Ambest Group Berhad IPO's Analysis

Ambest Group Berhad

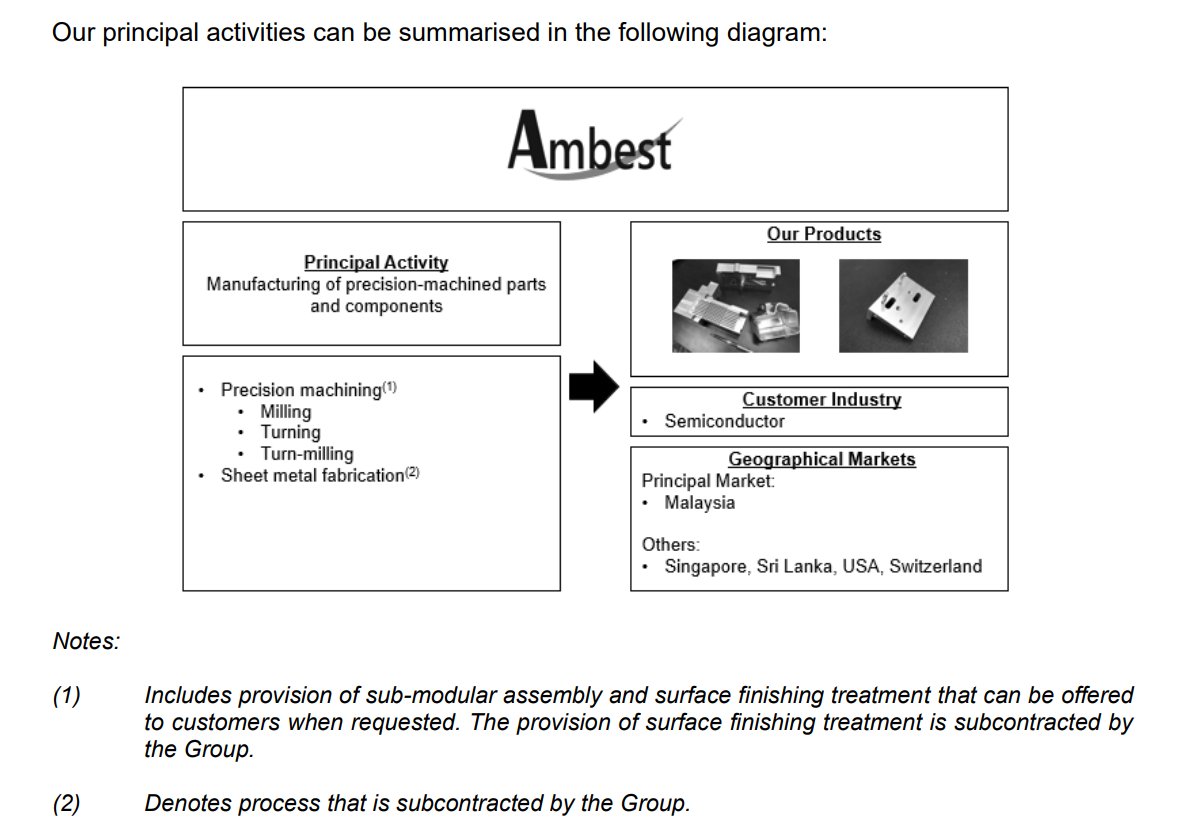

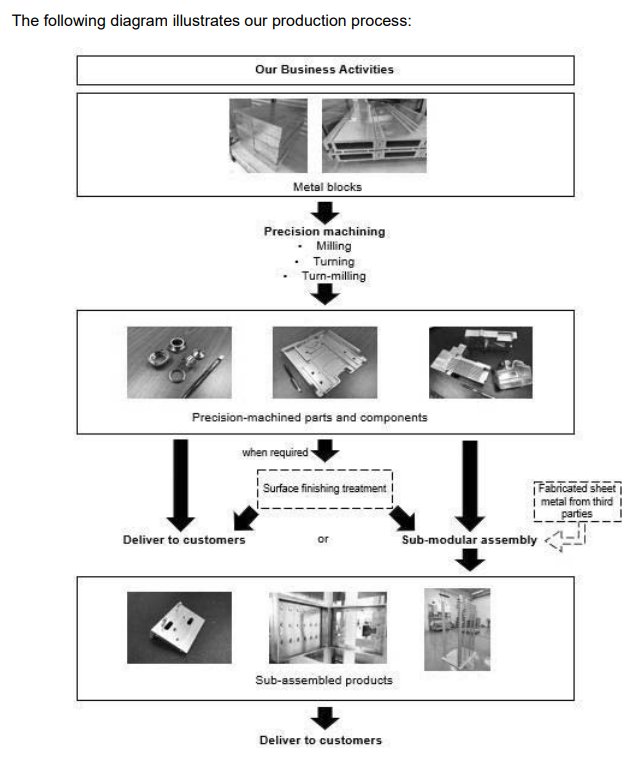

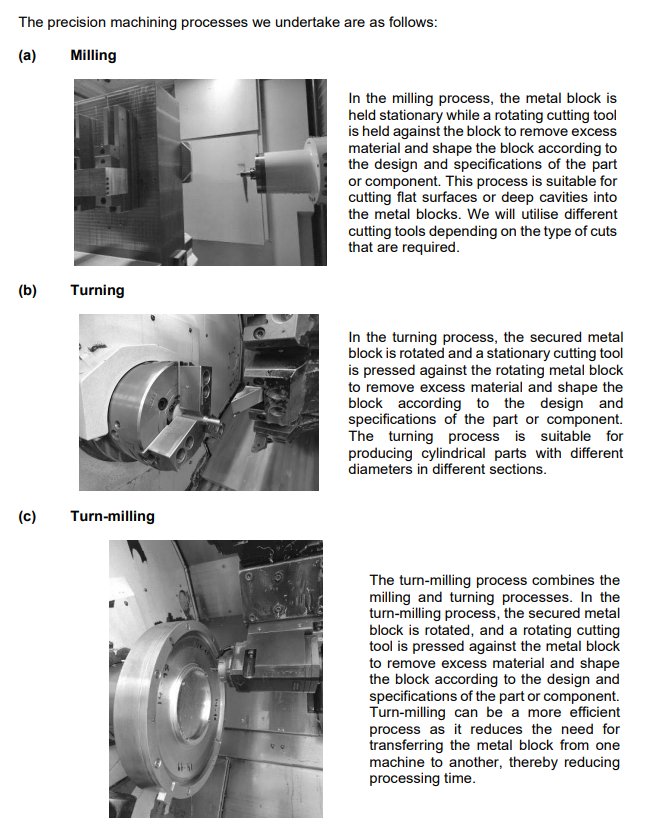

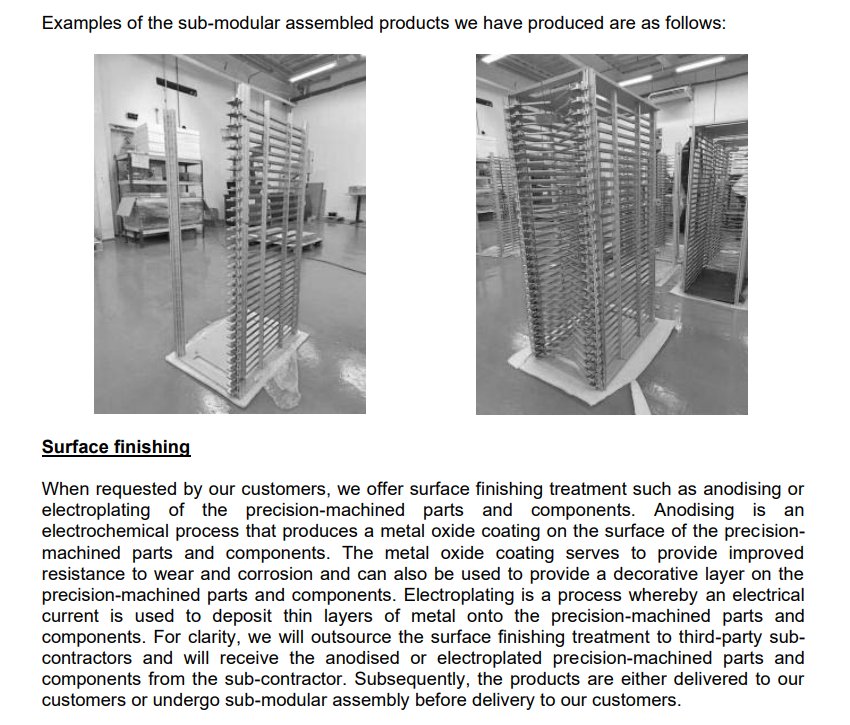

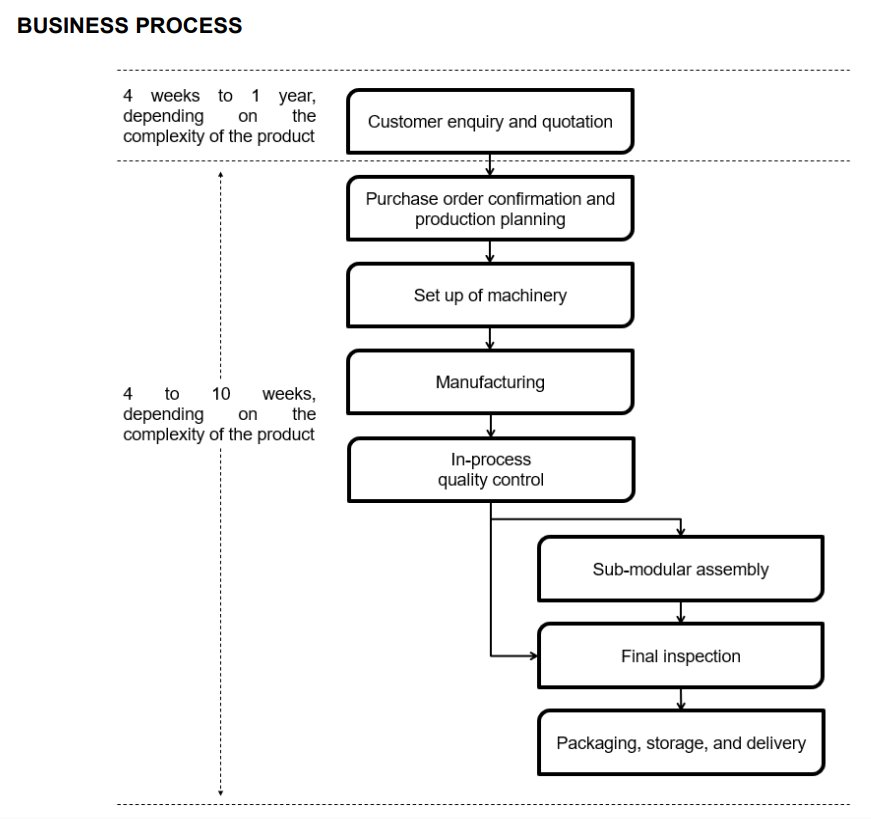

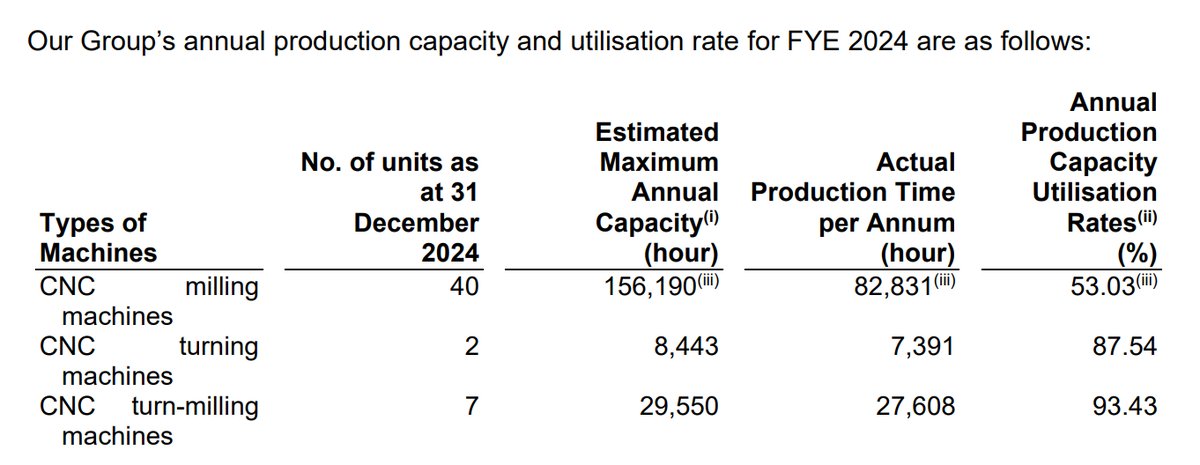

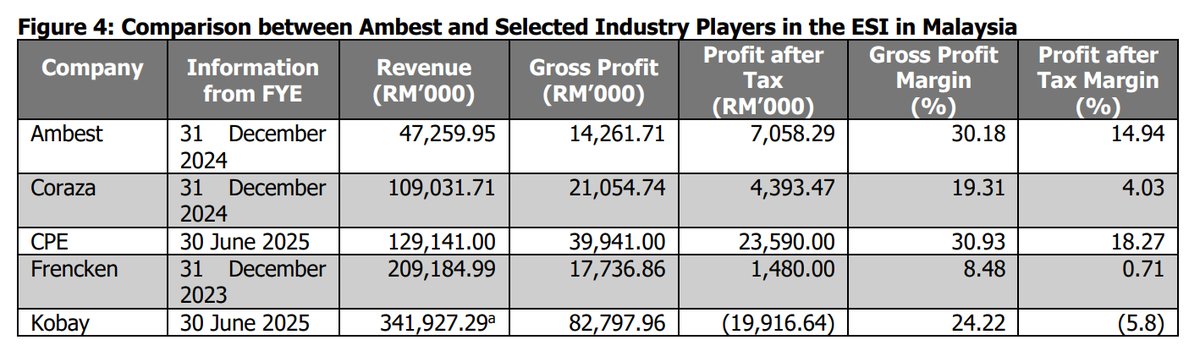

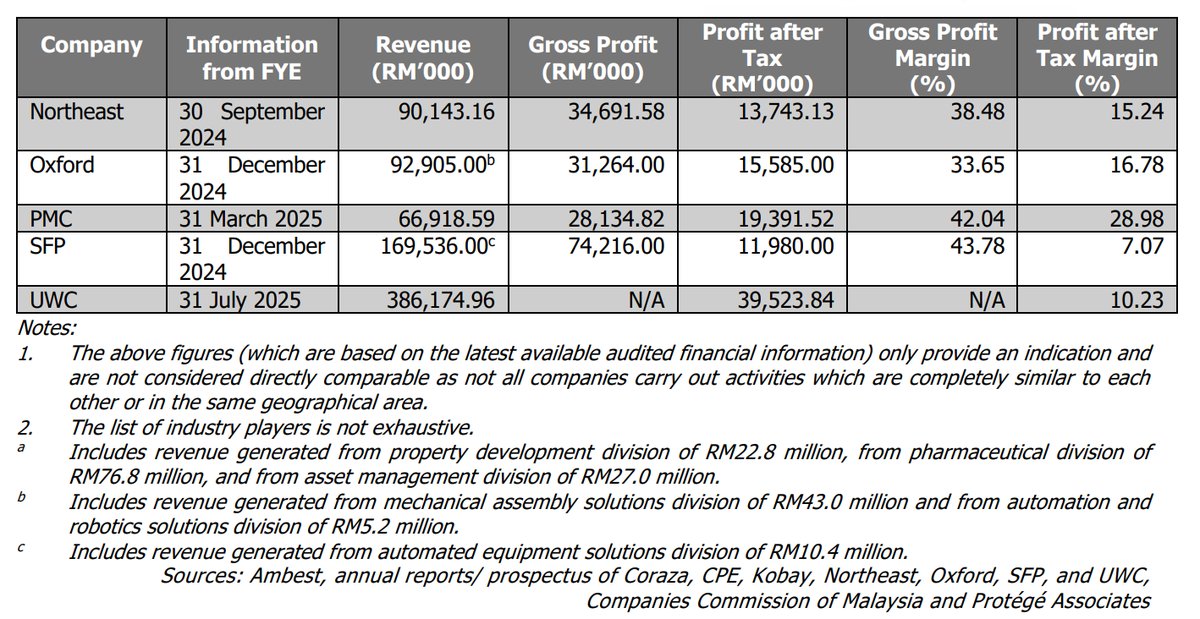

Ambest Group Berhad, through its subsidiary Ambest Technology, is an engineering supporting services provider primarily focused on providing precision machining and sheet metal fabrication for customers in the semiconductor industry. The Group's precision machining services involve processes like milling, turning, and turn-milling to produce high-precision parts and components. It also offers value-added services such as sub-modular assembly, which involves assembling precision-machined components with other metal parts to create frames and structures, and surface finishing treatments like anodising to enhance product properties. The sheet metal fabrication services, which are outsourced to sub-contractors, involve processes like stamping and bending to form desired shapes for enclosures. The company operates from its facilities in Penang, Malaysia, and serves both domestic and international markets, including Singapore and the USA.

IPO Details

Strategic Overview & Data Visuals

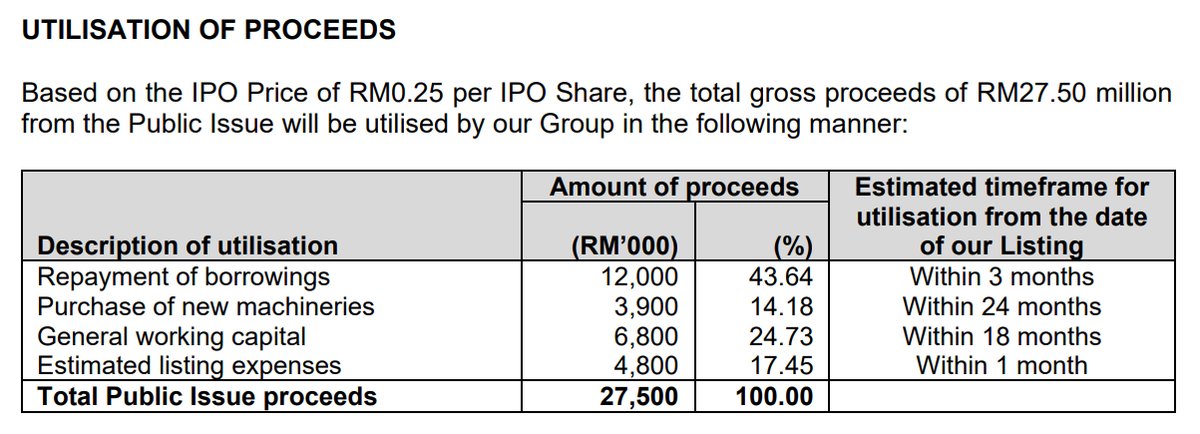

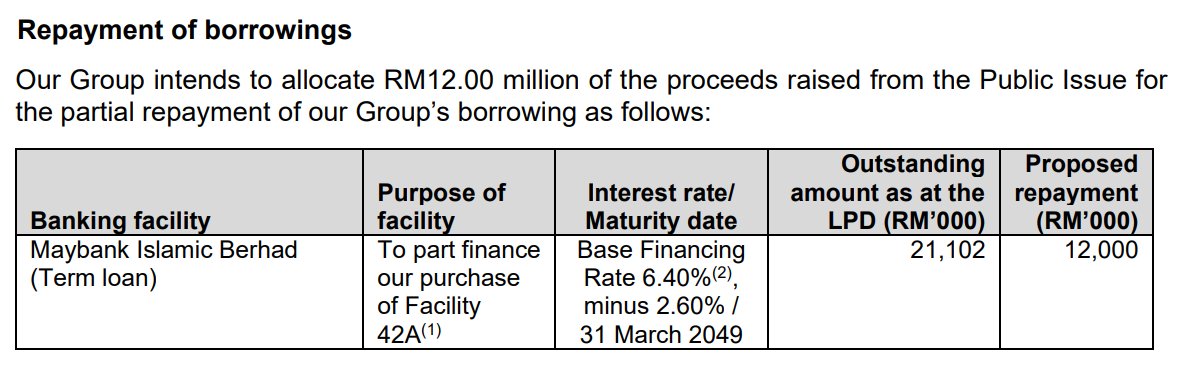

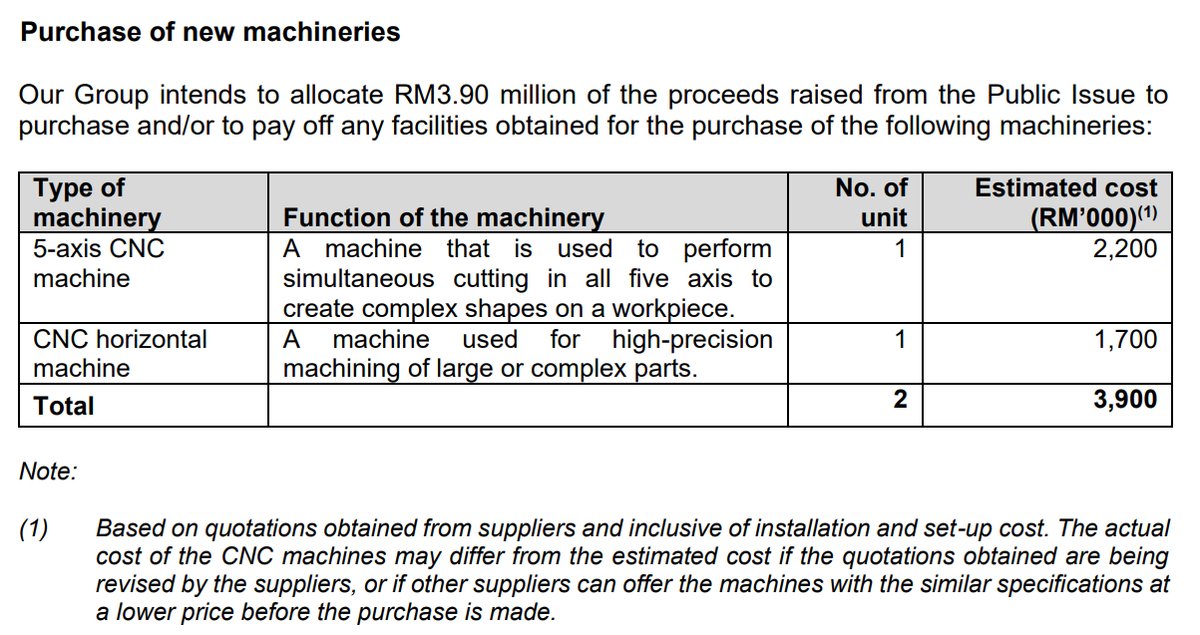

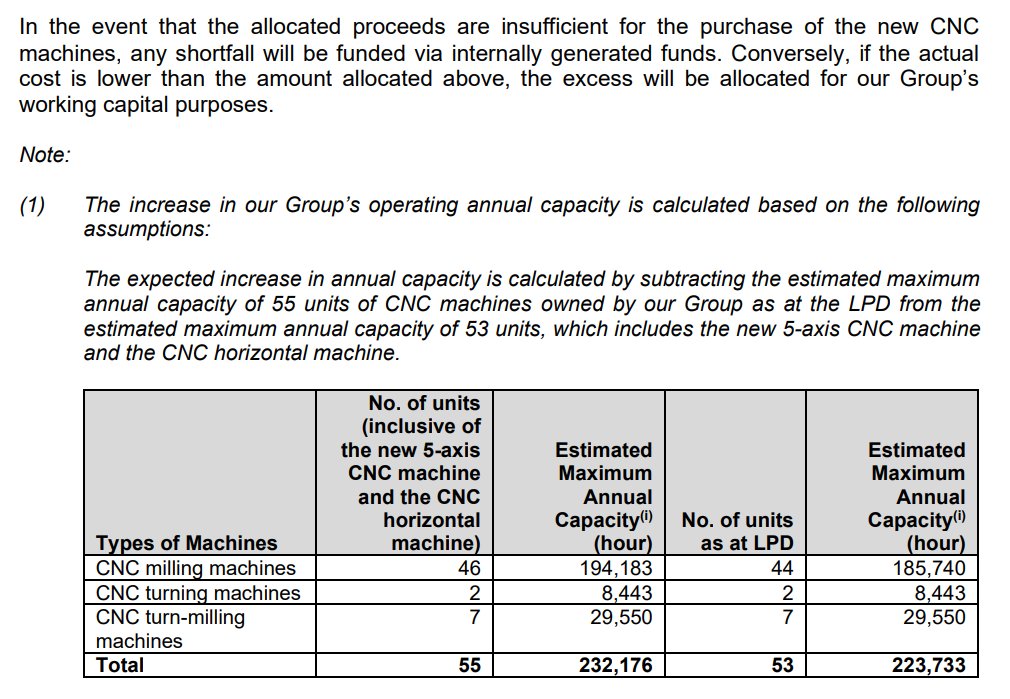

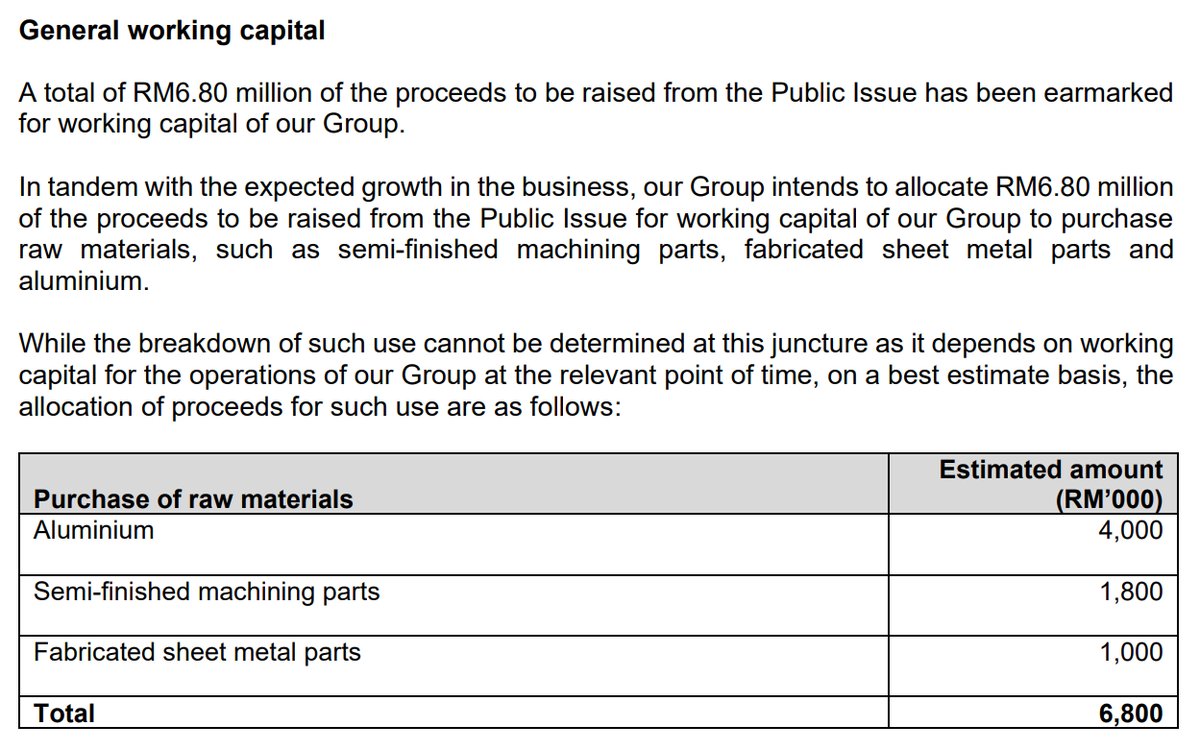

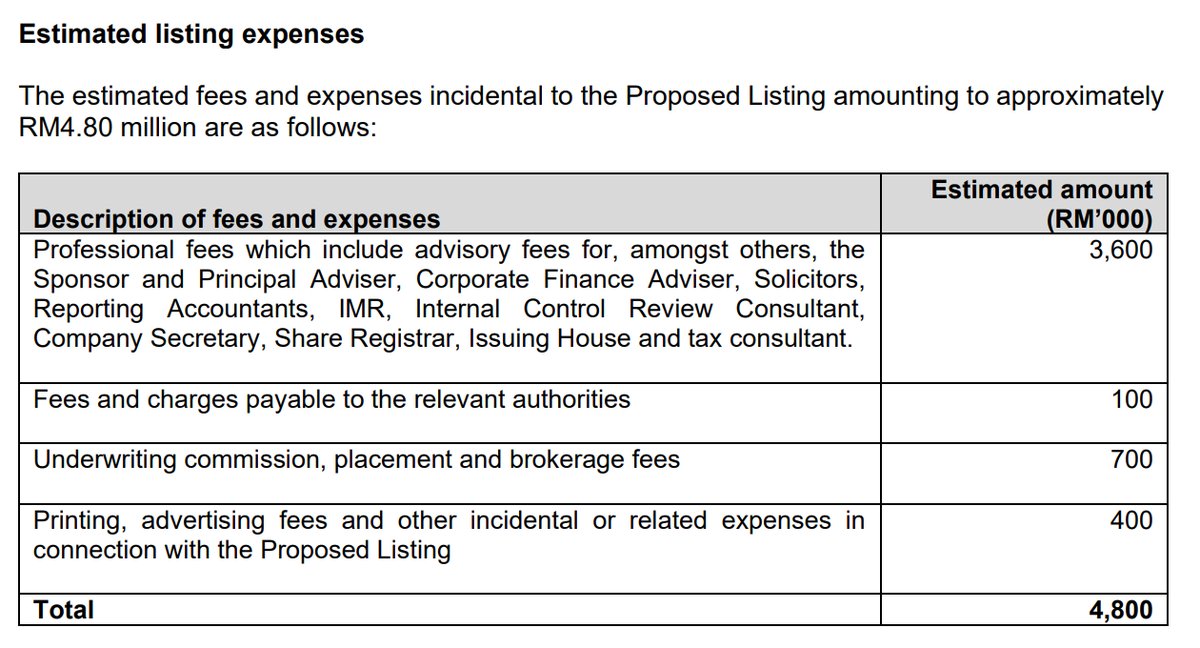

Utilisation of Proceeds

| Purpose | Amount (RM'000) | % | |

|---|---|---|---|

| Expansion | Purchase of new machineries | 3,900 | 14.18 |

| Working capital | General working capital | 6,800 | 24.73 |

| Listing expenses | Estimated listing expenses | 4,800 | 17.45 |

| Debt | Repayment of borrowings | 12,000 | 43.64 |

| Total | 27,500 | 100 | |

Analyst Highlights

| Date | Analyst Highlights |

|---|---|

|

03-Feb-2026

Kenanga |

|

|

27-Jan-2026

Public Invest |

|

|

27-Jan-2026

Mercury |

|

|

27-Jan-2026

TradeView |

|

|

26-Jan-2026

TA |

|

Utilisation of Proceeds

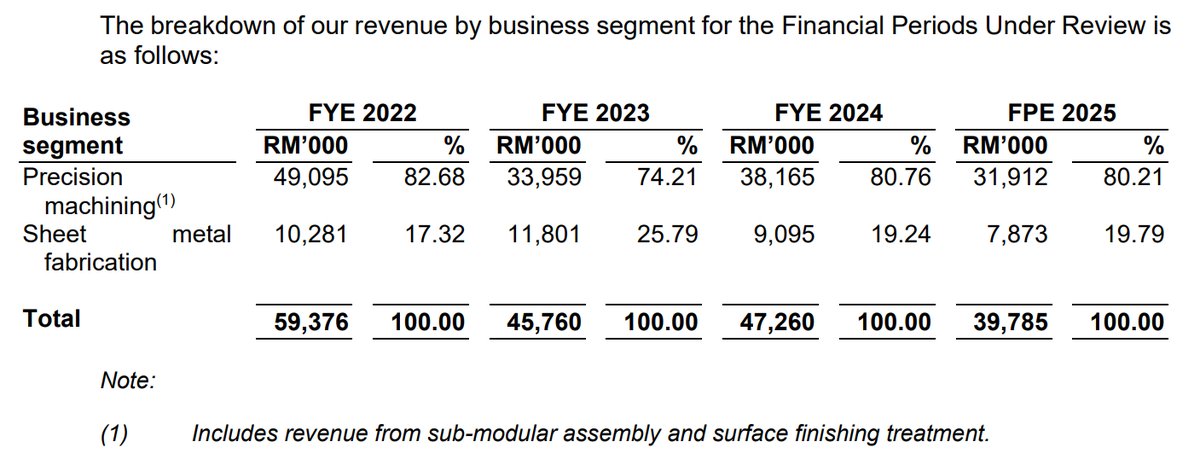

Business Segments

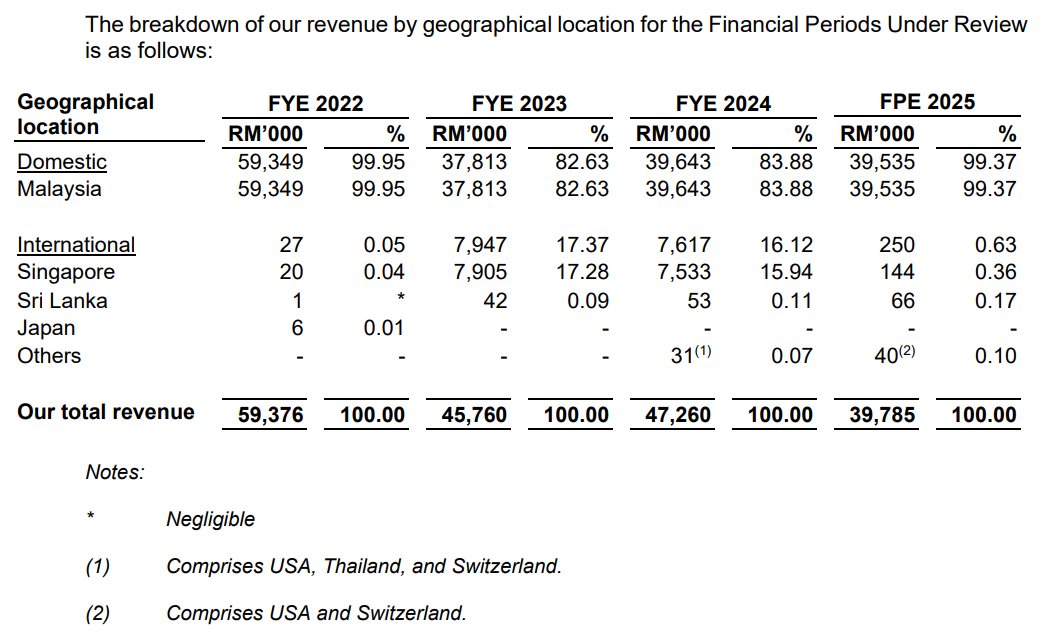

Geographical Segments

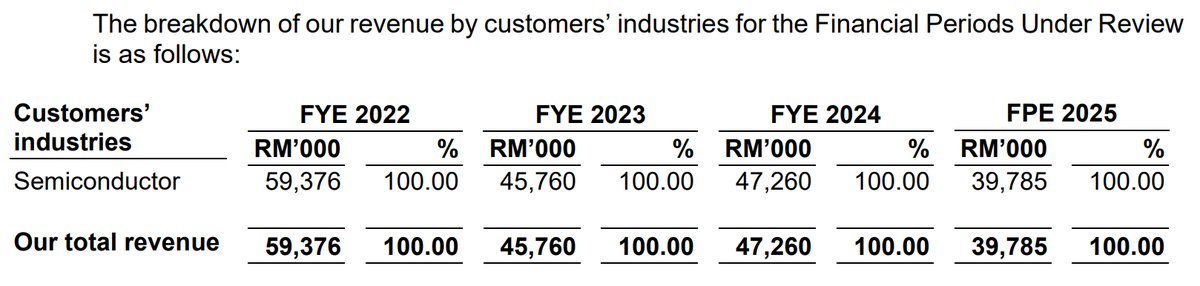

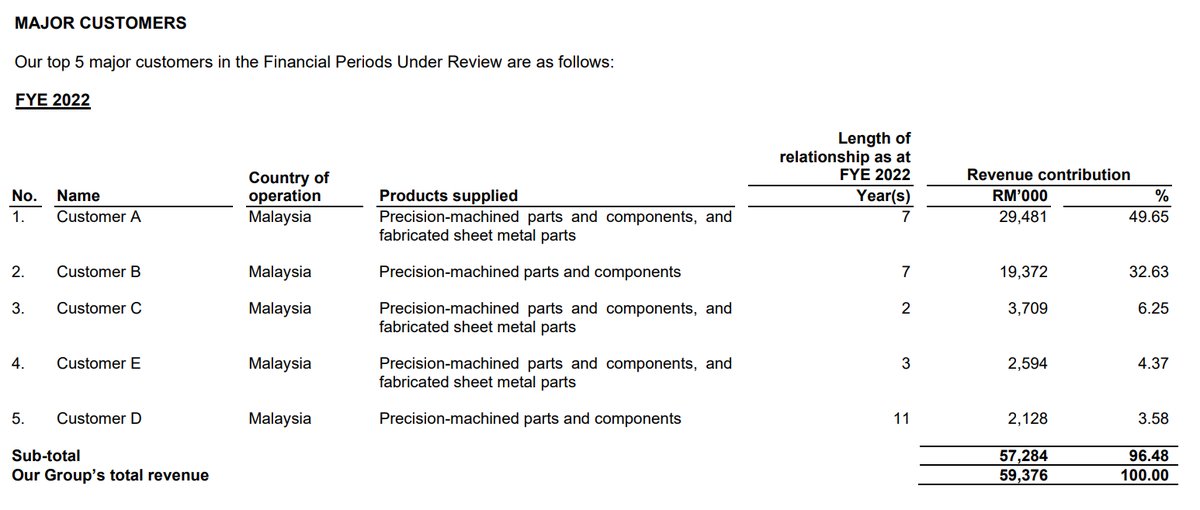

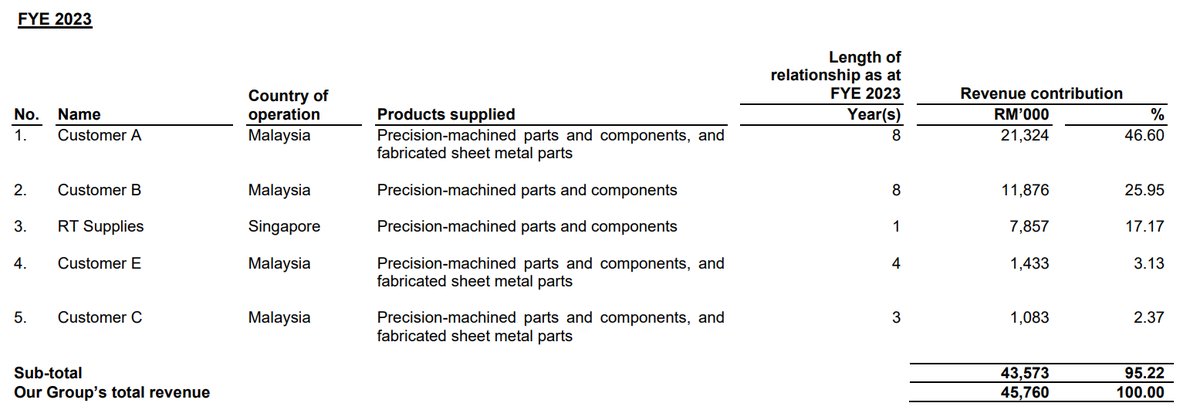

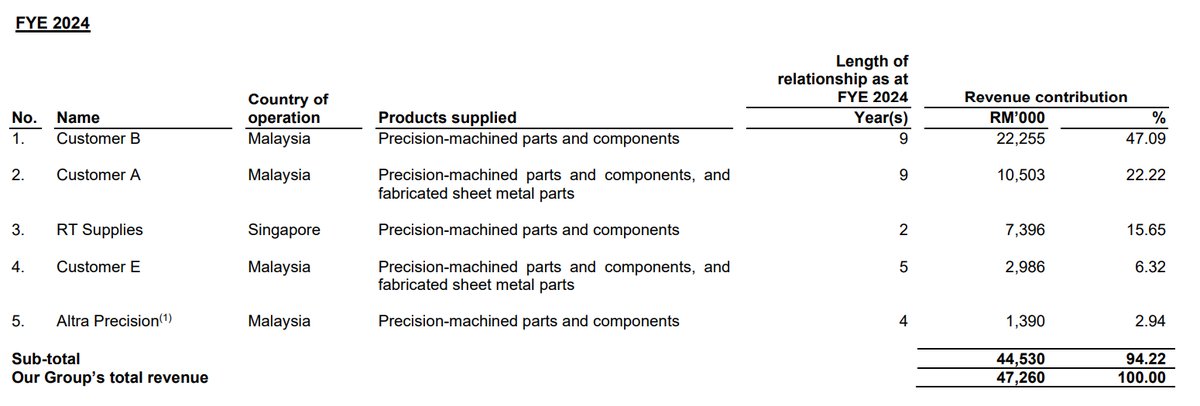

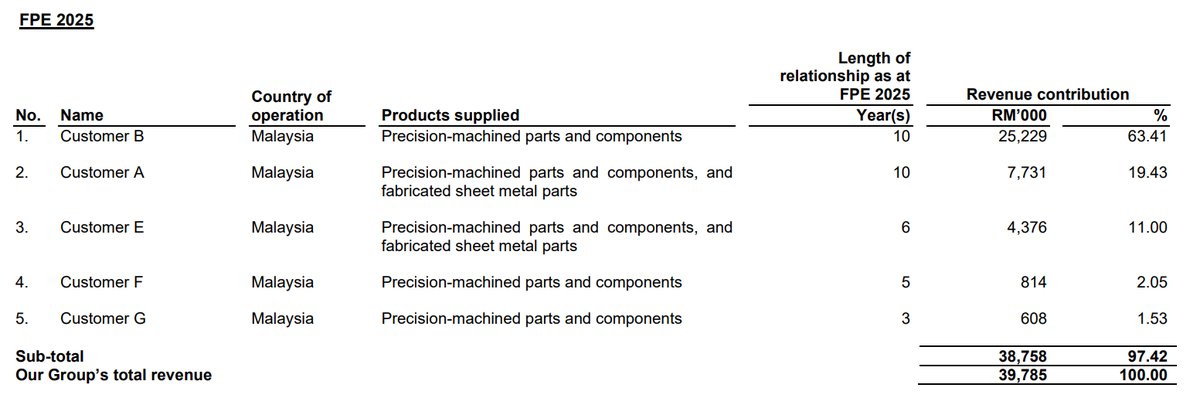

Major Customers

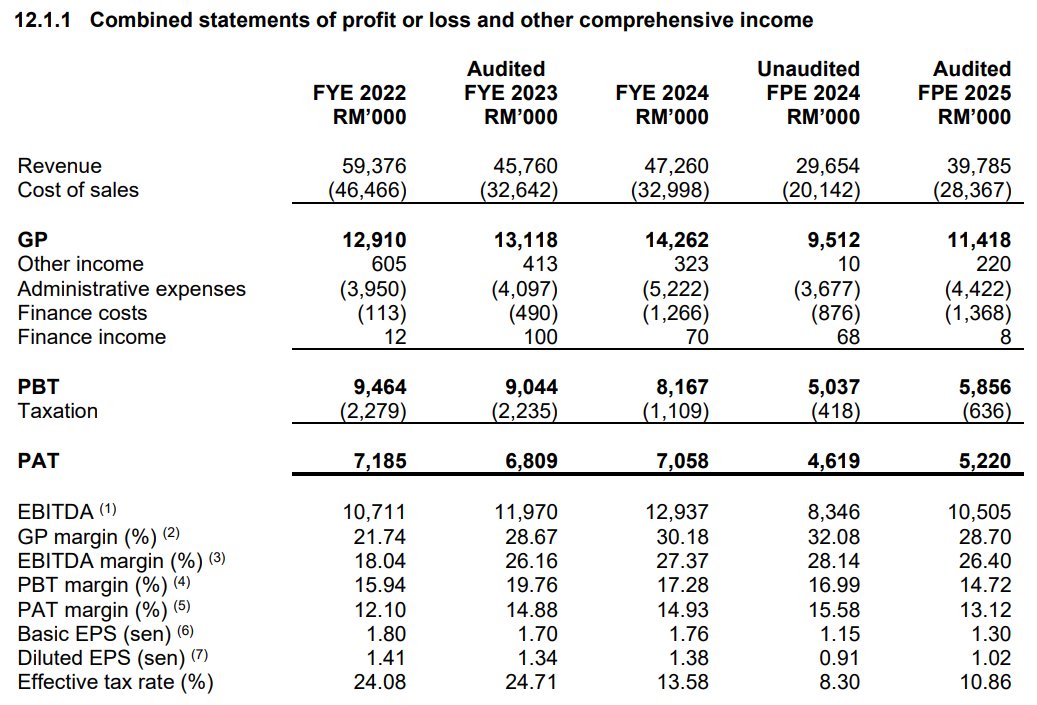

Revenue by Financial Year Ended

Profit After Tax (PAT) by Financial Year Ended

Revenue by Financial Period Ended

Profit After Tax (PAT) by Financial Period Ended

SWOT Analysis

Strengths

- Established Client Relationships: Maintains long-standing relationships of over 9 years with its two key customers, indicating a sticky and trusted business partnership.

- Improving Profitability: Despite stagnant revenue, the company has improved its Profit After Tax (PAT) margins from 12.1% in FY2022 to 14.9% in FY2024, suggesting better cost management.

- Niche Sector Expertise: Holds ISO 9001 and 14001 accreditations, specializing in precision machining and sheet metal fabrication for the high-specification semiconductor industry.

Weaknesses

- Extreme Customer Concentration: Critically dependent on a single client, Customer B, which accounted for 63.41% of revenue in FPE 2025. The top two customers make up 82.84% of total revenue.

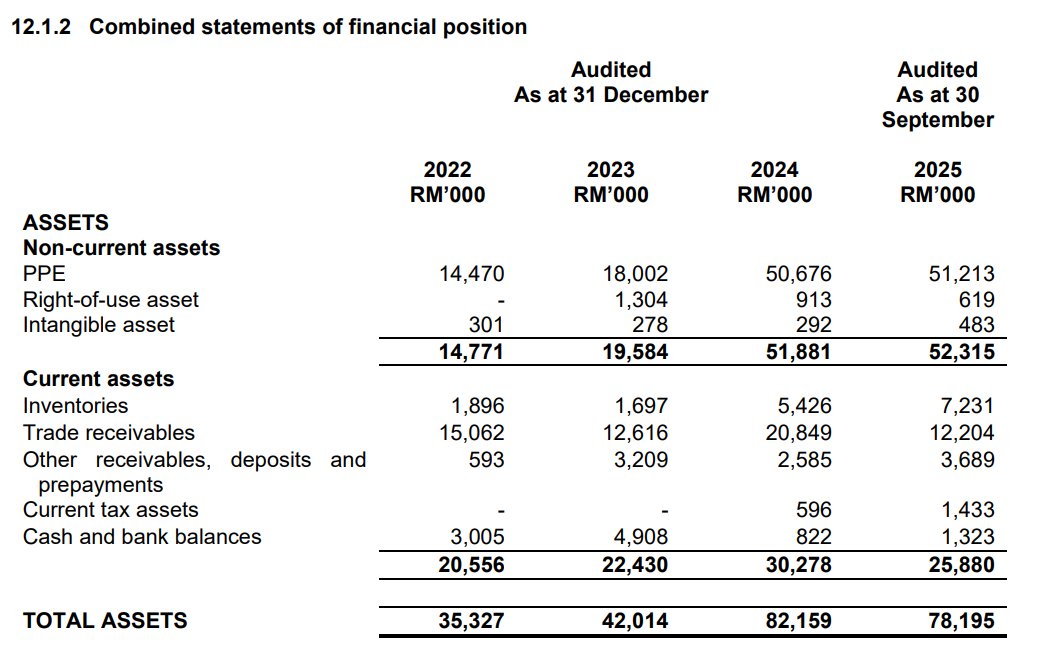

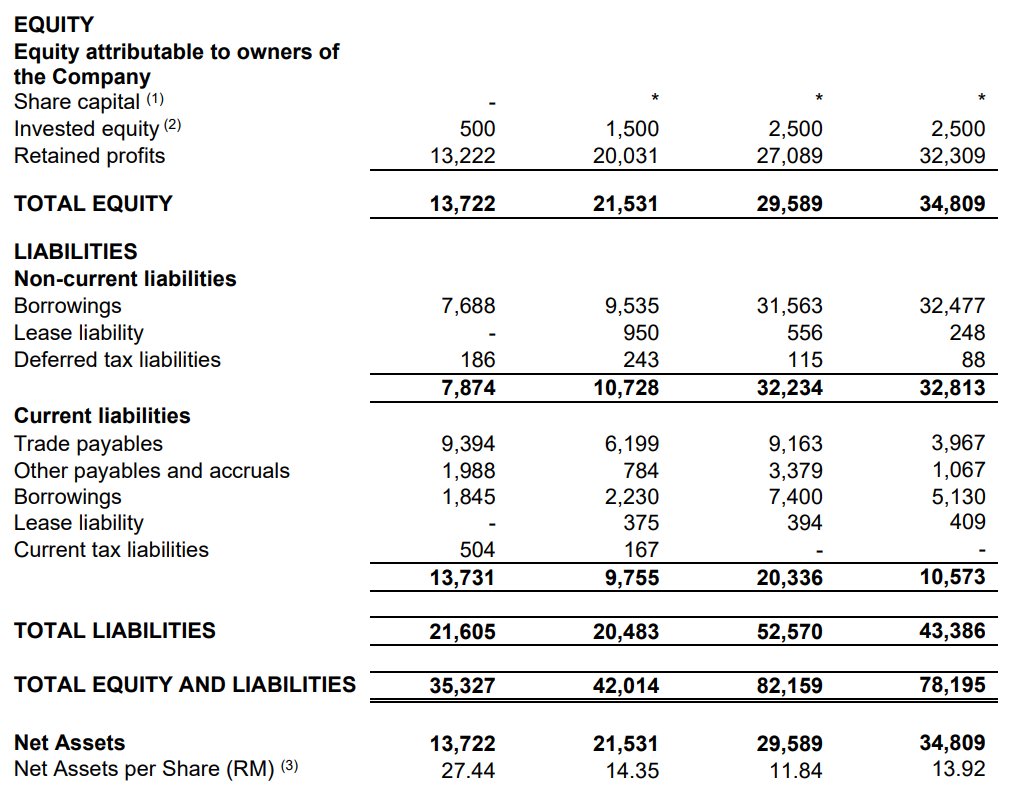

- High Financial Gearing: Operates with a high gearing ratio of 1.32x as of FY2024, indicating significant debt levels which constrain financial flexibility.

- Stagnant Revenue Growth: Revenue has declined from a peak of RM59.4 million in FY2022 to RM47.3 million in FY2024, showing a negative growth trend over the past three years.

Opportunities

- Enhanced Capabilities: The acquisition of Facility 42A and planned purchase of new 5-axis CNC machines could enhance its capacity and ability to produce more complex, higher-value parts.

- Semiconductor Cycle Recovery: A potential global recovery in the semiconductor industry in 2024/2025 could lead to an increase in order volumes from its existing and new customers.

- Potential Customer Diversification: New advanced machining capabilities could be leveraged to attract new clients and reduce its heavy reliance on its top two customers.

Threats

- Client Dependency Risk: Any reduction in orders or change in procurement strategy from its top two customers, particularly Customer B, would severely and immediately impact revenue and profitability.

- Raw Material Price Volatility: Exposed to fluctuations in the price of raw materials, especially aluminium, which constituted approximately 38% of its cost of materials.

- Intense Market Competition: Faces significant competition from larger, more diversified, and financially stronger peers in the precision engineering space such as Coraza and UWC.

Key Highlights

Sorry, this feature only available for iSaham Pro

Conclusion

Sorry, this feature only available for iSaham Pro

Ambest Group Berhad's Latest News