One Gasmaster Holdings Berhad IPO's Analysis

One Gasmaster Holdings Berhad

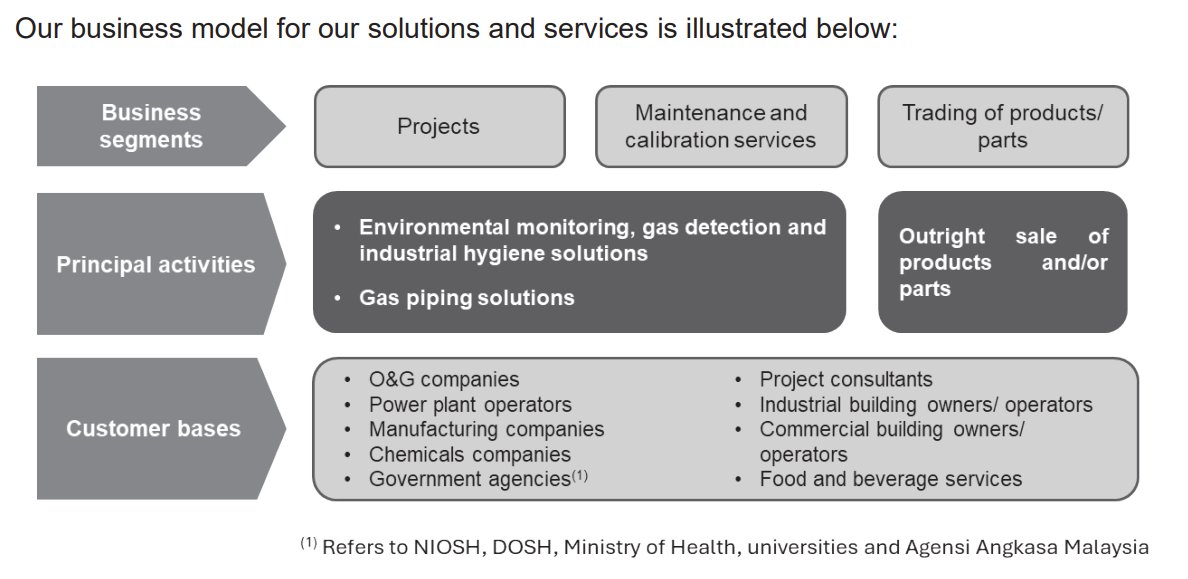

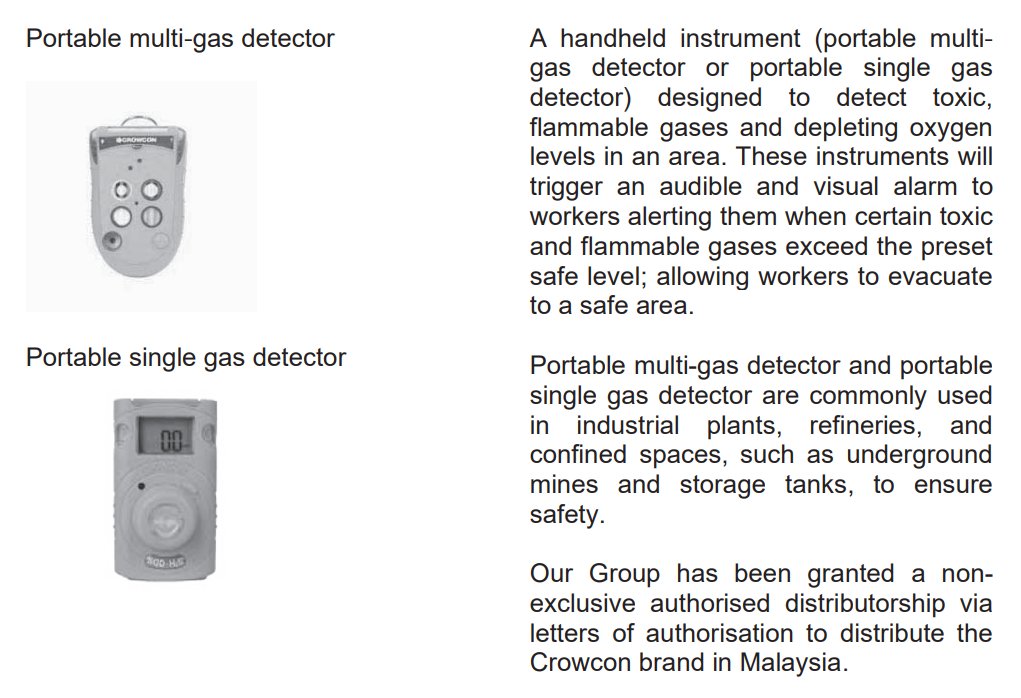

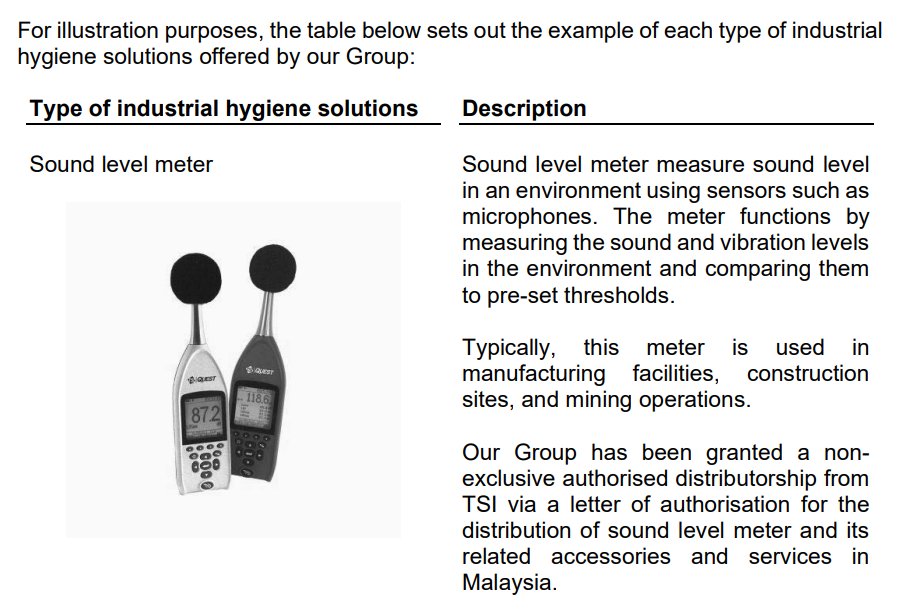

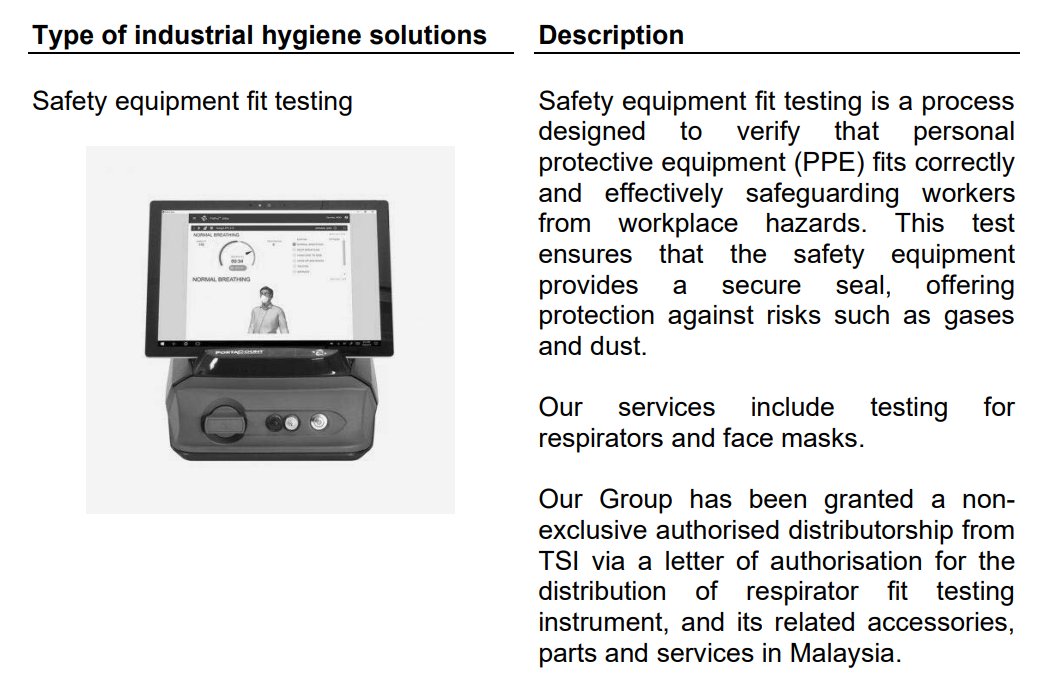

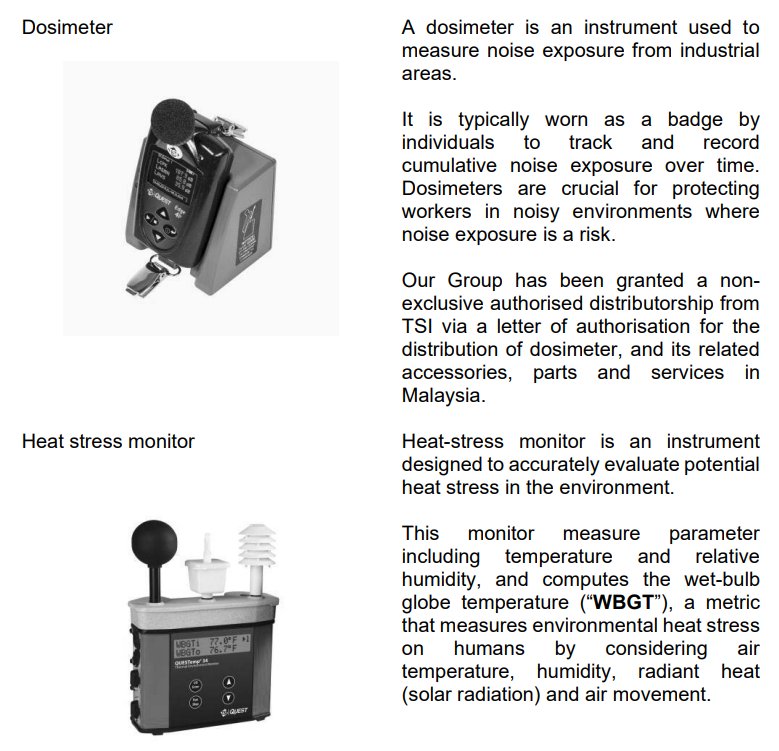

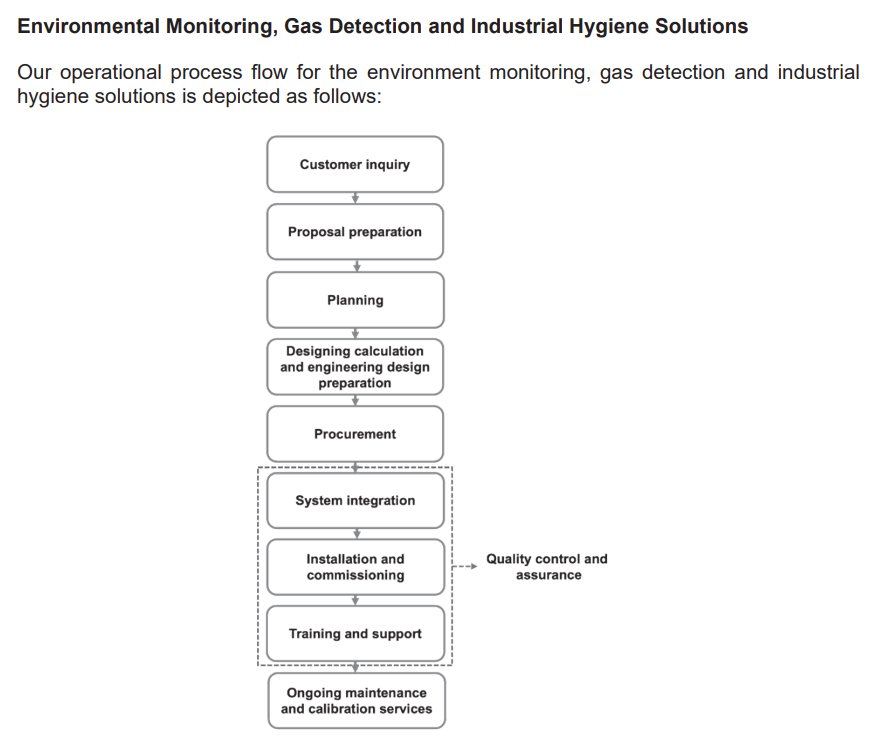

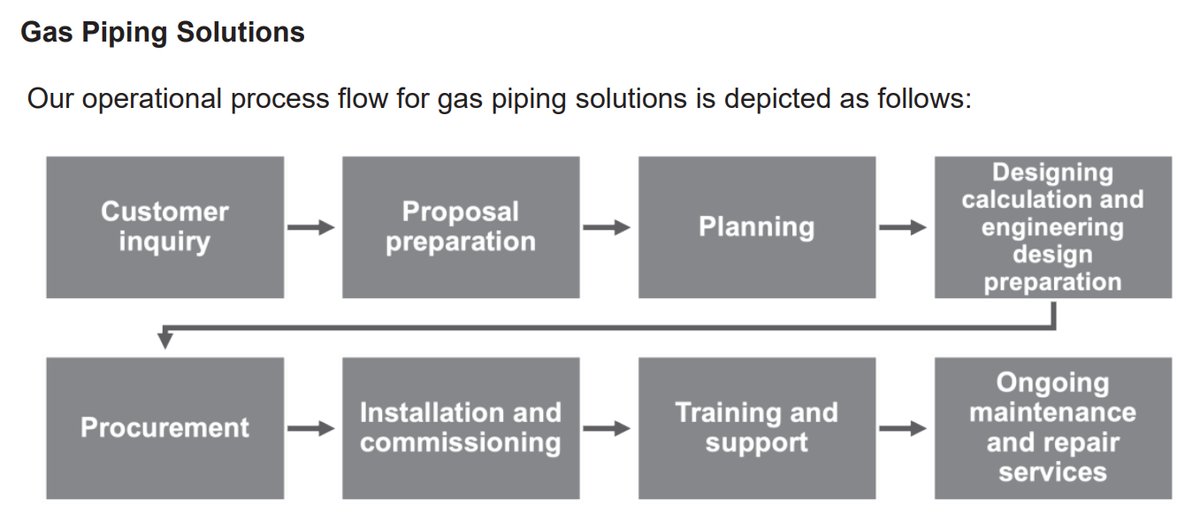

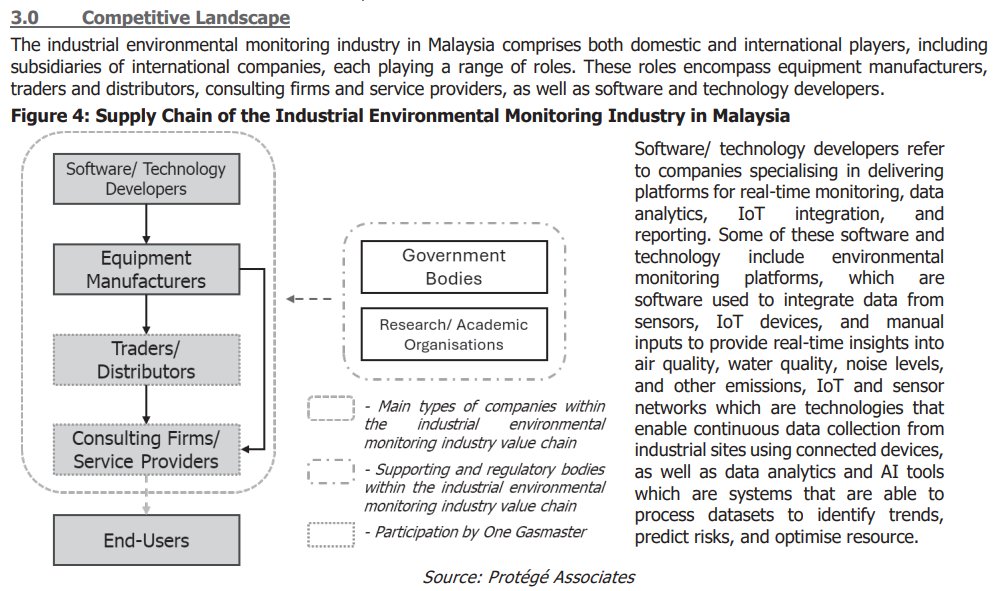

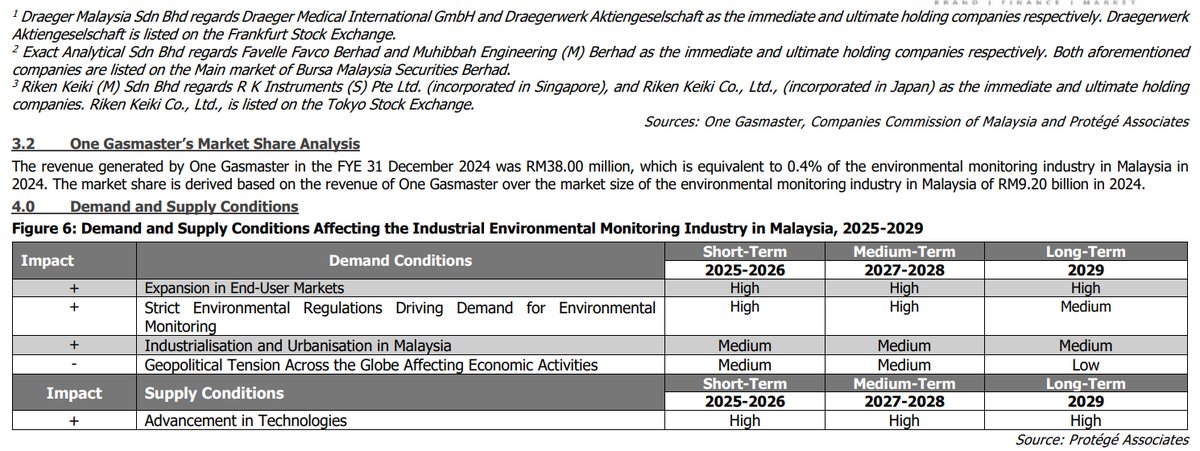

One Gasmaster Holdings Berhad is principally involved in providing environmental monitoring, gas detection, gas piping, and industrial hygiene services. The Group offers comprehensive solutions that include the design, supply, installation, testing, and commissioning of its systems. It complements these offerings with maintenance and calibration services through its ISO/IEC 17025 certified laboratory, ensuring accurate and reliable system performance for clients across various industries such as oil & gas, power generation, manufacturing, food and beverage, and chemicals. Additionally, the company trades in related products, including instruments, parts, and components to support its customers' operational needs.

IPO Details

Strategic Overview & Data Visuals

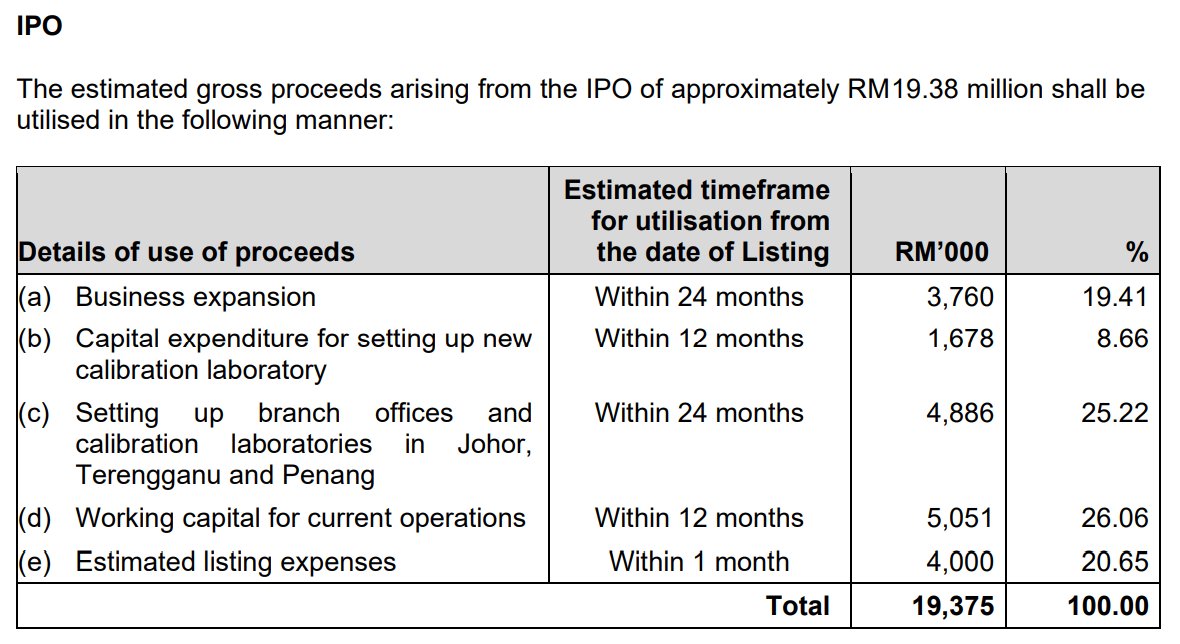

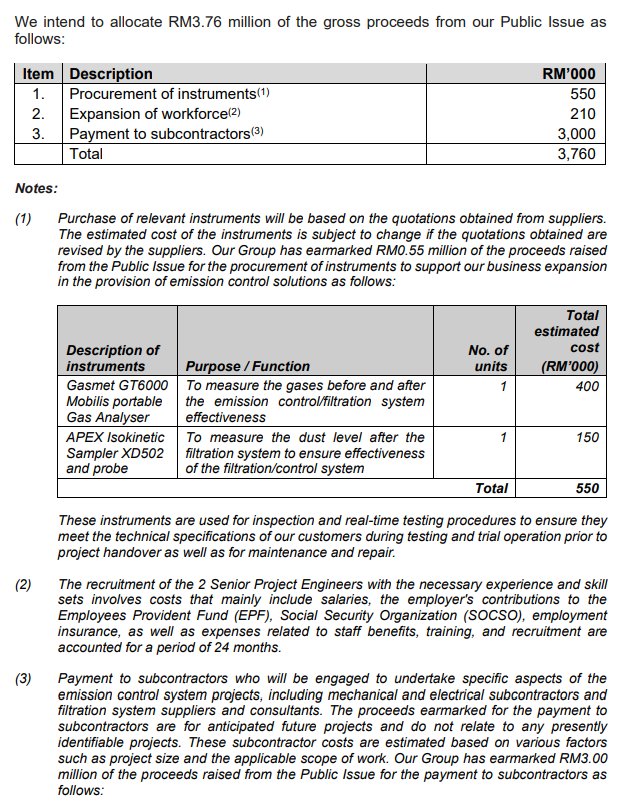

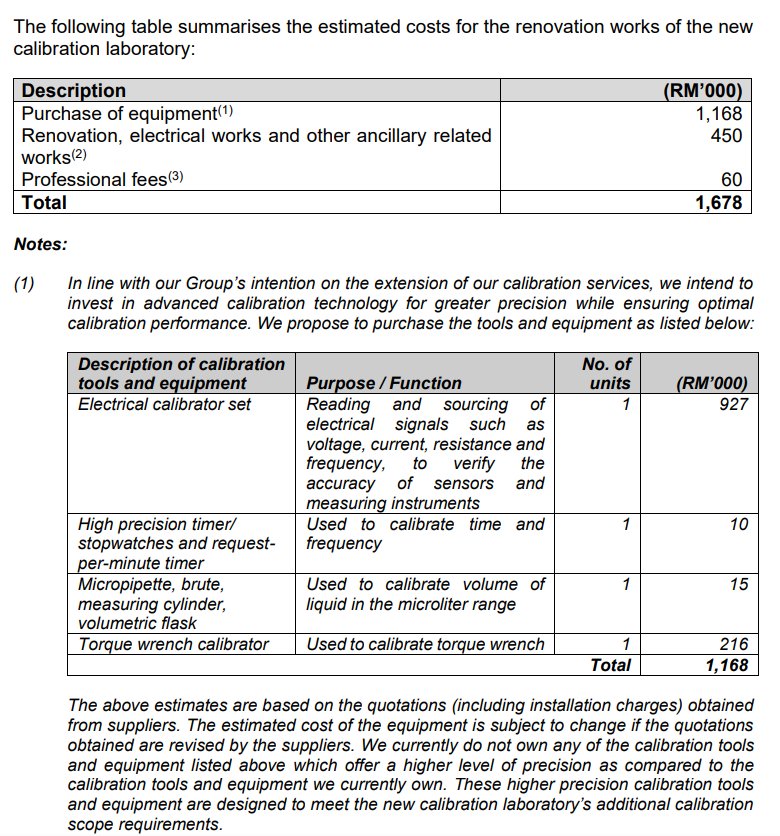

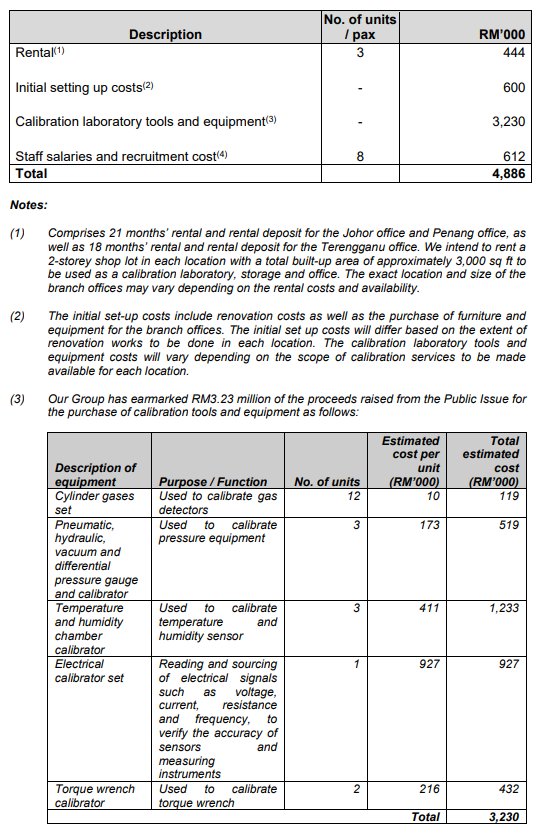

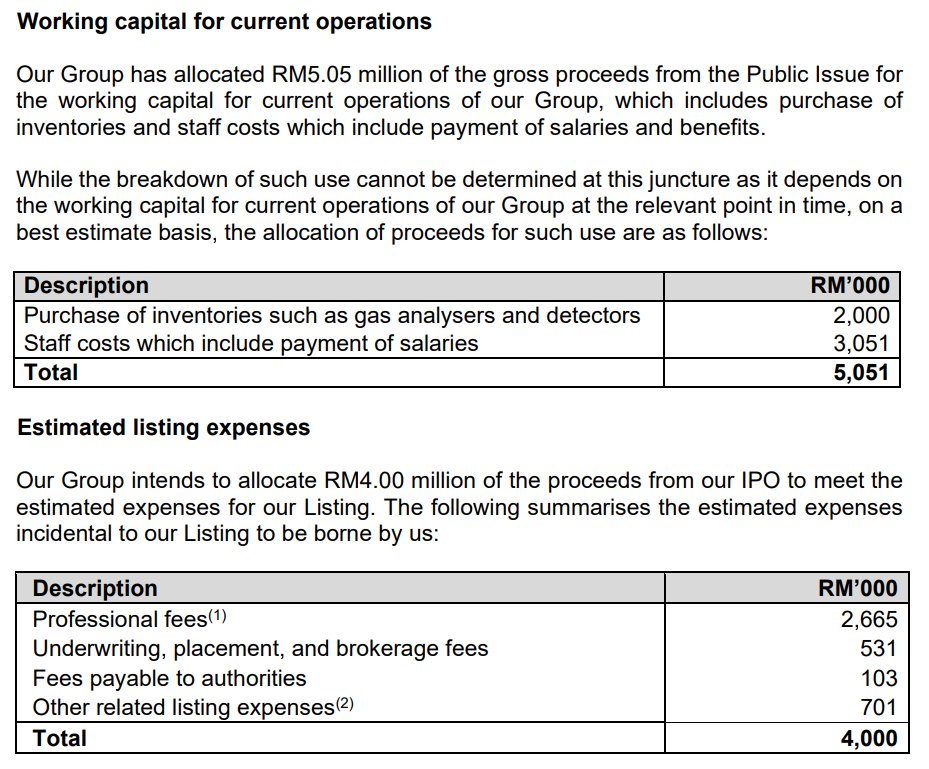

Utilisation of Proceeds

| Purpose | Amount (RM'000) | % | |

|---|---|---|---|

| Expansion | Business expansion | 3,760 | 19.41 |

| Expansion | Capital expenditure for setting up new calibration laboratory | 1,678 | 8.66 |

| Expansion | Setting up branch offices and calibration laboratories in Johor, Terengganu and Penang | 4,886 | 25.22 |

| Working capital | Working capital for current operations | 5,051 | 26.06 |

| Listing expenses | Estimated listing expenses | 4,000 | 20.65 |

| Total | 19,375 | 100 | |

Analyst Highlights

| Date | Analyst Highlights |

|---|---|

|

15-Jan-2026

TA |

|

Utilisation of Proceeds

Business Segments

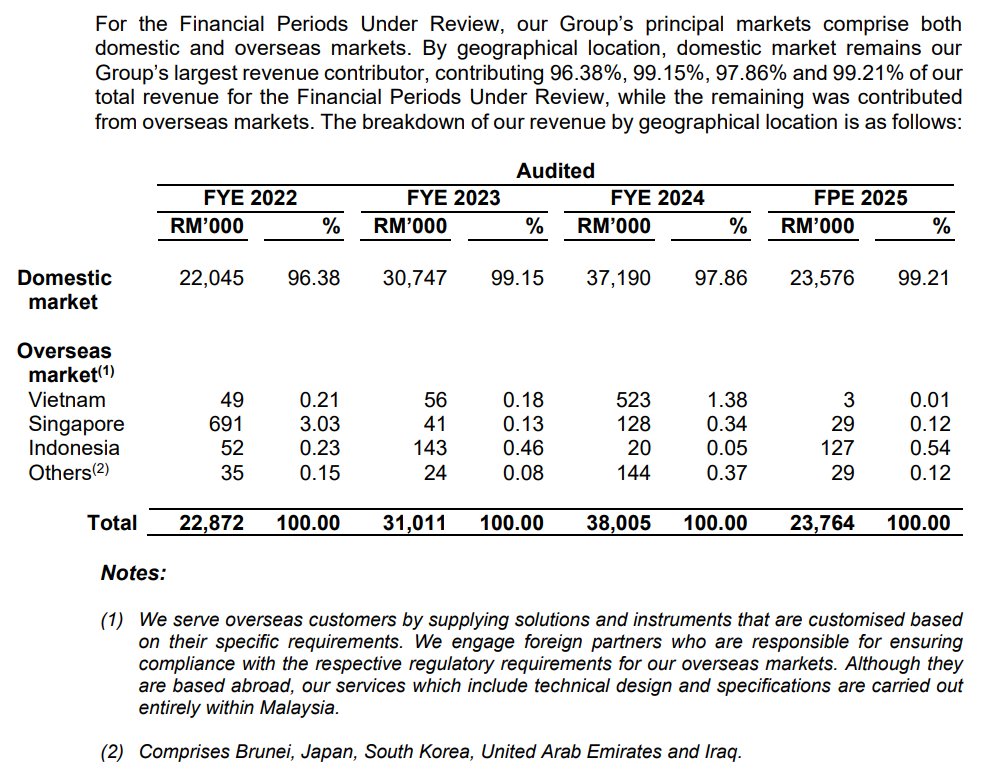

Geographical Segments

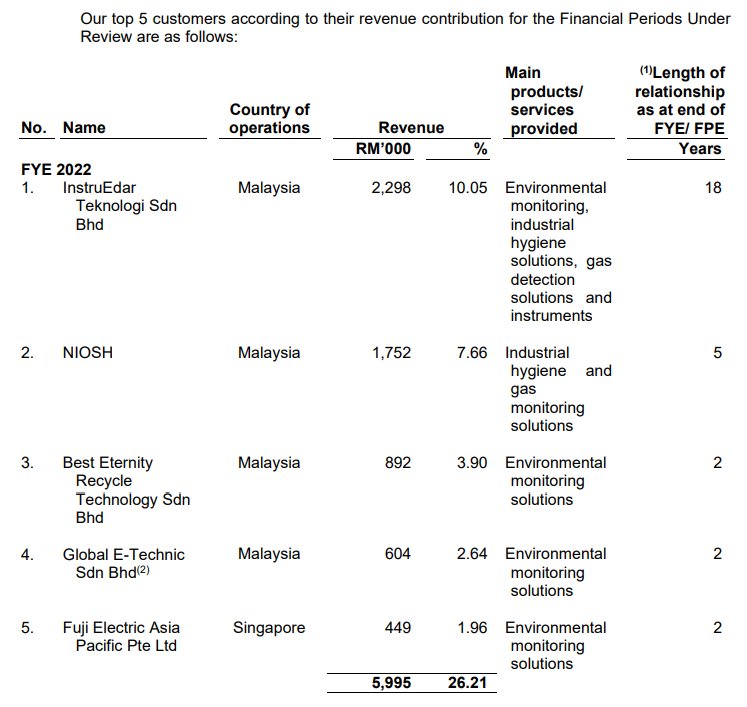

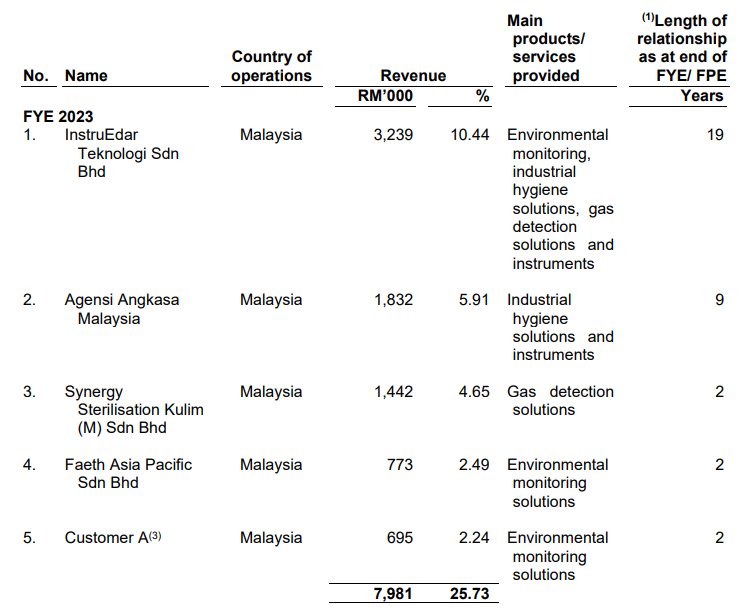

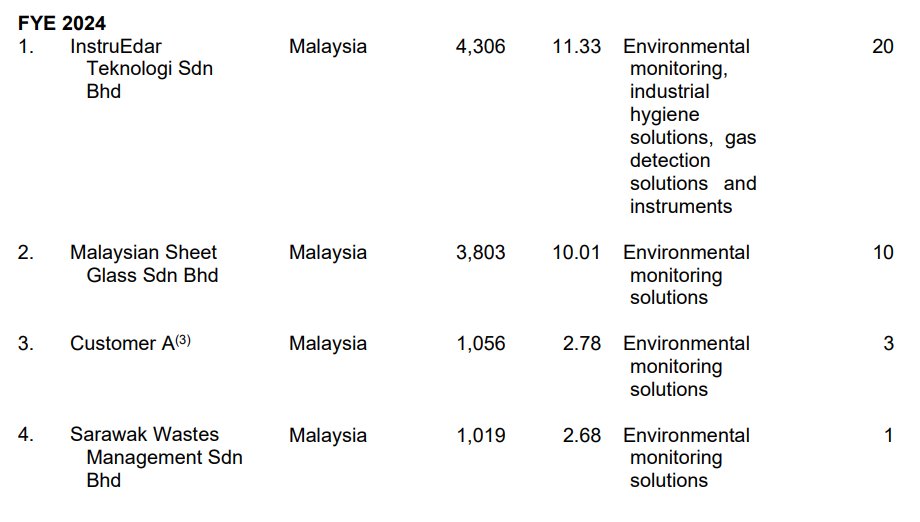

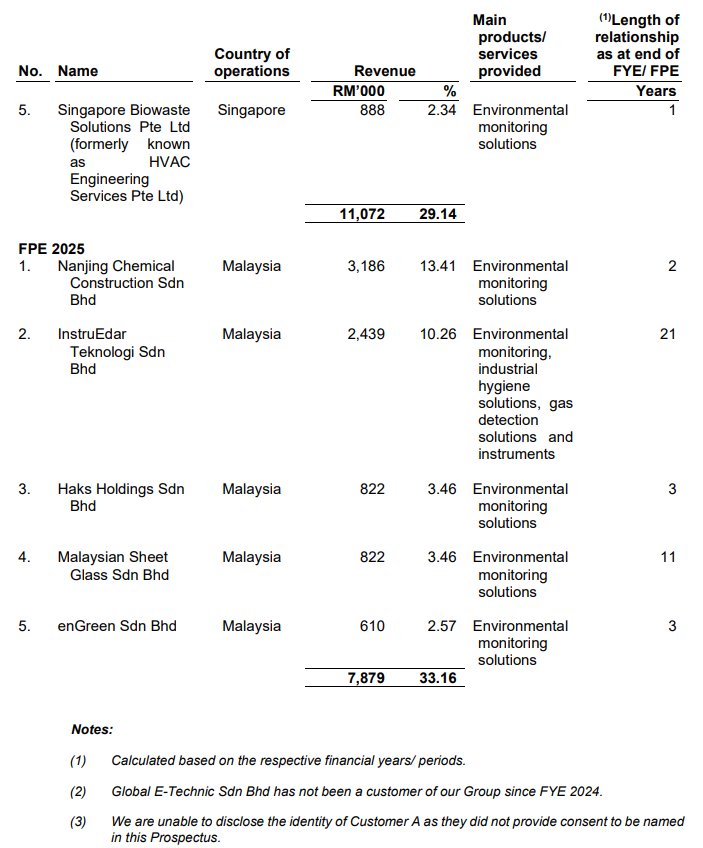

Major Customers

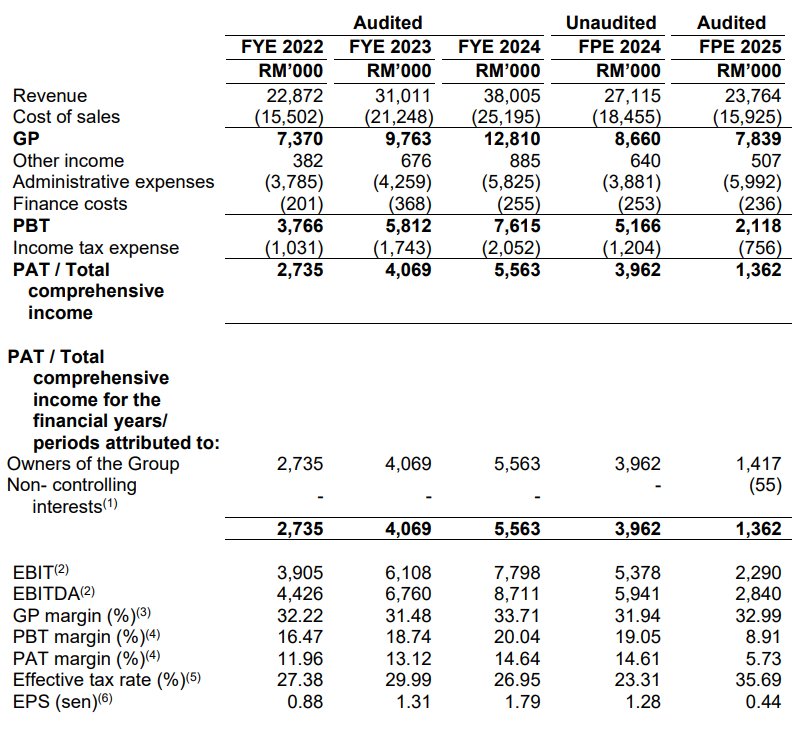

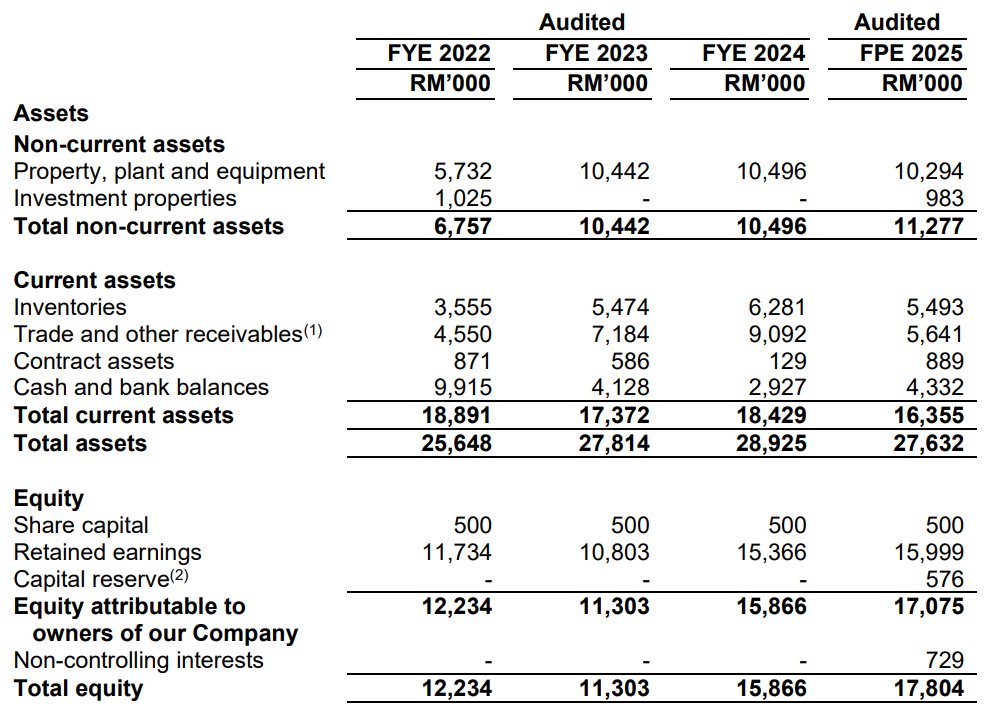

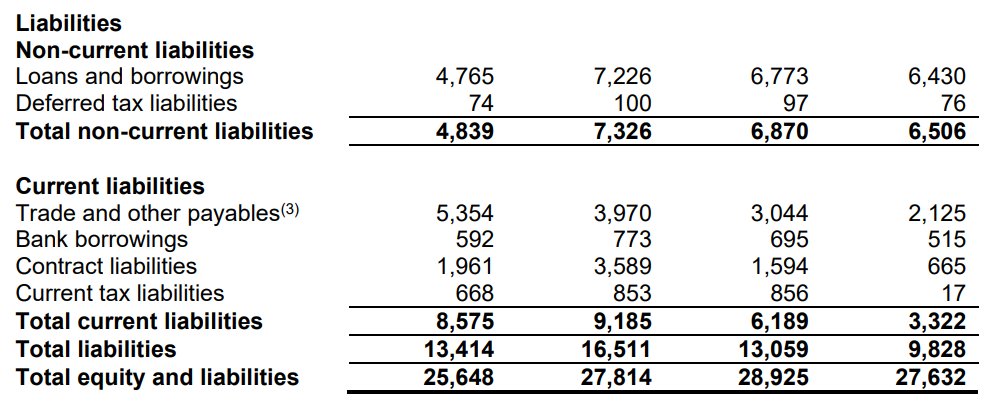

Revenue by Financial Year Ended

Profit After Tax (PAT) by Financial Year Ended

Revenue by Financial Period Ended

Profit After Tax (PAT) by Financial Period Ended

SWOT Analysis

Strengths

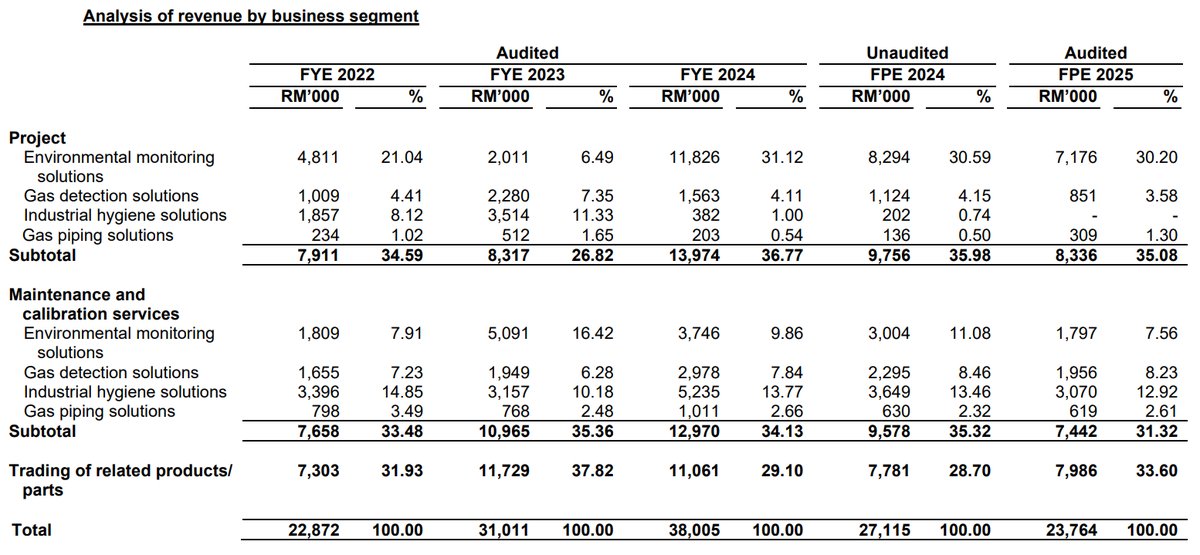

- Recurring Maintenance Revenue: Maintenance and calibration services contributed 34.13% of FYE 2024 revenue, providing a recurring income stream that buffers against the cyclical nature of project-based sales. This segment grew from RM7.66 million in FYE 2022 to RM12.97 million in FYE 2024.

- Integrated Solutions Capability: Unlike pure trading companies, the Group has in-house engineering design and system integration capabilities (28 engineers/technicians). This allows for customised environmental monitoring systems (CEMS) and gas piping solutions, fetching better margins (GP Margin ~33% vs Trading ~22%).

- Accredited Calibration Laboratory: Operates an ISO/IEC 17025 accredited laboratory for gas, acoustic, and temperature calibration. This accreditation is a high barrier to entry and essential for customers to meet regulatory compliance (DOE/DOSH), fostering customer stickiness.

Weaknesses

- Financial Performance Dip: Despite growth from FYE 2022-2024, revenue dropped by 12.4% in FPE 2025 (RM23.76m) compared to FPE 2024 (RM27.12m). Adjusted PAT for FPE 2025 also fell by 21.3%, indicating potential headwinds or project lumpiness immediately prior to IPO.

- High Valuation Premium: At an IPO price of RM0.25, the Hybrid PE stands at 26.16x. This is significantly higher than direct peer Progressive Impact Corp (PICORP) which trades at ~7-10x forward PE (based on recent profit recovery) and engineering peer AWC Berhad (~9.5x).

- Lack of Orderbook: The Group explicitly states it 'does not maintain an order book' as sales are based on purchase orders. This provides low earnings visibility compared to engineering peers like AWC or Favelle Favco who typically disclose substantial order books.

Opportunities

- Emission Control Expansion: Moving from monitoring (CEMS) to mitigation (Emission Control Solutions like scrubbers/filters) expands the total addressable market. This aligns with Malaysia's NIMP 2030 and stricter DOE enforcement on industrial emissions.

- Regional Office Expansion: Plans to set up branches and calibration labs in Johor, Terengganu, and Penang (allocated RM4.89m of proceeds). This captures the petrochemical hubs (Pengerang/Kerteh) and semiconductor cluster (Penang) more effectively by reducing service lead times.

- ESG Compliance Mandates: Increasing ESG reporting requirements for PLCs on Bursa Malaysia drive demand for continuous environmental monitoring data, benefiting the core CEMS business.

Threats

- Foreign Exchange Volatility: 60-66% of purchases are denominated in foreign currencies (EUR, GBP, USD), while 99% of revenue is in Ringgit Malaysia. Strengthening foreign currencies can severely compress margins, as seen in the fluctuated costs during the Financial Periods Under Review.

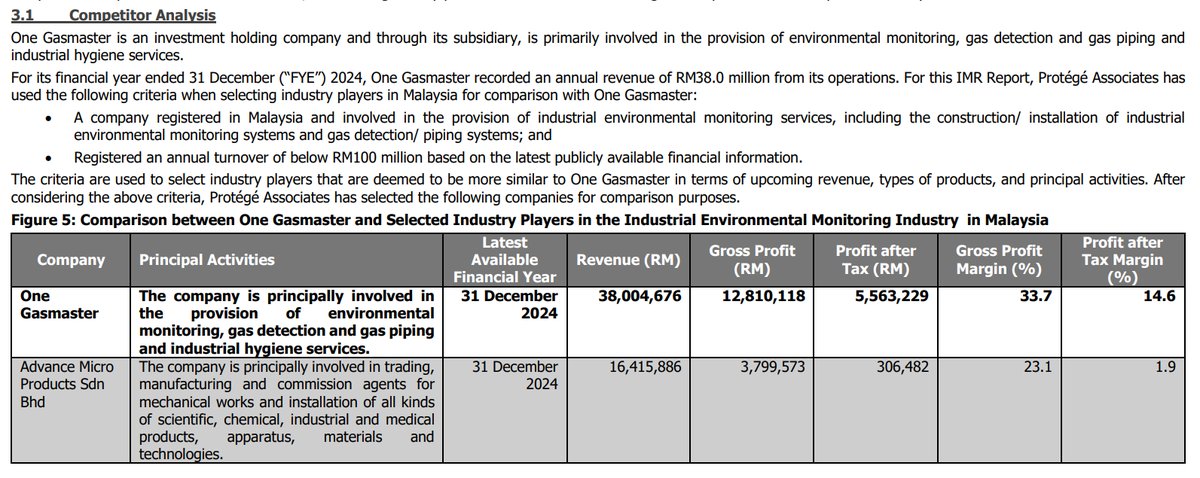

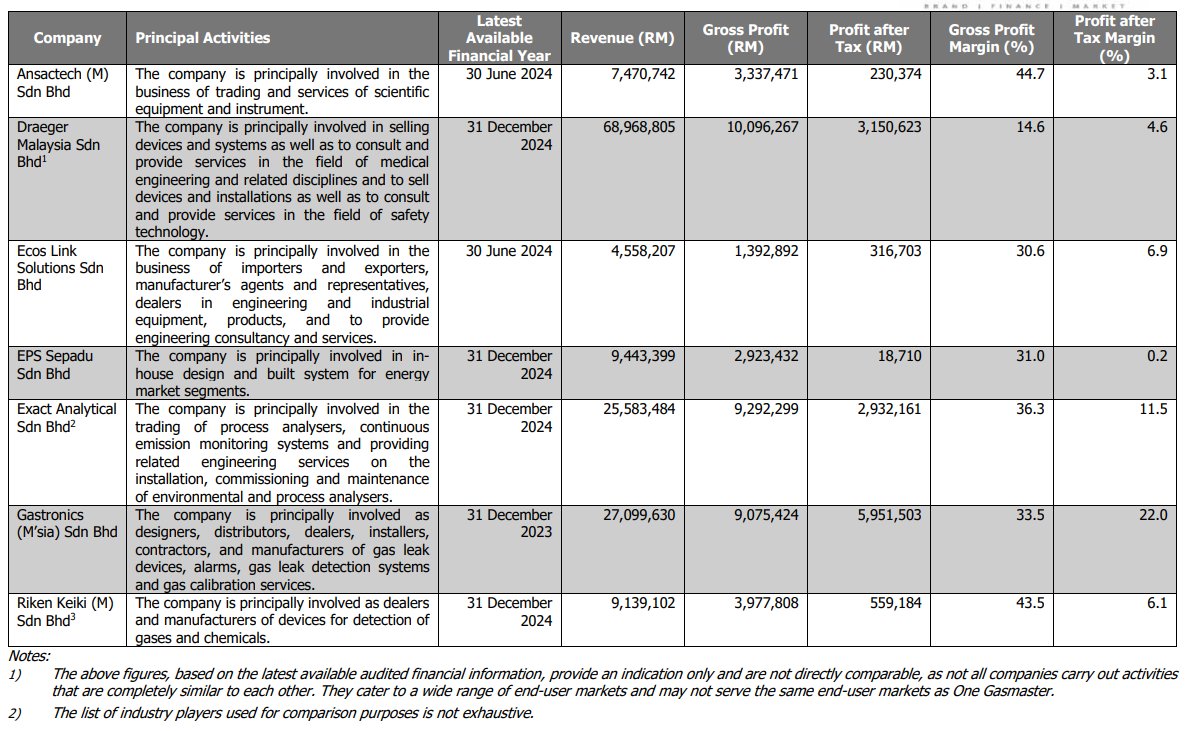

- Intense Competition: Competes with larger players like Exact Analytical (subsidiary of Favelle Favco) which reported ~RM69m revenue, nearly double OGM's size. Global brands like Draeger also have direct presence, potentially squeezing market share.

- Regulatory Dependency: Operations are heavily dependent on licenses from DOE and Energy Commission. Any revocation or non-renewal of the CEMS consultant registration or Class A Gas Contractor license would halt core business activities.

Key Highlights

Sorry, this feature only available for iSaham Pro

Conclusion

Sorry, this feature only available for iSaham Pro

One Gasmaster Holdings Berhad's Latest News