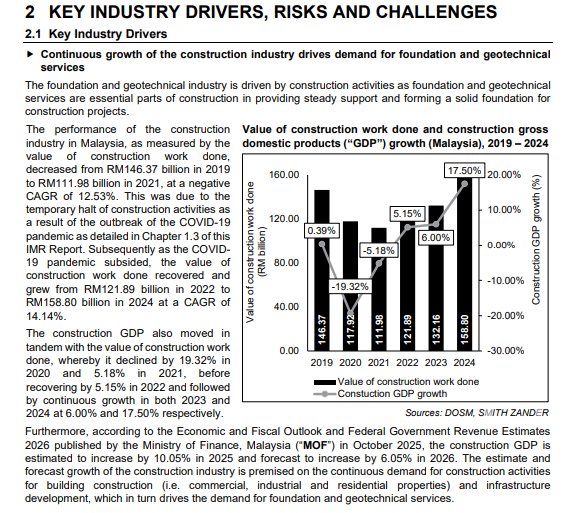

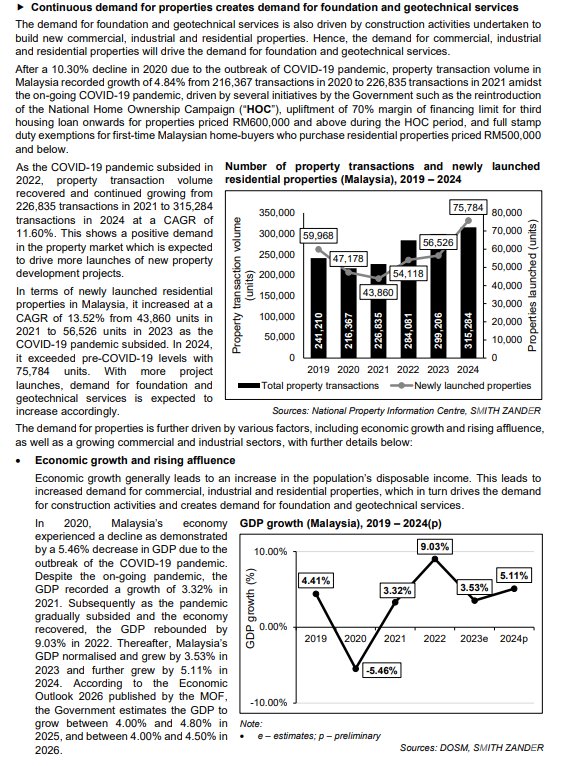

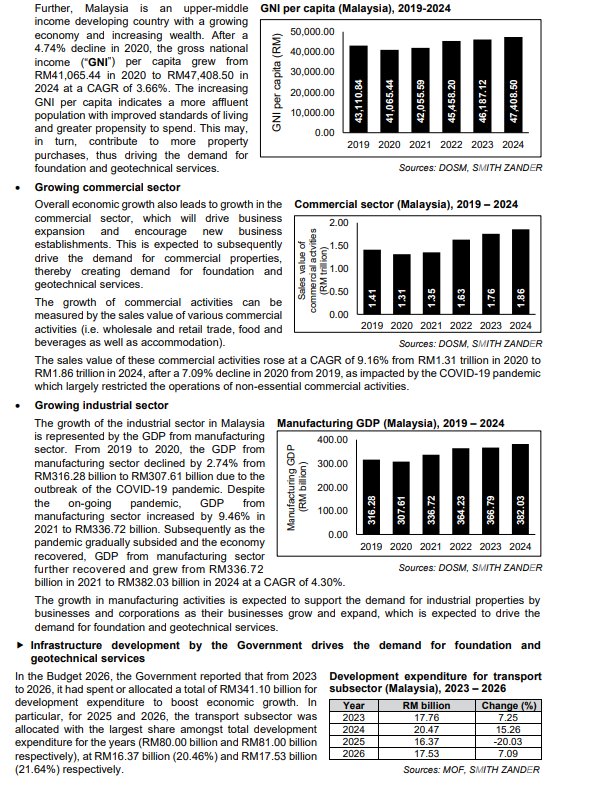

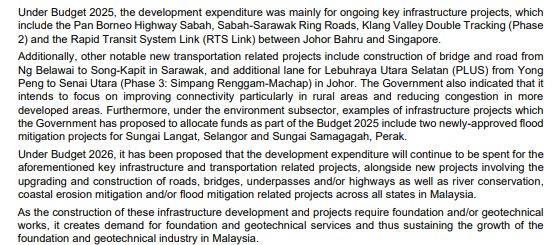

Geohan Corporation Berhad IPO's Analysis

Geohan Corporation Berhad

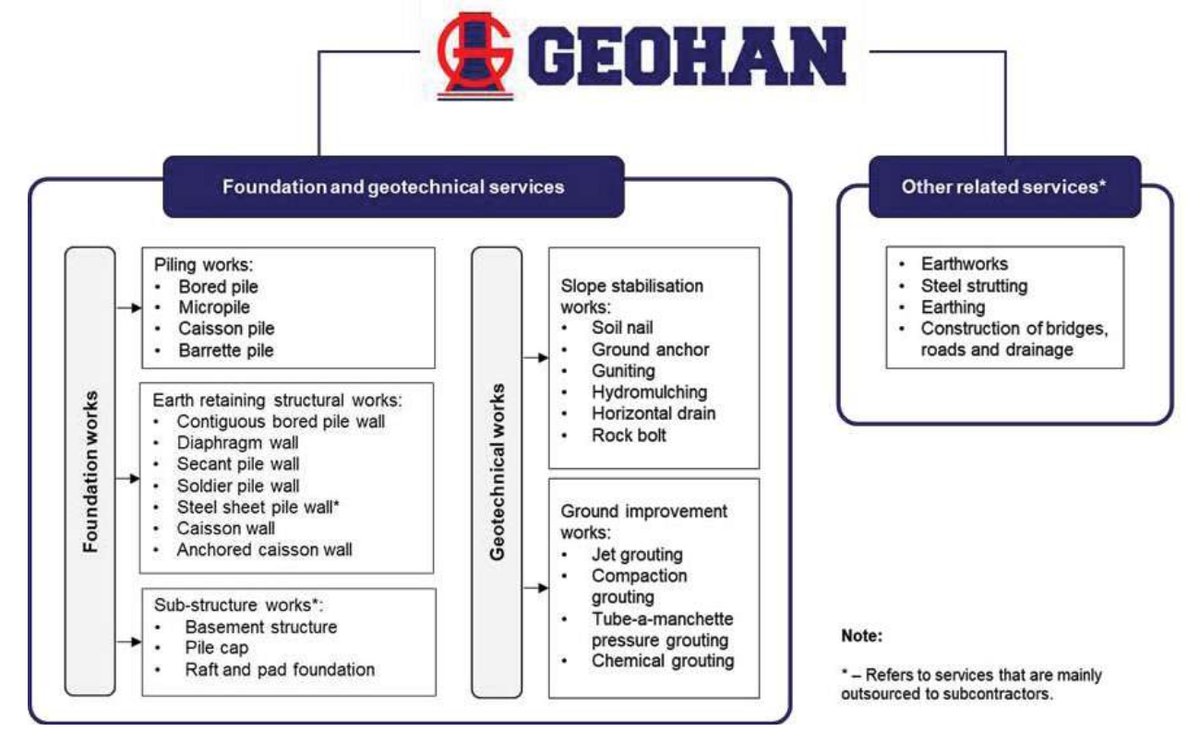

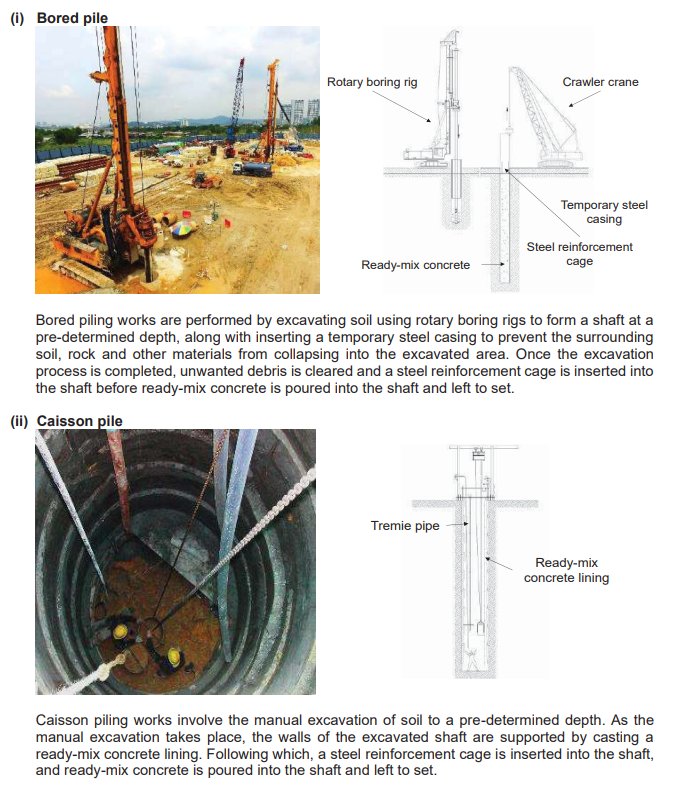

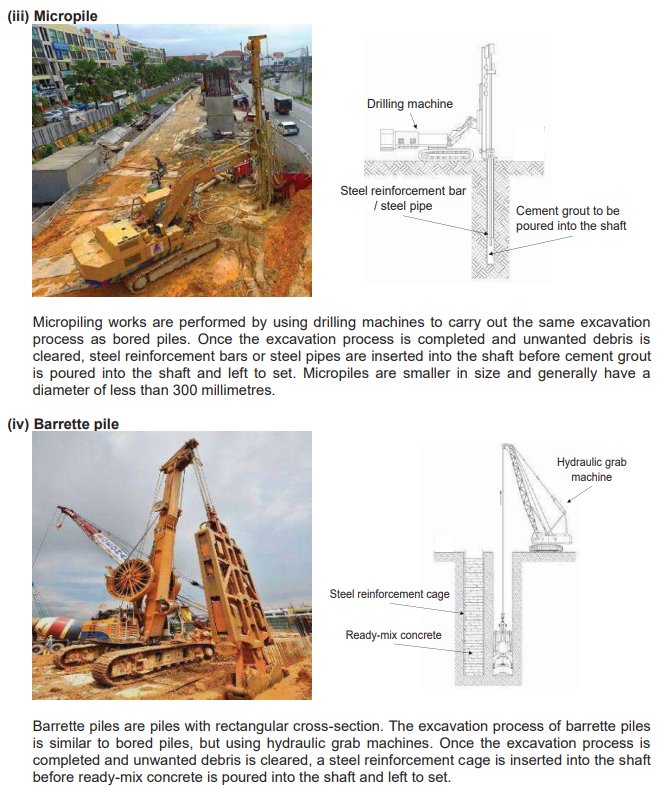

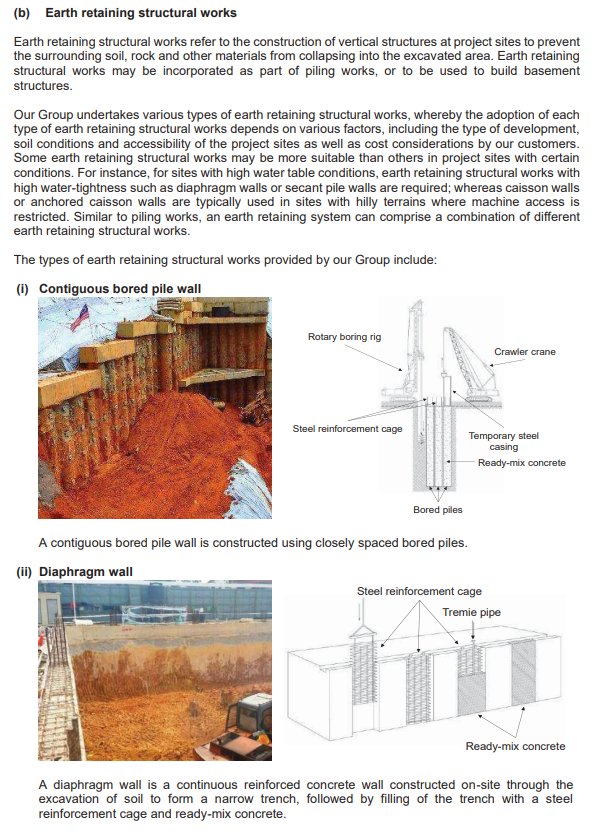

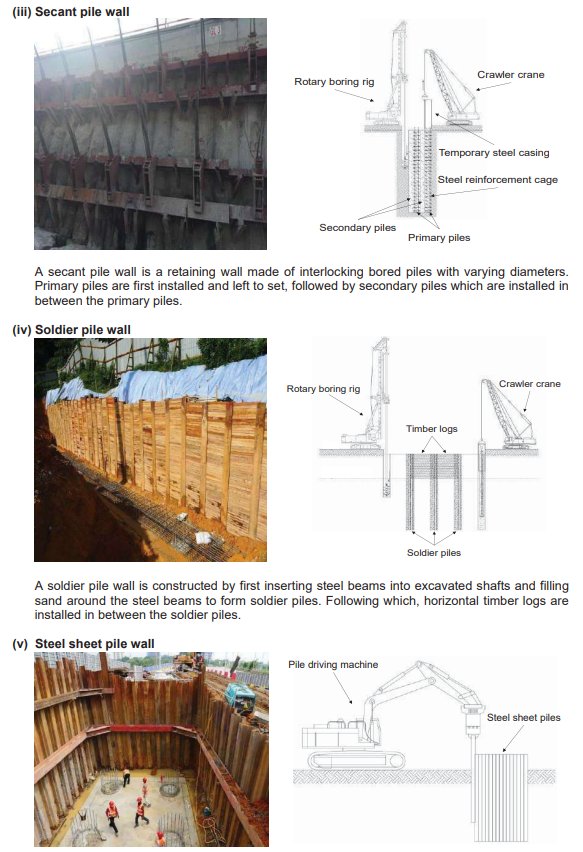

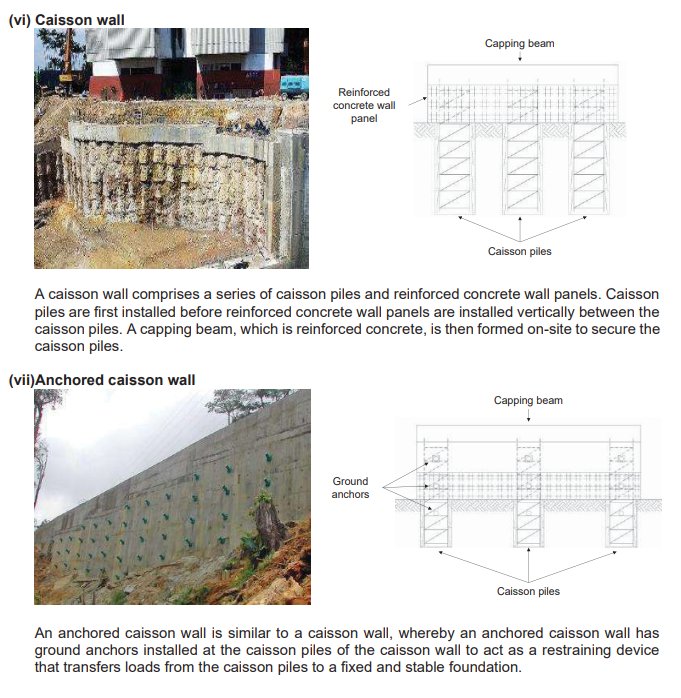

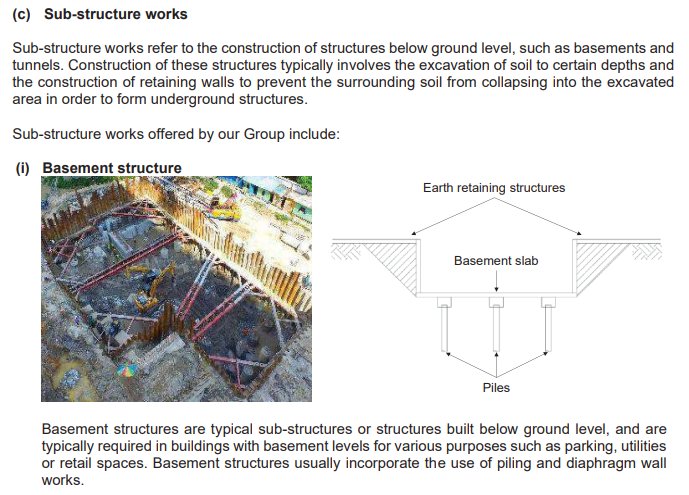

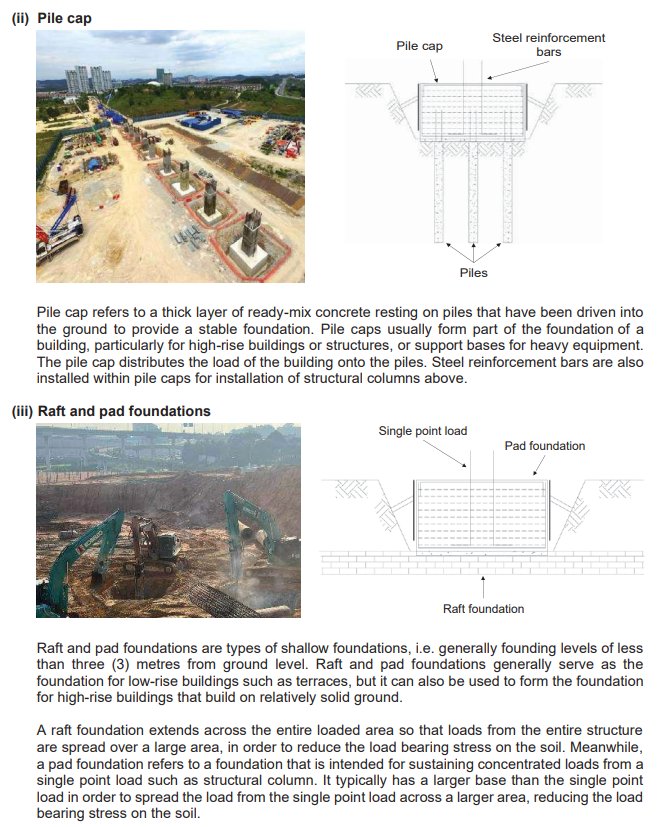

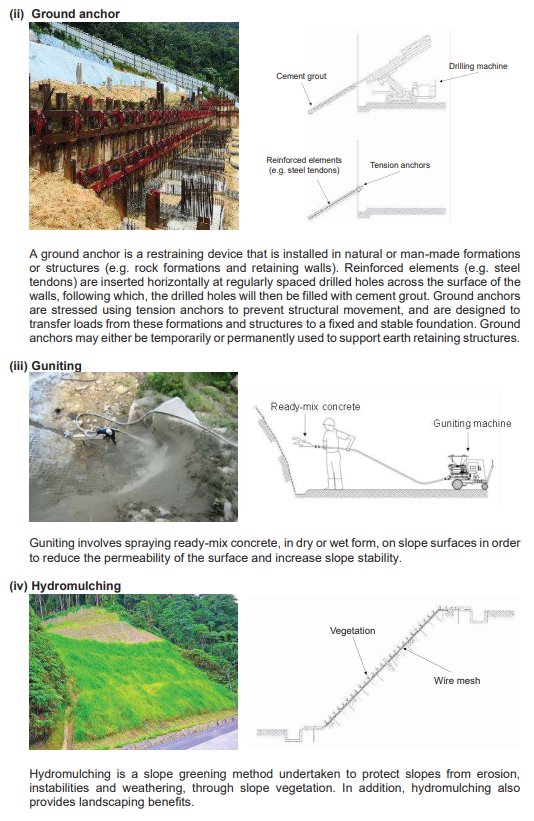

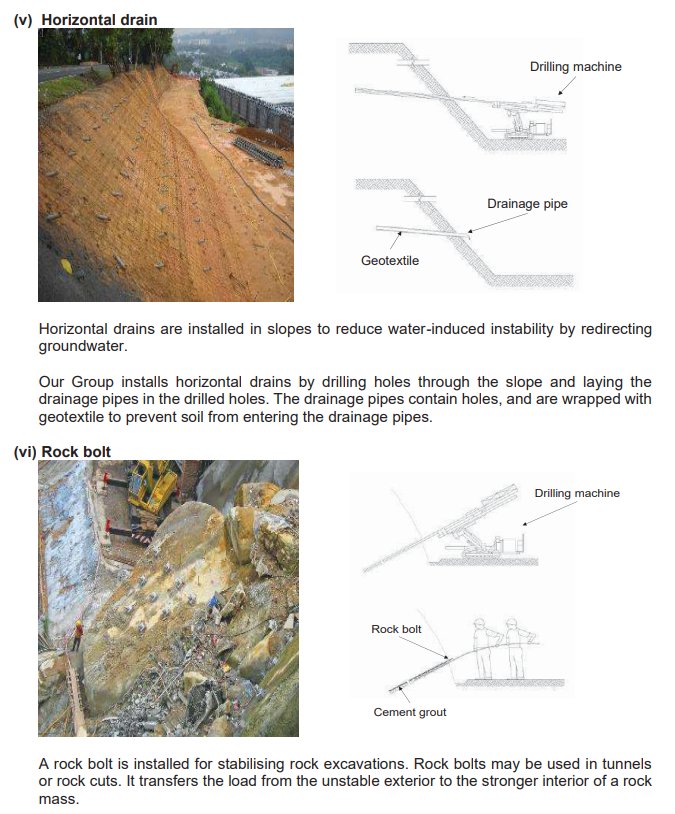

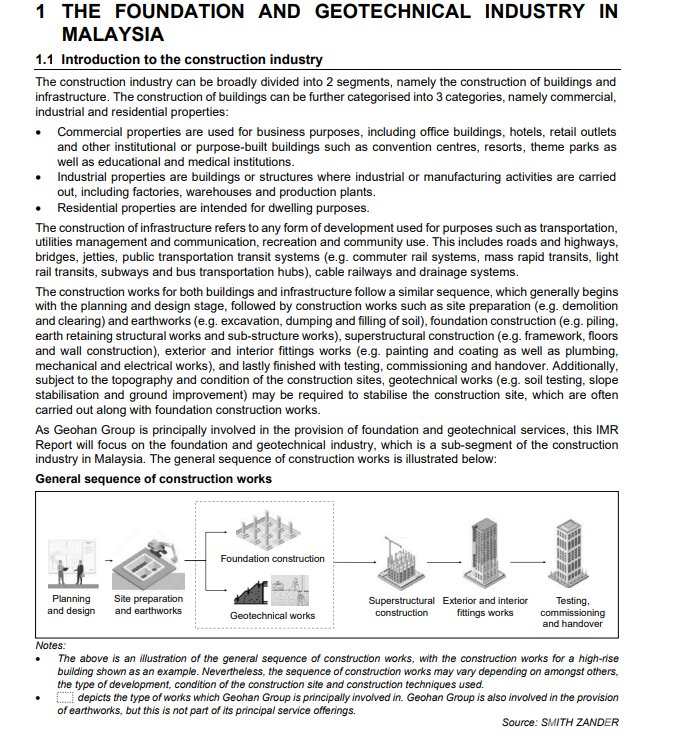

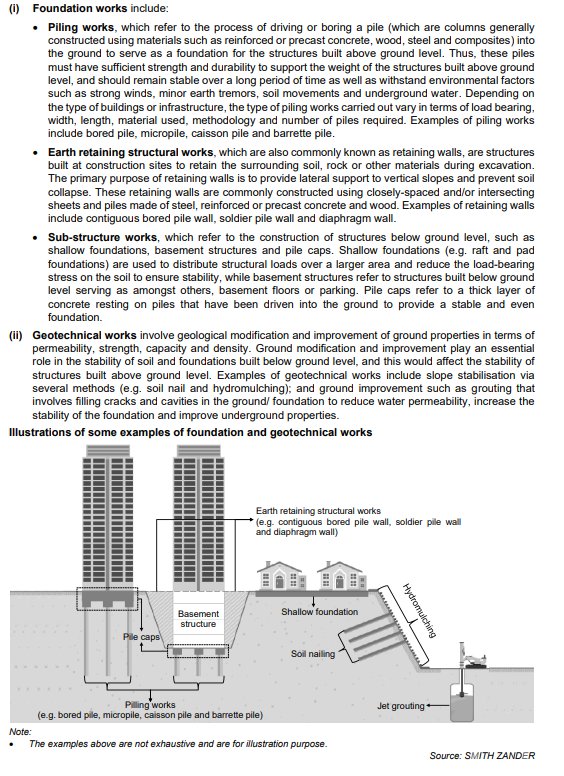

Geohan Corporation Berhad, through its subsidiaries, is principally involved in the provision of foundation and geotechnical services, as well as other related construction services in Malaysia. The Group's services focus on activities below ground level, providing stable foundations for buildings and infrastructure. Its offerings include a comprehensive range of foundation works such as piling (bored, caisson, micropile), earth retaining structures, and sub-structure works. It also provides geotechnical services like slope stabilisation and ground improvement. Additionally, the Group is involved in hiring out equipment and machinery, and the wholesale of construction materials. The Group was formed through a series of acquisitions and has key operational hubs including a headquarters in Kuala Lumpur and a depot facility in Selangor. It also has a subsidiary incorporated in Singapore, Geohan Pte Ltd, to facilitate expansion into the Singaporean market.

IPO Details

Strategic Overview & Data Visuals

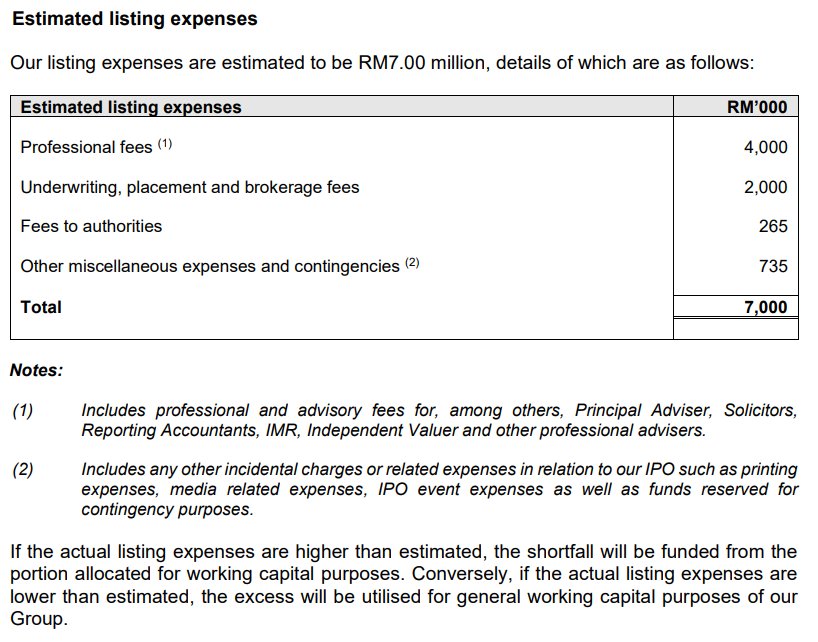

Utilisation of Proceeds

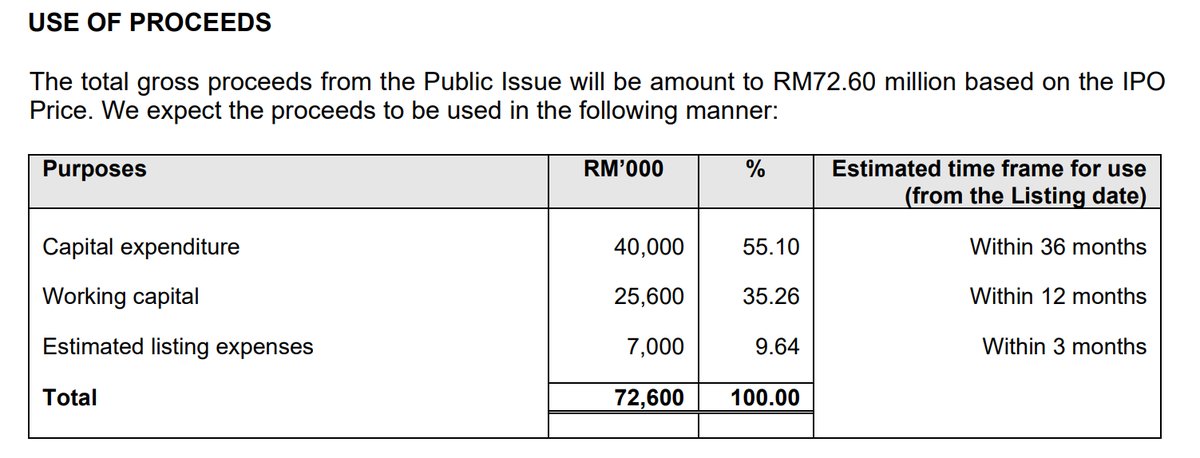

| Purpose | Amount (RM'000) | % | |

|---|---|---|---|

| Expansion | Capital expenditure | 40,000 | 55.1 |

| Working capital | Working capital | 25,600 | 35.26 |

| Listing expenses | Estimated listing expenses | 7,000 | 9.64 |

| Total | 72,600 | 100 | |

Analyst Highlights

| Date | Analyst Highlights |

|---|---|

|

21-Nov-2025

Mplus |

|

|

20-Nov-2025

Public Invest |

|

|

20-Nov-2025

TA |

|

|

19-Nov-2025

RHB |

|

Utilisation of Proceeds

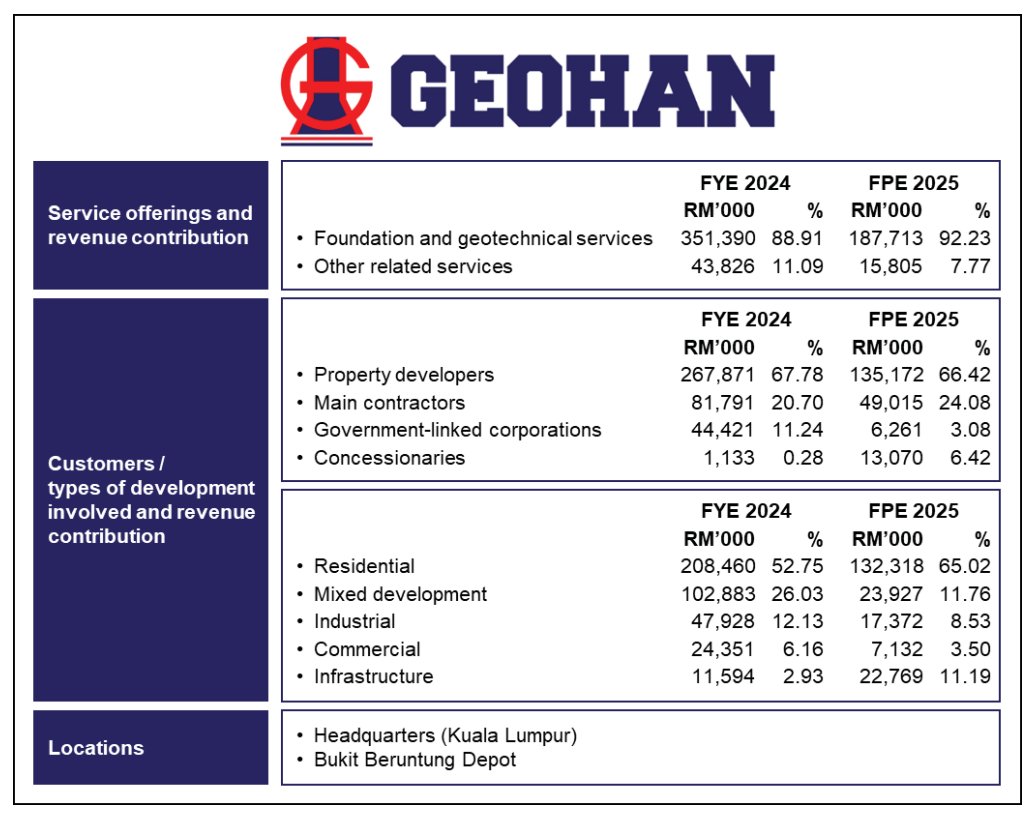

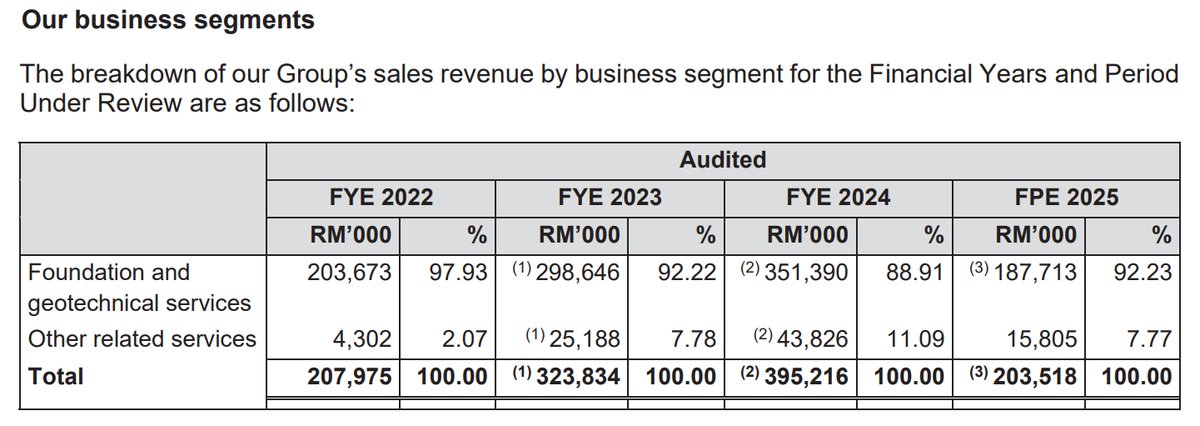

Business Segments

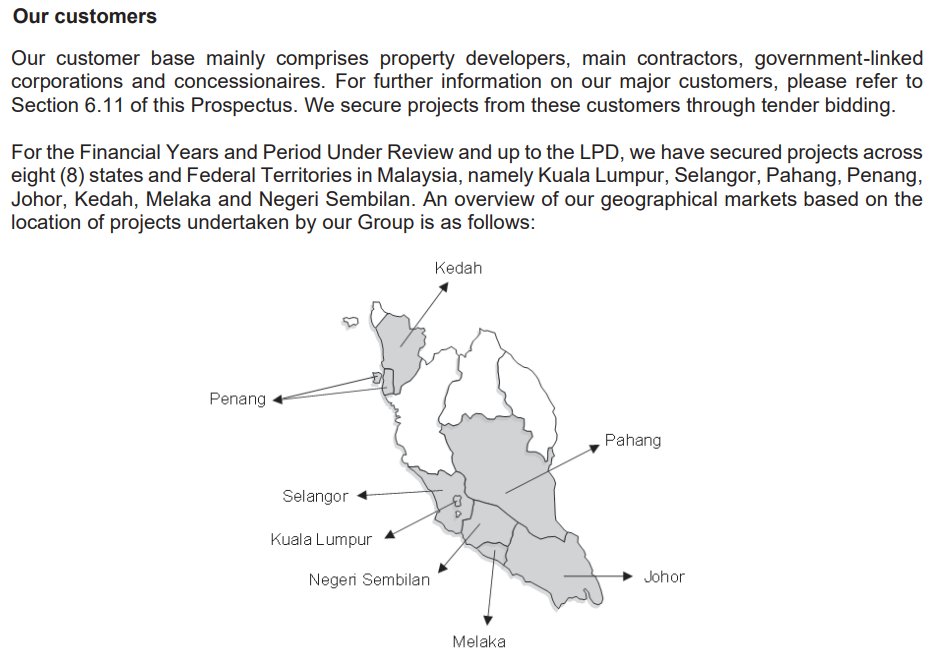

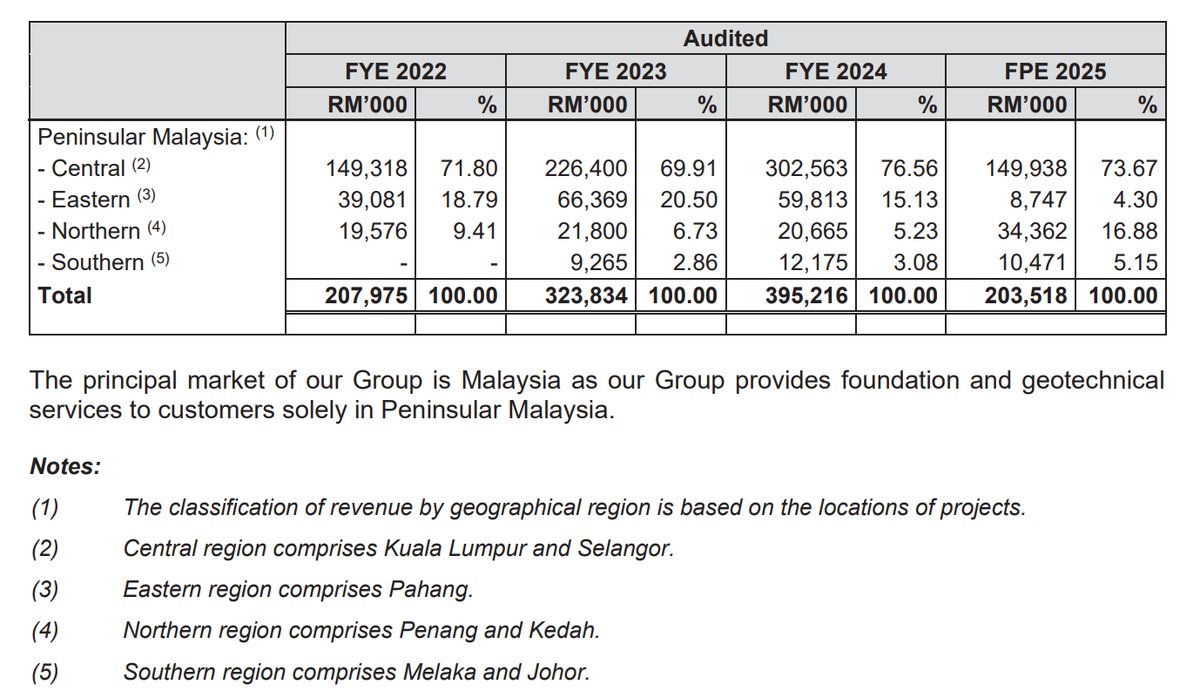

Geographical Segments

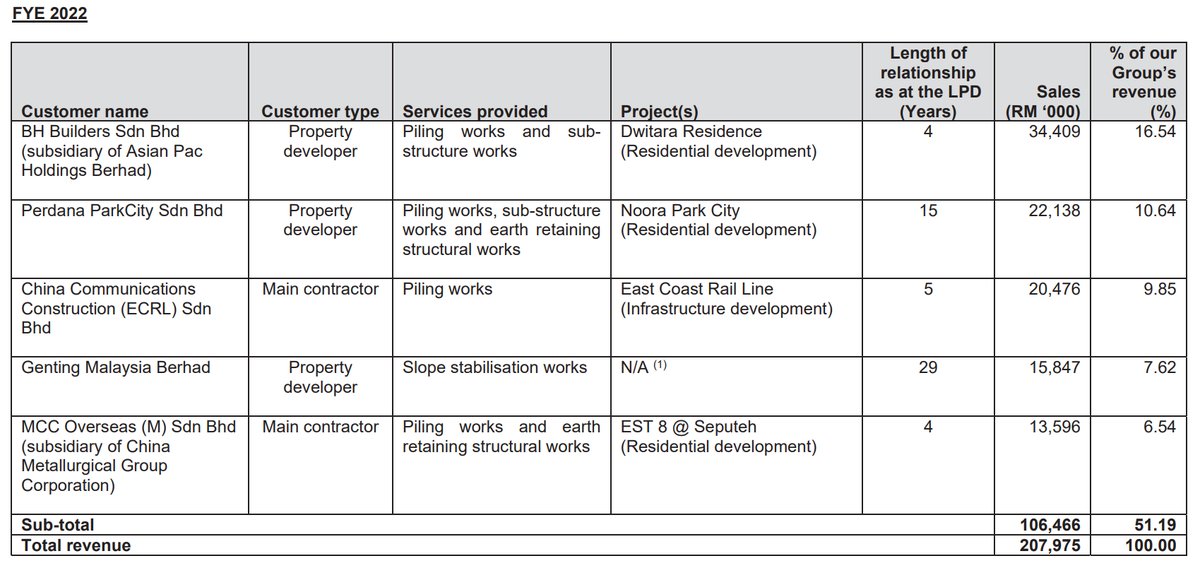

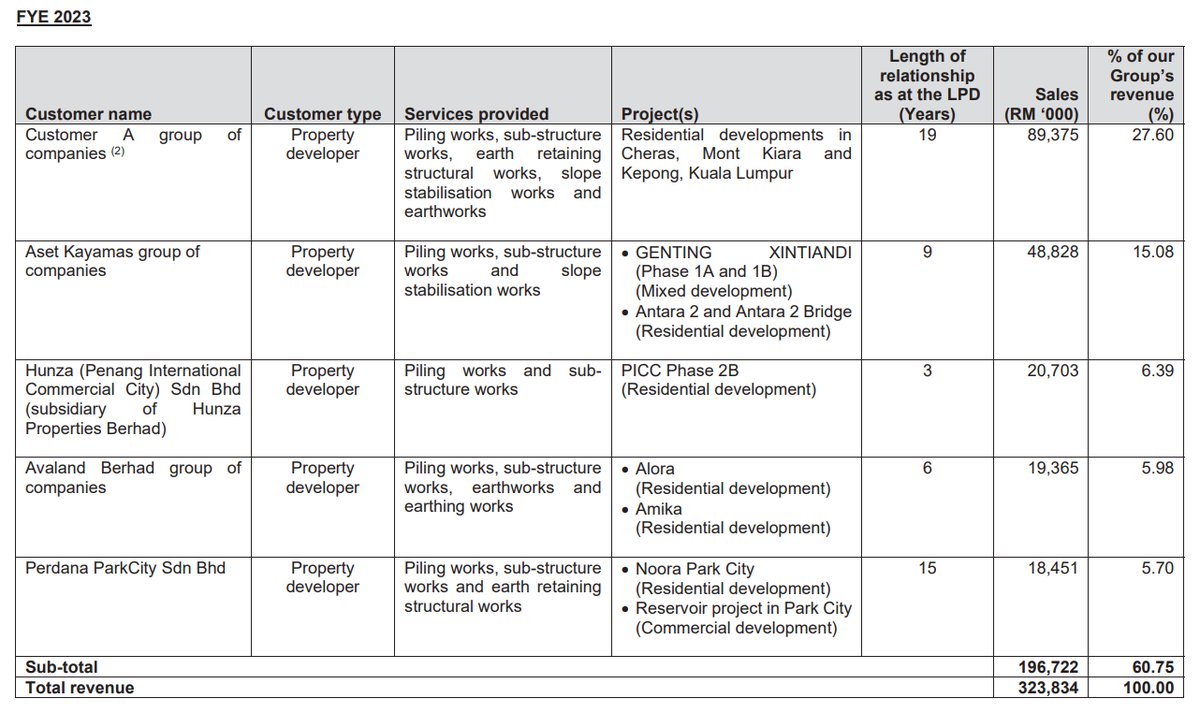

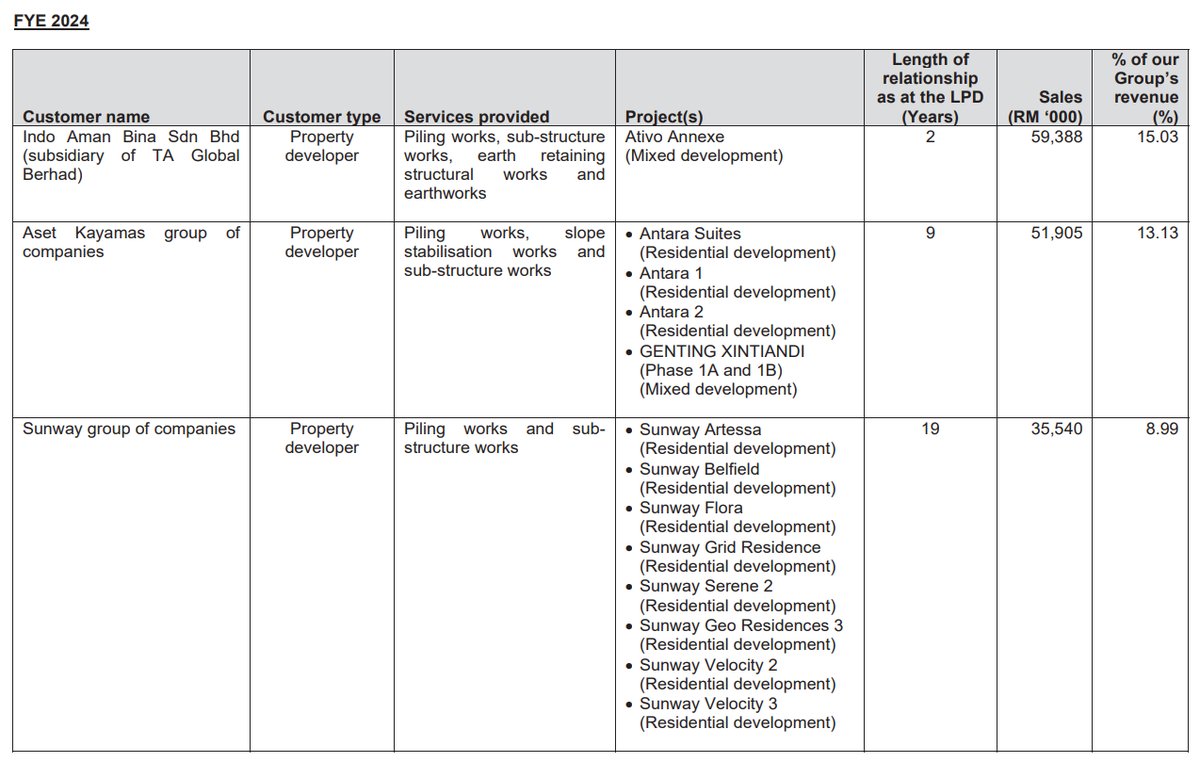

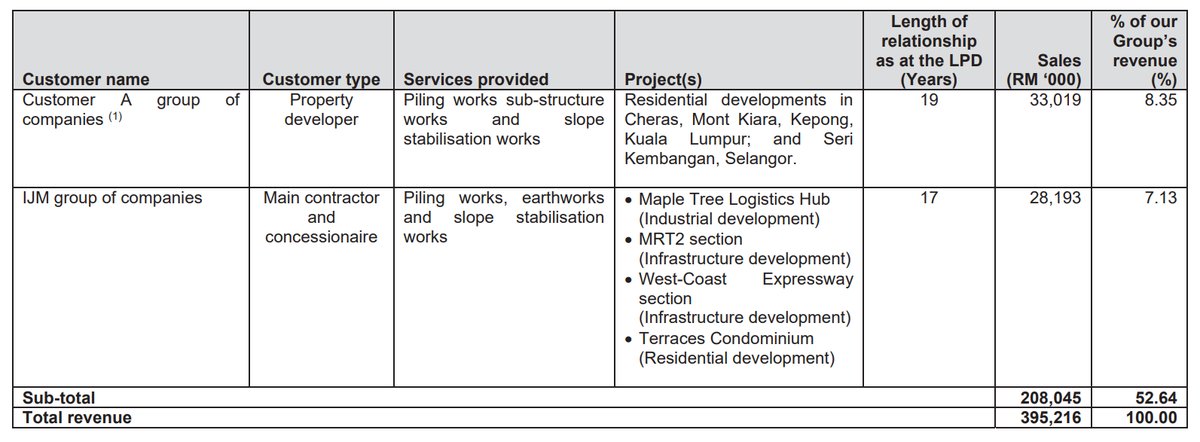

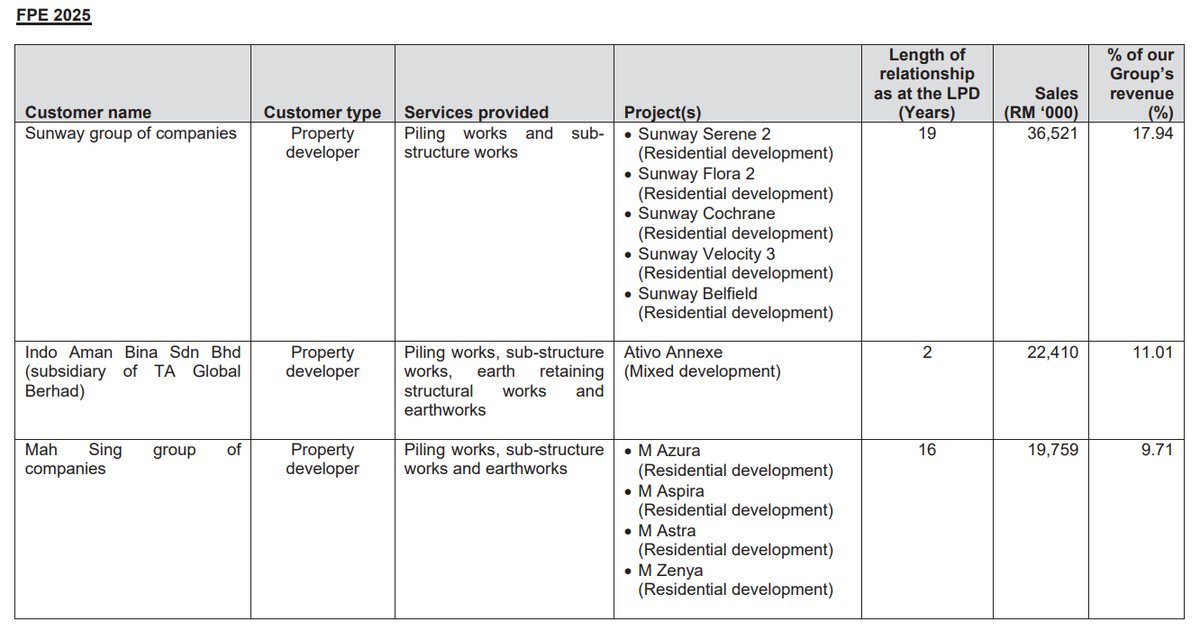

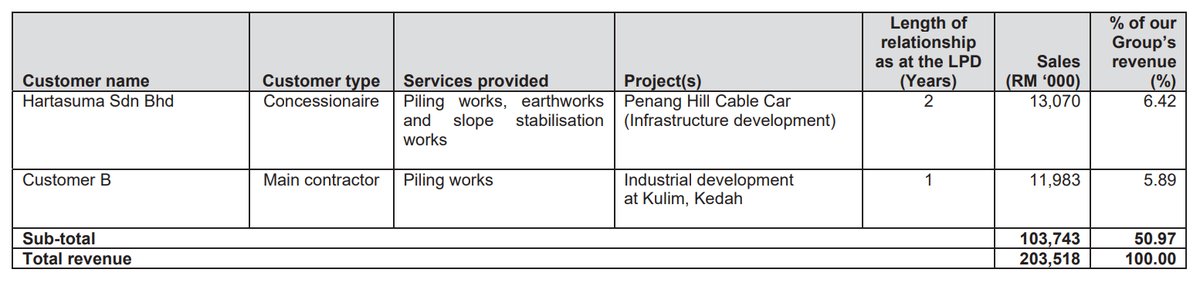

Major Customers

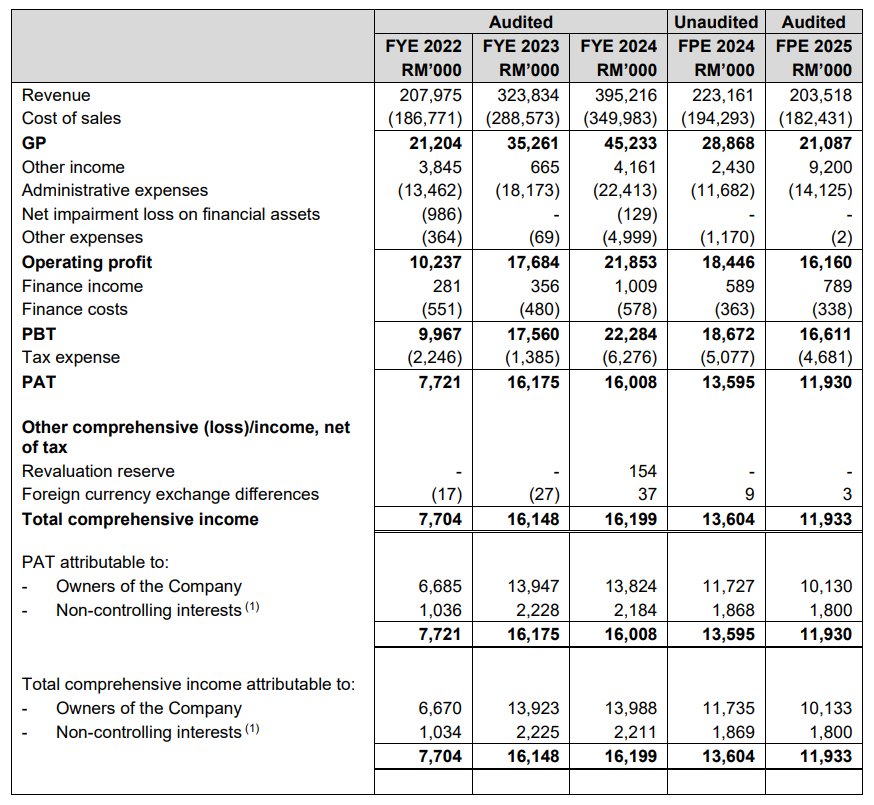

Revenue by Financial Year Ended

Profit After Tax (PAT) by Financial Year Ended

Revenue by Financial Period Ended

Profit After Tax (PAT) by Financial Period Ended

SWOT Analysis

Strengths

- High-Rise Residential Specialist: Geohan has established a strong foothold in the Klang Valley high-rise segment with Tier-1 clients like Sunway and Mah Sing, providing a steady baseline revenue stream that cushions against infrastructure project volatility.

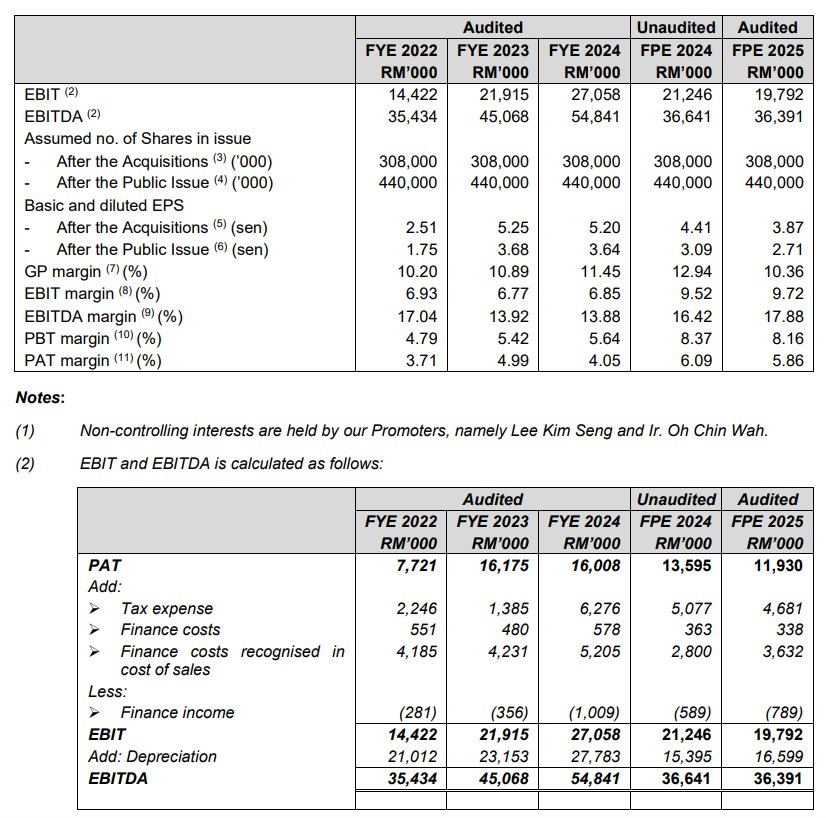

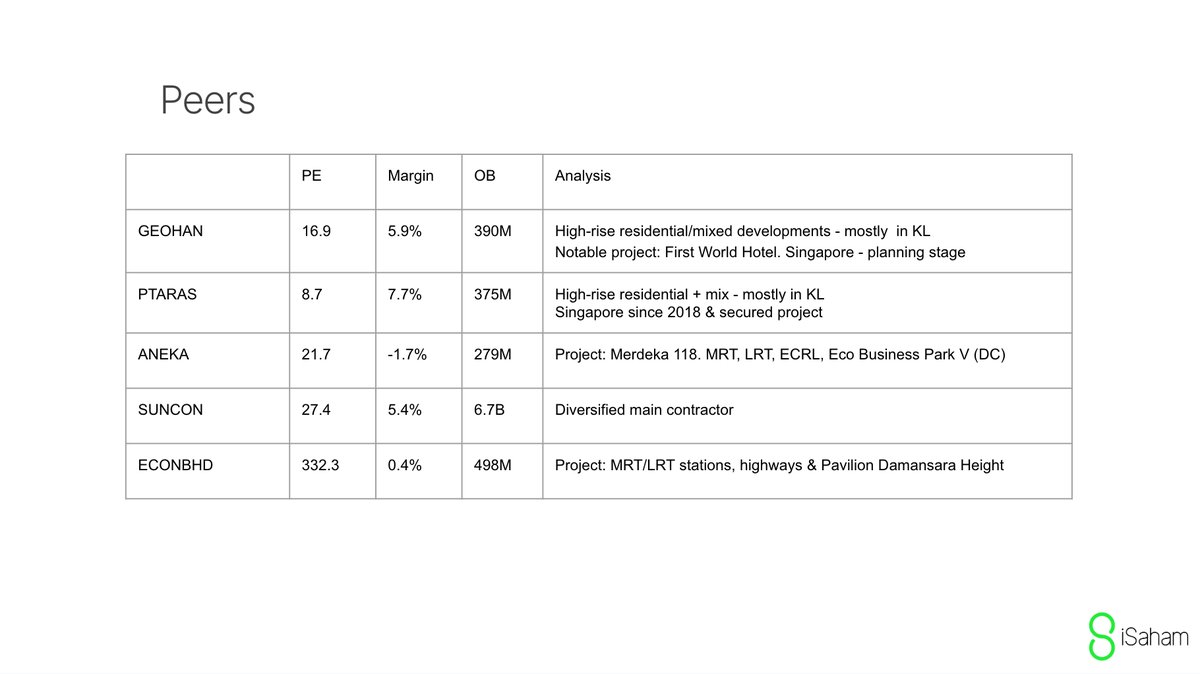

- Profit Margins: Geohan maintains a healthy 5.9% net margin, significantly outperforming peers like Aneka (-1.7%) and Econpile (0.4%), proving operational efficiency without sacrificing profits just to win volume.

- Previous Experience in Singapore: Having successfully delivered the Jurong East MRT modification (2009-2011) proves to Singapore regulators (BCA/LTA) that Geohan is technically capable, even if they have been away for a while.

Weaknesses

- Zero Singapore Projects: Unlike Pintaras Jaya which generates ~84% of its revenue (RM311 million) from Singapore, Geohan holds zero active contracts there, making entry high-risk against such a dominant incumbent with established economies of scale.

- Valuation Premium Risk: Listing at a PE of ~16.9x makes Geohan more expensive than its closest peer Pintaras (PE 8.7x)—which already generates ~84% of revenue from Singapore—potentially deterring value investors who prefer companies with a proven overseas track record.

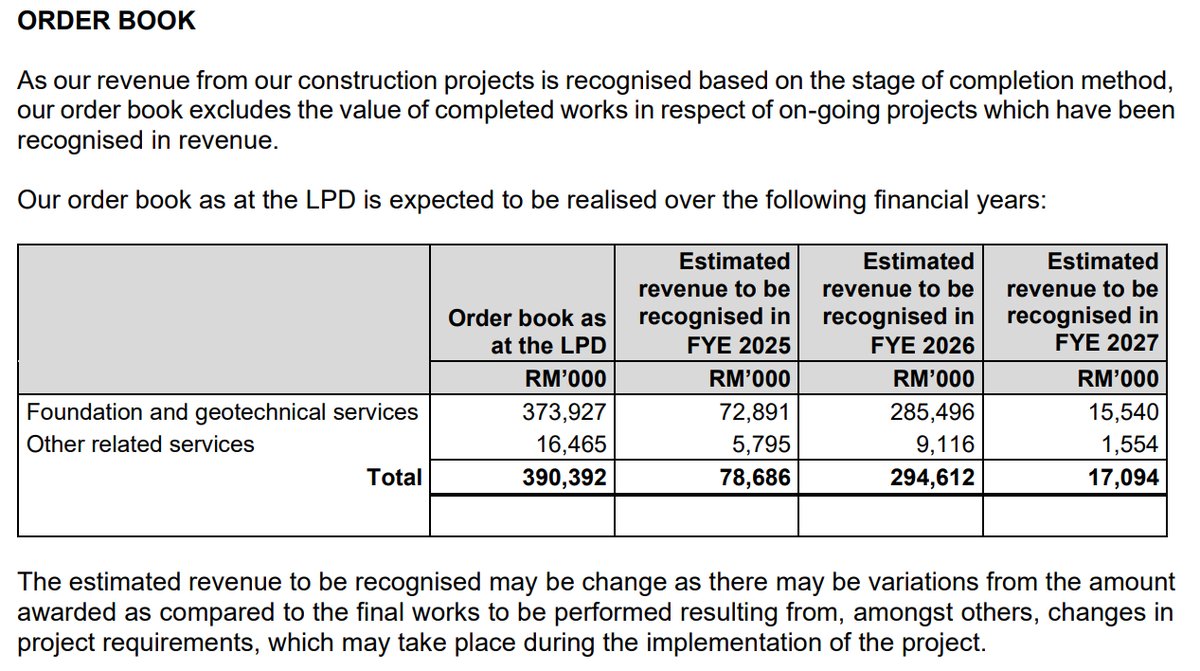

- Short-Term Order Visibility: With an order book coverage of 0.99x, Geohan trails behind direct peers like Pintaras (1.01x), Aneka (1.32x) and Econpile (1.19x). The breakdown reveals a massive revenue drop-off by FY2027 (only RM17m secured), creating urgent pressure to replenish the order book immediately post-listing.

Opportunities

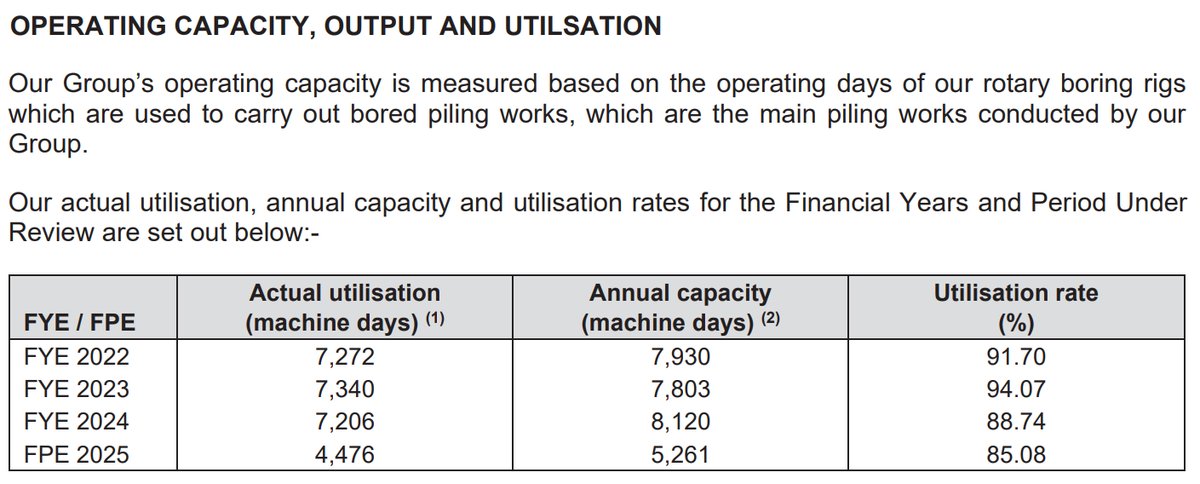

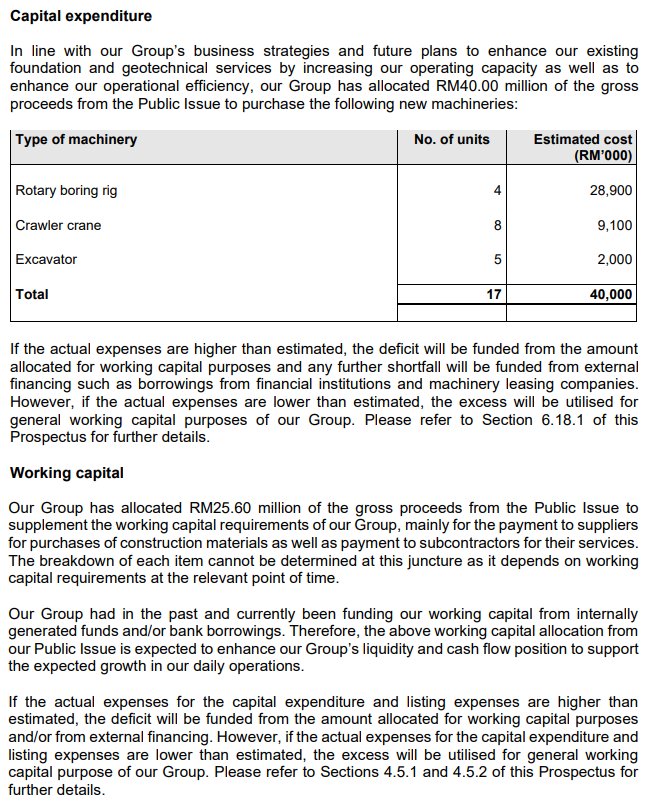

- Increased Operating Capacity: A significant portion of the IPO proceeds (55.10%) will be used for capital expenditure to purchase new machinery, including rotary boring rigs, crawler cranes, and excavators. This expansion is expected to increase operating capacity, enhance efficiency, and reduce reliance on rental machinery.

- Favorable Industry Outlook: The construction industry in Malaysia is experiencing continuous growth, driven by demand for properties and government-led infrastructure projects. This provides a steady pipeline of potential projects for foundation and geotechnical services.

- Singapore Infrastructure Boom: Massive demand from Changi T5, Data Centers, and MRT lines creates "spillover" opportunities for Geohan to win sub-contracts that incumbents like PTARAS or CSC cannot fulfill alone.

Threats

- Industry Cyclicality: The company's performance is heavily dependent on the cyclical nature of the construction industry, which is influenced by economic conditions, government policies, and market sentiment. An economic slowdown could reduce demand for its services.

- Material Price Volatility: The business is subject to fluctuations in the prices of key building materials like ready-mix concrete and steel bars. As contracts are often on a firm-price or lump-sum basis, the company may be unable to pass on increased costs to customers, potentially leading to cost overruns and reduced profitability.

- Intense Competition: The foundation and geotechnical industry is specialized and competitive. The company faces competition from other established players in Malaysia and will face new competitors in Singapore, competing on technical expertise, track record, and pricing.

- Profitless Revenue Risk: If desperate to refill its order book, Geohan risks underbidding for projects, potentially mirroring Aneka’s scenario of winning high-volume contracts but suffering net losses due to cost overruns.

Key Highlights

Sorry, this feature only available for iSaham Pro

Conclusion

Sorry, this feature only available for iSaham Pro

Geohan Corporation Berhad's Latest News