Hock Soon Capital Berhad IPO's Analysis

Hock Soon Capital Berhad

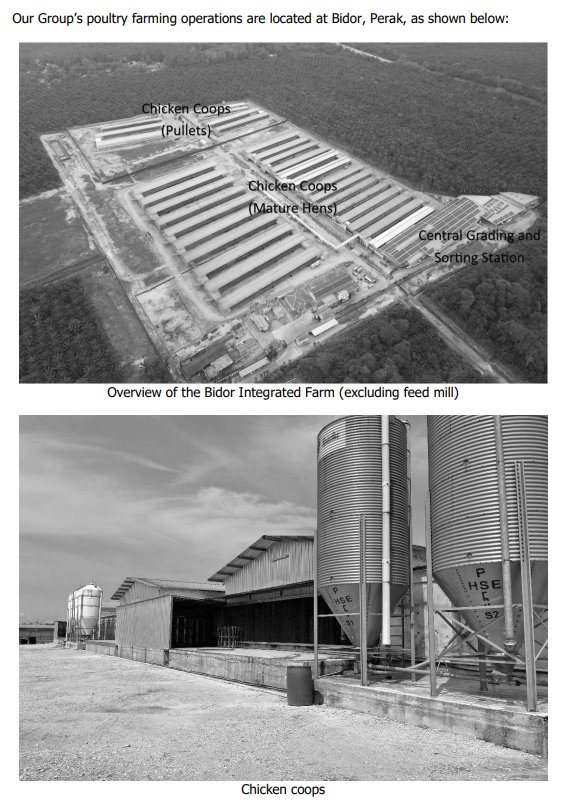

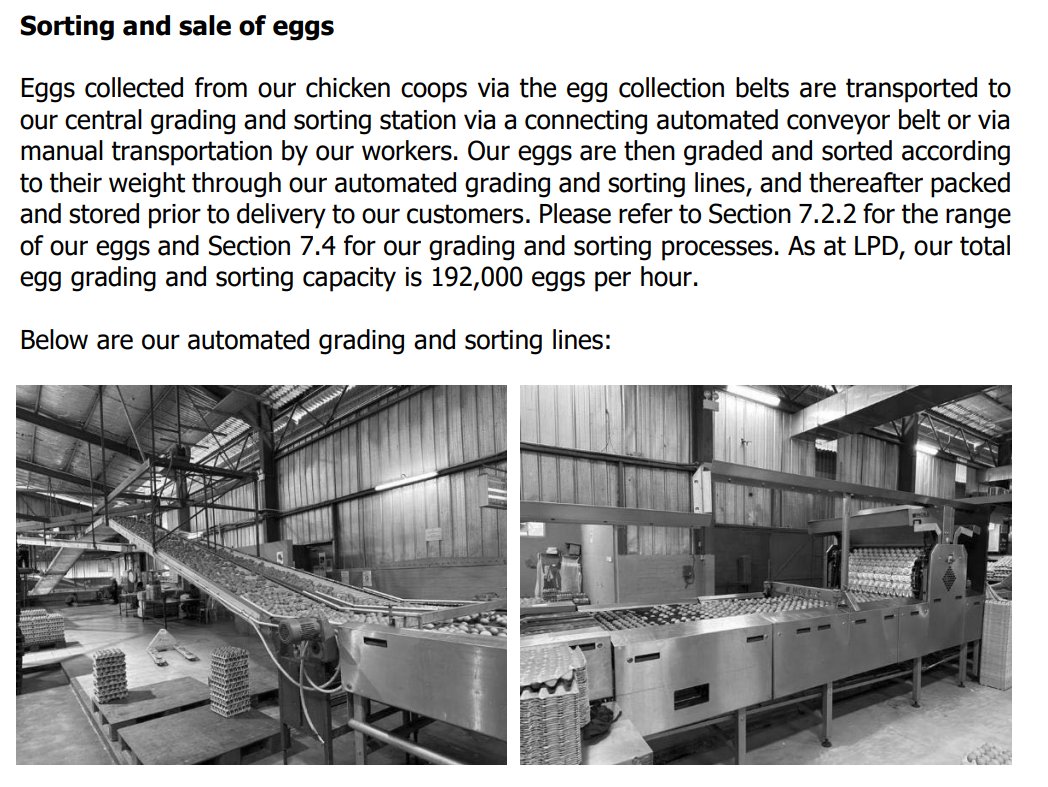

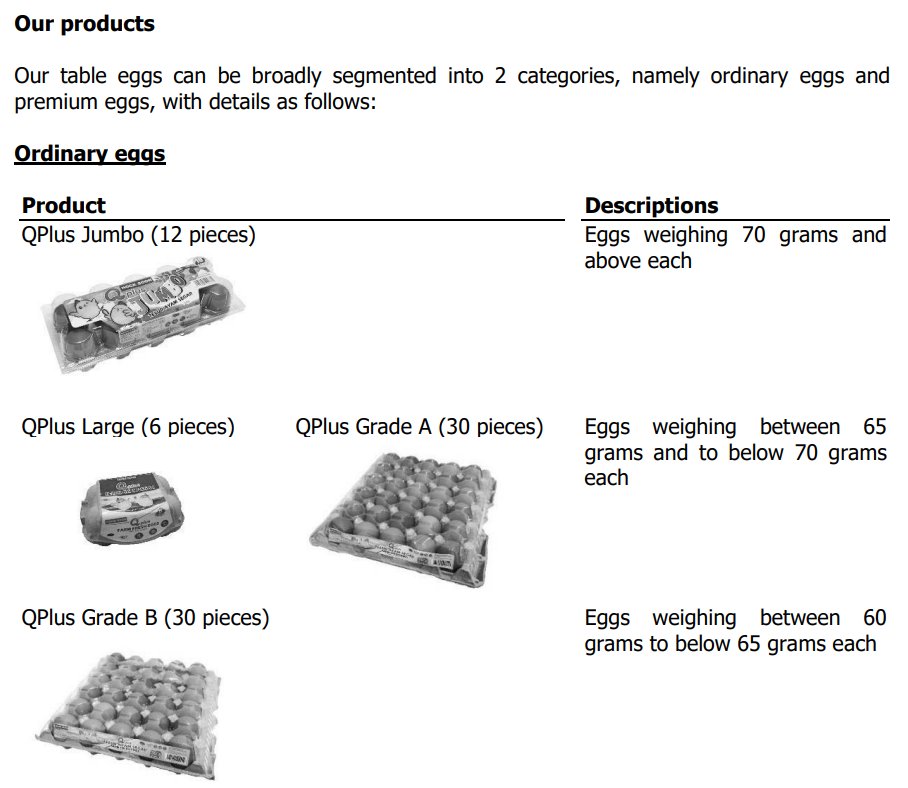

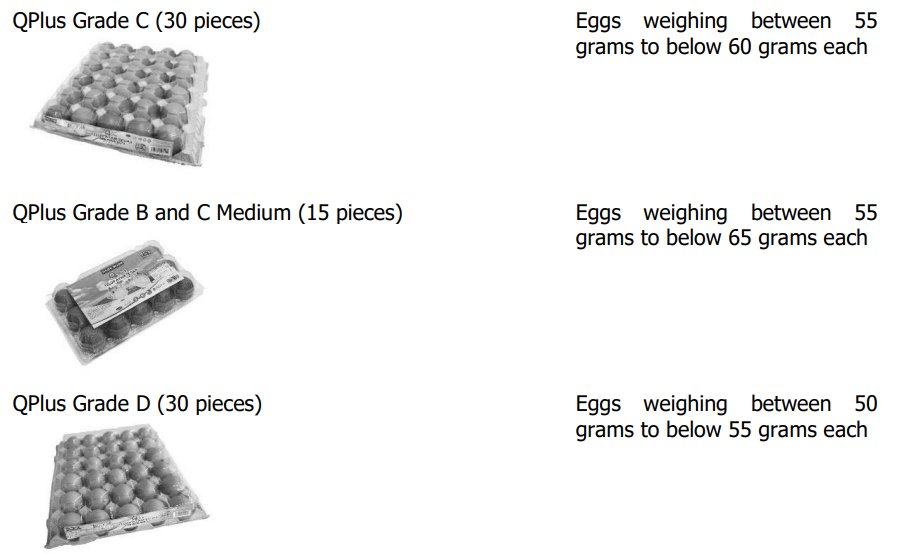

Hock Soon Capital Berhad, through its subsidiaries, is principally involved in the poultry farming industry, focusing on rearing layer chickens for the production and sale of table eggs. The Group operates a vertically integrated business model which includes in-house feed mill operations to produce its own poultry feed, ensuring quality control and cost efficiency. Its product range is categorized into ordinary eggs and premium eggs, with the latter being enriched with nutrients like Vitamin E, Omega DHA, and selenium. The eggs are sold both unbranded and under the Group's house-brand 'QPlus', and are also packaged under customers' brands upon request. The Group's operations are based in Bidor, Perak, at its Bidor Integrated Farm. The company serves a multi-channel distribution network that includes wholesalers, retailers (such as supermarkets and grocery stores), and food manufacturers primarily within Malaysia. Additionally, the Group exports a portion of its premium eggs to an overseas customer in Hong Kong.

IPO Details

Strategic Overview & Data Visuals

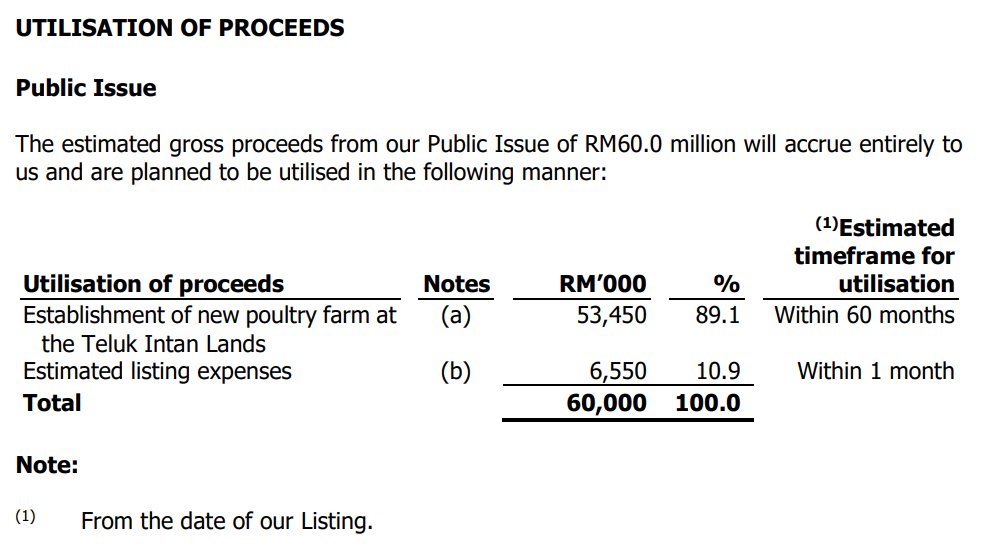

Utilisation of Proceeds

| Purpose | Amount (RM'000) | % | |

|---|---|---|---|

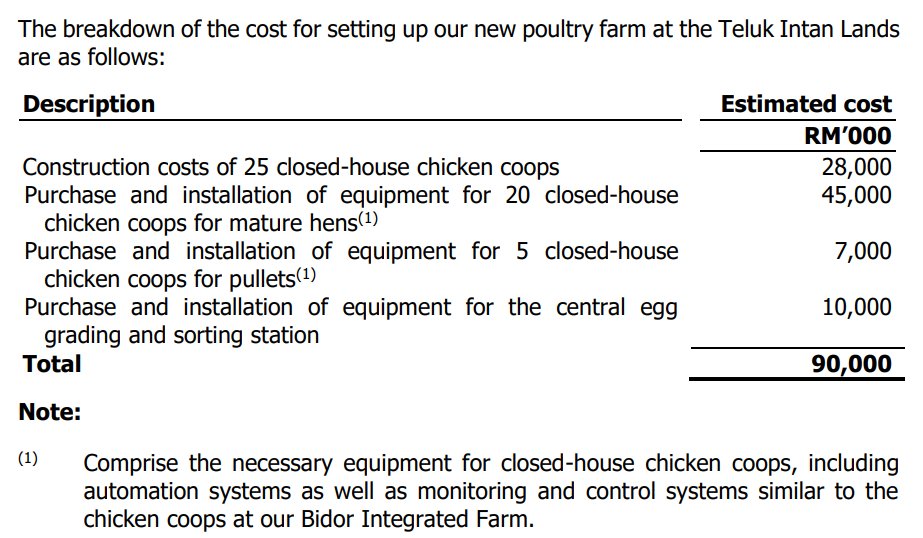

| Expansion | Establishment of new poultry farm at the Teluk Intan Lands | 53,450 | 89.1 |

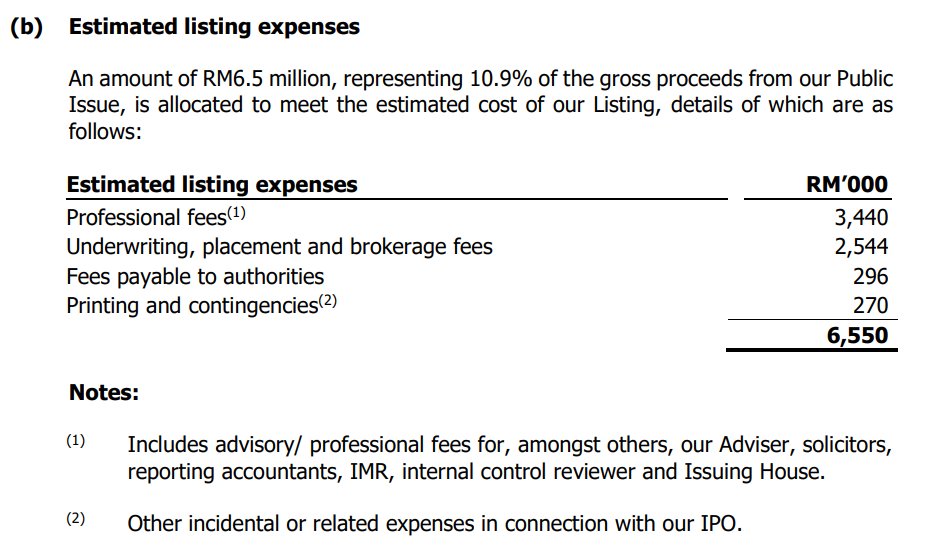

| Listing expenses | Estimated listing expenses | 6,550 | 10.9 |

| Total | 60,000 | 100 | |

Analyst Highlights

| Date | Analyst Highlights |

|---|---|

|

30-Jan-2026

Mplus |

|

|

29-Jan-2026

TA |

|

|

29-Jan-2026

RHB |

|

Utilisation of Proceeds

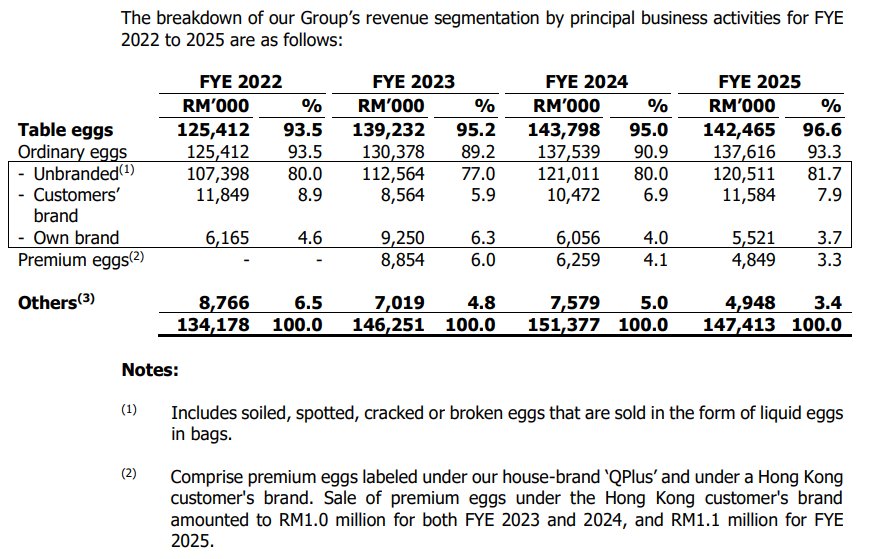

Business Segments

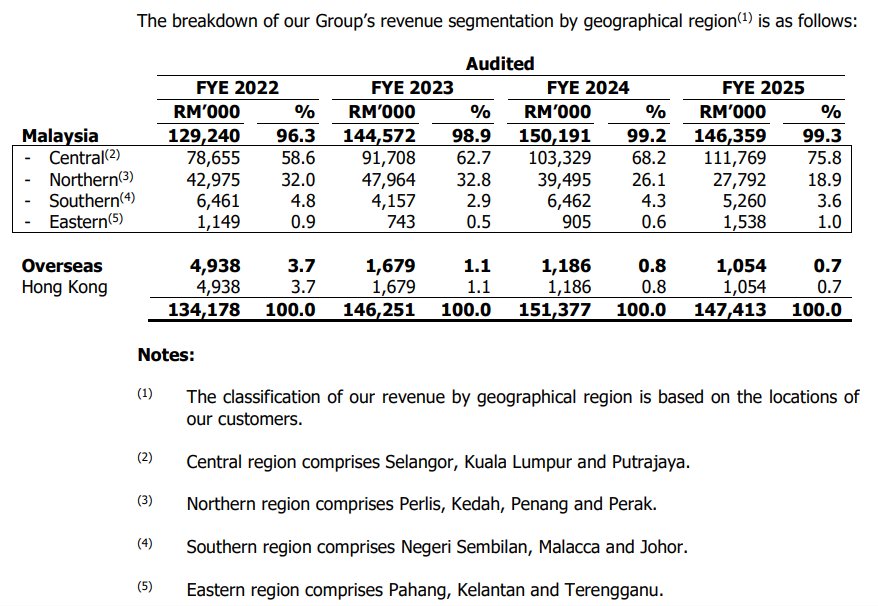

Geographical Segments

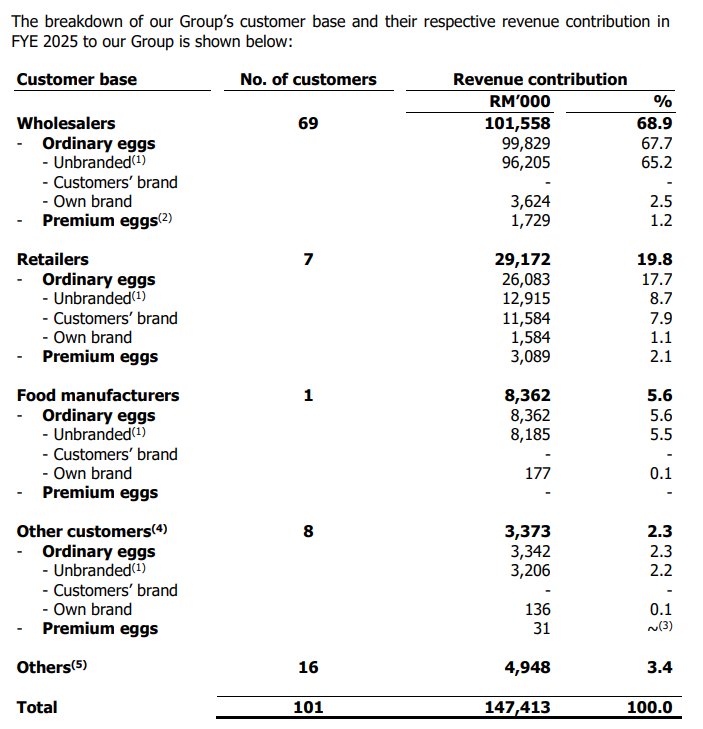

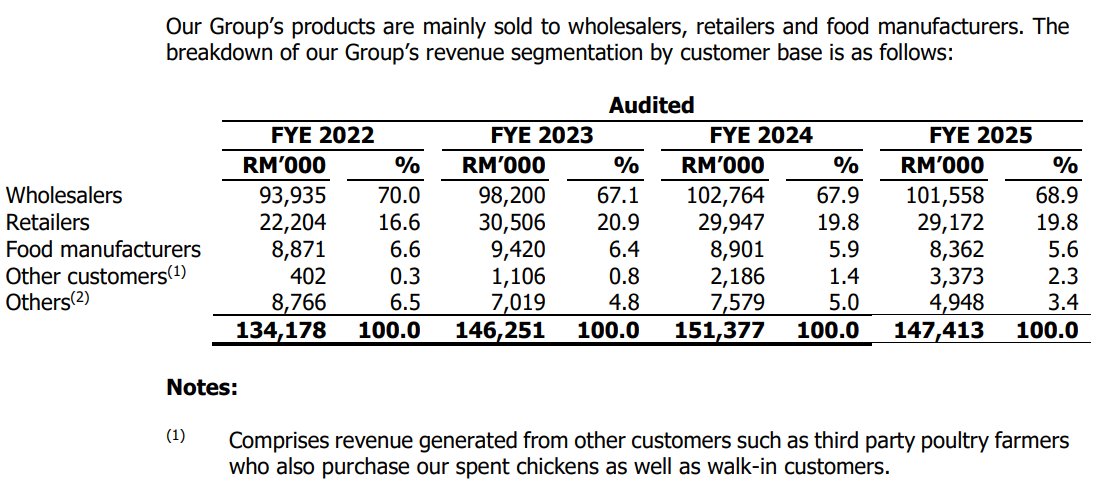

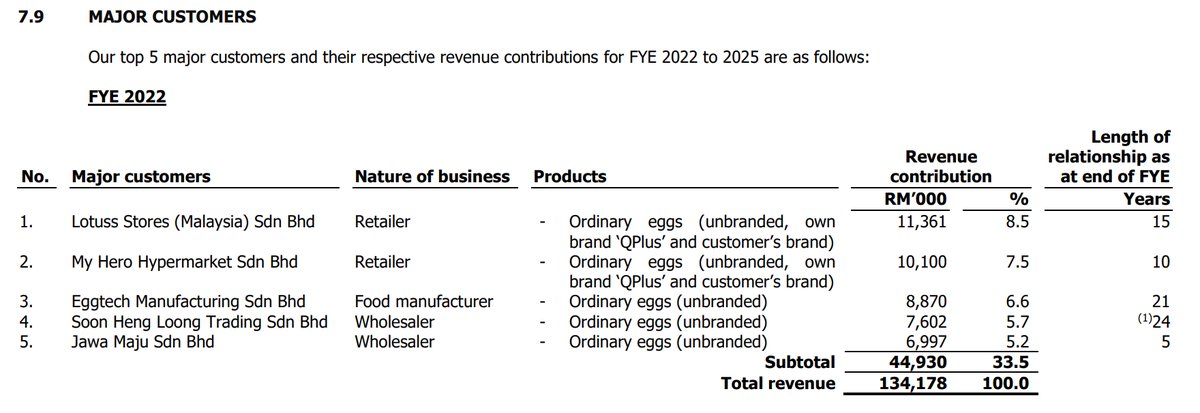

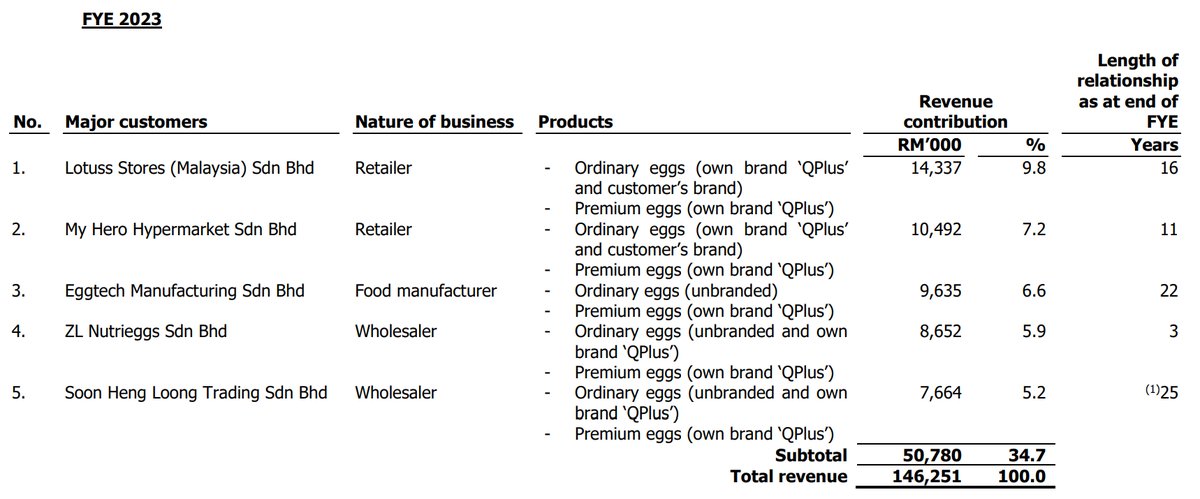

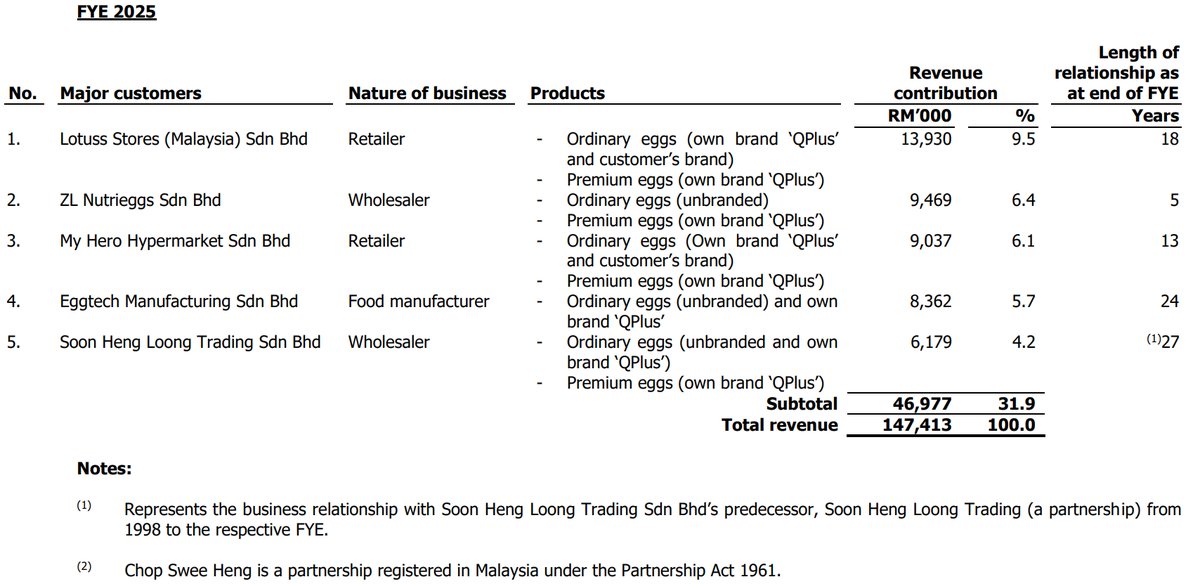

Major Customers

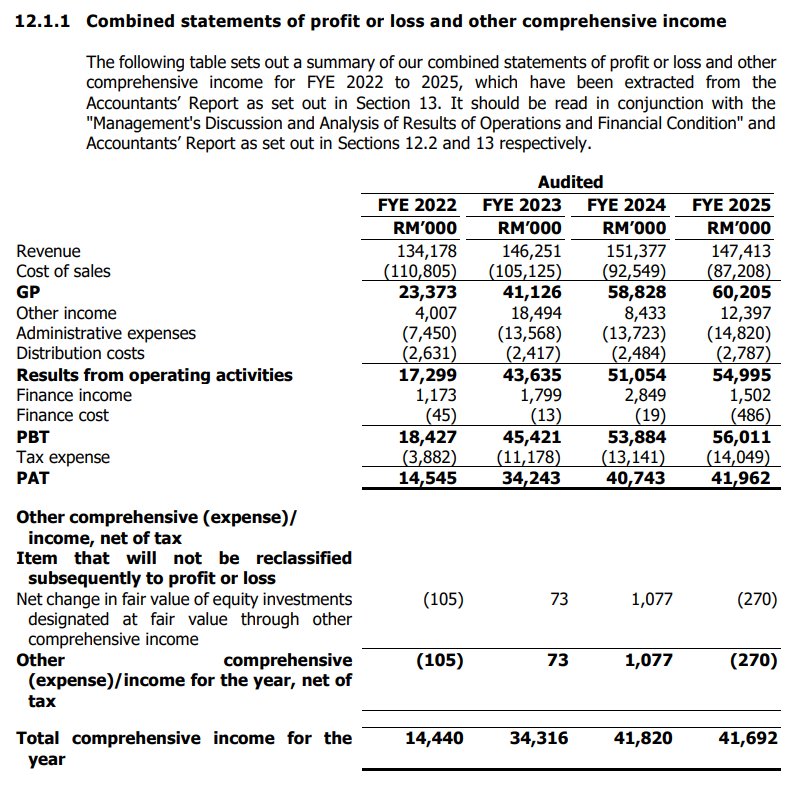

Revenue by Financial Year Ended

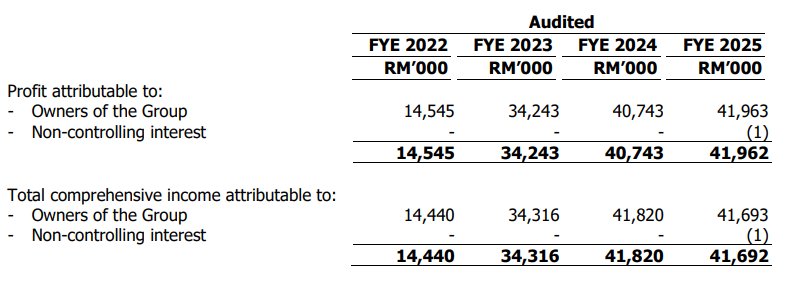

Profit After Tax (PAT) by Financial Year Ended

SWOT Analysis

Strengths

- Integrated Operations: In-house feed mill provides control over feed quality and costs, which is crucial for managing operational efficiency and margins in the poultry business.

- Automated Facilities: Operates 100% closed-house systems with automation for feeding, egg collection, and grading, which minimizes labor costs and reduces biosecurity risks.

- Established Brand: The 'QPlus' premium egg brand is sold in major retailers like Lotus’s and Jaya Grocer, potentially commanding higher margins than generic eggs.

- Low Customer Concentration: The top 5 customers account for only 31.9% of revenue, indicating a well-diversified customer base and low dependency risk on any single client.

Weaknesses

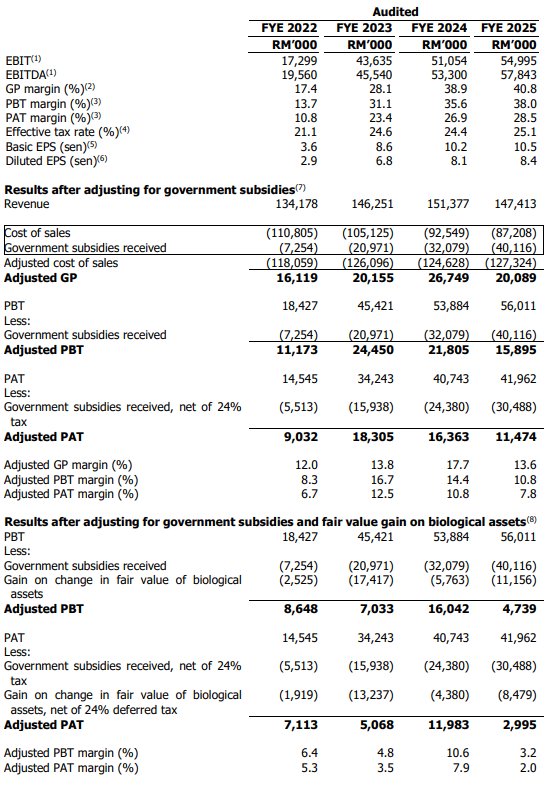

- Thin Core Margins: Excluding government subsidies and non-cash fair value gains, the core net profit margin is extremely thin at approximately 2%, showing high sensitivity to operational costs.

Opportunities

- Singapore Export Potential: A pending export license to Singapore could open a lucrative new market with stronger currency earnings and potentially higher selling prices.

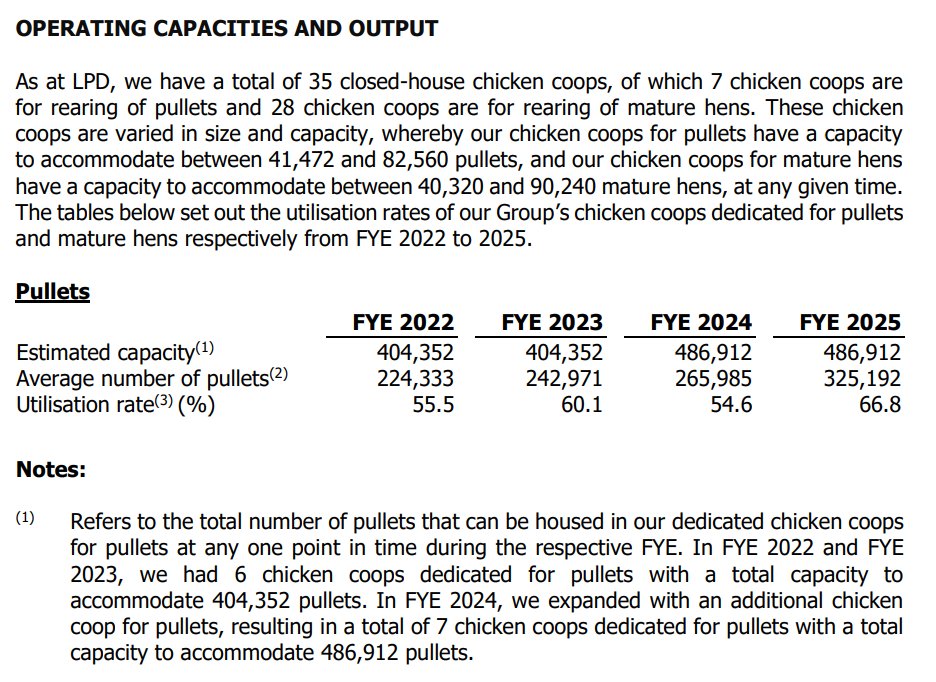

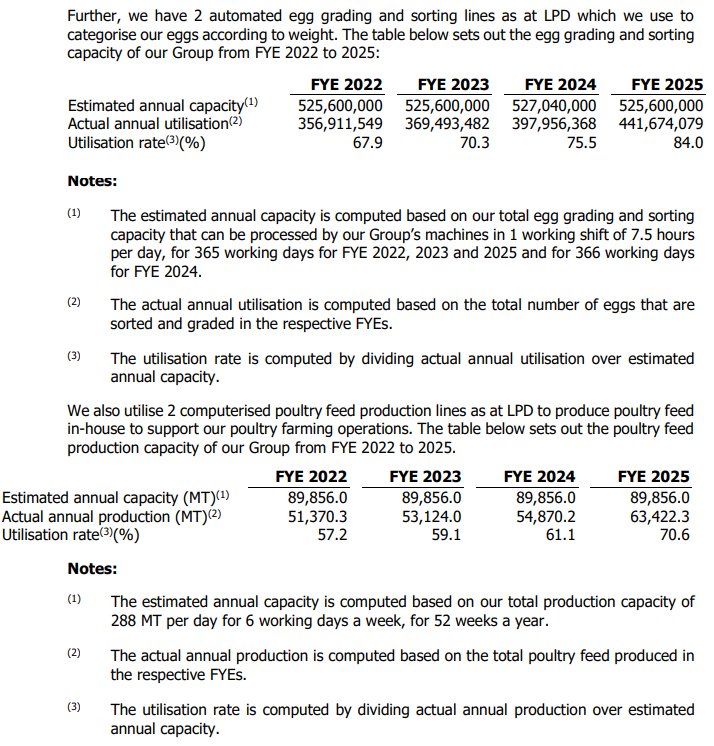

- Massive Capacity Expansion: The new Teluk Intan farm is set to nearly double production capacity by 94%, offering significant potential for market share growth if demand is met.

- Egg Price Deregulation: The removal of the government's egg price ceiling allows the company to potentially pass on rising input costs to consumers, which could restore core profitability.

Threats

- Subsidy Cliff: The cessation of government subsidies (RM40.1M in FY25) from August 2025 will immediately and significantly impact reported profitability, revealing the company's thin underlying margins.

- Feed Cost Volatility: Profitability is highly exposed to volatile global prices of maize and soybean meal, which constitute 82% of feed input costs and are denominated in USD.

- Single Supplier Risk: Sole reliance on Leong Hup for Day-Old-Chicks creates a critical vulnerability; any supply disruption could halt production cycles and impact revenue.

- Valuation Pressure: The IPO is priced at a significant premium (PE 7.1x) compared to direct peers like Teo Seng and Lay Hong trading at much lower multiples (PE 3x-4x), risking post-listing price correction.

- Disease Outbreaks: The poultry industry is inherently at risk of disease outbreaks, such as the company's past H9N2 incident in 2018, which can halt production and cause significant financial losses.

Key Highlights

Sorry, this feature only available for iSaham Pro

Conclusion

Sorry, this feature only available for iSaham Pro

Hock Soon Capital Berhad's Latest News