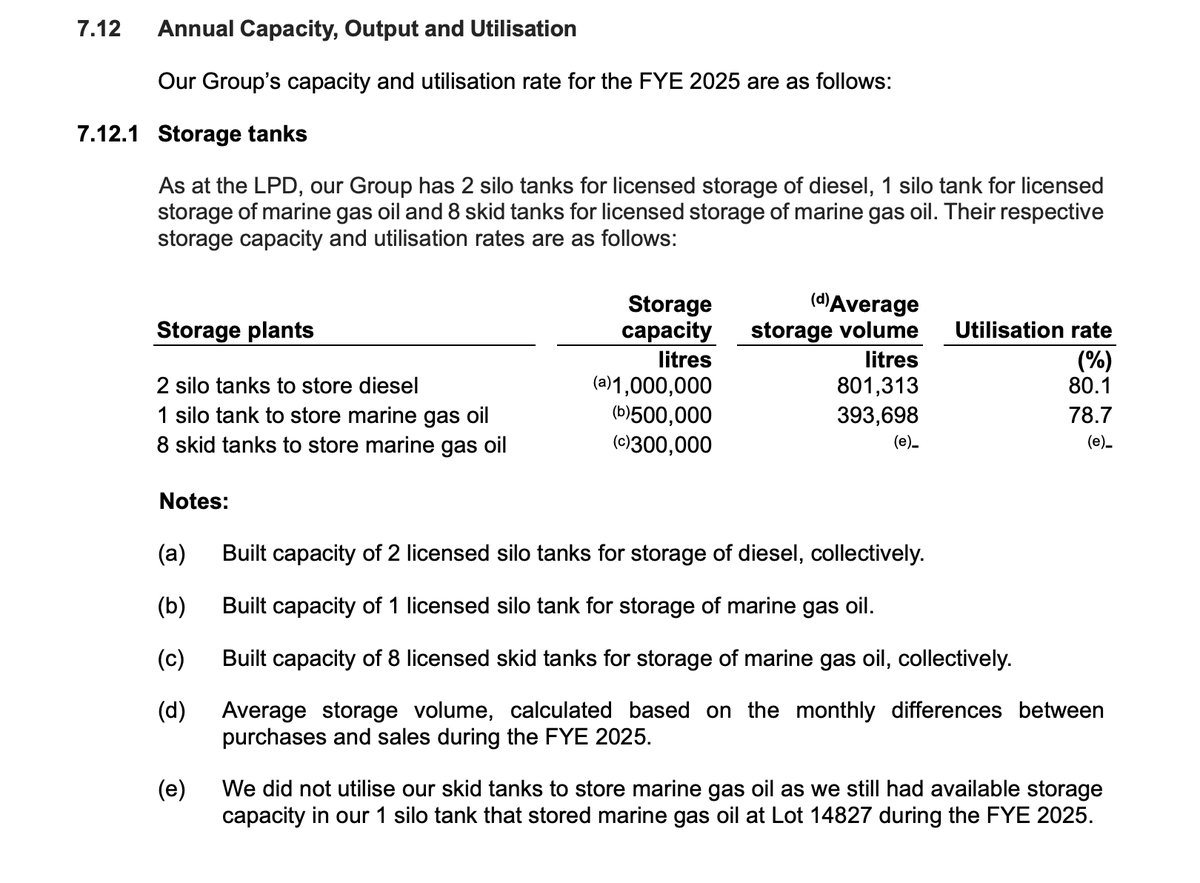

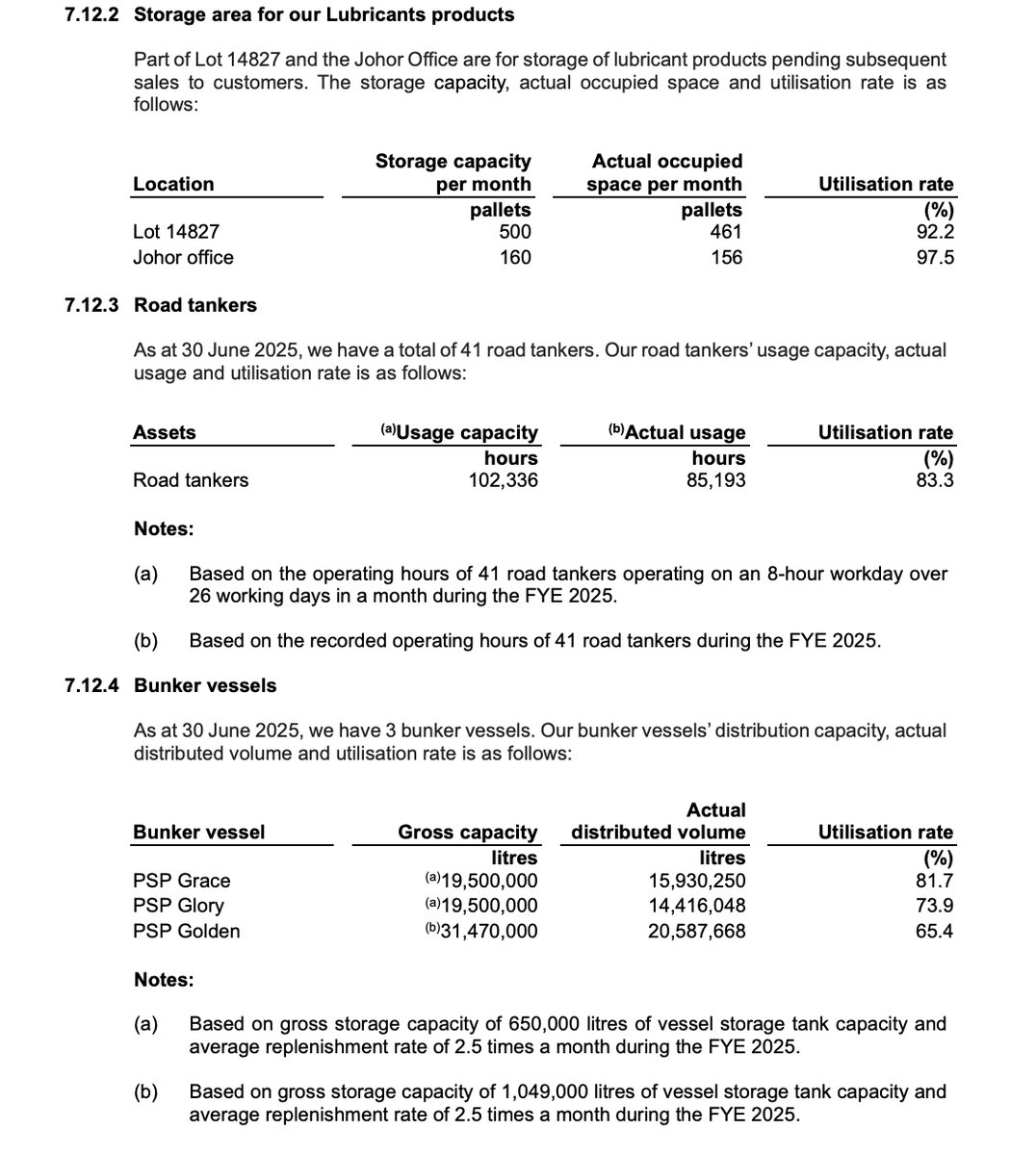

- Owns key assets: Owns and operates its own logistics and storage infrastructure, including 2 licensed storage plants, 42 road tankers, and 3 bunker vessels, providing operational flexibility and capacity.

Weaknesses

- Customer concentration: Highly dependent on a single major customer, Customer E, which accounted for 37.9% of the Group's total revenue in FYE 2025.

- Declining profitability: Gross profit margin declined significantly from 7.6% in FYE 2024 to 4.8% in FYE 2025, leading to a 17.8% drop in Profit After Tax (PAT) despite strong revenue growth.

- Intense competition: The petroleum products trading and distribution industry in Malaysia is fragmented and competitive, which can lead to margin compression.

Opportunities

- Expand bunkering services: Plans to acquire an additional completed and used bunker vessel to increase bunkering capacity and capitalize on the segment's significant revenue growth (CAGR of 11.7% from FYE 2022 to FYE 2025).

- Expand storage capacity: Intends to establish a new port-based bunkering service hub in Melaka by renting land and facilities at Tanjung Bruas Port, expanding its market reach regionally.

- Grow lubricants business: Aims to expand its lubricants business by setting up a branch office and warehouse in Pahang to penetrate the east coast region of Peninsular Malaysia.

Threats

- Price volatility: Subject to volatility in the market prices of fuel products, which are derived from crude oil. A sudden downward movement in prices could adversely impact profitability due to inventory holding.

- Regulatory requirements: Operates in a highly regulated industry, requiring numerous licenses and permits (e.g., PDA, CSA). Failure to maintain or renew these could disrupt business operations.

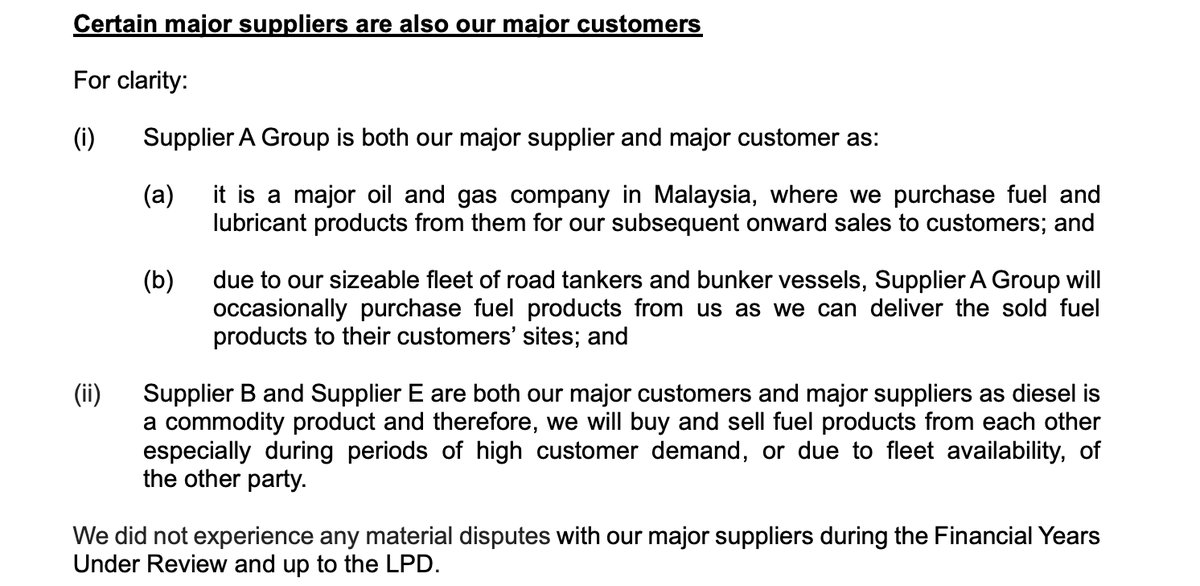

- Supplier dependency: Relies heavily on a few major oil and gas suppliers, with purchases from the top 3 suppliers (Supplier A Group, Shell Malaysia, and Supplier D) collectively making up 82.8% of total purchases in FYE 2025.

Key Highlights

Sorry, this feature only available for iSaham Pro

Conclusion

Sorry, this feature only available for iSaham Pro

PSP Energy Berhad's Latest News