ISF Group Berhad IPO's Analysis

ISF Group Berhad

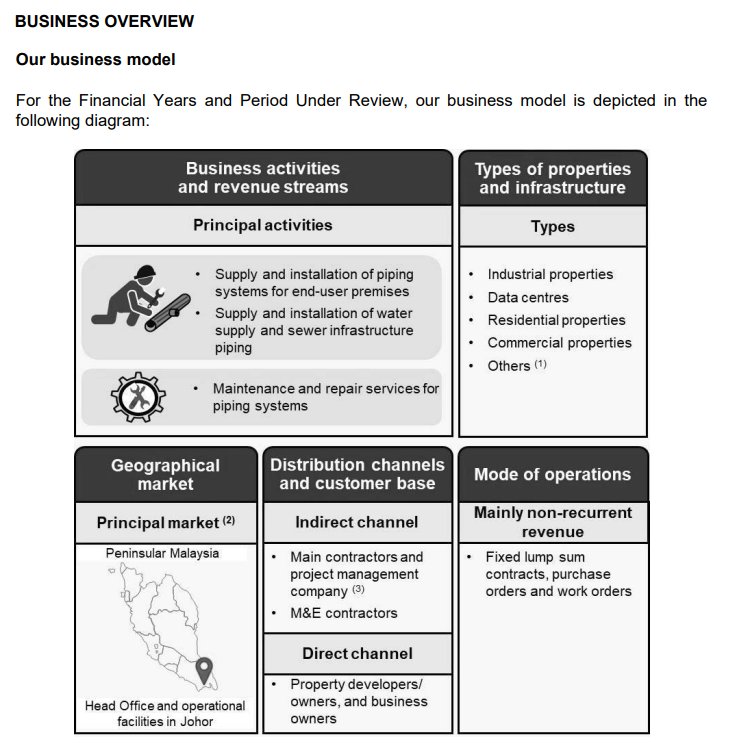

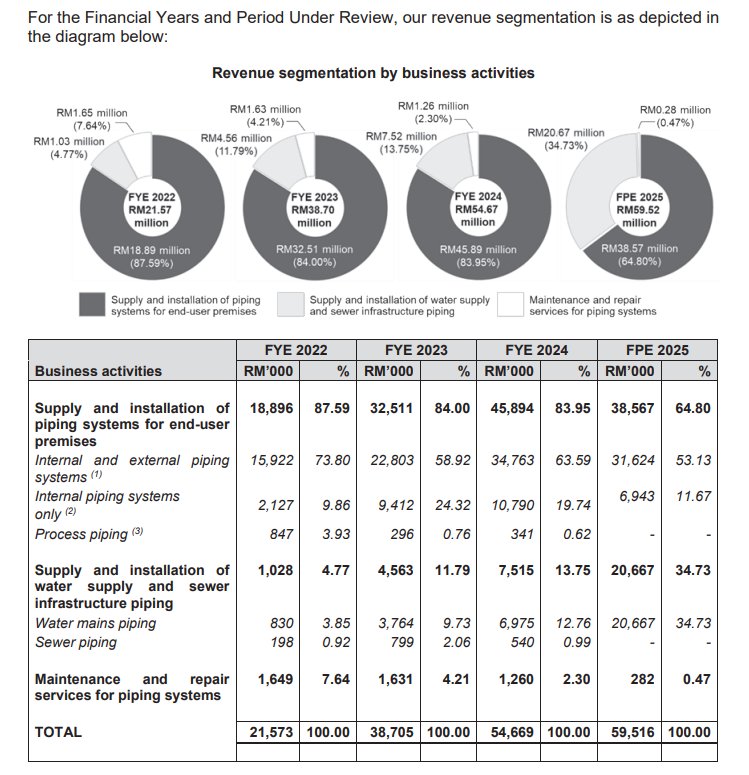

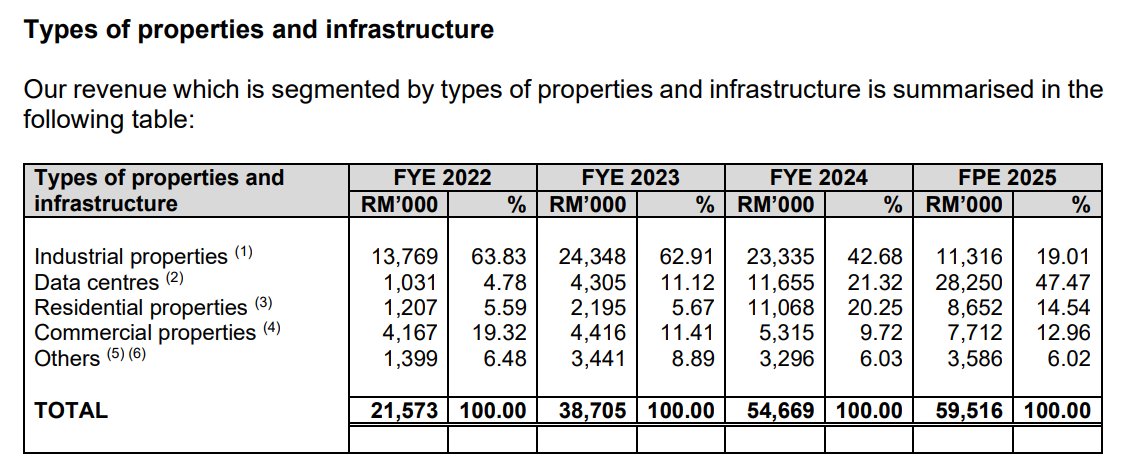

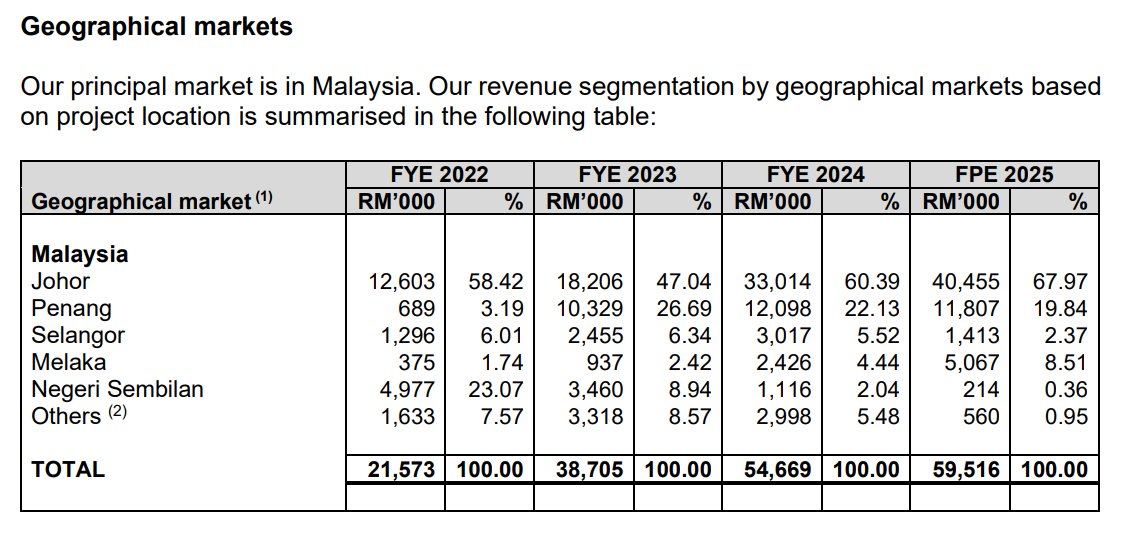

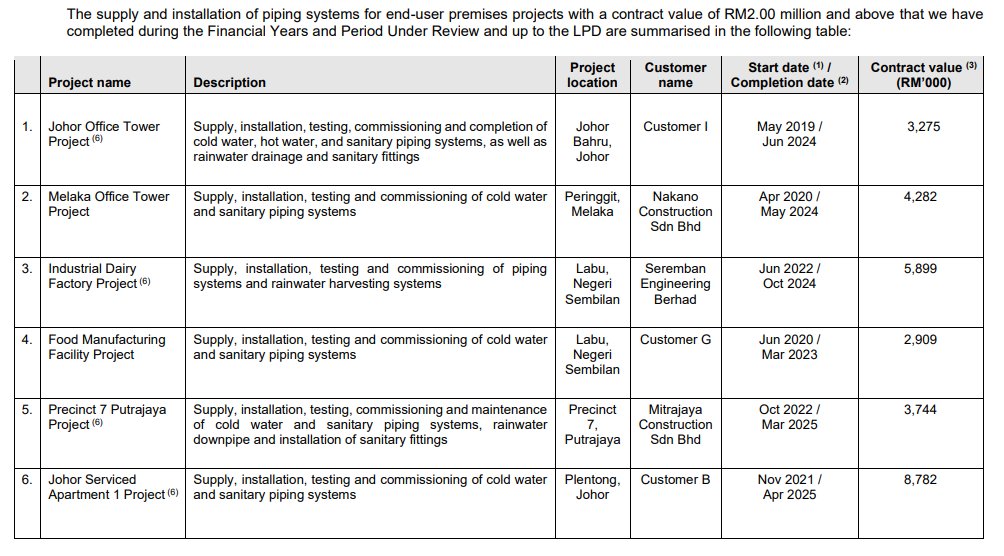

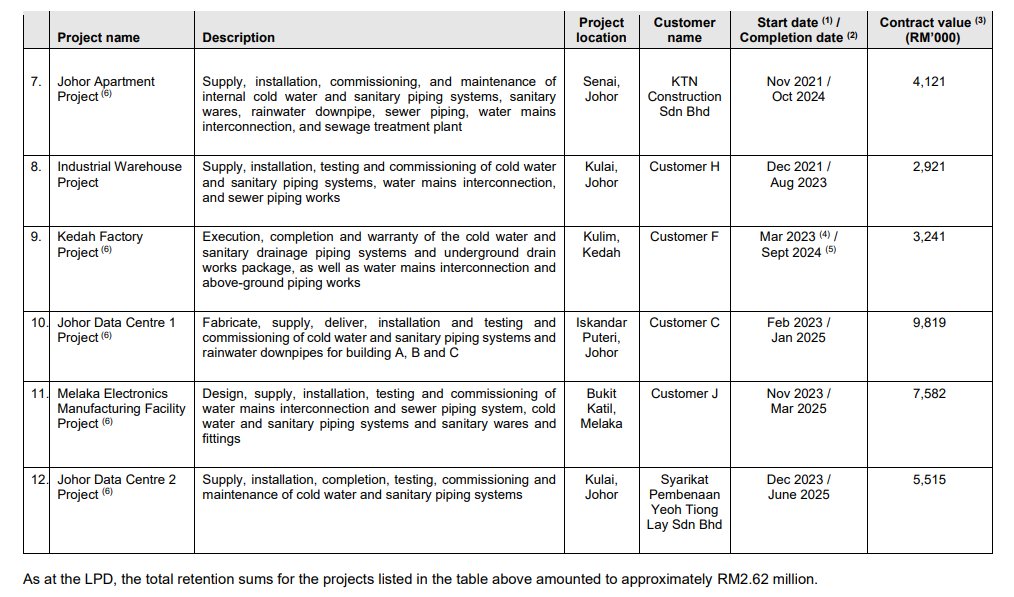

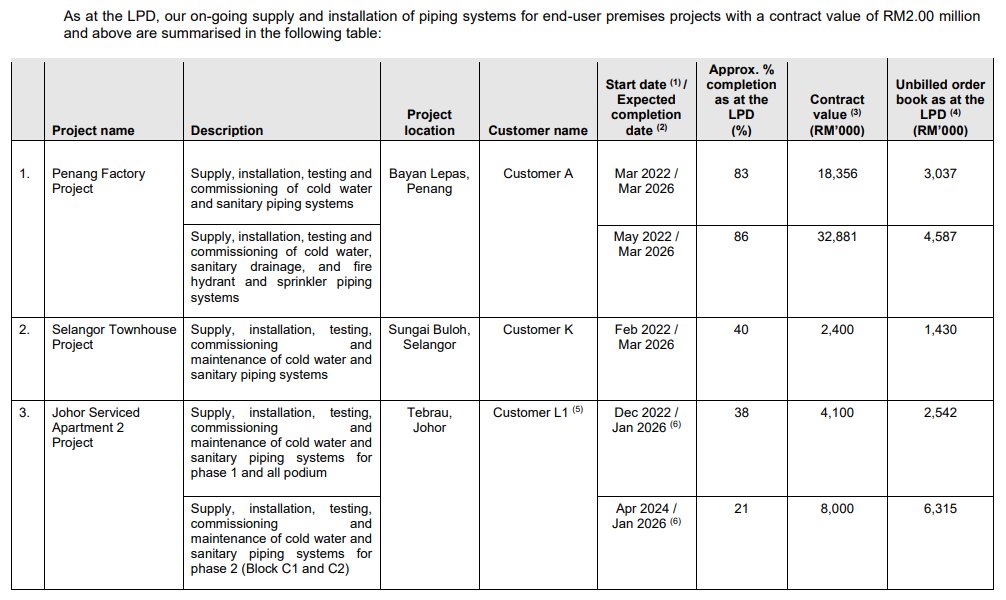

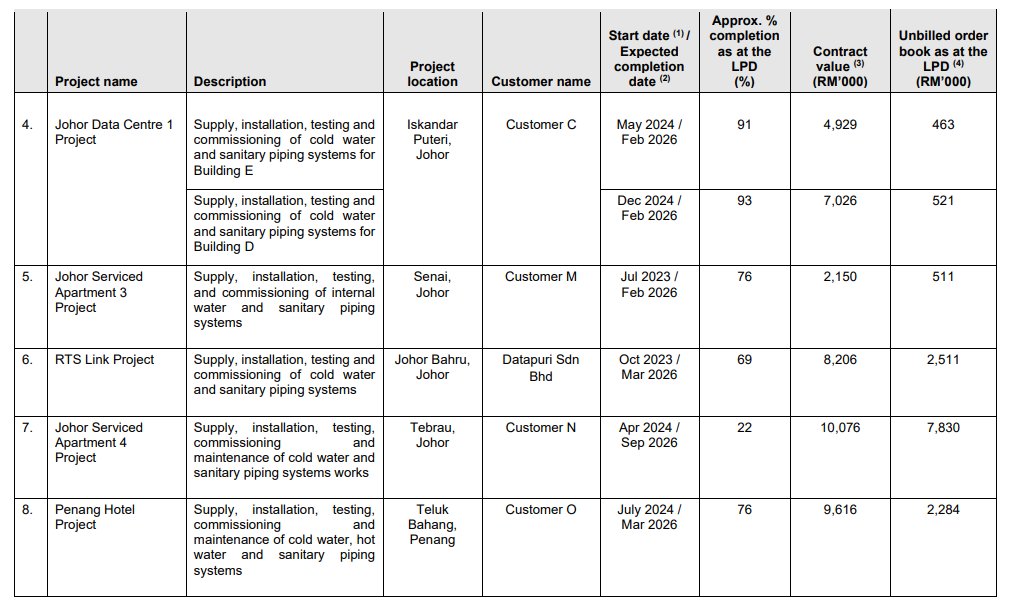

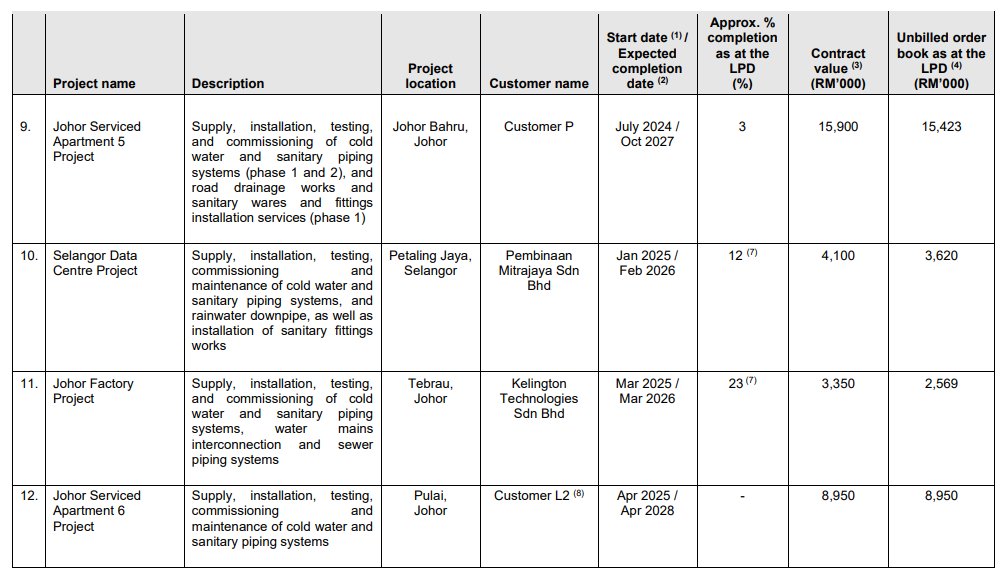

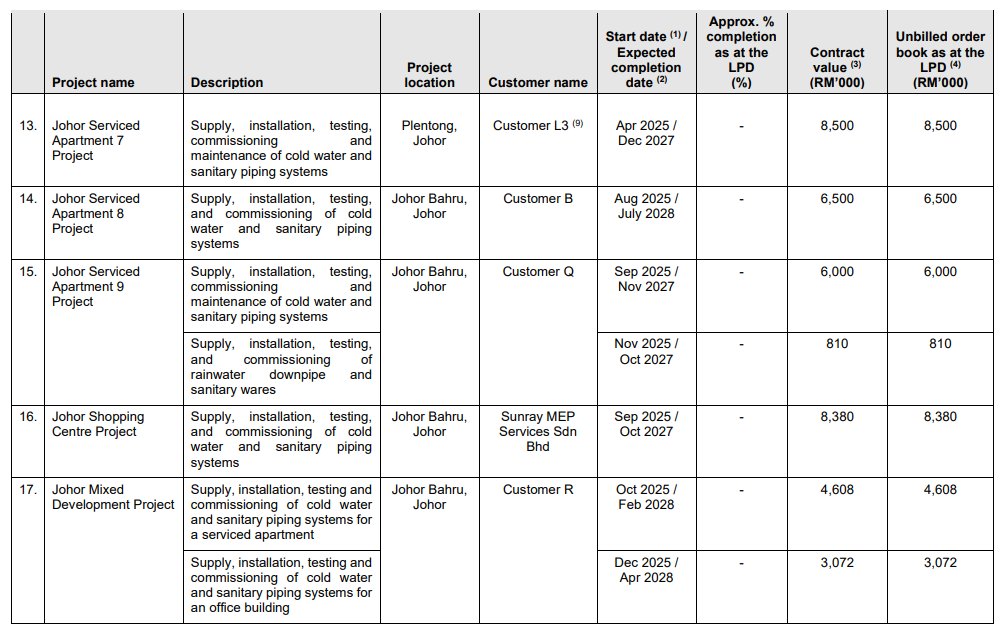

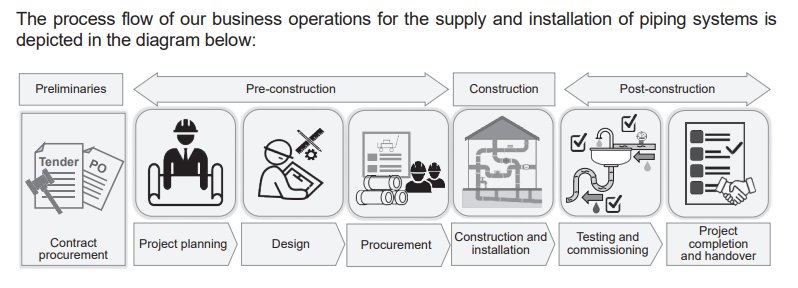

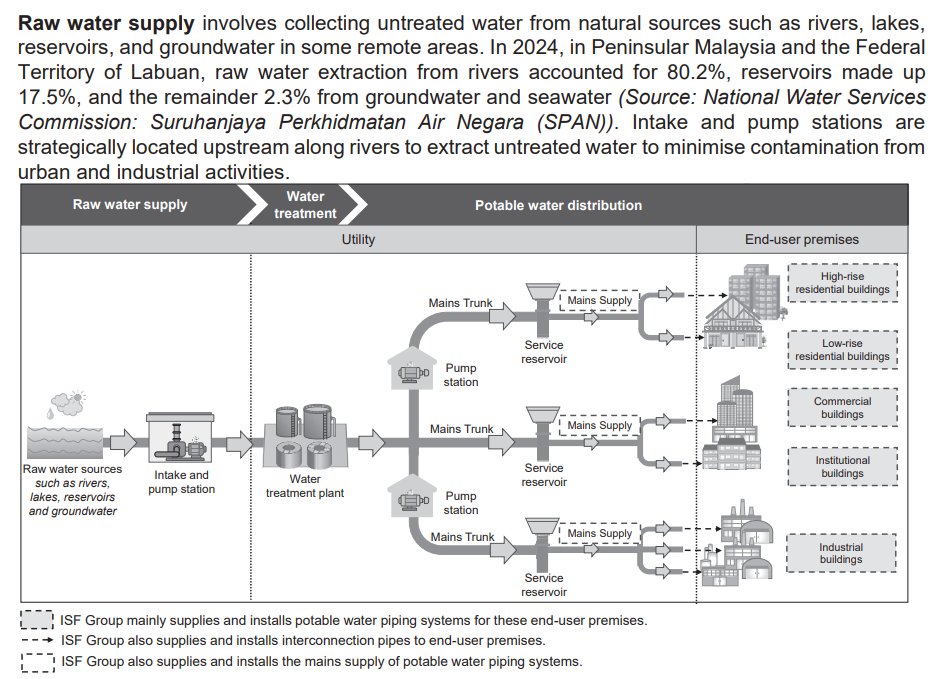

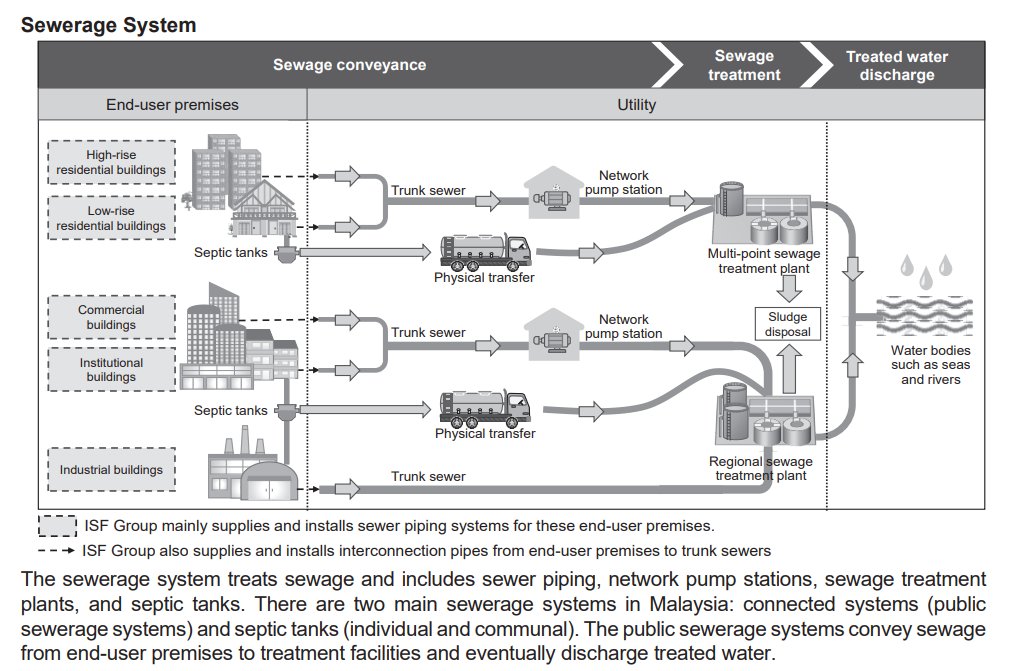

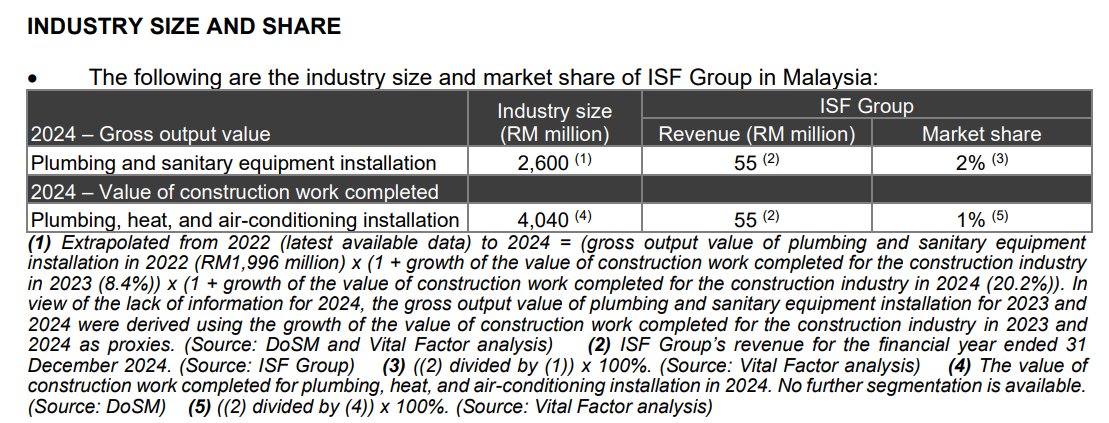

ISF Group Berhad, through its subsidiary Yeo Plumber Sdn Bhd, is primarily involved in the supply and installation of piping systems for end-user premises, as well as water supply and sewer infrastructure piping. The company also provides maintenance and repair services for these systems. Its operations cover a wide range of properties and infrastructure, including industrial facilities, data centres, residential and commercial buildings, and public infrastructure like power plants and mass transit facilities. The Group serves customers across Peninsular Malaysia, with a significant presence in Johor, and utilizes both direct and indirect distribution channels to secure projects from main contractors, project management companies, property developers, and business owners.

IPO Details

Strategic Overview & Data Visuals

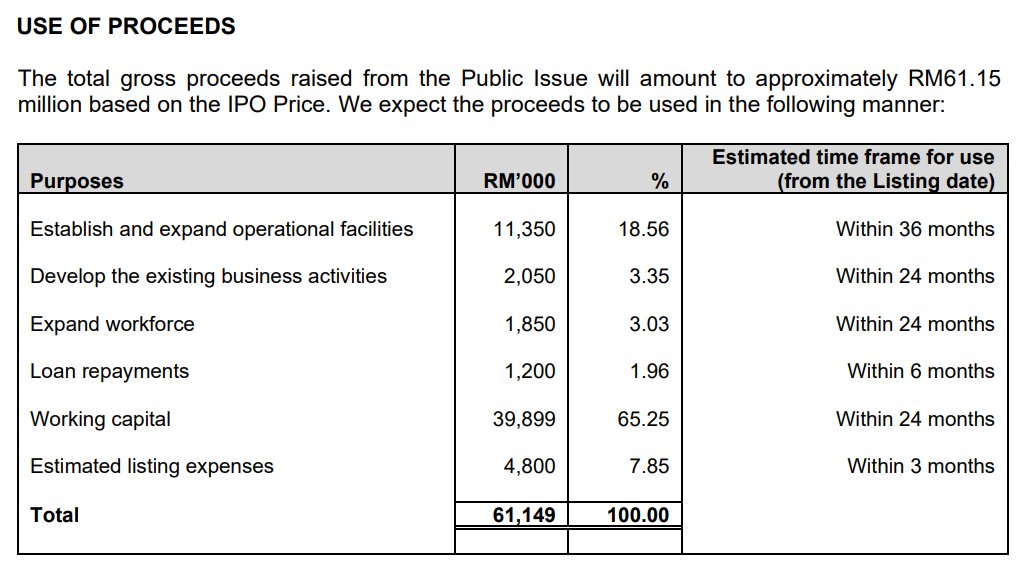

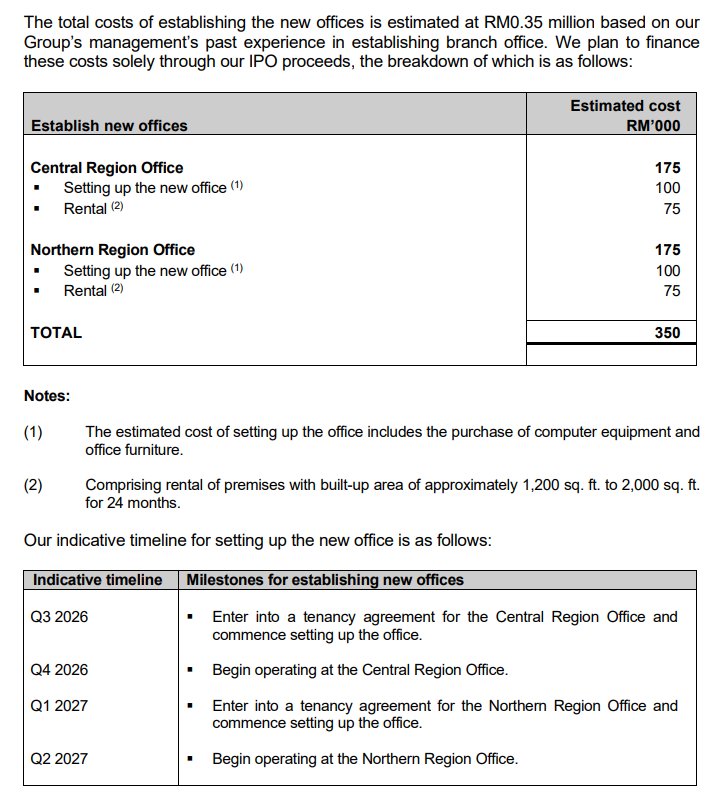

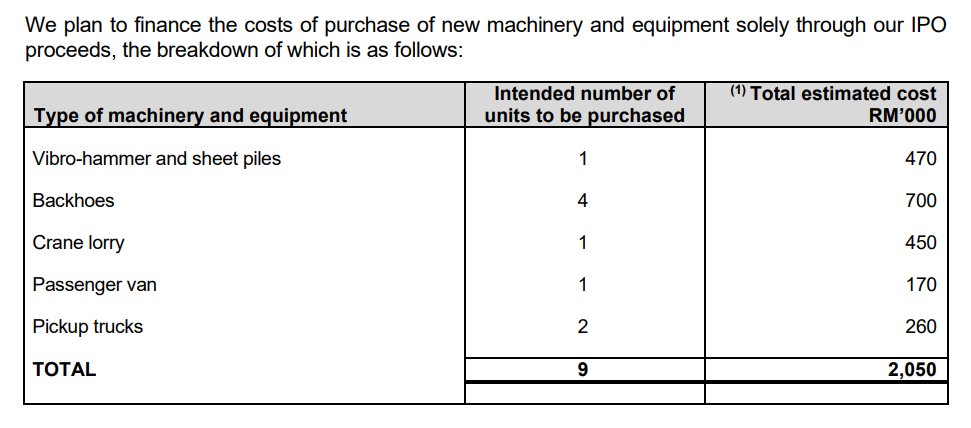

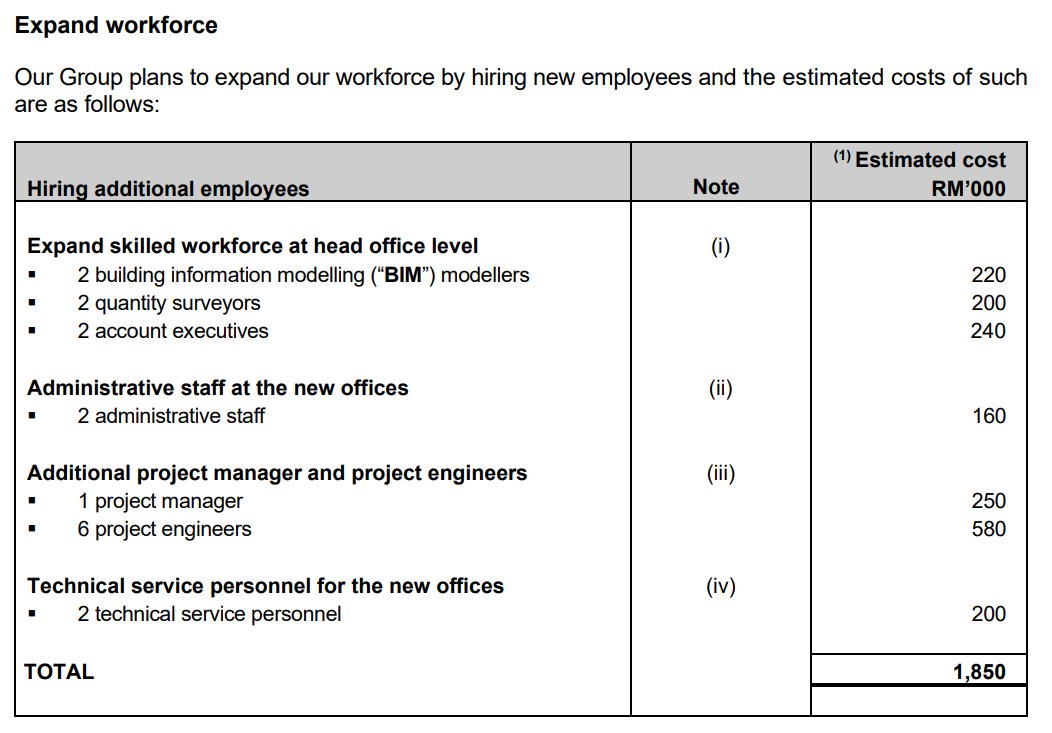

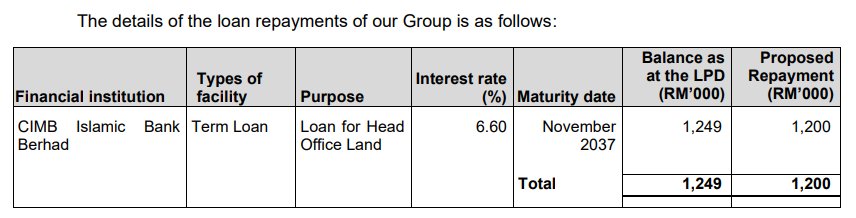

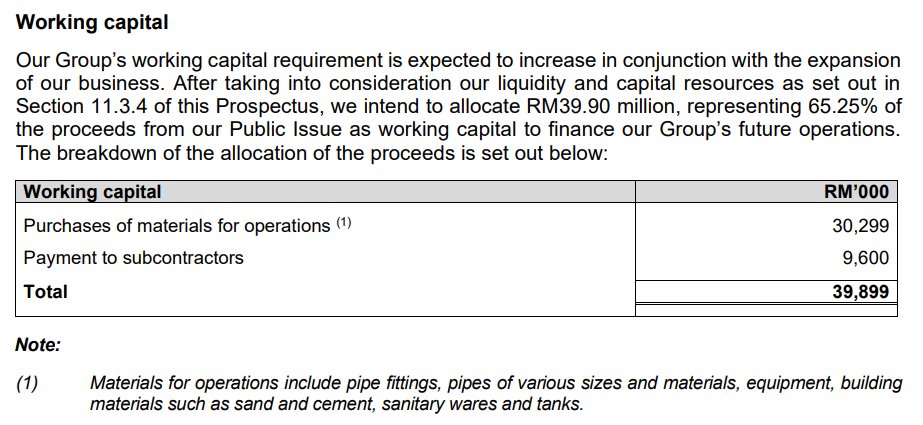

Utilisation of Proceeds

| Purpose | Amount (RM'000) | % | |

|---|---|---|---|

| Expansion | Establish and expand operational facilities | 11,350 | 18.56 |

| Expansion | Develop the existing business activities | 2,050 | 3.35 |

| Expansion | Expand workforce | 1,850 | 3.03 |

| Working capital | Working capital | 39,899 | 65.25 |

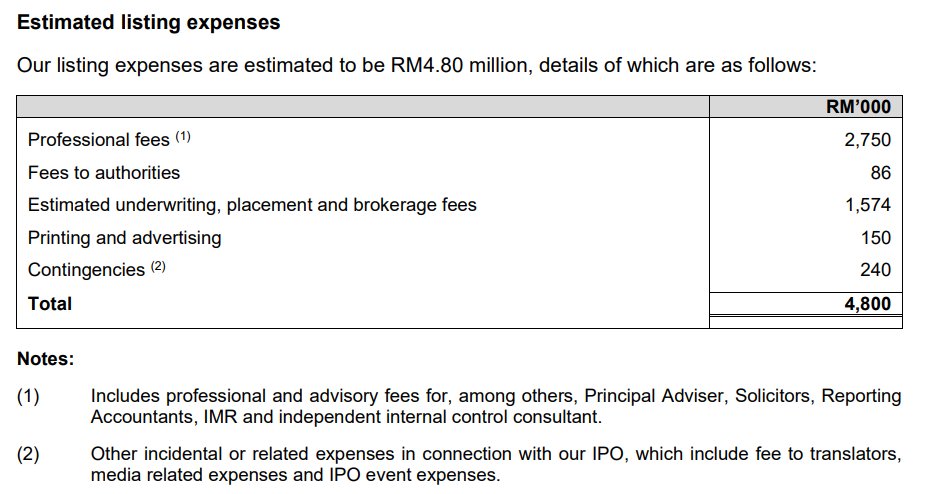

| Listing expenses | Estimated listing expenses | 4,800 | 7.85 |

| Debt | Loan repayments | 1,200 | 1.96 |

| Total | 61,149 | 100 | |

Analyst Highlights

| Date | Analyst Highlights |

|---|---|

|

04-Mar-2026

Apex |

|

|

26-Feb-2026

Apex |

|

|

16-Feb-2026

Apex |

|

|

27-Jan-2026

Apex |

|

|

14-Jan-2026

RHB |

|

|

14-Jan-2026

Public Invest |

|

|

13-Jan-2026

Mplus |

|

|

13-Jan-2026

Apex |

|

|

13-Jan-2026

TradeView |

|

|

12-Jan-2026

TA |

|

Utilisation of Proceeds

Business Segments

Geographical Segments

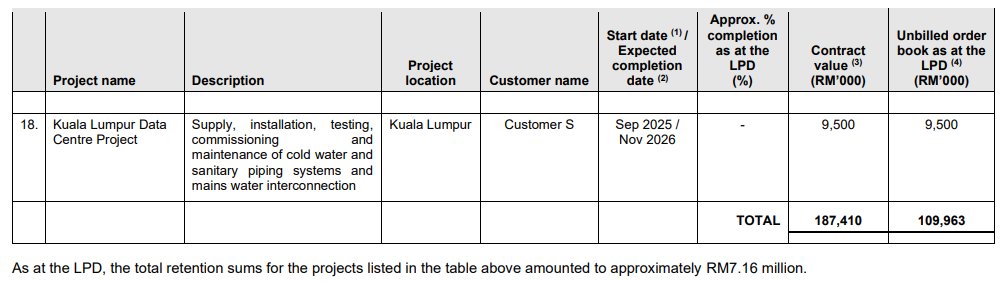

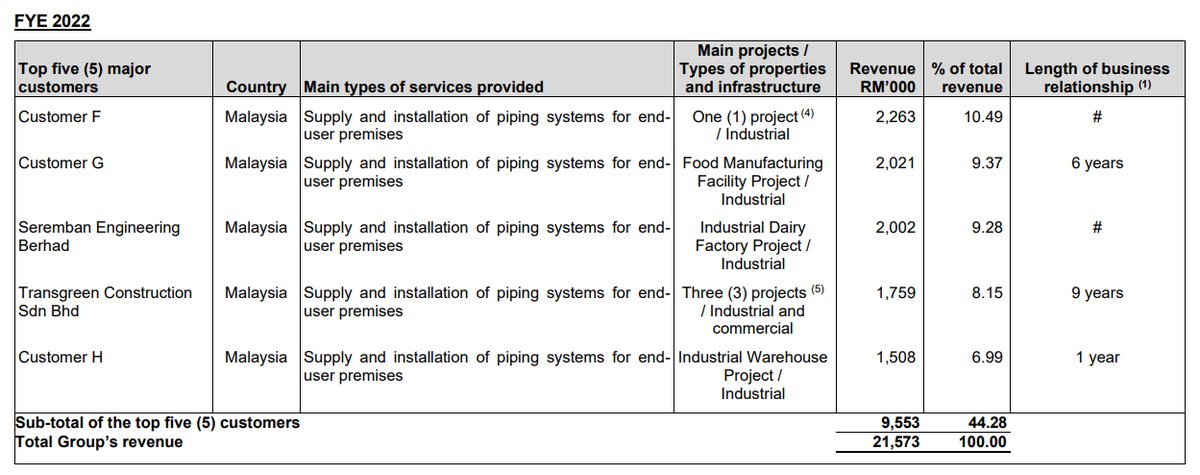

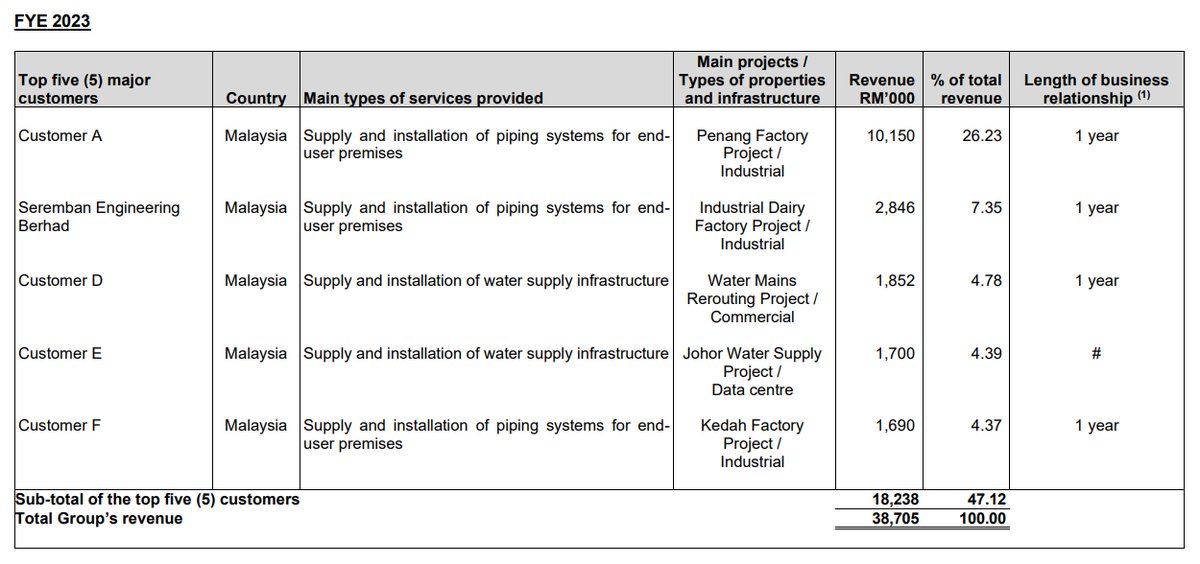

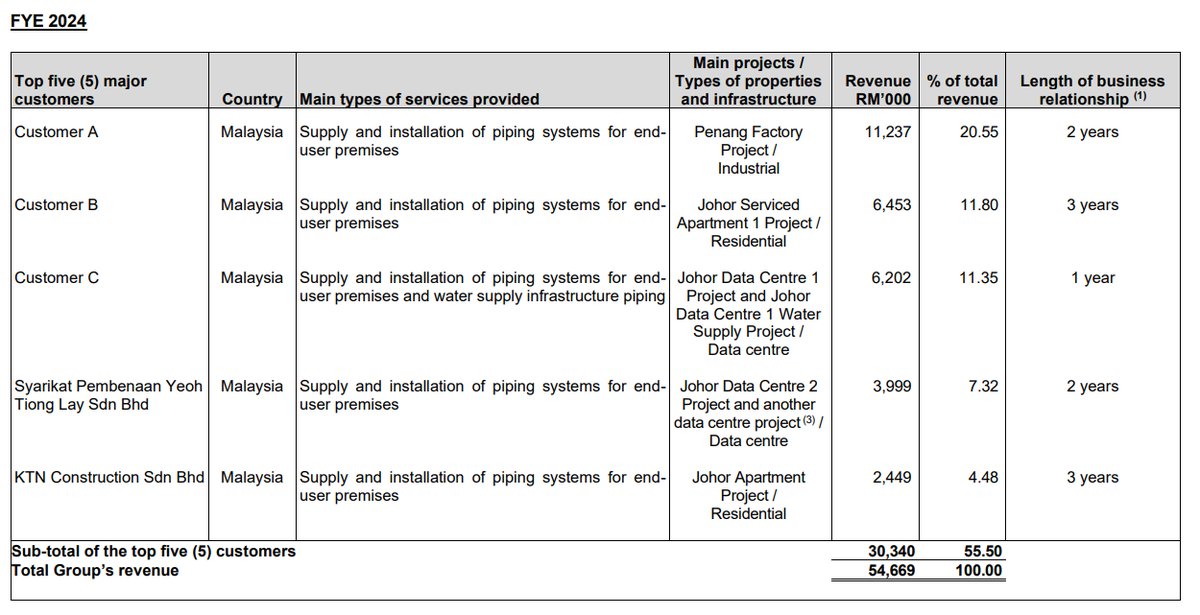

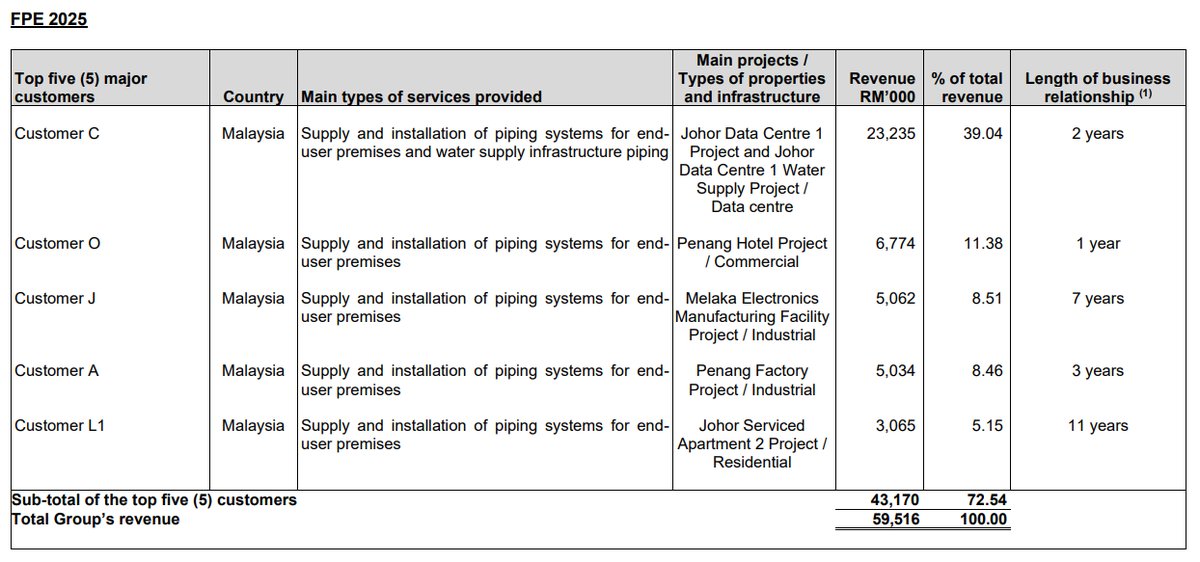

Major Customers

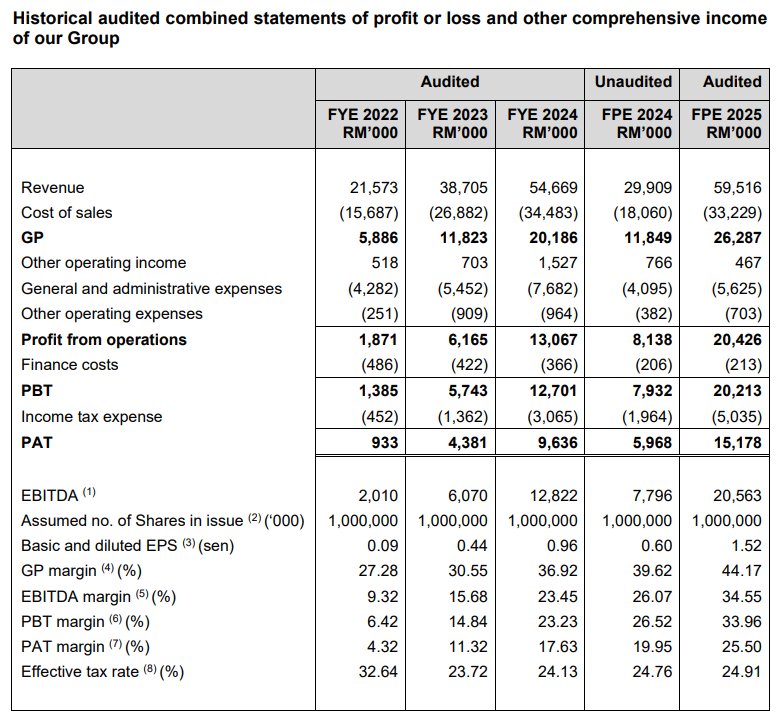

Revenue by Financial Year Ended

Profit After Tax (PAT) by Financial Year Ended

Revenue by Financial Period Ended

Profit After Tax (PAT) by Financial Period Ended

SWOT Analysis

Strengths

- Explosive Revenue Growth: Revenue surged by 99.0% in FPE 2025, primarily driven by high-value Data Centre projects, showcasing strong demand for its services.

- Superior Profit Margins: Achieved a Profit After Tax (PAT) margin of 25.5% in FPE 2025, significantly outperforming direct peers like Critical Holdings Berhad (8.6%).

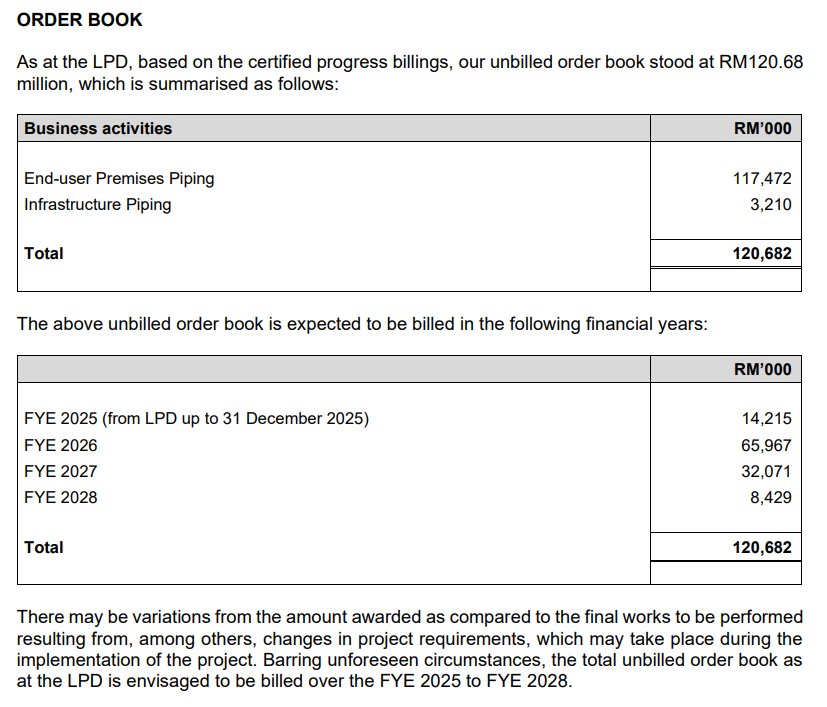

- Strong Earnings Visibility: Possesses a robust unbilled order book of RM120.68 million, which is 2.2 times its FYE2024 revenue, securing income streams through 2028.

Weaknesses

- High Working Capital Needs: Operations are cash-intensive, with 65.3% of IPO proceeds allocated to working capital rather than asset expansion, indicating potential cash flow pressures.

- Significant Customer Concentration: Highly dependent on a small number of clients, with its top 5 customers accounting for 72.5% of revenue and a single Data Centre customer contributing 39.0%.

Opportunities

- Data Centre Boom: Positioned to benefit from Malaysia's emergence as a major Data Centre hub, with significant investments from tech giants like Microsoft and ByteDance driving demand for its specialized piping services.

- National Infrastructure Projects: Government initiatives, such as water infrastructure upgrades and affordable housing projects outlined in Budget 2025, create sustained demand for its core piping system services.

Threats

- Raw Material Volatility: Profitability is exposed to price fluctuations of key raw materials like steel, copper, and PVC pipes, which constitute approximately 48% of its cost of sales.

- Foreign Labour Reliance: High dependency on foreign workers, who make up 68% of its workforce, makes operations vulnerable to changes in immigration policies, levy hikes, and potential labour shortages.

- Geographical Dependence: Operations are heavily concentrated in Johor, which contributed 68.0% of FPE 2025 revenue, exposing the group to localized economic and project risks.

Key Highlights

Sorry, this feature only available for iSaham Pro

Conclusion

Sorry, this feature only available for iSaham Pro

ISF Group Berhad's Latest News